When you need cash fast, a same day loan in Canada can feel like the answer. But speed comes with trade-offs that matter.

At Financial Canadian, we break down what these loans actually are, how to find legitimate lenders, and whether they’re right for your situation. This guide covers the real costs and benefits so you can make an informed choice.

How Same Day Loans Work in Canada

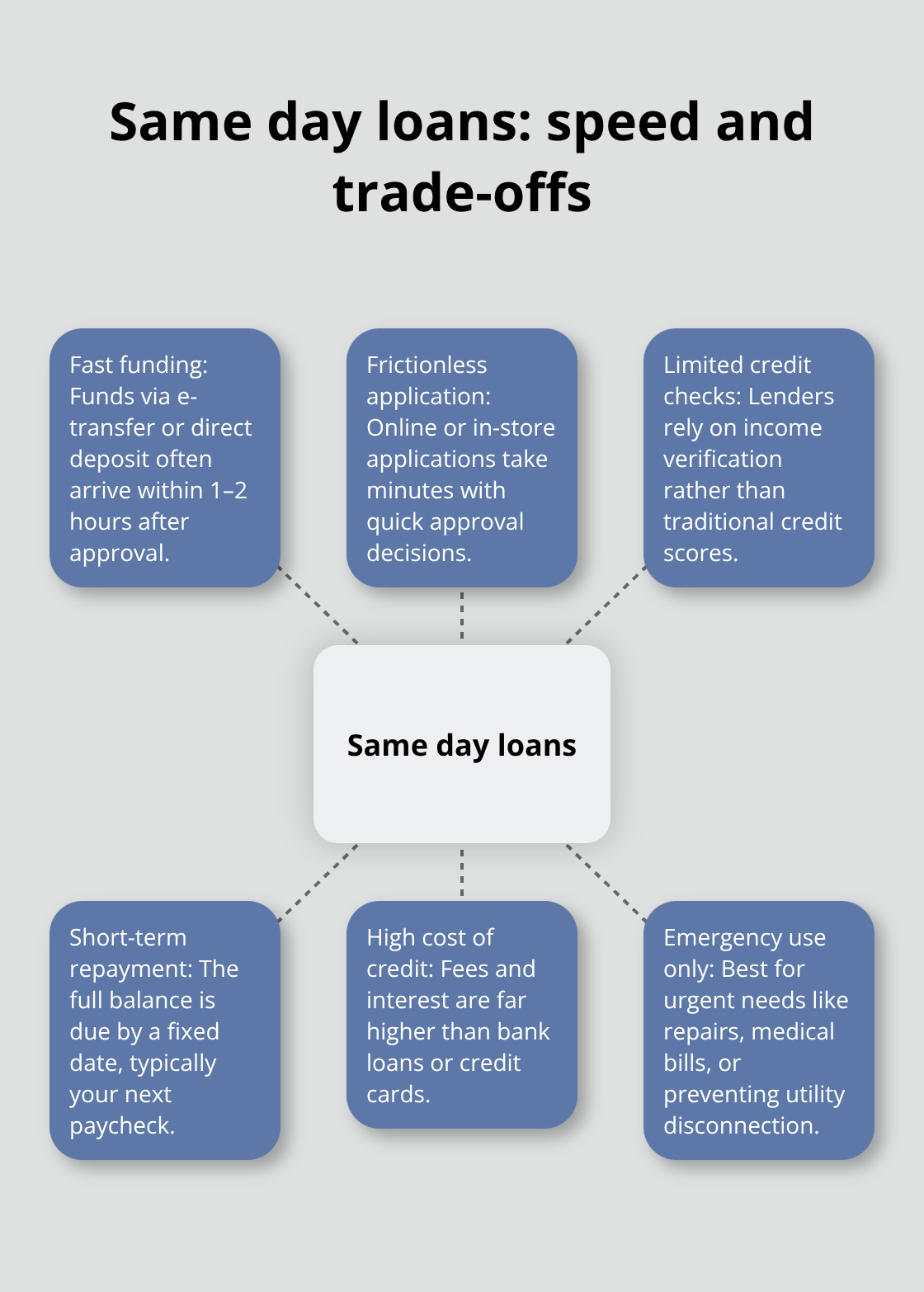

Same day loans are short-term borrowing products that deposit cash into your bank account within hours of approval, not days or weeks. The application happens entirely online or at a physical location, takes minutes to complete, and lenders make approval decisions quickly without traditional credit checks. Once approved, funds arrive via e-transfer or direct deposit, often within 1–2 hours depending on your bank. You repay the full amount by a set due date, typically aligned with your next paycheck. This speed appeals to those facing urgent expenses like car repairs, medical bills, or utility arrears, but the trade-off is substantial: interest rates and fees are extremely high compared to traditional loans.

What You Actually Pay for Speed

The cost structure is straightforward but punishing. In Ontario, you pay $14 for every $100 borrowed, meaning a $500 loan costs $70 in fees alone. For a $1,500 loan over 14 days, total repayment reaches $1,710, with an annual percentage rate (APR) of 365%. British Columbia caps costs at 14% of the principal, so a $300 loan for 14 days costs $42. Alberta charges $14 per $100 borrowed, and if you stretch a loan over 42 days on a weekly pay cycle, the APR drops to 121.67%, which is still staggering. Nova Scotia uses the same $14-per-$100 model. The longer your loan term, the lower the effective APR becomes, but these remain high-cost loans designed only for genuine emergencies, not regular borrowing.

Eligibility and the Application Reality

You must be 18 or older, have a valid Canadian bank account with online access, government-issued photo ID, and proof of employment income to qualify. Employment doesn’t need to come from a traditional job; Employment Insurance benefits, pension income, disability payments, and child tax credits all count. If you’ve been employed for less than 2 months, you’ll need to wait until you hit that threshold before applying. The application process strips away paperwork-you fill out a form online, verify your bank account, and sometimes upload recent bank statements. Approval happens in minutes, and funds land in your account almost immediately after. No credit check means bad credit won’t disqualify you, but this speed exists because lenders rely on income verification rather than assessing your ability to handle debt responsibly.

What Happens If You Miss a Payment

Late payments carry serious consequences that most borrowers overlook. A returned item fee applies when your payment bounces, and the lender charges 30% per annum in returned item interest on top of that. If your account falls seriously delinquent, the lender may turn it over to a collections agency, which damages your credit score and creates a record that follows you for years. This reality makes same day loans dangerous for anyone uncertain about their ability to repay on the exact due date-there are no extensions, refinancing options, or rollovers allowed.

Finding a Legitimate Lender

Not all same day loan providers operate with the same standards. Check whether the lender holds proper provincial licensing and operates across multiple provinces (a sign of legitimate operations). Trustpilot reviews offer real feedback from actual borrowers, though you should read both positive and negative comments to understand the full picture. Verify that the lender discloses all fees upfront before you apply, and confirm that the terms match provincial regulations in your area. Comparing multiple lenders takes time, but it prevents you from accepting predatory terms out of desperation.

The Real Trade-Off: Speed vs. Cost

Why Speed Matters in a Financial Crisis

Same day loans deliver on their promise of speed, but that velocity comes at a price that makes them fundamentally different from conventional borrowing. The convenience is genuine: you can apply at 11 PM on a Sunday, get approved within minutes, and have cash in your account before Monday morning. This matters when your car breaks down and you need it for work, when a dental emergency can’t wait, or when utility disconnection notices arrive. The application process strips away the friction of traditional lending-no lengthy forms, no credit inquiries, no waiting for a loan committee to review your file. For someone facing a genuine crisis with a tight timeline, same day loans solve a real problem that banks simply cannot match.

The Cost Structure That Defines These Loans

This speed exists because lenders have shifted the risk entirely onto borrowers, and the cost structure reflects that shift starkly. A $500 same day loan in Ontario costs $70 in fees for 14 days, but extend that loan to 42 days and you pay roughly $140-more than 28% of the borrowed amount. The 365% APR that dominates 14-day loans drops to 121.67% over 42 days in Alberta, which sounds better until you realize you’re still paying interest rates that would be illegal on credit cards.

Compare this to a credit card cash advance at 19.99% APR or a personal bank loan at competitive rates, and the gap becomes impossible to ignore. The speed premium is real, and lenders price it accordingly.

When Borrowers Fall Into a Debt Trap

The danger emerges when borrowers use same day loans for non-emergencies or stack multiple loans to cover ongoing expenses. If you take out a $500 same day loan to cover groceries because your paycheck is short, you’ve entered a cycle where the next paycheck gets consumed by repayment, leaving you short again. Trustpilot reviews from actual borrowers reveal this pattern repeatedly-people who took one loan to cover an emergency and then needed another to cover the repayment. The lack of comparison shopping amplifies this risk; desperation pushes people toward the first lender that approves them rather than the cheapest option. A borrower who spends 30 minutes comparing three lenders might save $20–$30 on a $500 loan, which is meaningful money when you’re already in financial distress.

The Consequences of Missing a Payment

Missing a payment creates a cascading problem that most borrowers overlook. A returned item fee applies when your payment bounces, and the lender charges 30% per annum in returned item interest on top of that. If your account falls seriously delinquent, the lender may turn it over to a collections agency, which damages your credit for years. Same day loans work only when you treat them as genuine emergencies with a clear repayment plan, not as a financial product to reach for repeatedly.

Finding the Right Lender Before You Borrow

Not all same day loan providers operate with the same standards, which is why your choice of lender matters as much as your decision to borrow. Check whether the lender holds proper provincial licensing and operates across multiple provinces (a sign of legitimate operations). Trustpilot reviews offer real feedback from actual borrowers, though you should read both positive and negative comments to understand the full picture.

Verify that the lender discloses all fees upfront before you apply, and confirm that the terms match provincial regulations in your area. Comparing multiple lenders takes time, but it prevents you from accepting predatory terms out of desperation-and this comparison process becomes your first line of defense against the debt trap that catches so many borrowers.

How to Pick a Same Day Loan Lender Worth Trusting

The lender you choose matters more than you think, because a bad choice can cost you hundreds of dollars in avoidable fees and trap you in a cycle of repeated borrowing. Start by pulling up the websites of at least three lenders operating in your province and comparing their fee structures side by side. In Ontario, all lenders must charge $14 per $100 borrowed, so the rate is fixed by law, but in British Columbia the maximum is 14% of principal, which creates real differences in what you’ll repay. A $500 loan costs $70 in Ontario but only $70 in BC if you borrow for 14 days, so your location determines the baseline cost. What separates lenders within those legal limits is transparency and how they treat borrowers who face genuine hardship.

Check Fee Disclosure Before You Apply

Look for lenders that disclose all fees upfront in writing before you apply, not after approval. Some lenders bury fees in fine print or add surprise costs at the final screen, which is a red flag that signals they prioritize extraction over service. Legitimate lenders state the exact dollar amount you’ll repay, not just the interest rate. A lender that tells you a $500 loan costs $70 with a total repayment of $570 operates honestly; one that hides the fee until the final screen plays games with desperation.

Read Real Reviews From Actual Borrowers

Real reviews from actual borrowers reveal patterns that marketing claims never will. Read both positive and negative reviews to understand where problems occur. Common complaints in negative reviews include difficulty with the repayment process, confusion about fees, or aggressive collection tactics when payments are late. If you see multiple reviews mentioning the same problem, that lender has a systemic issue worth avoiding.

Verify Provincial Licensing and Multi-Province Operations

Provincial licensing matters, though this verification takes only minutes. Each province publishes a list of licensed payday lenders, and you can check whether your chosen lender appears on it within minutes. Operating without a license is illegal, and unlicensed lenders offer no protection if something goes wrong. Lenders operating across multiple provinces like Ontario, British Columbia, Alberta, and Nova Scotia demonstrate they’ve met regulatory standards in different jurisdictions, which is harder to achieve than operating in a single province.

Ask Direct Questions Before You Borrow

Contact the lender before you apply and ask specific questions about their policies. If you call and ask whether extensions or rollovers are available and the representative hesitates or avoids answering, walk away. Legitimate lenders state clearly that loans must be repaid in full by the due date with no exceptions (no extensions, no refinancing options, no rollovers allowed). This clarity upfront prevents misunderstandings that cost money later.

Final Thoughts

Same day loan Canada products solve a genuine problem for people facing real emergencies, but they work only when you treat them as a last resort, not a financial habit. The speed is real, the costs are staggering, and the consequences of misuse are severe. If you need cash within hours because your car broke down, a medical bill arrived unexpectedly, or utilities are about to disconnect, a same day loan can bridge that gap when nothing else will. The key is borrowing only what you need, understanding exactly what you’ll repay, and having a concrete plan to repay the full amount by the due date.

The math matters more than the marketing. A $500 same day loan costs $70 in Ontario, which feels manageable until you realize that’s a 365% annual rate. Compare that to credit card cash advances, personal bank loans, or asking family for help before you apply. If you can wait even a few days, traditional lending options will cost you significantly less. If you cannot wait, verify that the lender holds provincial licensing, discloses all fees upfront, and operates transparently. Read actual borrower reviews on Trustpilot to understand where problems occur. Contact the lender directly and confirm that no extensions or rollovers exist, so you know exactly what you’re signing up for.

Same day loans become dangerous when people use them repeatedly to cover ongoing expenses rather than genuine emergencies. One loan to cover a crisis is manageable; three loans in six months signals a deeper financial problem that borrowing will only worsen. If you find yourself needing multiple loans, pause and reassess your budget, look for ways to increase income, or seek help from non-profit credit counseling services in your province.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment