When unexpected expenses hit, same day loans in Canada offer a quick way to access funds. We at Financial Canadian understand that emergencies don’t wait, and sometimes you need money fast.

This guide breaks down how same day loans work, what types are available, and whether they’re the right choice for your situation. We’ll also show you alternatives worth considering before you borrow.

How Same Day Loans Work in Canada

Speed Through Simplified Assessment

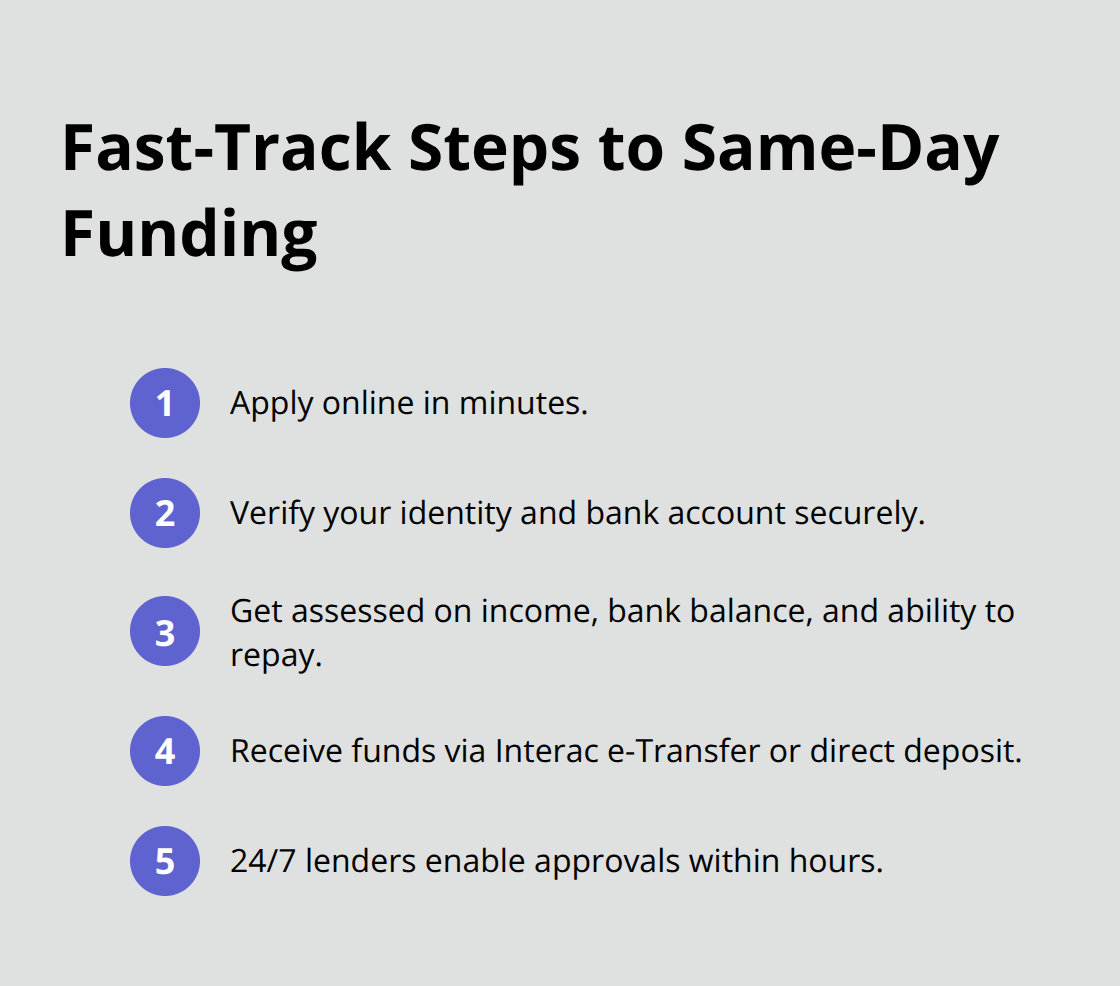

Same day loans are short-term borrowing products that move cash into your account within hours, not days. You apply online, verify your identity and bank account, and if approved, funds arrive via Interac e-Transfer or direct deposit. Most lenders operate 24/7, so you can apply at midnight on a Sunday and have money by Monday morning.

The speed comes from skipping traditional credit checks. Instead of reviewing your credit history, lenders assess your current income, bank balance, and ability to repay. This shift in evaluation criteria means approval decisions happen in minutes rather than weeks.

Loan Amounts and Costs

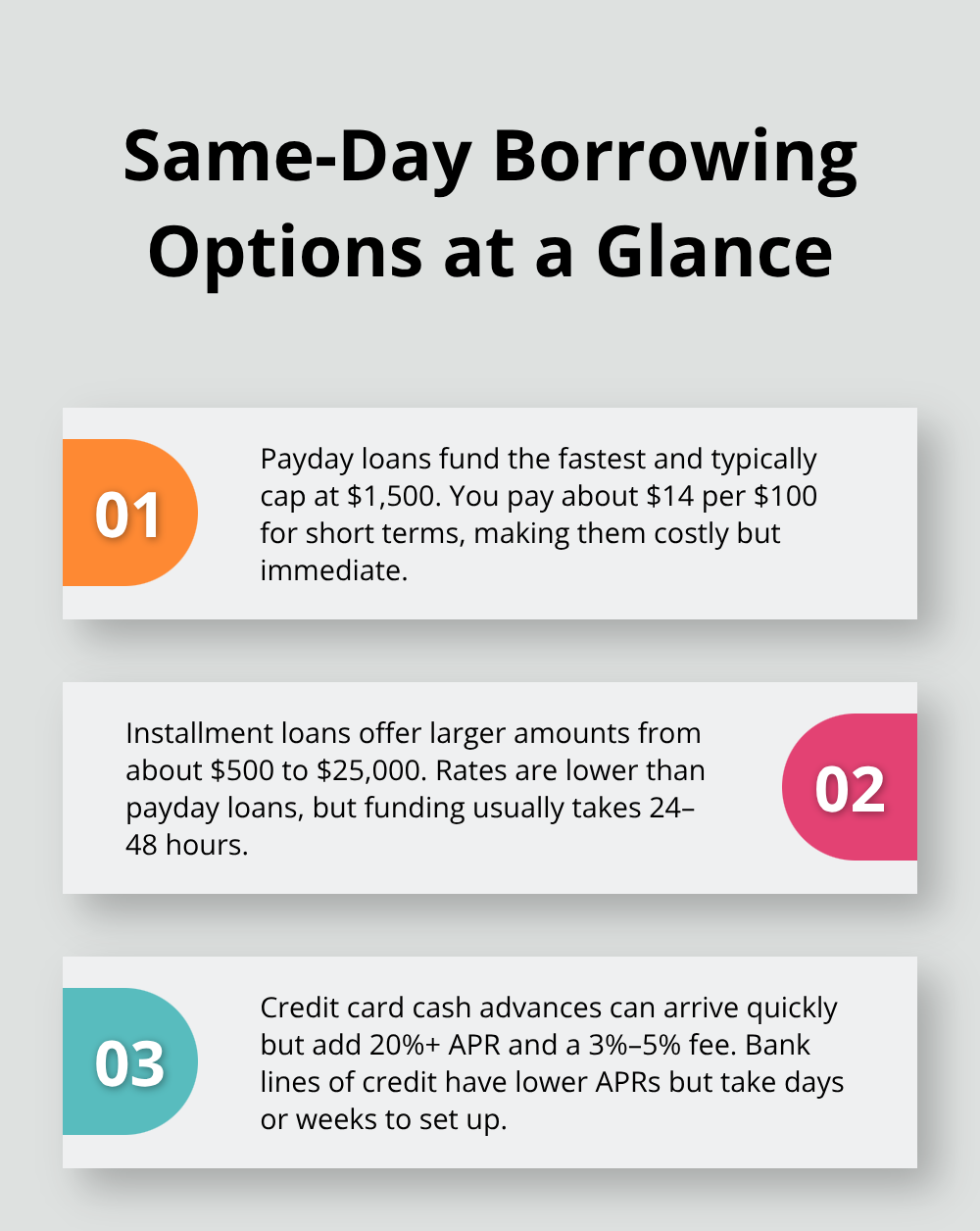

Payday loans cap out at around $1,500 in most provinces, while installment loans range from $500 to $25,000 depending on the lender and your province. The cost structure varies significantly between product types.

A typical payday loan charges $14 per $100 borrowed, which translates to roughly 365% APR on a 14-day loan. For example, borrowing $300 for 14 days costs $42 in fees, meaning you repay $342 total. Installment loans offer lower rates, sometimes around 34% APR, but stretch payments over months or years, increasing total interest paid.

Eligibility and Application Requirements

Most employed Canadians meet the basic eligibility criteria lenders require. You need to be at least 18 or 19 years old, have verifiable monthly income from employment, disability benefits, pensions, or child tax credits, and maintain an active Canadian bank account for at least 180 days. Some lenders require a minimum of two months employment, while others accept applicants with four months of income history.

The online application itself takes 10 to 15 minutes and asks for your personal details, income information, and banking credentials. After submission, identity verification happens instantly through secure bank connections, and the lender’s algorithm processes your application in real time.

From Approval to Funds in Your Account

If approved, you electronically sign the loan agreement, and funds move within minutes using Interac e-Transfer or within 24 hours via standard direct deposit. The entire process from clicking apply to seeing money in your account can happen in under an hour (though timing depends on your bank and the time of day you apply).

If automation fails-which occasionally occurs with smaller financial institutions-you may need to upload bank statements or sign pre-authorized debit forms manually, adding a day or two to funding. This manual step remains rare, but it’s worth knowing about before you apply. Understanding these mechanics helps you decide whether a same day loan fits your situation, or whether another borrowing option might serve you better.

Same Day Loan Types and What They Cost

Payday Loans: Speed Over Affordability

Payday loans represent the fastest and smallest borrowing option, capping at $1,500 across most Canadian provinces. These work best when you need $300 to $500 to cover an unexpected car repair or medical bill before your next paycheck arrives. The cost structure hits hard: you pay $14 per $100 borrowed for a typical 14-day term, which equals $42 on a $300 loan. That $300 becomes $342 repaid in two weeks.

The math worsens with longer terms. A 62-day loan costs $14 per $100 as well, but spreads the fee over more time, making the APR drop to around 82.4%. The real advantage of payday loans is speed: you can have cash within 15 minutes via Interac e-Transfer if you apply during business hours, or within 24 hours otherwise.

Who Qualifies for Payday Loans

You don’t need perfect credit or a long employment history to qualify. Four months of income from any source (employment, disability, pensions, or child tax credits) typically qualifies you. The application takes 10 to 15 minutes online, and lenders operate 24/7, so Sunday night emergencies don’t have to wait until Monday morning.

Installment Loans: Larger Amounts, Longer Terms

Installment loans offer a different structure entirely. These range from $500 to $25,000 depending on your province and the lender, with APRs typically ranging from 6%-24% through banks and major financial institutions. A $4,500 loan spread over 36 months costs roughly $203 per month at 34.95% APR, making monthly payments predictable and manageable compared to payday loans. Some lenders offer terms up to 84 months, which lowers your monthly payment further but increases total interest paid over time.

The trade-off is clear: installment loans take longer to fund than payday loans (typically 24 to 48 hours), but they let you borrow larger amounts and repay without crushing yourself on a single payday.

Credit Cards and Lines of Credit: The Middle Ground

Credit card cash advances give you immediate access to funds (sometimes within hours) but charge interest rates exceeding 20% annually plus upfront fees of 3% to 5% of the amount withdrawn. A $500 cash advance costs $15 to $25 just to get the money, then interest accrues daily. Personal lines of credit through banks offer better rates (often 7% to 12% APR) but require established credit and take days or weeks to set up, defeating the purpose when you need same-day funds.

Choosing the Right Loan Type for Your Situation

For genuinely urgent situations where you can repay within weeks, payday loans remain the only realistic same-day option despite their cost. For emergencies where you can stretch repayment across months, installment loans provide breathing room and lower overall interest, though you’ll wait longer for funding. The decision between these products depends on how quickly you need money and how much you can afford to repay each month. Understanding these distinctions helps you avoid overpaying for speed you don’t need or underpaying for flexibility you do. Before committing to any loan product, you should also weigh the hidden costs that lenders don’t always advertise upfront.

When Same Day Loans Help (And When They Hurt)

True Emergencies vs. Recurring Shortfalls

Same day loans solve genuine emergencies where timing matters more than cost. A car breakdown that prevents you from reaching work, an unexpected veterinary bill, or a medical expense that cannot wait until payday-these situations justify the high fees. You borrow $300, pay $42 in interest, and solve the problem before it cascades into job loss or health complications. The math works when the alternative is worse.

This calculus breaks down quickly once you move beyond true emergencies. Research from the Financial Consumer Agency of Canada shows that payday loan borrowers renew their loans multiple times per year, meaning they end up paying far more in fees than the original loan amount. A borrower who takes a $300 payday loan every month for a year pays roughly $504 in fees alone-68% of the original borrowed amount-without actually reducing the underlying debt.

The Renewal Trap and Cash Flow Compression

This pattern occurs because same day loans do not address the root problem: insufficient income to cover expenses. They provide temporary relief while the underlying cash shortage persists, creating a cycle where you borrow again the following month when the same gap reappears.

Taking a payday loan for $300 means your next paycheck is already committed before you receive it, leaving no margin for additional emergencies. This compressed cash flow is why borrowers fall into the renewal trap. Each new loan compounds the problem rather than solving it. The fees stack up faster than your ability to escape the cycle.

Hidden Costs Beyond Interest Rates

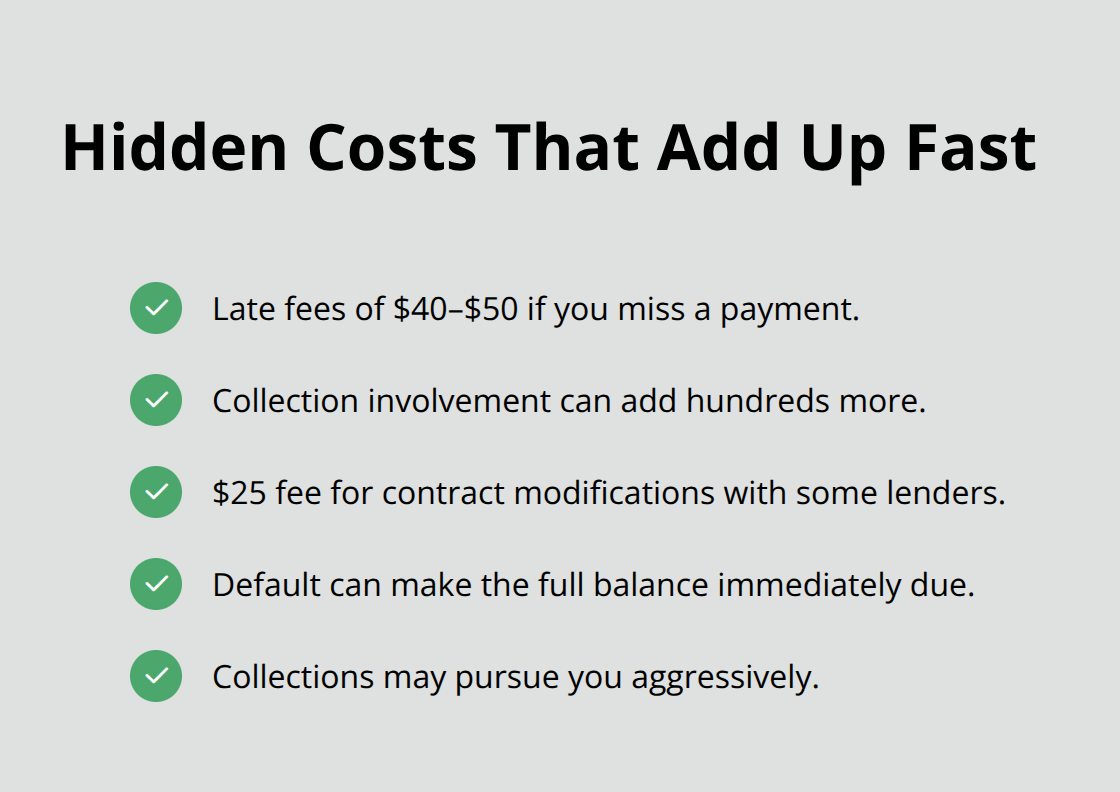

The hidden costs extend well beyond interest rates. Late fees run $40 to $50 if you miss a payment, collection agency involvement can add hundreds more, and some lenders charge $25 for contract modifications if you need to adjust your repayment date. If you default, the full loan balance becomes immediately due, and collection agencies may pursue you aggressively.

Same day loans also damage your financial flexibility. Installment loans offer more breathing room through smaller monthly payments, but they carry their own danger: a $4,500 installment loan at 34.95% APR costs $3,090 in total interest over 36 months, meaning you repay $7,590 total. The longer the term, the more interest you ultimately pay.

When to Borrow and When to Find Alternatives

For long-term financial health, same day loans should be your absolute last resort, used only when you have exhausted every alternative and the emergency genuinely cannot wait. If you are borrowing repeatedly for the same expenses, you need income growth or expense reduction, not another loan. The pattern of repeated borrowing signals a structural problem with your budget that no short-term loan can fix. Protecting yourself from future debt cycles means staying informed about your financial situation-something that begins with understanding where you stand today.

Final Thoughts

Same day loans in Canada serve a narrow but real purpose: they bridge genuine emergencies when time matters more than cost. Payday loans move cash to your account within hours, while installment loans offer larger amounts with lower rates but require waiting a day or two. The choice between them depends on your specific situation, not on marketing promises of instant approval or guaranteed funding.

Same day loans work only when you face a true one-time emergency and can repay without borrowing again next month. A car repair that prevents you from working, a medical bill that cannot wait, or a utility disconnection notice justifies the $14-per-$100 fee structure. The moment you find yourself renewing the same loan repeatedly, the product stops solving your problem and starts creating a worse one.

Before committing to any same day loan, exhaust your alternatives: ask family or friends for a short-term loan with no interest, check whether your employer offers wage advances or emergency assistance programs, review your budget to see if you can delay non-essential spending, and contact creditors directly to negotiate payment extensions. If you have already borrowed multiple times, the real issue is not access to credit but insufficient income or excessive expenses-no loan fixes that structural problem. We at Financial Canadian offer resources to help you build a stronger financial foundation and reduce your reliance on emergency borrowing altogether.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment