When unexpected expenses hit, waiting weeks for a loan approval isn’t an option. Instant personal loans in Canada offer a faster path to the funds you need, with some lenders approving applications within hours.

At Financial Canadian, we’ve put together this guide to help you understand how these loans work, what options are available, and what to watch out for before you borrow.

How Instant Personal Loans Work in Canada

Most lenders in Canada complete the entire approval process within 24 hours, though some online platforms approve applications in as little as one to three hours. The speed depends heavily on how quickly you submit your documentation and whether you apply during business hours. Online lenders typically move faster than traditional banks because they automate much of the underwriting process.

The Pre-Qualification and Credit Check Process

When you apply, lenders conduct a soft credit pull first, which doesn’t damage your credit score, to give you an indicative rate. This pre-qualification step takes minutes and lets you see what you might qualify for before committing to a full application. The hard credit pull comes later, after you decide to proceed, and this does show on your credit report.

You’ll need to provide recent pay stubs, two pieces of ID, and proof of income or employment. Some lenders also ask for bank statements to verify your income stability and assess your ability to repay. If you apply on a Friday evening, don’t expect funding until the following Monday at earliest, since most lenders don’t process transfers on weekends.

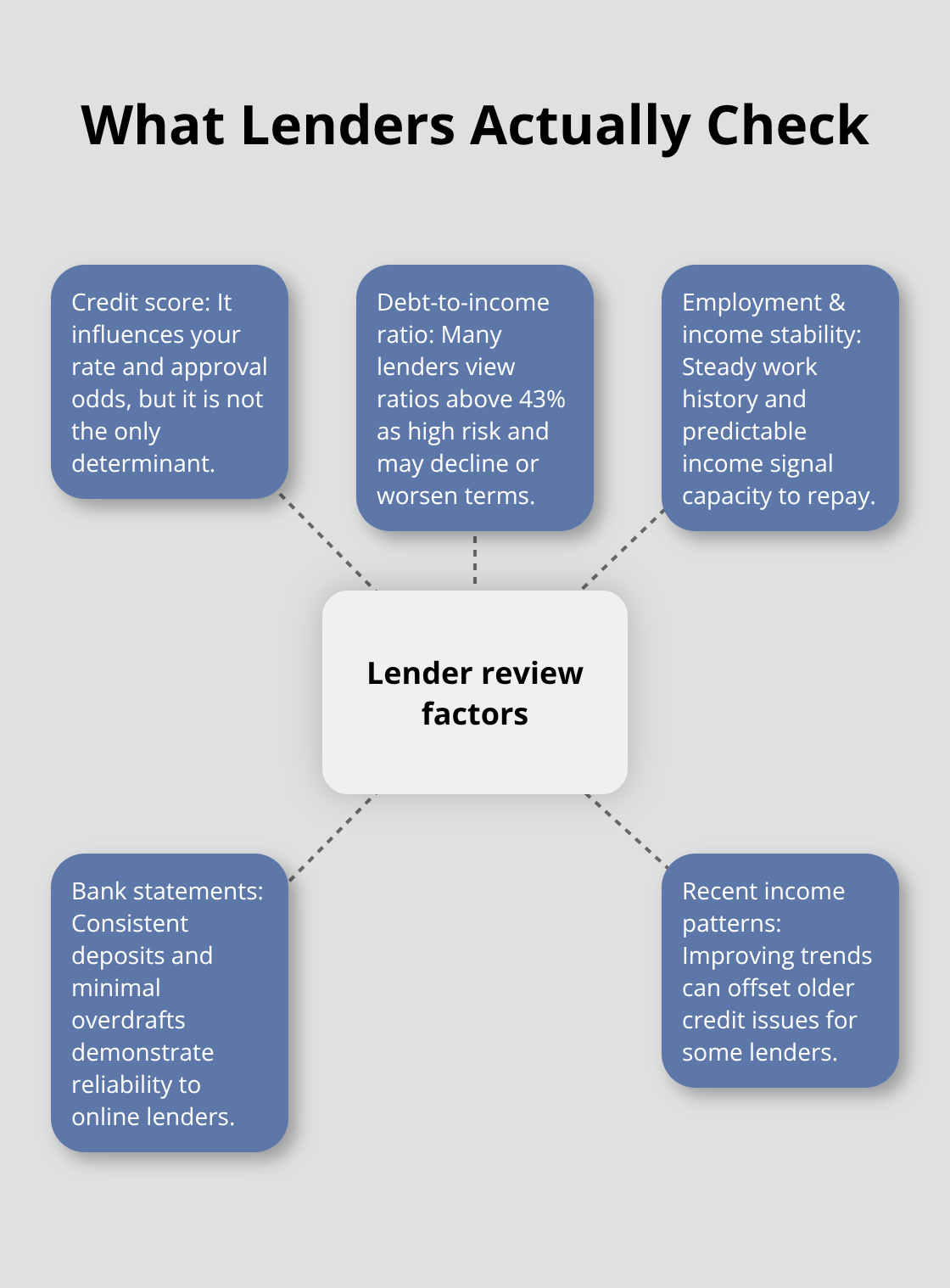

What Lenders Actually Check

Your credit score matters, but it’s not the only factor. Lenders examine your debt-to-income ratio, a percentage that evaluates your debt compared to your gross income. If this ratio exceeds 43%, many lenders will decline your application or offer less favorable terms.

Your employment status and income stability carry significant weight, especially for online lenders who can’t rely on traditional banking relationships. A bank statement showing consistent deposits and low overdraft activity signals financial reliability. Some lenders focus more on recent income patterns than overall credit history, which can work in your favor if you’ve had credit problems but have improved your finances recently.

Provincial regulations also matter. In some provinces, lenders must be licensed, and interest rates may be capped. Verify that any lender you’re considering is properly registered with your provincial financial regulator before applying.

How Funding Reaches Your Account

Once approved, funding speed depends on the lender and the time of day you’re approved. Many online lenders deposit funds directly into your bank account within 24 hours, though some advertise same-day funding if you apply early enough on a business day.

You’ll need to provide your banking details during the application, and the lender will set up direct deposit for disbursement. The lender also uses this account for automatic withdrawals on your repayment date, so make sure you have sufficient funds available when payments are due. If you miss a payment or don’t have enough money in your account, the lender may attempt withdrawal twice, potentially triggering NSF fees from your bank.

Set up automatic payments from your account to avoid this situation entirely. Some lenders offer flexibility by allowing you to adjust payment dates, though this typically extends the loan term and increases total interest paid. Understanding these mechanics helps you avoid costly mistakes-but the real decision comes down to which type of loan actually fits your situation.

Types of Instant Personal Loans Available

Why Payday Loans Trap You in Debt

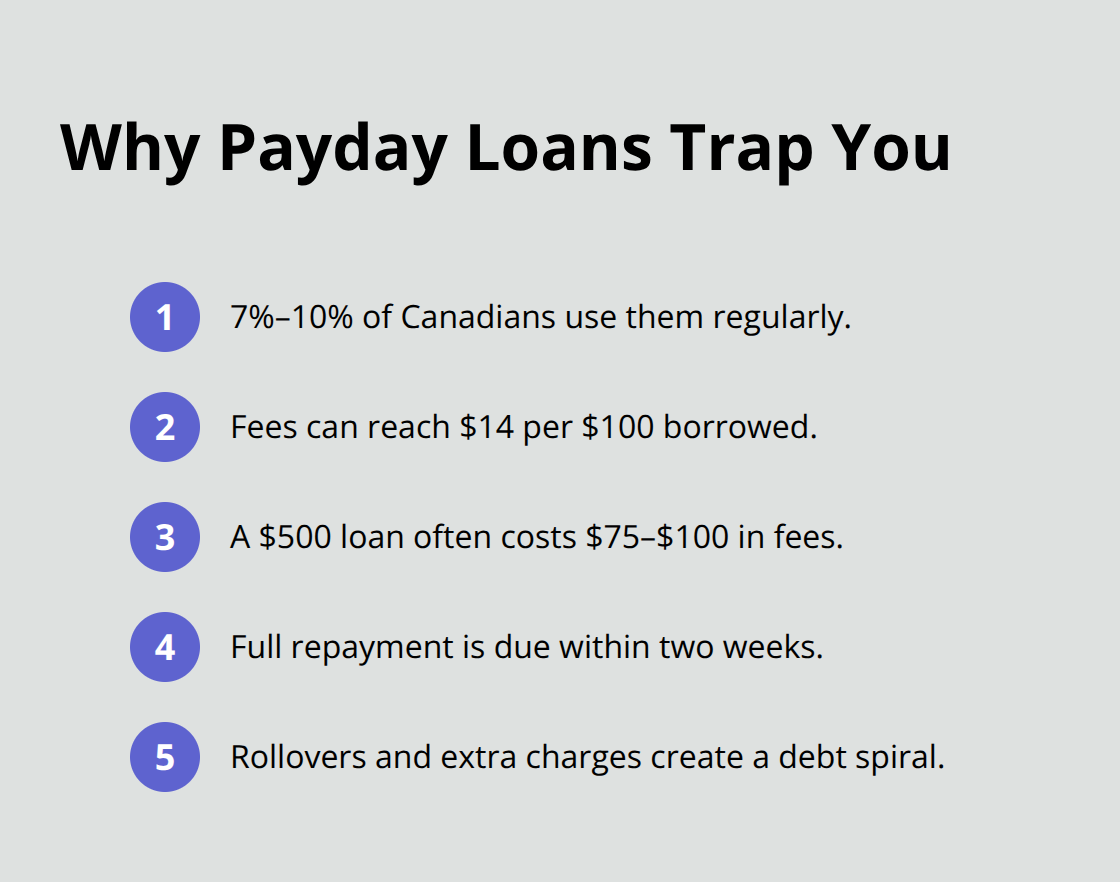

Payday loans in Canada dominate the quick-cash market, with 7% to 10% of Canadians using them regularly. These loans carry brutal economics: upfront fees combined with interest rates that can reach $14 per $100 borrowed. A typical payday loan of $500 costs you $75 to $100 in fees alone, due within two weeks. If you can’t repay on time, lenders add extra interest or charges, creating a debt spiral that’s hard to escape.

The ease of access makes this worse. You apply online, get approved in minutes, and suddenly you’re trapped in a cycle where one payday loan leads directly to another. Payday lenders don’t participate in voluntary debt management plans, meaning if you get stuck, your only real options are bankruptcy or a Consumer Proposal through a Licensed Insolvency Trustee. This is why payday loans should be your absolute last resort, not your first choice.

Online Lenders Offer Speed Without the Debt Trap

Online lenders and traditional banks offer genuinely faster alternatives that won’t destroy your finances. Online platforms like Mogo, Money Express, and LendingPoint approve applications within hours and fund accounts within 24 hours, sometimes same-day if you apply early on a business day. These lenders care about your bank statements and income stability as much as your credit score, which matters if you’ve had recent credit problems but have cleaned up your finances.

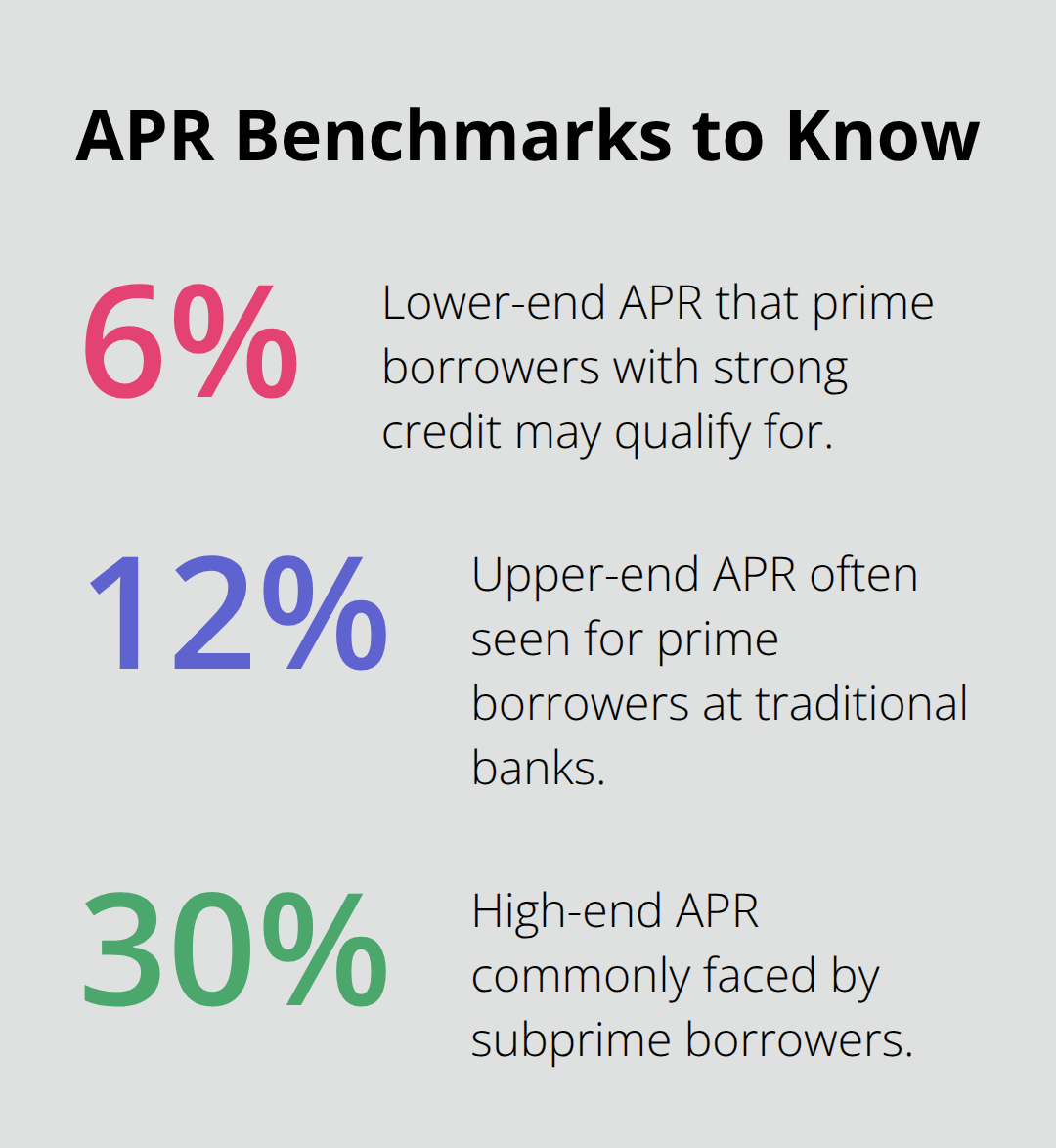

Traditional banks moved slowly for decades, but major Canadian banks now offer fast-track personal loans with approval timelines measured in hours rather than weeks. The APR you’ll pay depends on your creditworthiness-prime borrowers with good credit typically qualify for rates between 6% and 12%, while subprime borrowers pay 15% to 30% or higher.

Lines of Credit Provide Flexibility When You’re Uncertain

A line of credit from your bank works differently: you access funds only when needed and pay interest only on what you use, making it ideal if you’re unsure about the exact amount you need. This flexibility costs slightly higher interest rates than fixed-term loans, but you avoid paying interest on borrowed money sitting unused in your account.

Compare multiple lenders across banks, credit unions, and online platforms before committing-the difference between a 10% APR and a 25% APR on a $5,000 loan over three years costs you roughly $2,000 more in interest. Check that any lender is licensed with your provincial financial regulator, since some provinces cap interest rates and require proper licensing. The practical reality is that online lenders move fastest for most people, traditional banks offer the best rates if you have strong credit, and lines of credit provide flexibility when your exact borrowing need isn’t clear. Your next decision involves understanding what these lenders actually examine when they assess your application.

Key Factors to Consider Before Borrowing

The interest rate you see advertised is only part of the story. When you borrow $5,000 at 15% APR over three years, you’ll pay roughly $1,186 in interest alone, but that’s before origination fees, service charges, or prepayment penalties enter the equation. Online lenders typically charge origination fees between 1% and 8% of your loan amount, meaning a $5,000 loan could cost you $50 to $400 just to get approved. Some lenders also charge monthly service fees or late payment penalties that can exceed $50 per occurrence.

Calculate the total repayment cost by adding the principal, all interest, and every fee mentioned in the loan agreement. A loan with a slightly higher interest rate but no origination fee often costs less than a cheaper-looking rate buried under hidden charges. The difference between a 10% APR and a 25% APR on a $5,000 loan over three years costs you roughly $2,000 more in interest, which is significant enough to justify spending an hour comparing offers.

How Repayment Terms Affect Your Total Cost

Fixed-term installment loans lock in monthly payments, which simplifies budgeting but limits flexibility. Shorter terms reduce total interest paid but increase your monthly burden, so a two-year repayment period costs less than a five-year term but demands higher monthly payments. If you’re already stretched financially, the lower monthly payment of a longer-term loan might prevent missed payments that damage your credit score and trigger default fees.

Lines of credit offer the opposite trade-off: you pay interest only on what you use, but the interest rate typically runs 2% to 5% higher than fixed-term loans. Some lenders allow you to adjust payment dates, but this extends your loan term and increases total interest paid, so use this flexibility sparingly. Match your repayment capacity to the loan structure, not just the lowest advertised rate.

Verify Lender Legitimacy Before You Apply

A lender’s reputation reveals whether you’ll face honest terms or predatory practices. Verify lender legitimacy by checking provincial financial regulator licensing, since unlicensed operators often hide behind aggressive marketing and buried fees. Read customer reviews on independent sites like Trustpilot or the Better Business Bureau, focusing on complaints about hidden fees, delayed funding, or aggressive collection practices.

If multiple reviews mention NSF fees or unexpected charges, that lender prioritizes aggressive collection over customer service. Contact the lender’s customer service team with a specific question before applying, and gauge how quickly and clearly they respond. Lenders that avoid straightforward answers about fees or terms usually have something to hide. Provincial regulations matter too, since some provinces cap interest rates or require specific disclosures. Verify that the lender operates legally in your province before entering any agreement.

Final Thoughts

Instant personal loans in Canada require you to match your urgent need with the right lender structure. Payday loans move fastest but cost the most, trapping borrowers in cycles of debt that often require bankruptcy or a Consumer Proposal to escape. Online lenders like Mogo and Money Express offer genuine speed without predatory pricing, approving applications within hours and funding accounts within 24 hours, while traditional banks now compete on speed too, though their approval timelines depend on your credit profile.

Your choice hinges on three concrete factors. First, compare total repayment costs across lenders, not just advertised rates-a $5,000 loan at 10% APR costs roughly $2,000 less in interest over three years than the same loan at 25% APR. Second, verify that any lender holds licensing with your provincial financial regulator and check independent reviews on Trustpilot or the Better Business Bureau for complaints about hidden fees or aggressive collection practices. Third, match the repayment structure to your cash flow, since a longer-term loan prevents missed payments that damage your credit score, even if it costs more in total interest.

Start by obtaining pre-qualification with multiple lenders using soft credit pulls, which take minutes and don’t affect your credit score. Gather your recent pay stubs, two pieces of ID, and bank statements showing income stability, then apply during business hours on a weekday to maximize your chances of same-day or next-day funding. We at Financial Canadian provide comprehensive resources to help you navigate financial decisions with confidence and choose the loan that costs the least over its full term, not the one with the lowest advertised rate.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment