When unexpected expenses hit, payday loans can feel like your only option. We at Financial Canadian created this payday loans Canada guide to help you understand how they work, what they cost, and whether they’re right for your situation.

The reality is that payday loans come with steep fees and interest rates. Before you borrow, you need to know the actual numbers and explore better alternatives that might save you money.

How Payday Loans Actually Work

Payday loans in Canada operate on a simple but expensive premise: you borrow money against your next paycheck and repay it within two weeks or by your next payday. Most lenders cap loans between $300 and $1,500, though some provinces allow higher amounts. The application process is deliberately fast-you typically submit proof of income, a valid ID, and banking information online or in-store, and approval happens within hours or the same day. Lenders prioritize speed over thorough credit checks, which is why people with poor credit scores can qualify.

The True Cost of Borrowing

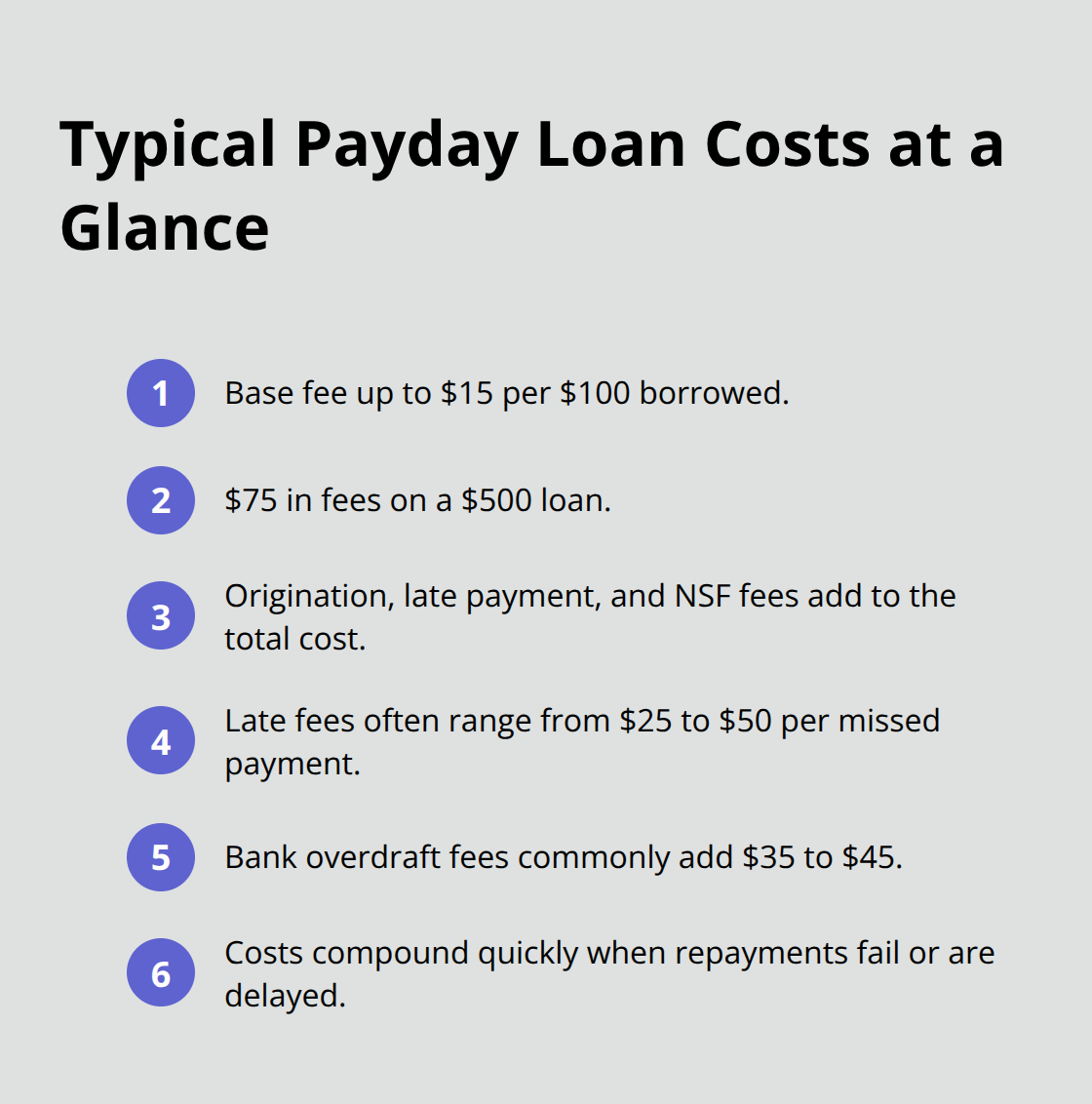

This speed comes at a price that catches many borrowers off guard. Canadian payday lenders charge up to $15 per $100 borrowed, which translates to an annual interest rate of 365 percent. On a $500 loan, you pay $75 in fees alone. Beyond the base fee, lenders add origination fees, late payment penalties, and NSF charges if your bank account lacks sufficient funds when they attempt to withdraw repayment.

These hidden costs compound quickly.

If you miss a single payment, late fees range from $25 to $50, and if the lender’s withdrawal triggers an overdraft, your bank adds another $35 to $45 in fees. The real trap emerges when you cannot repay on time. Most borrowers end up rolling over their loans, taking out new payday loans to cover the previous ones. This debt cycle is intentional by design-lenders profit when borrowers cannot repay, so the two-week term practically guarantees repeat borrowing.

The Debt Cycle Reality

Statistics show that payday loans can lead to chronic borrowing and leave borrowers trapped in a debt cycle, paying hundreds in fees for a few hundred dollars borrowed. The psychological impact matters too. Financial stress from payday loans correlates with anxiety, depression, and sleep problems according to research on debt-related stress. Payday loans are not a solution to cash flow problems; they are a Band-Aid that worsens the underlying wound.

What to Watch Before Signing

Predatory lenders exploit desperation by burying terms in fine print. Always verify that your lender is licensed in your province, as unlicensed operators work outside consumer protection laws entirely. Read the complete fee schedule before you agree to anything. Some lenders charge application fees, document fees, or verification fees that inflate the total cost.

Check whether your province caps interest rates. Ontario, for example, limits payday loans to $15 per $100 borrowed, while other provinces allow higher rates. Confirm the exact repayment date and whether you can repay early without penalty. Some lenders penalize early repayment, locking you into the full fee schedule. Understand that payday loans do not build credit history. Missed payments get reported to credit bureaus and can trigger collections, legal action, or wage garnishment, damaging your financial future far beyond the immediate debt.

Now that you understand how payday loans work and what they cost, the next question becomes whether they make sense for your situation at all.

Should You Actually Use a Payday Loan

When Payday Loans Make Sense

Payday loans make sense in exactly one scenario: you face a genuine emergency that costs money you do not have, repayment arrives with your next paycheck within two weeks, and you have exhausted every other option. A burst water pipe, an urgent car repair needed to get to work, or a medical bill you cannot delay might qualify. The key word is exhausted. Most people turn to payday loans without actually exploring alternatives, which is a costly mistake.

Better Alternatives That Save You Money

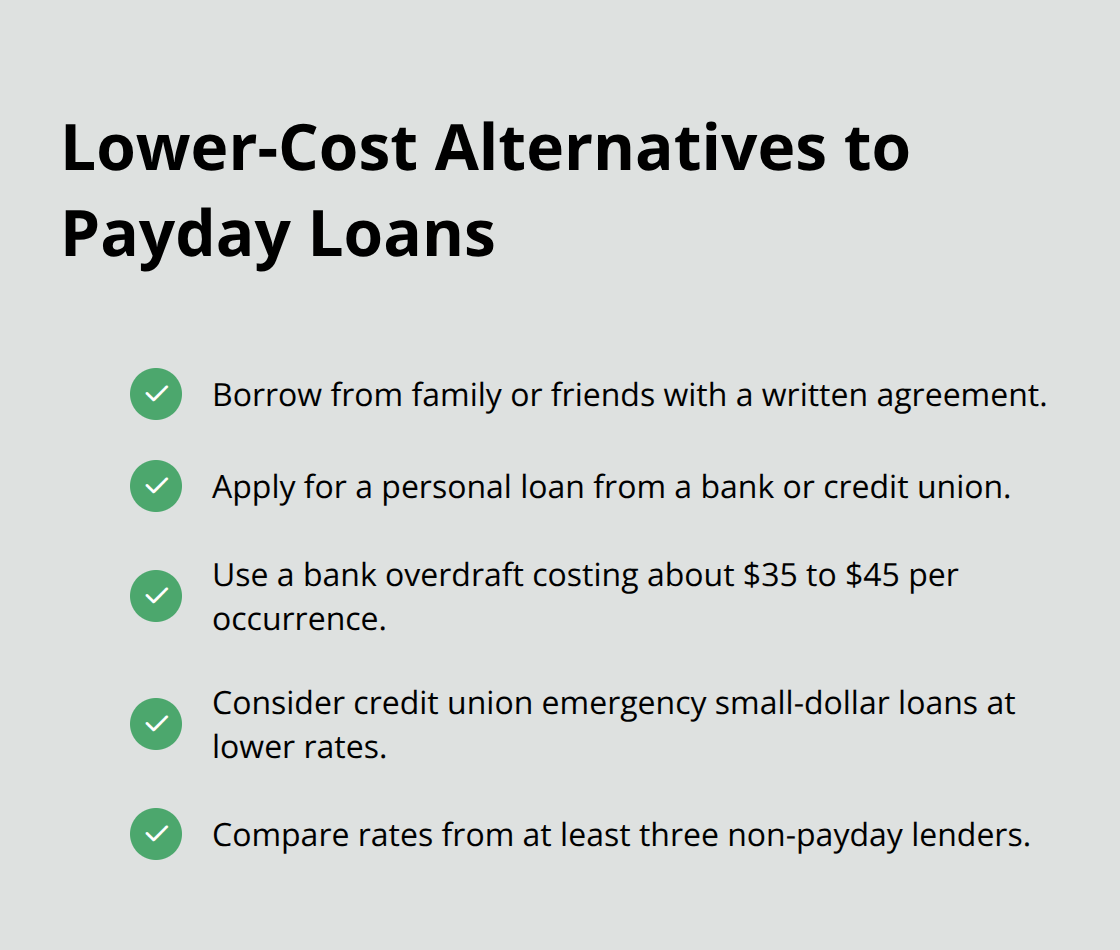

If you can borrow from family or friends with a written repayment agreement, that saves you hundreds in fees. A personal loan from your bank or credit union typically charges interest instead of the 365 percent rate payday lenders charge. Even a bank overdraft, which costs around $35 to $45 per occurrence, beats paying $75 in fees on a $500 payday loan. Credit unions in Canada often offer emergency small-dollar loans at rates far below payday lenders, and many do not require perfect credit. Before you apply for a payday loan, contact three lenders outside the payday industry and compare their rates.

When Payday Loans Become Actively Harmful

The situations where payday loans become actively harmful are when you borrow to cover recurring expenses, when you lack a concrete plan to repay within two weeks, or when you already carry other debt. If you need cash because your rent or groceries exceed your income, a payday loan does not solve the problem; it delays it and adds expense. Payday borrowers roll over their loans an average of eight times per year, meaning they pay thousands in fees for the privilege of staying broke. Do not use a payday loan to cover credit card payments, other loan repayments, or lifestyle spending.

Breaking Free Without Payday Loans

If you cannot repay within fourteen days without borrowing again, the loan will trap you. Side gigs like food delivery, freelance writing, or task services can generate $200 to $500 monthly and eliminate the need to borrow at all. A licensed insolvency trustee offers free consultations to assess whether debt consolidation, a consumer proposal, or bankruptcy protection makes more sense than accumulating payday debt. Contact one before you commit to a payday loan, especially if you already carry existing debts. Understanding your actual options puts you in control of your financial future rather than at the mercy of lenders who profit from your desperation.

Regulations and Protections for Canadian Borrowers

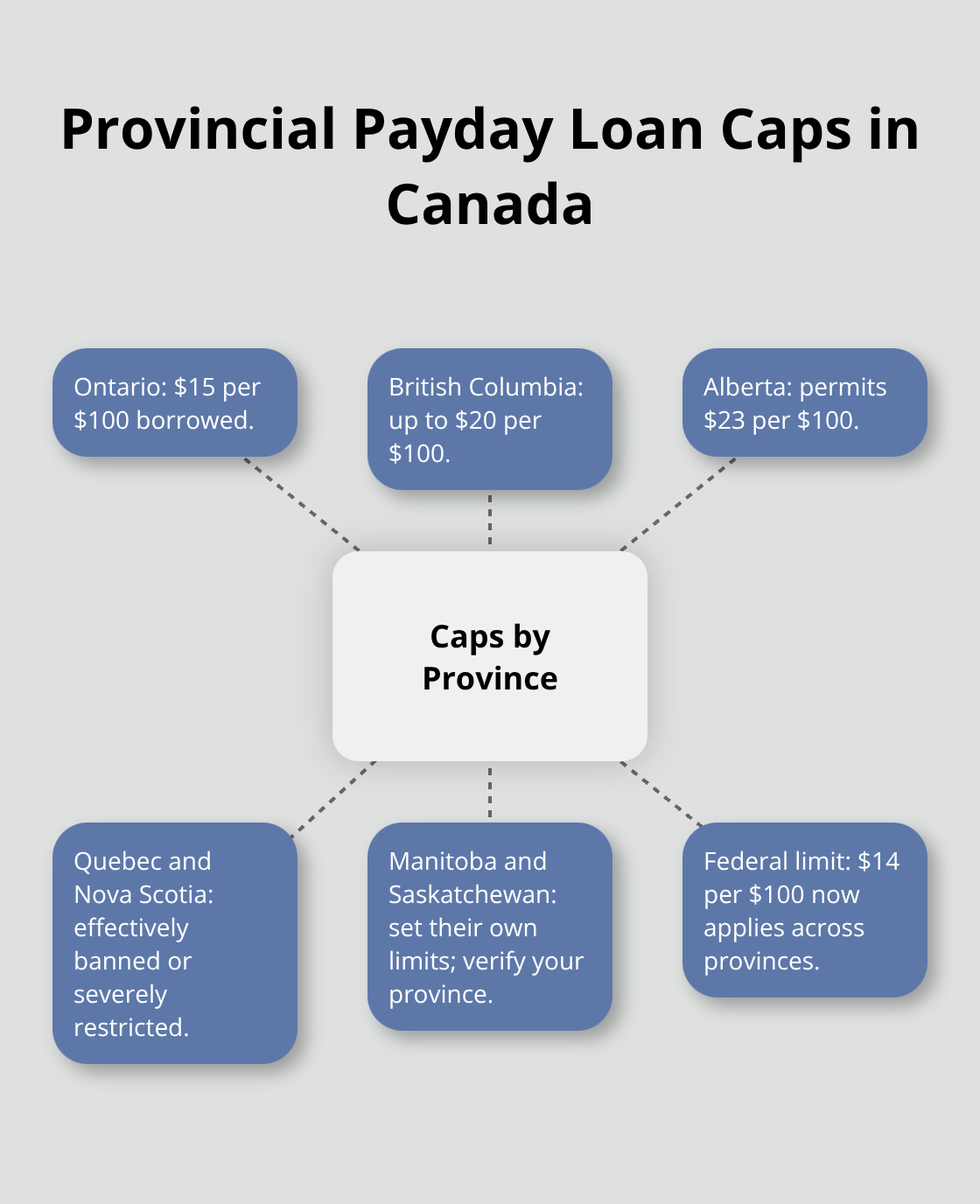

Canada’s payday loan regulations differ drastically by province, which means your protection depends entirely on where you live. Ontario caps rates at $15 per $100 borrowed, while British Columbia allows up to $20 per $100, and Alberta permits $23 per $100. Manitoba and Saskatchewan set their own limits, but several provinces including Quebec and Nova Scotia have effectively banned payday lending or restricted it severely.

This fragmentation creates a serious problem: if you live in a province with weak regulations, you face significantly higher costs than borrowers across provincial borders. Check your specific province’s cap before signing anything, because lenders will charge whatever the law allows in your jurisdiction. A federal limit of $14 per $100 borrowed now applies across all provinces, so verify the exact ceiling before you commit.

What Provincial Consumer Protection Laws Require

Beyond interest rate caps, provincial consumer protection laws typically require lenders to disclose the total cost in writing before you borrow, prohibit lenders from rolling over loans automatically, and mandate clear repayment schedules. However, these protections only work if you read the disclosure documents completely. Many borrowers sign without reviewing the fine print, which means they miss important details about when payments are due and what happens if they cannot pay. Some provinces require lenders to offer a cooling-off period where you can cancel the loan within a short window, usually two business days, without penalty. Alberta and Ontario have this protection, but others do not. Your province’s consumer protection act spells this out explicitly, so contact your provincial consumer protection office before borrowing.

Why Unlicensed Lenders Pose Real Danger

Unlicensed payday lenders operate outside these protections entirely, which is why verifying your lender’s license with your province’s financial regulator is non-negotiable. Borrowing from an unlicensed operator means you have virtually no legal recourse if the lender charges excessive fees, violates repayment terms, or engages in aggressive collection practices. Licensed lenders know the rules and follow them because violations cost them their licenses. Unlicensed operators have nothing to lose, which is why they operate with impunity in some regions.

How Predatory Tactics Exploit Regulatory Gaps

Regulations exist, but predatory lenders exploit gray areas constantly. Some lenders pressure you to take larger loans than you need, knowing you will struggle to repay and roll over the debt multiple times. Others use aggressive collection methods including repeated calls to your employer, threats of legal action, or demands for post-dated cheques that lock you into repayment regardless of your circumstances. If a lender threatens wage garnishment, legal action, or criminal charges before exhausting proper collection procedures, they violate consumer protection laws in every Canadian province. Document these interactions and report them to your provincial regulator immediately.

Final Thoughts

Payday loans in Canada offer speed when you need cash fast, but that speed comes with a financial cost most borrowers underestimate. You pay $15 per $100 borrowed, fees compound when you miss payments, and the two-week repayment cycle traps most people into rolling over their debt repeatedly. If you borrow $500, you could easily pay $200 or more in fees within a year through repeated rollovers, and that money disappears into lender profits instead of building your financial stability.

Better options exist in nearly every situation covered in this payday loans Canada guide. A personal loan from your bank or credit union charges a fraction of payday rates, and borrowing from family with a written agreement costs nothing. A licensed insolvency trustee offers free consultations to explore debt consolidation or consumer proposals if you already carry existing debts, and these alternatives require slightly more effort than applying online for a payday loan, but the savings justify that effort completely.

Your path forward depends on addressing the underlying problem, not masking it with expensive short-term debt. If you earn too little, side gigs generate additional income without borrowing; if expenses exceed income, budgeting and expense tracking reveal where money actually goes; if unexpected emergencies drain your savings, building an emergency fund prevents future payday borrowing. Contact your provincial consumer protection office, verify your lender’s license, and explore alternatives before you apply for a payday loan.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment