A credit score below 600 puts you in a tough spot when applying for traditional loans. Banks and major lenders often reject applications outright, leaving you searching for alternatives.

At Financial Canadian, we know bad credit Canada loans exist-and they’re more accessible than you think. This guide walks you through your actual options, how to compare lenders fairly, and how to avoid traps that make your situation worse.

What Counts as Bad Credit in Canada

Understanding Your Credit Score

Your credit score tells lenders whether you pay your bills. In Canada, credit bureaus Equifax and TransUnion track your payment history, outstanding debts, and credit inquiries. A score below 600 signals serious risk to traditional lenders, but the damage extends beyond one number. If you’ve missed payments by 30 or more days, defaulted on accounts, or filed for bankruptcy or a consumer proposal, you’re locked out of conventional financing.

How Lenders Assess Your Creditworthiness

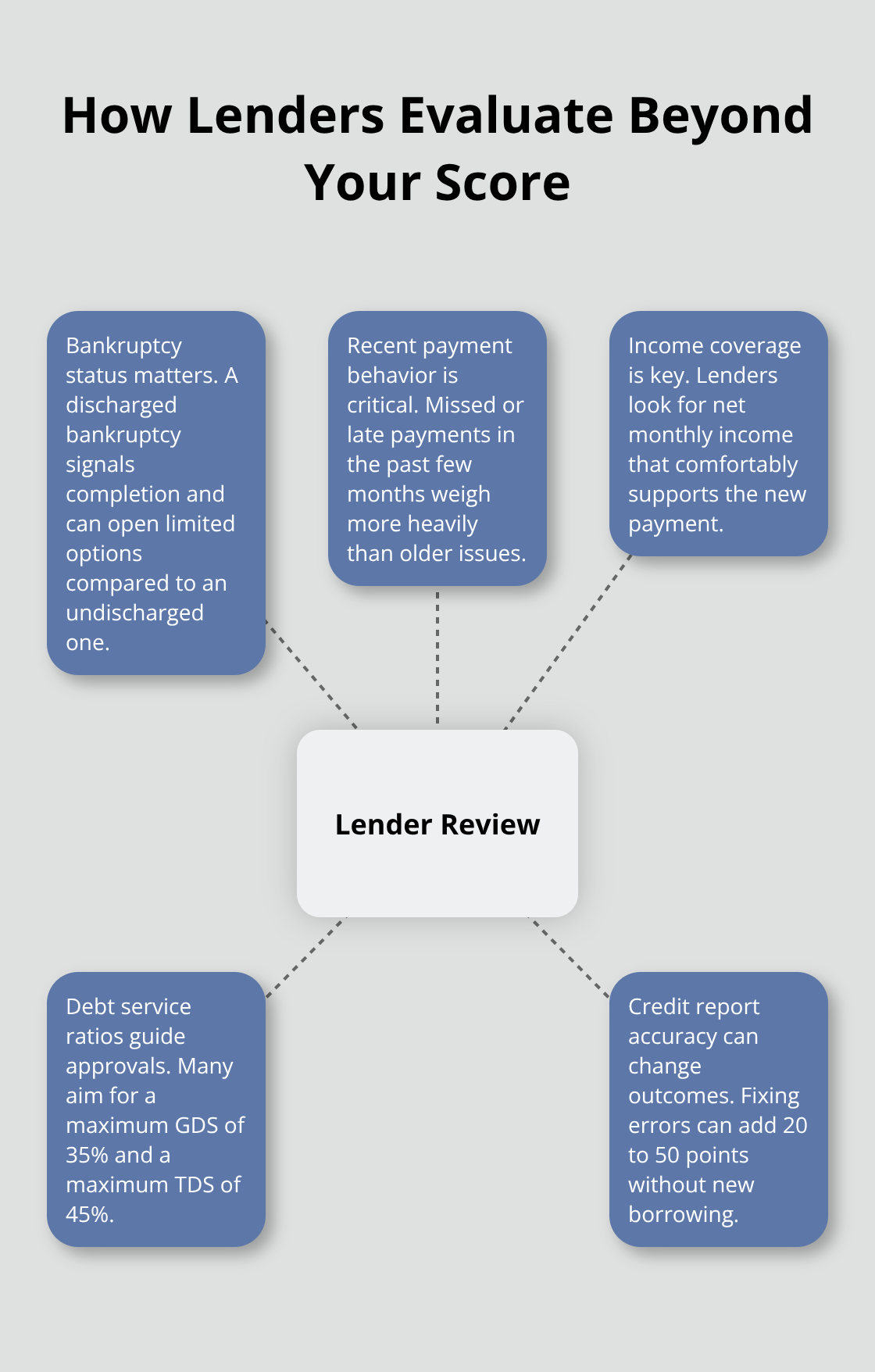

Credit unions and alternative lenders look beyond the score itself. They examine whether you’ve discharged a bankruptcy, how recently you missed payments, and whether your net monthly income can cover new debt. A score of 541 doesn’t automatically disqualify you from credit builder loans through credit unions, though lenders may require stronger income ratios (maximum GDS of 35% and maximum TDS of 45%). Getting copies of your credit reports from both Equifax and TransUnion costs nothing and shows exactly what lenders see about you. Many people find errors on their reports-accounts they don’t recognize or payments marked late when they were actually on time.

Correcting these mistakes can lift your score by 20 to 50 points without any additional effort.

The Real Cost of Bad Credit Borrowing

Bad credit doesn’t mean you have no options, but it does mean expensive ones if you choose poorly. Personal loans marketed to bad credit borrowers often carry high interest rates, making them far costlier than secured alternatives. Payday lenders exploit desperation with rates exceeding 400% annualized, trapping borrowers in cycles of repeated borrowing.

Credit Builder Loans as a Better Path

Credit builder loans through credit unions function differently. You deposit money into a secured savings account that the lender holds as collateral, then borrow against it at reasonable rates while building payment history. Terms typically range from $2,000 to $5,000 over 6 to 24 months with fixed rates, and on-time payments report to credit bureaus, lifting your score over time. These loans require income verification and no prior write-offs with the lender, but approval can happen within one business day if paperwork is complete.

Getting Professional Guidance Before You Borrow

A nonprofit credit counsellor through organizations like the Credit Counselling Society can review your entire financial picture and recommend whether a credit builder loan, debt management program, or other approach actually solves your problem rather than adding to it. This step costs nothing and prevents you from borrowing your way deeper into trouble. Understanding what qualifies as bad credit and how lenders evaluate your situation sets the foundation for exploring the loan options that actually work for your circumstances.

Real Loan Options That Actually Work for Bad Credit

Credit Builder Loans: Fixing Your Credit While You Borrow

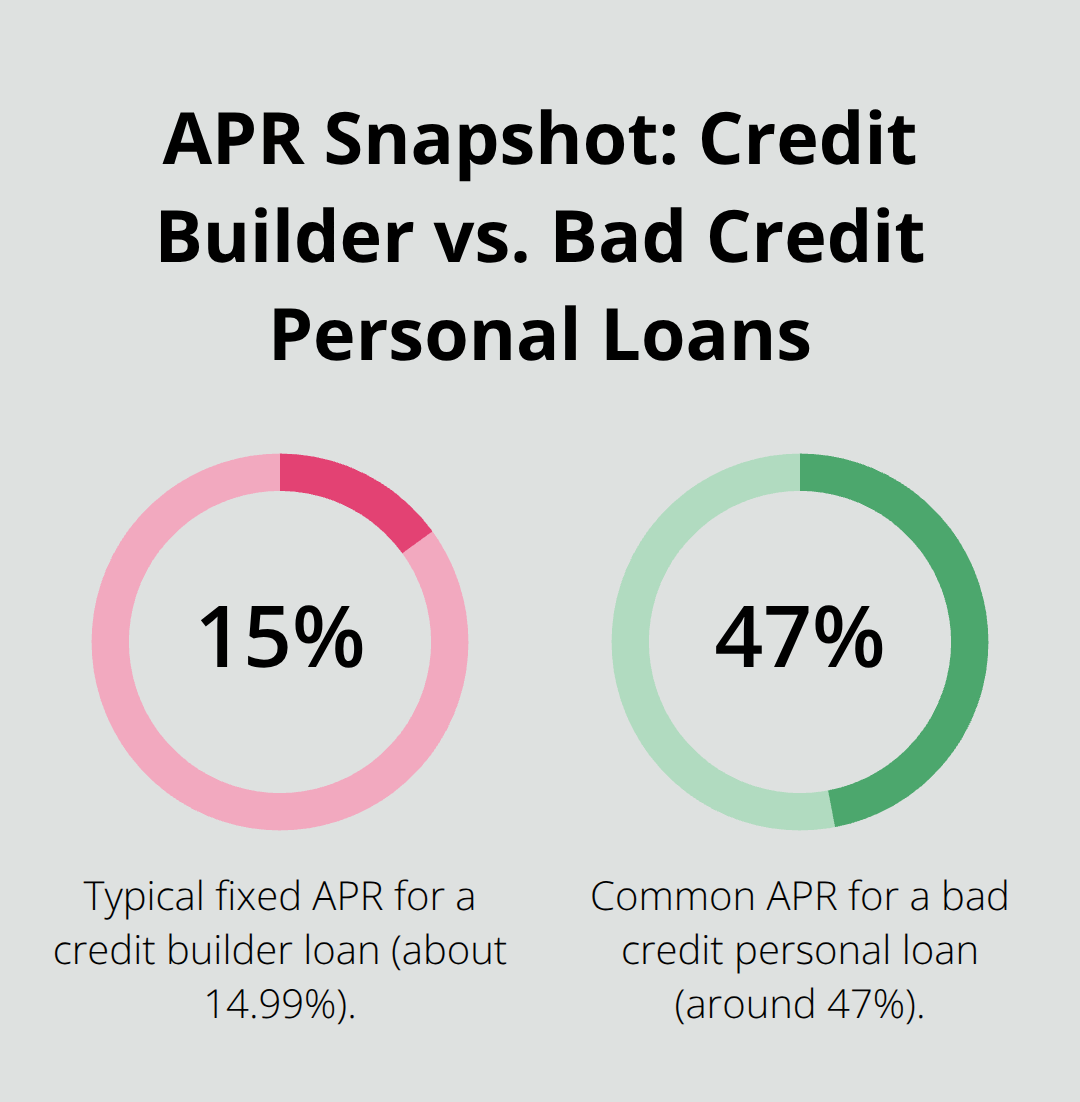

Credit builder loans through credit unions stand apart from other bad credit alternatives because they fix your credit while you borrow, not trap you in debt. With a credit builder loan, you deposit money into a redeemable term investment (GIC) that the lender holds as security. You then borrow against that deposit at a fixed rate, typically 14.99% for terms ranging from $2,000 to $5,000 over 6 to 24 months. Every on-time payment reports to Equifax and TransUnion, directly strengthening your credit score. The approval process moves fast-within one business day if your paperwork is complete-and you’ll need income verification showing your gross debt service ratio doesn’t exceed 35% and your total debt service ratio stays under 45%. Once you finish repaying, you get your deposit back plus any investment income earned during the loan term. That cash becomes available for a major purchase or continued savings.

Why Payday Loans and High-Rate Personal Loans Fail You

Payday loans and high-rate personal loans marketed to bad credit borrowers demand immediate rejection. Payday lenders charge rates exceeding 400% annualized, according to Government of Canada research, creating a vicious cycle where borrowers take out new loans to repay old ones. Personal loans for bad credit commonly carry around 47% APR, making them substantially more expensive than credit builder alternatives over time. This structure works because it removes lender risk while giving you a genuine path forward, not a predatory trap.

Practical Alternatives Before You Borrow

If you’re desperate for cash, cut expenses first-eliminate or downgrade your internet plan, reduce your cell phone service, or sell items you no longer need. A nonprofit credit counsellor through organizations like the Credit Counselling Society can review whether a debt management program makes more sense for your situation. These programs consolidate unsecured debts into one affordable monthly payment, often eliminating or reducing interest entirely, with typical timelines around 2.5 years. The counselling costs nothing and remains confidential. Secured loans using personal assets as collateral offer another route, though you risk losing that asset if payments fail.

Moving Forward With the Right Choice

The core principle here is straightforward: avoid expensive borrowing that masks underlying financial problems rather than solving them. Your next step involves comparing the specific lenders and terms available to you, understanding exactly what each option costs, and identifying which path actually addresses your situation rather than postponing it.

Getting Approved and Managing Bad Credit Loans Responsibly

Review Your Credit Reports Before You Apply

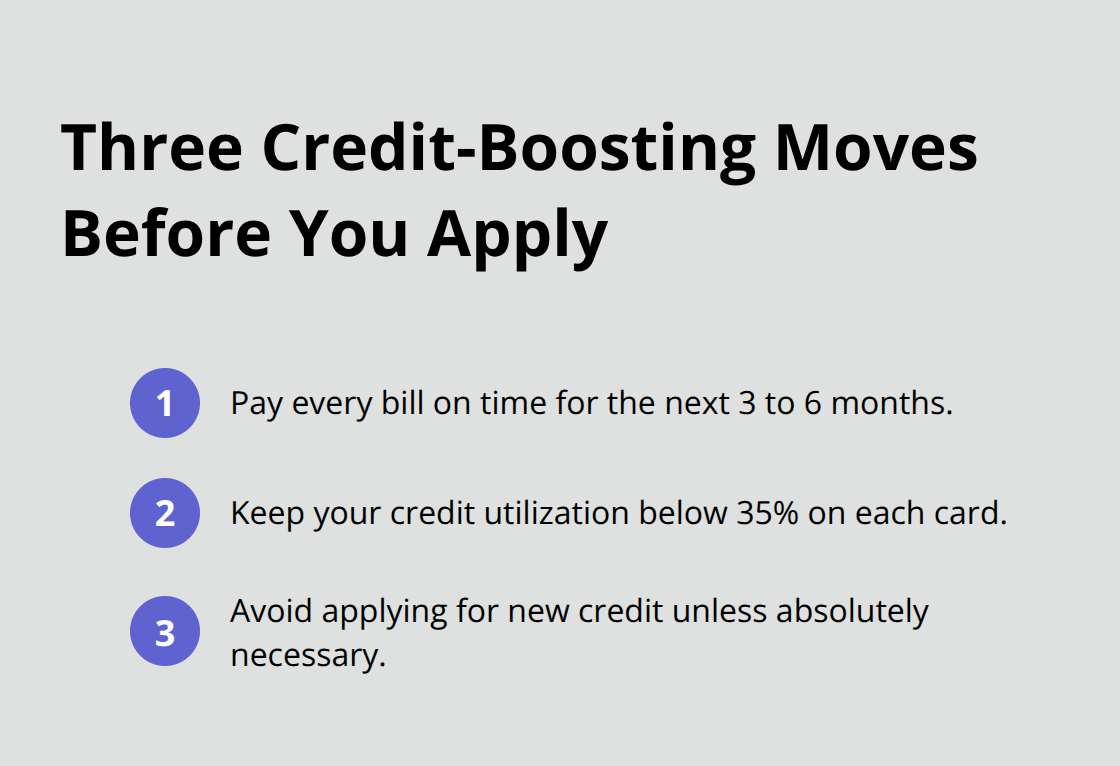

Pull your credit reports from Equifax and TransUnion before you apply anywhere. This step takes minutes and costs nothing, yet most people skip it. Your reports show exactly what lenders see, and you’ll likely find errors that drag your score down unnecessarily. The Government of Canada’s guidance on improving your credit score emphasizes that correcting inaccuracies can boost your rating by 20 to 50 points without borrowing a single dollar. Once you have your reports in hand, focus on three concrete actions: pay every bill on time for the next 3 to 6 months, keep your credit utilization below 35% on any existing cards, and avoid applying for new credit unless absolutely necessary.

Minimize Hard Inquiries and Compare Lenders Strategically

Each hard inquiry from a lender temporarily lowers your score, so batch your applications within a two-week window to minimize damage. When you compare lenders, ignore the marketing language and focus on the actual numbers. A credit builder loan at 14.99% fixed over 24 months costs substantially less than a personal loan at 47% APR, even though both are technically available to you. Calculate the total interest you’ll pay on each option using an online loan calculator, then factor in whether the loan actually solves your problem or just delays it. A credit counsellor from a nonprofit organization like the Credit Counselling Society can walk through these calculations with you at no cost, helping you avoid borrowing more than you need.

Set Up Automatic Payments and Understand Late Payment Policies

Your repayment plan determines whether the loan rebuilds your credit or destroys it further. Set up automatic payments from your bank account so you never miss a due date, since even one late payment can trigger loan collapse if you fall 31 or more days in arrears. If your lender offers a no-fee bank account bundled with the loan, use it exclusively for this purpose so the payment flows automatically without friction. Before you sign anything, ask your lender directly about their late payment policy and what happens if you face temporary hardship. Some lenders will work with you on a modified payment schedule, while predatory operators will seize your collateral immediately.

Explore Debt Management Programs as an Alternative

The cost difference between a legitimate credit builder loan and a payday lender is enormous, so if you’re only seeing payday options available to you, contact a nonprofit credit counselling organization before proceeding. These organizations can connect you to better alternatives like debt management programs that consolidate your debts into one payment, often reducing interest rates or eliminating them entirely, with typical timelines around 2.5 years. A debt management program (rather than a new loan) addresses your underlying financial problems instead of masking them with additional borrowing. This approach costs nothing and remains confidential, giving you a genuine path forward without the trap of expensive debt cycles.

Final Thoughts

Bad credit Canada loans work when you choose the right option and commit to responsible repayment. A credit builder loan at 14.99% fixed over 24 months costs a fraction of what payday lenders demand, and every on-time payment strengthens your credit score with Equifax and TransUnion. This matters because your next loan, mortgage, or job application depends on that score improving.

Pull your credit reports from both bureaus and correct any errors before you apply anywhere. Contact a nonprofit credit counsellor through the Credit Counselling Society to review whether a credit builder loan, debt management program, or other approach actually solves your situation (this guidance costs nothing and remains confidential). Compare lenders on actual numbers, not marketing promises, and set up automatic payments so you miss no due dates.

Responsible borrowing means understanding that a loan is a tool to fix your credit, not a shortcut to avoid fixing your finances. If you’re only seeing payday lenders available to you, that’s a signal to seek professional guidance before you proceed. Visit Financial Canadian to explore tools and guidance that support your path toward stronger credit and financial stability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment