Personal loans can help you cover unexpected expenses, consolidate debt, or fund a major purchase. At Financial Canadian, we know that Canada personal loan options vary widely in terms of rates, terms, and eligibility requirements.

The right loan depends on your financial situation, credit score, and borrowing needs. This guide walks you through the main types available and how to compare them effectively.

Types of Personal Loans Available in Canada

Unsecured Personal Loans: Speed Over Collateral

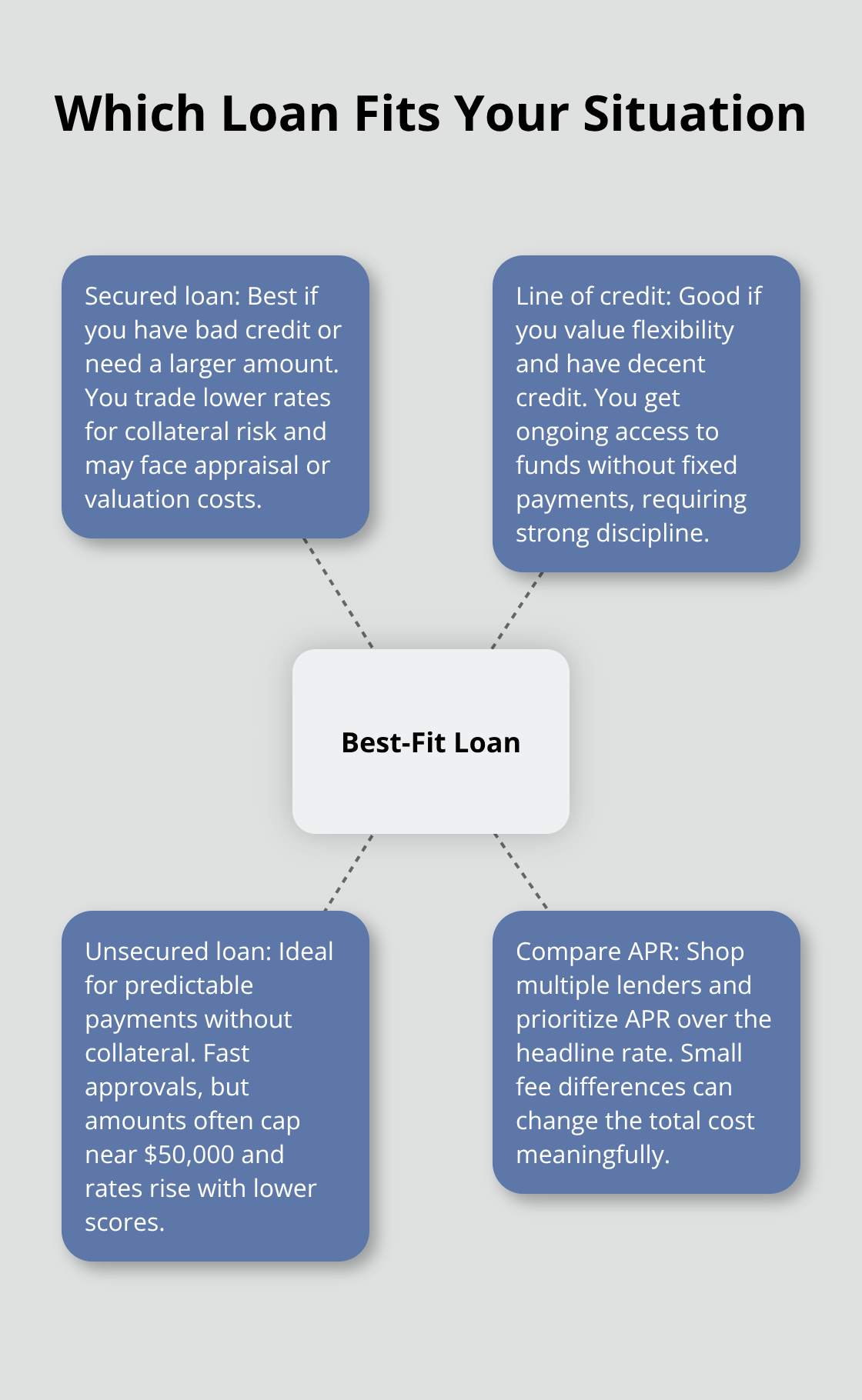

Unsecured personal loans rank as the most common option in Canada. Banks like CIBC offer fixed or variable rates with terms from 1 to 5 years for borrowers with solid credit, while alternative lenders may charge higher rates depending on your profile. The real advantage lies in speed and simplicity-you don’t need collateral, and online lenders can approve you within minutes. However, this convenience carries a cost. Unsecured loans cap out around $50,000 with most lenders, and if your credit score sits below 650, expect rates closer to 20% or higher. The Bank of Canada held the overnight rate at 2.25% in January 2026, which influences how banks price these loans. If you consolidate debt or cover an unexpected expense, unsecured loans work well, but only if your credit score reaches 650 or above. Below that threshold, the interest you’ll pay makes other options more attractive.

Secured Personal Loans: Lower Rates With Asset Risk

Secured personal loans backed by collateral like your home or vehicle offer much lower interest rates than unsecured loans. CIBC’s Home Power Plan, for example, lets you borrow at least $10,000 using home equity, with rates tied to the CIBC Prime rate. The catch is real: if you default, the lender can seize your collateral. This trade-off appeals to borrowers who own substantial assets and want to access larger amounts at competitive rates. The property valuation fee ($300 for CIBC’s Home Power Plan) adds to your upfront costs, so calculate whether the rate savings justify the expense.

Lines of Credit: Flexibility Without Fixed Payments

Lines of credit sit between unsecured and secured loans. They give you ongoing access to funds without a fixed repayment schedule, which appeals to people who value flexibility over predictable monthly payments. CIBC offers lines of credit with rates typically lower than credit cards. The downside is that lines of credit don’t force you to repay on a schedule, which means some borrowers end up carrying balances longer than necessary and pay more interest overall. This flexibility works best for borrowers with strong discipline and clear short-term borrowing needs.

Which Option Fits Your Situation

If you have bad credit or need a larger amount, a secured loan makes sense despite the asset risk. If you value flexibility and have decent credit, a line of credit works. But if you want predictable payments and don’t own substantial collateral, stick with unsecured loans and shop aggressively across lenders to find the best rate for your situation. Your choice here shapes which factors matter most when you compare offers-and that comparison process is where most borrowers either win or lose money.

Key Factors to Compare When Choosing a Personal Loan

Interest Rates and APR: Look Beyond the Headline Number

Most borrowers fixate on interest rate alone and miss the real cost of borrowing. Interest rates and APR tells the complete story because it includes mandatory lender fees that increase the total cost of borrowing beyond the stated interest rate. A lender advertising 8% interest might actually cost you 10.5% APR once fees are factored in. Always compare APR across offers, not just the advertised rate. The Bank of Canada held the overnight rate at 2.25% in January 2026, which influences how banks price loans, but your personal rate depends heavily on your credit score and income.

If your score sits around 600 to 650, expect rates in the 15% to 25% APR range from alternative lenders. The Big Six banks typically advertise 6% to 24% APR for those with strong credit or existing banking relationships. Online lenders can respond within minutes, but their rates often climb higher because they accept riskier borrowers. Before you apply anywhere, check your credit score with Equifax Canada or TransUnion Canada. A score above 700 unlocks substantially better rates across all lenders, potentially saving you thousands over the loan term.

Repayment Terms and Flexibility: How Monthly Payments Shape Total Cost

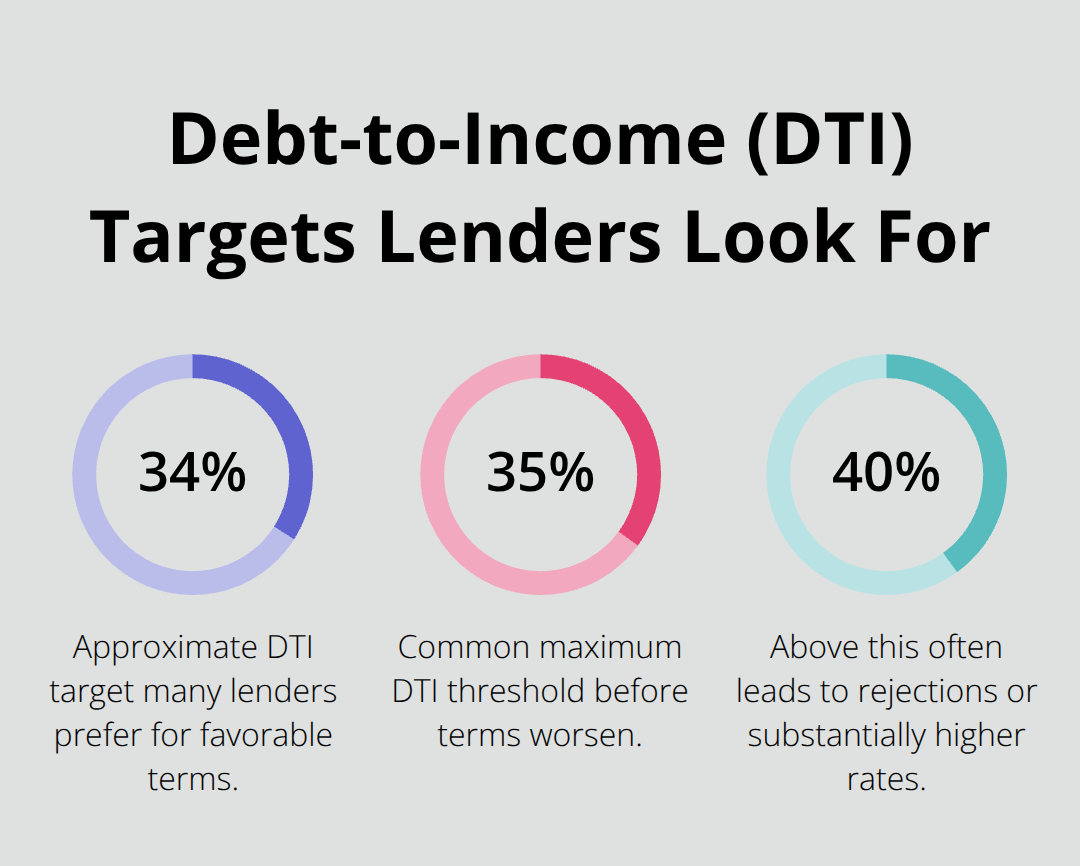

Repayment terms shape your monthly payment and total interest paid far more than most people realize. A five-year term spreads payments over 60 months, lowering your monthly obligation but increasing total interest. A two-year term cuts interest dramatically but demands higher monthly payments. Your debt-to-income ratio matters here: lenders typically want to see approximately 34% or less of your gross monthly income going toward debt payments before offering favorable terms. Calculate your DTI by dividing total monthly debt payments by gross monthly income. Most lenders want to see DTI below 35% before offering favorable terms.

Prepayment options vary wildly between lenders, so ask directly whether you can make extra payments or pay off the loan early without penalties. Some lenders impose prepayment penalties that cost hundreds of dollars, while others allow unlimited extra payments. If you think your financial situation might improve within two years, choose a lender offering penalty-free prepayment. Fixed-rate loans provide predictable payments that never change, while variable-rate loans follow Bank of Canada movements and can increase if Prime rises. Given the current economic uncertainty, fixed rates offer peace of mind, though variable rates sometimes start lower.

Fees and Hidden Costs: Calculate the True Total

Read the fine print on origination fees, monthly service fees, and any fees tied to late payments. A lender charging $0 origination fee but $15 monthly service fees can cost more than a lender charging 2% upfront. Gather loan offers from at least three different lenders before deciding, then calculate the total cost including all fees over the full term. This comparison reveals which lender actually costs the least, not which one sounds cheapest. Once you understand what separates a good offer from a bad one, the next step involves preparing your application materials and knowing exactly where to apply.

How to Apply for a Personal Loan in Canada

Check Your Credit Score and Financial Health

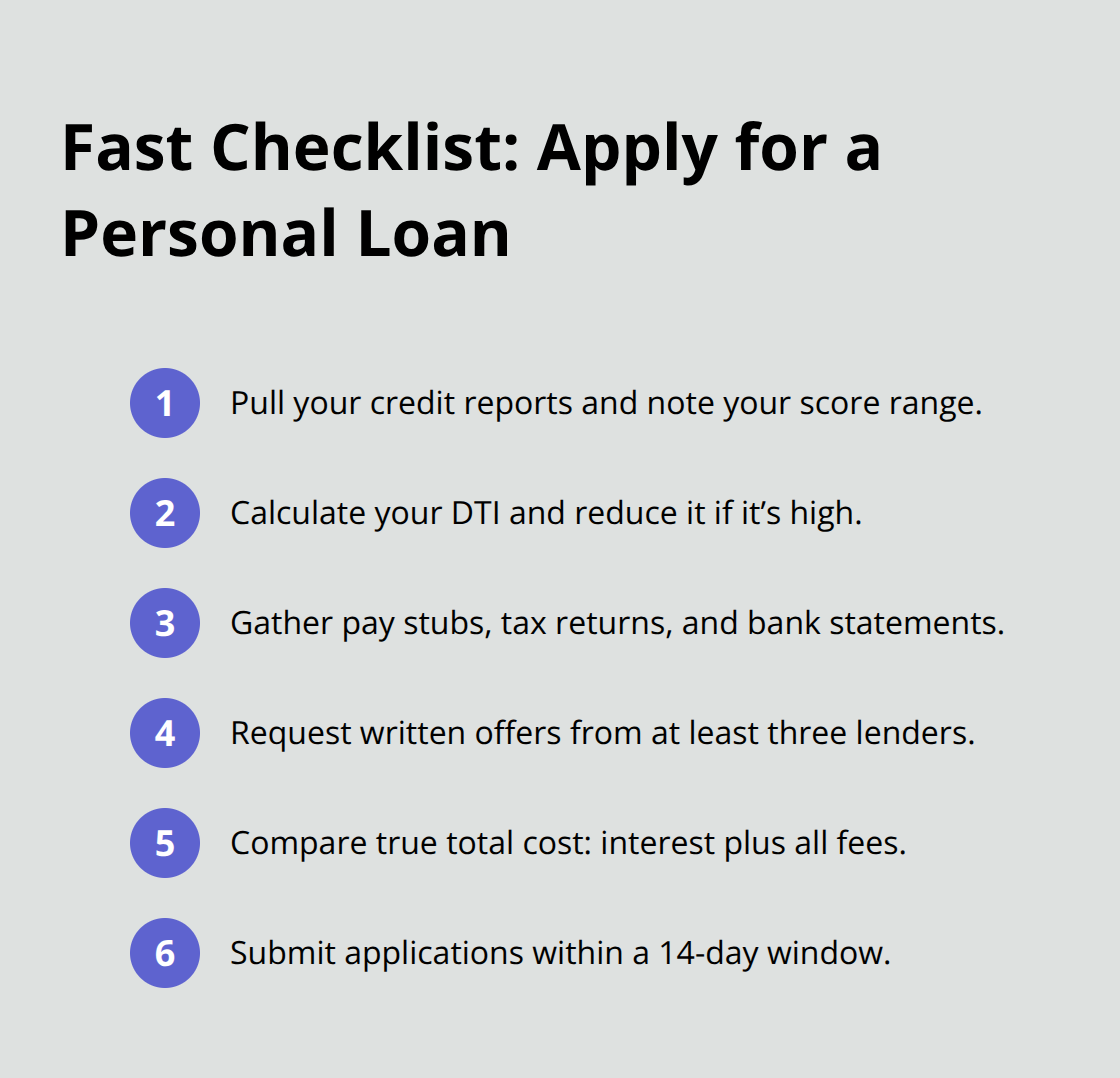

Pull your credit report from Equifax Canada or TransUnion Canada at least two weeks before applying anywhere. This action gives you time to spot errors and understand exactly what rate range you’ll qualify for based on your score. In Canada, a score of 660+ is good, and 760+ is excellent, unlocking better rates and loan terms. Each hard inquiry can temporarily lower your score by a few points, so knowing your score prevents wasted applications and protects your credit.

Calculate your debt-to-income ratio while you’re at it. Divide your total monthly debt payments by your gross monthly income. If that number exceeds 40%, focus on paying down existing debt before applying, because lenders will either reject you or charge substantially higher rates.

Gather Your Documentation

Collect your last two months of pay stubs, recent tax returns, and bank statements showing your account history. Online lenders move fastest and typically need these documents uploaded within minutes of application, while banks may request additional paperwork like employment letters or proof of address. Having everything organized before you start applications cuts your approval timeline from days to hours.

Compare Lenders and Their Specific Terms

Contact at least three lenders directly and ask specific questions about their terms rather than relying on advertised rates. Call CIBC at 1-866-294-5964 if you own a home and want to explore the Home Power Plan, which offers rates tied to Prime with a $300 property valuation fee but can save thousands compared to unsecured loans. For unsecured options, compare offers from at least one major bank, one online lender, and one credit union to see how rates and fees differ across the lending spectrum.

Ask each lender whether prepayment penalties exist, what their origination fees are as a percentage, and whether they allow extra payments without cost. Some lenders charge 0.5% origination fees while others charge 8%, and that difference compounds over your loan term.

Calculate Total Cost and Submit Applications

Once you have written offers from multiple lenders, calculate the total cost of each loan by adding the interest you’ll pay over the full term plus all fees, then divide by the loan amount to see the true cost per dollar borrowed. This number matters far more than the advertised interest rate.

Submit applications strategically within a two-week window so multiple inquiries count as a single inquiry for credit scoring purposes. Wait for decisions before committing to any lender.

Final Thoughts

Choosing the right personal loan in Canada requires matching your financial situation to the loan type that costs you the least over time. Unsecured loans work best if you have decent credit and want speed, secured loans make sense when you own collateral and need lower rates, and lines of credit suit borrowers who value flexibility over fixed payments. The real money-saving move happens when you stop comparing interest rates and start comparing APR across multiple lenders, because that single number tells you the true cost of borrowing.

Your credit score determines which Canada personal loan options are actually available to you. Pull your report from Equifax Canada or TransUnion Canada before applying anywhere, calculate your debt-to-income ratio, and gather your documentation. Then contact at least three lenders directly and ask about origination fees, prepayment penalties, and whether they allow extra payments without cost.

Submit applications within a two-week window so multiple inquiries count as a single hard inquiry on your credit report. Calculate the total cost of each offer by adding interest plus all fees, then compare that number across lenders rather than fixating on advertised rates. We at Financial Canadian help you compare loan offers and make informed borrowing decisions that align with your financial goals.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment