Mortgage rates in Canada hit a 23-year high in 2023, leaving many homebuyers scrambling for affordable mortgage options Canada that fit their budget. The good news is that you have more choices than ever before.

At Financial Canadian, we’ve put together this guide to help you navigate fixed-rate mortgages, variable-rate options, and government programs designed for first-time buyers. Whether you’re working with a traditional bank or exploring alternative lenders, we’ll show you how to find the right fit for your financial situation.

Your Mortgage Rate Options Today

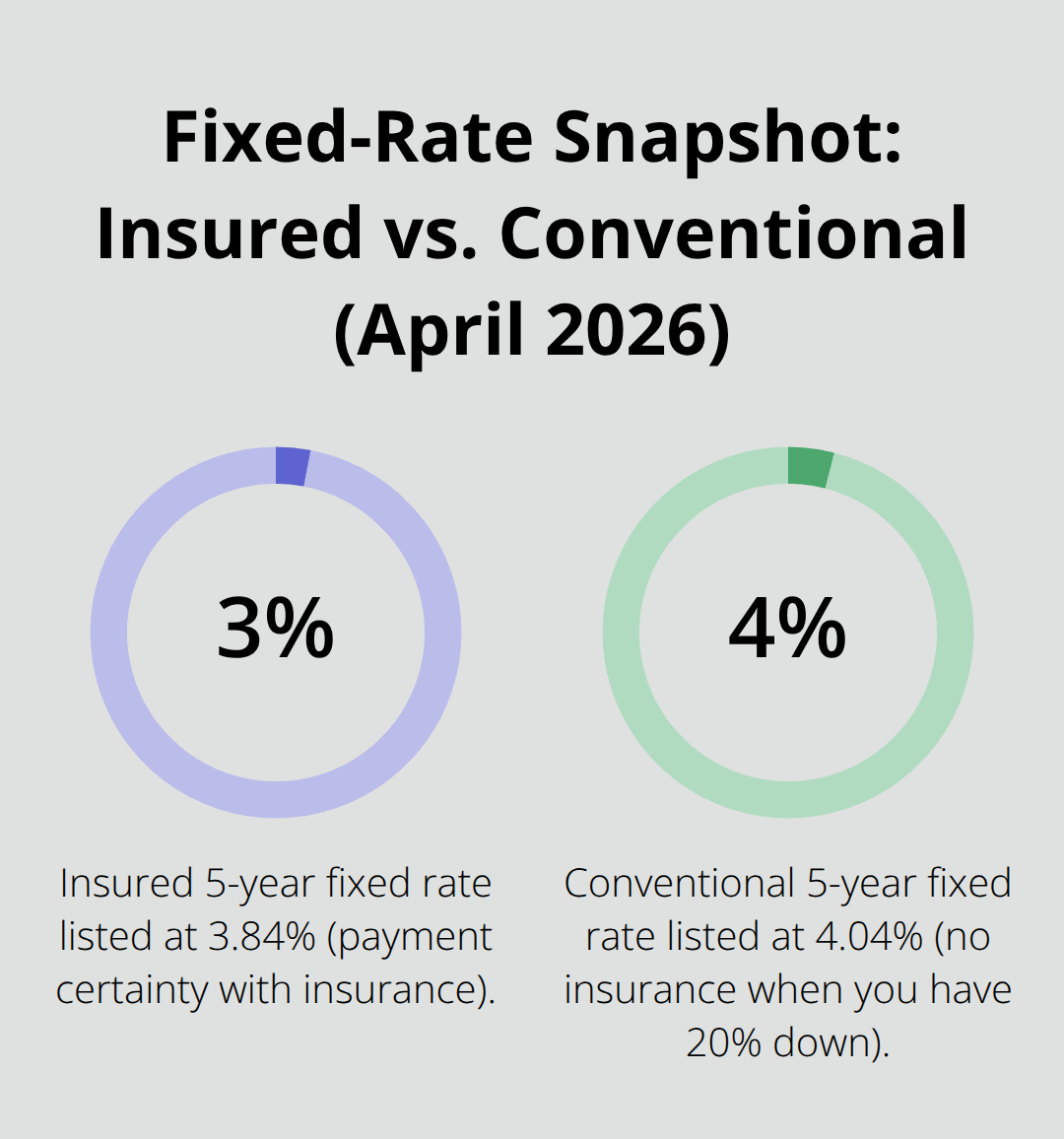

Fixed-rate mortgages lock in a single interest rate for your entire term, protecting you from rate increases. As of April 2026, insured 5-year fixed rates sit around 3.84%, while conventional 5-year fixed rates hover near 4.04% according to current market data. You pay a slightly higher rate than variable options in exchange for payment certainty. This matters most when you budget tight or when rates are climbing. If you believe rates will spike, a fixed rate eliminates guessing games.

The downside appears when rates fall during your term-you remain locked into the higher rate until renewal. Most Canadians choose 5-year terms because they balance stability with reasonable pricing, though terms range from 6 months to 10 years depending on your lender.

When Variable Rates Win

Variable-rate mortgages track the Bank of Canada’s prime rate, currently at 4.45%, and your payment adjusts as prime moves. Insured 5-year variable rates currently sit around 3.30%, while conventional options reach 3.40%-meaningfully lower than fixed counterparts. You save real money if rates stay flat or drop further. However, rising rates mean your payment climbs, sometimes substantially. Variable mortgages work best when you have income cushion to absorb payment increases and confidence that rates will decline or remain stable. Many borrowers use variable rates during economic uncertainty when the Bank of Canada cuts rates, then lock into a fixed rate before the next hiking cycle begins.

Government Programs That Lower Your Cost

The First-Time Home Buyer Incentive provides a shared-equity loan covering 5% or 10% of your purchase price, reducing the down payment you need from your own pocket. You repay it when you sell or after 25 years, whichever comes first. This program works alongside insured mortgages to improve affordability without requiring you to reach the traditional 20% down threshold. First-time buyers can also withdraw up to $35,000 tax-free from an RRSP through the Home Buyers’ Plan, effectively creating additional down payment funds. The recent mortgage rule changes in December 2024 raised the insured mortgage price cap to $1.5 million and extended amortization to 30 years for eligible first-time buyers and new builds, lowering monthly payments substantially. For homes between $500,000 and $1.5 million, you now put 5% down on the first $500,000 and 10% on the remainder rather than facing a 20% requirement on the full amount. These changes directly expand who qualifies for insured financing and how much home you can afford.

How to Choose Between Fixed and Variable

Your choice between fixed and variable depends on your risk tolerance and income stability. If rate volatility keeps you up at night, fixed rates provide peace of mind despite their higher starting cost. If you can weather payment increases and expect rates to fall, variable rates offer substantial savings. Test both scenarios with your lender or broker-run the numbers at different rate levels to see which option fits your budget comfortably. Your comfort with uncertainty matters as much as the math.

Next Steps: Comparing Lenders and Programs

Now that you understand your rate options, the real work begins. You need to compare how different lenders price these mortgages and which programs you actually qualify for. Traditional banks, alternative lenders, and mortgage brokers all offer different access to rates and programs, and the difference in your final cost can reach thousands of dollars.

Comparing Mortgage Rates and Terms That Actually Matter

Look Beyond the Headline Interest Rate

Comparing mortgages means looking beyond the headline interest rate. Lenders publish different numbers in different ways, making side-by-side comparison difficult without a clear framework. The interest rate itself only tells half the story. A 5-year insured fixed rate of 3.84% sounds attractive until you learn that the mortgage default insurance premium depends on a number of factors including your down payment size. That premium wraps into your mortgage and you pay it over 25 or 30 years, increasing your total borrowing cost substantially. When comparing two lenders, request the same mortgage scenario from each one, then calculate your total monthly payment including the insurance premium if applicable. A rate that looks lower often disappears when premiums and fees are factored in.

Conventional mortgages at 4.04% for a 5-year fixed term avoid insurance entirely if you have 20% down, making them genuinely cheaper for borrowers who can reach that threshold. The real comparison happens when you see the full amortization schedule and total interest paid over the life of the loan, not just the rate number alone.

How Amortization Length Controls Your Budget

Amortization length directly controls your monthly payment and total cost. A standard 25-year amortization is the Canadian norm, but the recent mortgage rule changes allow first-time buyers and new-build purchasers to extend to 30 years on insured mortgages. That extra five years lowers your monthly payment by roughly 15% to 20%, which matters when you’re tight on cash flow. However, you pay significantly more total interest over time. Someone borrowing $400,000 at 4% over 25 years pays approximately $233,000 in interest; stretching that same loan to 30 years increases total interest to roughly $279,000.

The choice between 25 and 30 years isn’t theoretical-it determines whether you qualify for a mortgage at all. If a lender stress-tests your application and you barely qualify at 25 years, moving to 30 years creates breathing room in your monthly budget.

Prepayment Flexibility and Mortgage Penalties

Prepayment flexibility matters equally. Some mortgages allow you to pay extra toward principal without penalty; others lock you in completely. If you expect a bonus or inheritance, confirm your mortgage permits lump-sum payments. Closed mortgages typically offer lower rates in exchange for payment restrictions, while open mortgages cost more but let you pay off early. The penalty for breaking a closed mortgage early can reach thousands of dollars, so understand this commitment before signing.

Test your specific scenario with numbers from your lender-not general assumptions. Your mortgage broker or lender can model different amortization lengths, prepayment options, and rate scenarios to show you exactly how each choice affects your monthly payment and total cost. This analysis reveals which lender actually offers the best deal for your situation, not just the lowest advertised rate.

Where to Find Your Best Mortgage Rate

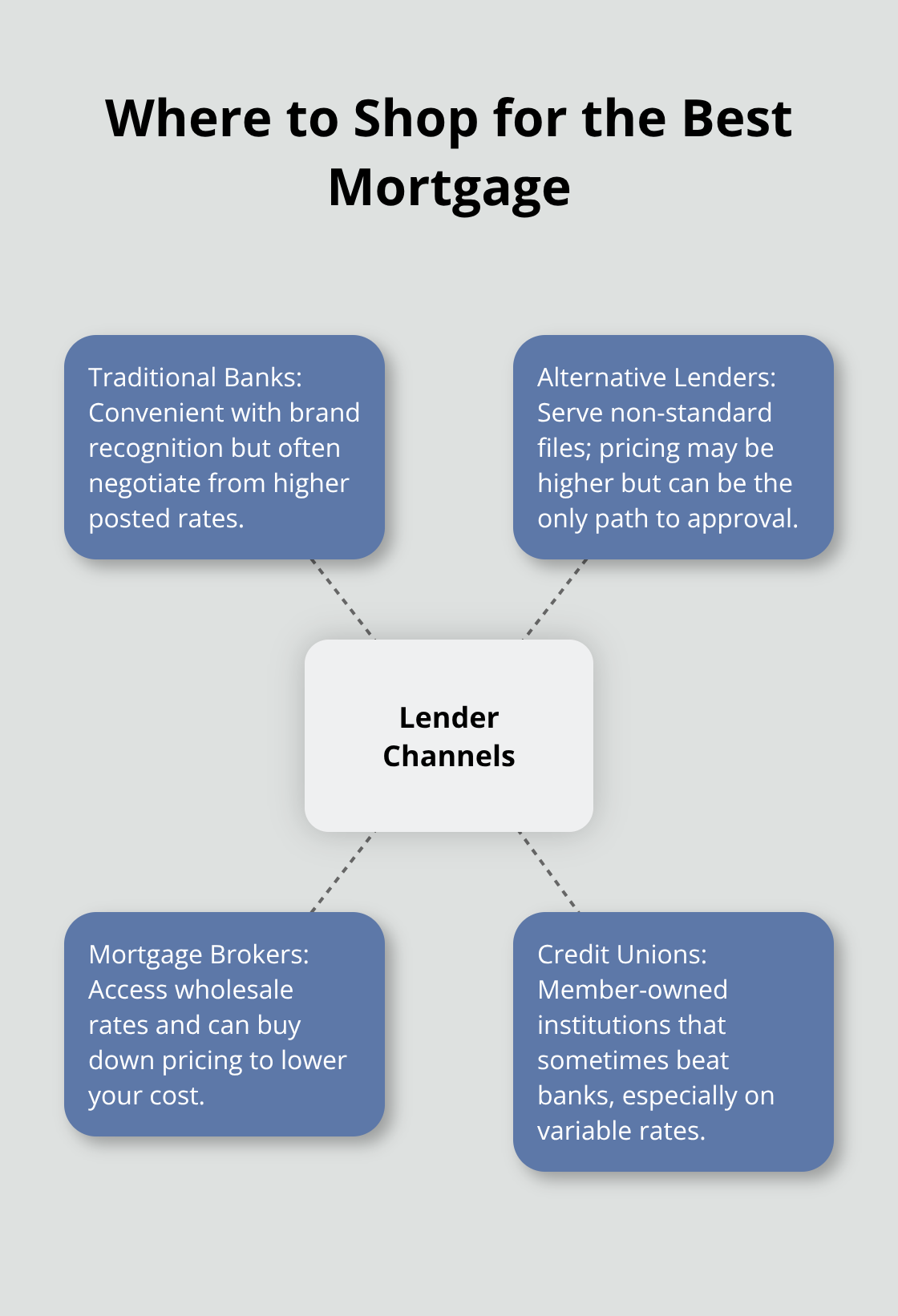

Choosing a lender matters as much as choosing between fixed and variable rates. The lender you work with determines which programs you access, how aggressively they compete for your business, and ultimately how much you pay. Borrowers often leave thousands of dollars on the table by defaulting to their bank without exploring other options. The mortgage market in Canada fragments into three distinct channels: traditional banks, alternative lenders, and mortgage brokers. Each operates differently, and understanding those differences directly affects your final cost.

Traditional Banks and Their Hidden Pricing

Traditional banks offer convenience and brand recognition, but they rarely offer their best rates to walk-in customers. Banks use mortgages as relationship products-they want you to hold a chequing account, credit card, and investment accounts with them. This bundling strategy means their posted rates sit higher than what they’ll actually negotiate with you, and their rates often lag behind competitors. If you call your bank and ask for their best 5-year fixed rate, you’ll likely hear something close to the rates lenders publish when they collect rates from 50+ lenders three times daily. But brokers and alternative lenders frequently beat those published bank rates because they compete aggressively for volume rather than relying on customer loyalty. Borrowers who shop only at their existing bank typically overpay by 0.25% to 0.50% annually-on a $400,000 mortgage, that difference costs you $1,000 to $2,000 per year.

Alternative Lenders and Private Mortgages

Alternative lenders and private lenders fill gaps that banks won’t touch. They work with borrowers who have recent credit issues, self-employment income that doesn’t fit traditional lending boxes, or non-standard properties. Their rates run higher because they accept more risk, but for the right borrower in the right situation, they’re the only option available. The trap occurs when borrowers assume alternative lenders are always more expensive-sometimes they’re not, particularly when a bank would decline you entirely.

Mortgage Brokers and Wholesale Access

Mortgage brokers access wholesale pricing that borrowers cannot reach directly. A broker can use part of their compensation to buy down your rate, effectively lowering the published rate you’d see elsewhere. Brokers typically earn around 1% in finder’s fees on prime mortgages, and they negotiate that fee with lenders rather than charging you directly. The advantage compounds when you have a complex file (self-employment income, a condo purchase, or a renewal with a new lender where a stress test previously blocked you). Brokers know which lenders specialize in which situations and can position your application accordingly. The disadvantage appears if you work with a broker who doesn’t shop aggressively or who steers you toward lenders paying higher commissions rather than offering you the lowest rate.

Credit Unions as a Local Alternative

Credit unions represent a third path that many Canadians overlook. Credit unions offer rates competitive with major banks and sometimes beat them, particularly on variable mortgages. They operate as member-owned institutions rather than shareholder-driven corporations, which changes their incentive structure. A credit union in your province may offer better terms than a national bank because they’re invested in your community’s prosperity. However, credit unions vary dramatically by province and size. Some offer sophisticated mortgage products and competitive rates; others operate with older systems and higher costs. The practical approach involves checking your local credit union’s current rates against what lenders publish, since the comparison takes minutes and could save you real money.

Final Thoughts

Selecting the right mortgage comes down to three concrete decisions: understanding your rate options, calculating your true monthly cost including all fees and insurance, and comparing what different lenders actually offer you. Fixed rates provide payment certainty at a higher starting cost, while variable rates save money when rates fall but expose you to payment increases. Government programs like the First-Time Home Buyer Incentive and extended 30-year amortizations for eligible buyers have genuinely expanded who qualifies for affordable mortgage options Canada.

Your next move is straightforward: obtain a mortgage pre-approval from at least two sources (a traditional bank and a mortgage broker), then request identical mortgage scenarios from each. Run the numbers at different amortization lengths to see how 25 versus 30 years affects your monthly payment, and ask about prepayment flexibility and what happens at renewal. These conversations take hours but save thousands of dollars over your mortgage lifetime.

We at Financial Canadian understand that navigating mortgage options feels overwhelming, which is why we help financial professionals and lenders establish a strong digital presence where borrowers can access clear, practical information. Visit Financial Canadian to explore how we create responsive, user-friendly websites that drive engagement and trust in the mortgage space.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment