Buying your first home in Canada is one of the biggest financial decisions you’ll make. At Financial Canadian, we know the process can feel overwhelming-from understanding mortgages to navigating closing costs.

This roadmap breaks down everything first time homebuyers Canada need to know, step by step. We’ll walk you through assessing your finances, comparing mortgage options, and completing your purchase with confidence.

Understanding Your Financial Readiness

Your credit score sits at the foundation of homeownership because lenders use it to determine whether they’ll approve your mortgage and what interest rate you’ll pay. A score above 680 typically qualifies you for conventional mortgages, but scores above 720 unlock significantly better rates. Check your credit report through Equifax or TransUnion to spot errors that could be dragging your score down, then dispute any inaccuracies immediately. Your payment history accounts for 35% of your score, so even one missed payment can cost you thousands in higher interest rates over a 25-year mortgage. Lenders scrutinize your history for patterns-if you’ve had multiple late payments or high credit utilization in the past two years, many will view you as higher risk, regardless of your current score.

How Much Down Payment Can You Actually Afford

The down payment amount directly affects your mortgage approval and monthly payments. Most lenders require a minimum 5% down, but putting down less than 20% means you’ll pay mortgage default insurance premiums ranging from 2.8% to 4% of your mortgage value. On a $400,000 home with a 10% down payment, that insurance could add $10,000 to $13,000 to your total borrowing.

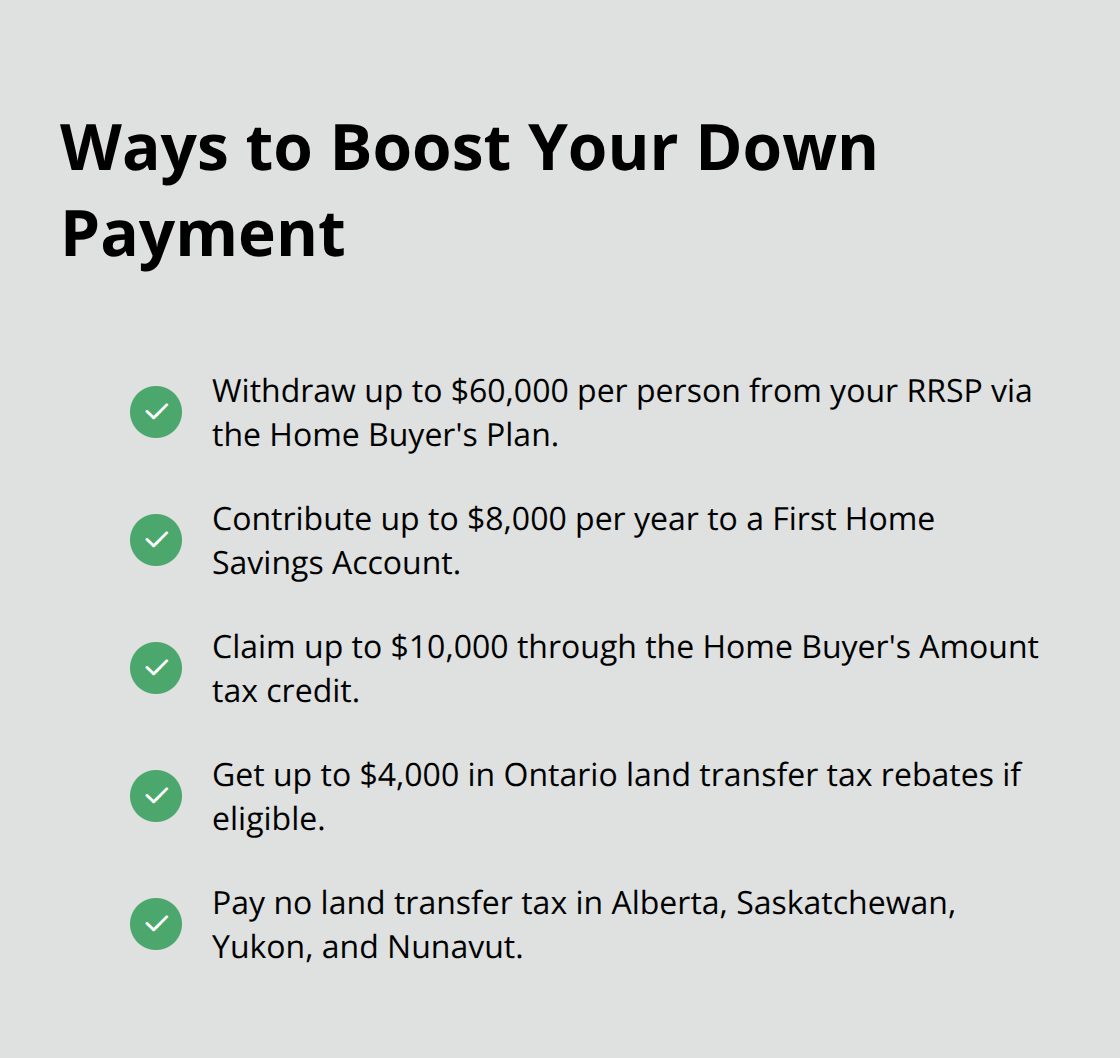

Multiple legitimate sources can boost your down payment without waiting years. The Home Buyer’s Plan allows you to withdraw up to $60,000 per person from your RRSP with a 15-year repayment schedule starting two years after withdrawal. The First Home Savings Account, launched in 2023, lets you contribute up to $8,000 per year with tax deductions and tax-free withdrawals when you buy. First-time buyers also qualify for the Home Buyer’s Amount, providing up to $10,000 in non-refundable tax credits. Some provinces offer additional support: Ontario provides up to $4,000 in land transfer tax rebates for qualifying first-time buyers, while Alberta, Saskatchewan, Yukon, and Nunavut charge no land transfer tax at all. Try to calculate what you can realistically save within your timeline rather than stretching for a larger down payment that strains your emergency fund.

The Debt-to-Income Test That Lenders Actually Use

Lenders assess your ability to carry a mortgage through your debt-to-income ratio. Most Canadian lenders cap your total debt payments, including the new mortgage, at 44% of your gross monthly income. If you earn $5,000 monthly and carry $800 in existing debt payments, your new mortgage payment can only reach around $1,400 maximum. This calculation is brutal and non-negotiable.

Add up every monthly debt before applying for pre-approval: car loans, credit cards, student loans, and personal loans. Then calculate your maximum mortgage payment by taking your gross monthly income, multiplying by 0.44, and subtracting your existing debts. This gives you the actual ceiling lenders will work within. Many first-time buyers underestimate their existing obligations, then face shock when pre-approval comes in lower than expected. Pay down high-interest debt aggressively in the months before applying for pre-approval. Eliminating even one car payment or credit card can increase your approved mortgage amount by $50,000 to $100,000.

What Comes Next in Your Mortgage Journey

Your financial readiness determines not just whether you qualify for a mortgage, but what terms you’ll receive. Once you’ve assessed your credit, calculated your down payment capacity, and confirmed your debt-to-income ratio, you’re ready to explore the mortgage options available to you.

Navigating Mortgages and Financing Options

Fixed-Rate vs Variable-Rate Mortgages: Which Protects Your Budget?

The mortgage rate you select determines your payment stability and total interest cost over 25 years, yet most first-time buyers treat it as an afterthought. Fixed-rate mortgages lock in your interest rate for the entire term, meaning your payment stays identical whether rates climb or fall. Variable-rate mortgages tie your rate to the prime lending rate, so your payment fluctuates with market conditions. The Bank of Canada held rates at 5% in early 2024, and historically, variable rates save borrowers 0.5% to 1.5% compared to fixed rates during stable periods.

However, if you can’t absorb payment increases of $200 to $400 monthly without stress, fixed rates eliminate that uncertainty. On a $350,000 mortgage, a 5.5% fixed rate costs roughly $1,982 monthly, while a 4.75% variable rate starts at $1,851-but could rise to $2,100 if rates climb 1%. The math favors variable rates only if you have breathing room in your budget and can handle volatility. Most first-time buyers lack that flexibility, making fixed rates the smarter choice despite their higher starting rate.

How Mortgage Brokers Access Better Rates

Your mortgage broker becomes invaluable at this stage because they access rates from major banks and alternative lenders that you cannot negotiate independently. A complete step-by-step guide walks you through mortgage requirements and insider strategies to secure approval. The difference between a 5.4% and 5.2% rate on a $350,000 mortgage adds up to $7,000 in extra interest over five years.

Closing Costs and Hidden Expenses That Catch Most Buyers Off Guard

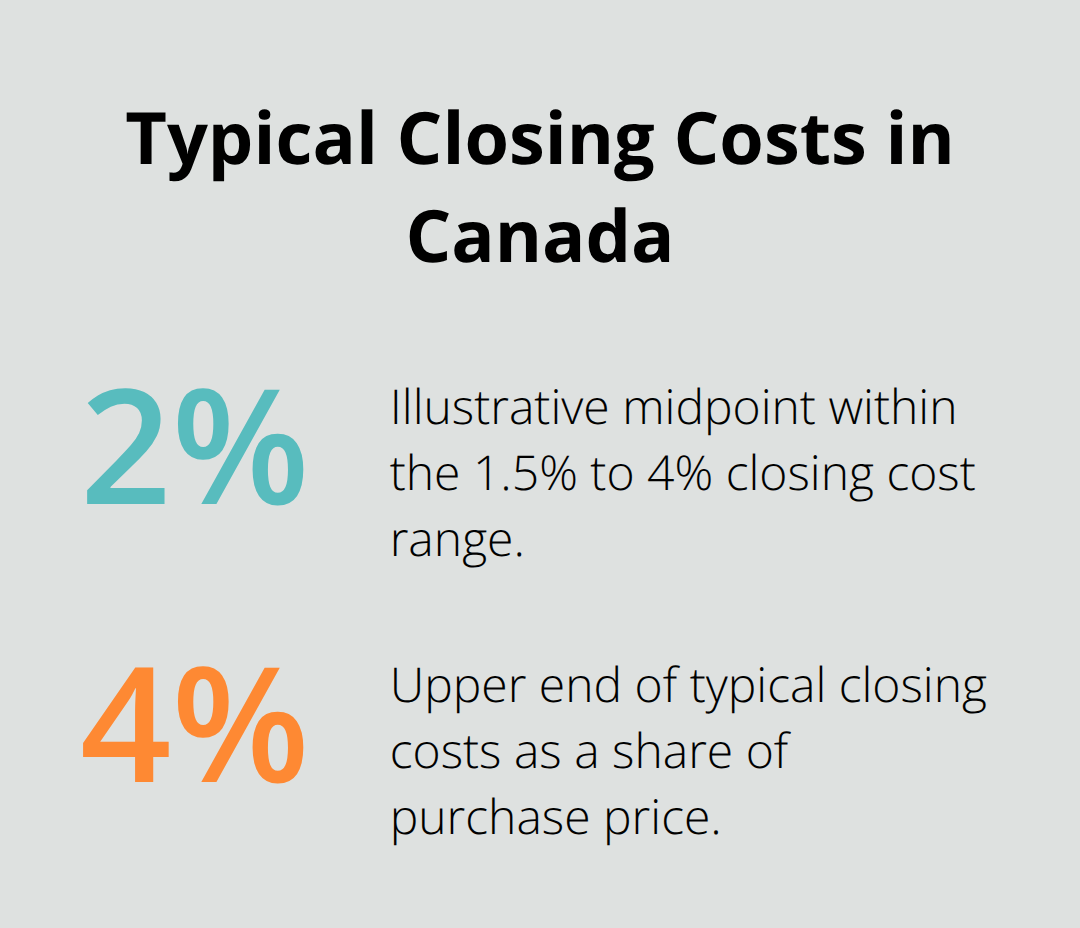

Beyond rates, closing costs and hidden expenses consume between 1.5% and 4% of your home’s purchase price. Home inspection costs run $300 to $1,000 and reveal structural issues that directly impact your negotiating power. Land survey costs typically range from $1,000 to $2,000 when lenders require confirmation of property boundaries. Legal fees from a real estate lawyer or notary cost $900 to $2,000 and cover purchase agreement review, mortgage documents, and title verification.

Title insurance protects against defects or fraud and costs $200 to $500. Land transfer tax varies dramatically by province-Ontario charges roughly $6,475 on a $500,000 property, while Alberta, Saskatchewan, Yukon, and Nunavut charge nothing. New home warranties are mandatory in British Columbia, Ontario, and Quebec, with Ontario coverage costing $385 to $1,800 (though builders often absorb this cost).

Getting a Complete Picture Before You Commit

Request a detailed closing cost estimate from your lender and lawyer before committing, then add 10% as a safety buffer because unexpected adjustments for utilities and property taxes frequently emerge at closing. This preparation positions you to move forward confidently when you find the right property and need to act quickly on your offer.

The Home Search and Purchase Process

Get Pre-Approved for Your Mortgage

Pre-approval transforms you from a casual browser into a serious buyer that sellers take seriously. You should obtain pre-approval before you start house hunting because it shows sellers your financing is confirmed and you can close quickly. Most lenders provide pre-approval within 24 to 48 hours, and it typically remains valid for 90 to 120 days. During pre-approval, the lender verifies your income, pulls your credit report, and confirms your debt-to-income ratio matches what you disclosed. This pre-approval letter states your maximum borrowing amount, but that ceiling doesn’t mean you should spend it all. A pre-approval for $450,000 doesn’t obligate you to buy a $450,000 home if your actual budget comfortably sits at $350,000.

Many first-time buyers attach themselves emotionally to their maximum approval amount and overextend themselves. Stick to what feels sustainable for your lifestyle and emergency fund, not what lenders technically allow you to borrow.

Work with a Real Estate Agent

A real estate agent serves as your tactical advantage because they access properties before they hit public listings and negotiate on your behalf. You should interview at least three agents and ask specifically how many first-time buyer transactions they closed in the past year. An agent experienced with first-time buyers understands your timeline pressures and guides you through common mistakes. When you find a property, your agent prepares the purchase offer and manages negotiations with the seller’s agent. This partnership accelerates your search and protects your interests throughout the transaction.

Make an Offer and Complete Due Diligence

Before you submit any offer, you must conduct due diligence that protects your investment. Schedule a home inspection within 72 hours of your offer acceptance; inspectors identify foundation issues, roof damage, electrical problems, and plumbing defects that could cost thousands to repair. The inspection contingency in your offer allows you to renegotiate the price downward or walk away if major problems surface. Many sellers in competitive markets push buyers to waive inspections, but this gamble destroys first-time buyers financially.

Land surveys confirm property boundaries and typically cost $1,000 to $2,000; your lender may require one, or your lawyer can advise whether your specific property needs this protection. Title searches verify the seller actually owns the property free of liens or claims against it. Your real estate lawyer handles this search and title insurance, protecting you against fraud or defects discovered after closing. You must move deliberately through these steps because rushing through due diligence to beat competing offers leads to expensive surprises after you own the property.

Final Thoughts

Your financial readiness determines your entire trajectory as a first-time homebuyer in Canada. A credit score above 720, a down payment of at least 10%, and controlled debt payments position you to access better rates and approval amounts that match your actual budget. The Home Buyer’s Plan, First Home Savings Account, and provincial tax rebates provide legitimate pathways to boost your down payment without overextending yourself, so calculate what you can realistically afford and stick to that number even when pre-approval letters suggest you could borrow more.

The mortgage you select shapes your monthly budget for 25 years, making this decision far more important than most first-time homebuyers Canada realize. Fixed-rate mortgages eliminate payment uncertainty, while variable rates save money only if your budget absorbs rate increases without stress. Mortgage brokers access rates from multiple lenders and typically charge no upfront fee if you’re well qualified, making them invaluable for securing better terms than you’d negotiate independently.

Due diligence protects your investment after you make an offer because home inspections reveal costly structural problems before you commit, land surveys confirm boundaries, and title searches verify the seller actually owns the property. These steps cost money upfront but prevent far more expensive surprises after closing. Start by gathering your financial documents, checking your credit report, and contacting a mortgage broker to understand your pre-approval amount, then interview real estate agents who specialize in first-time buyers and begin your search with realistic expectations about your budget and timeline. We at Financial Canadian support your journey with expert resources and guidance to help you establish confidence in your homeownership decision.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment