Getting a loan when your credit history is thin or damaged feels impossible. At Financial Canadian, we know that guaranteed loans Canada offer a real path forward for borrowers in this position.

A guarantor-whether a person or government program-backs your loan, which means lenders take on less risk. This opens doors to financing that would otherwise stay closed.

How Guaranteed Loans Actually Work in Canada

A guaranteed loan in Canada is straightforward: a third party repays the lender if you default. That third party can be a person (like a family member or friend) or a government program designed to reduce lender risk. The guarantor’s commitment changes everything about your approval odds. Without a guarantor, lenders view your thin or damaged credit as a deal-breaker. With one, they see a safety net that makes lending to you acceptable. This is why guaranteed loans exist-they’re not charity, they’re risk management that benefits both you and the lender.

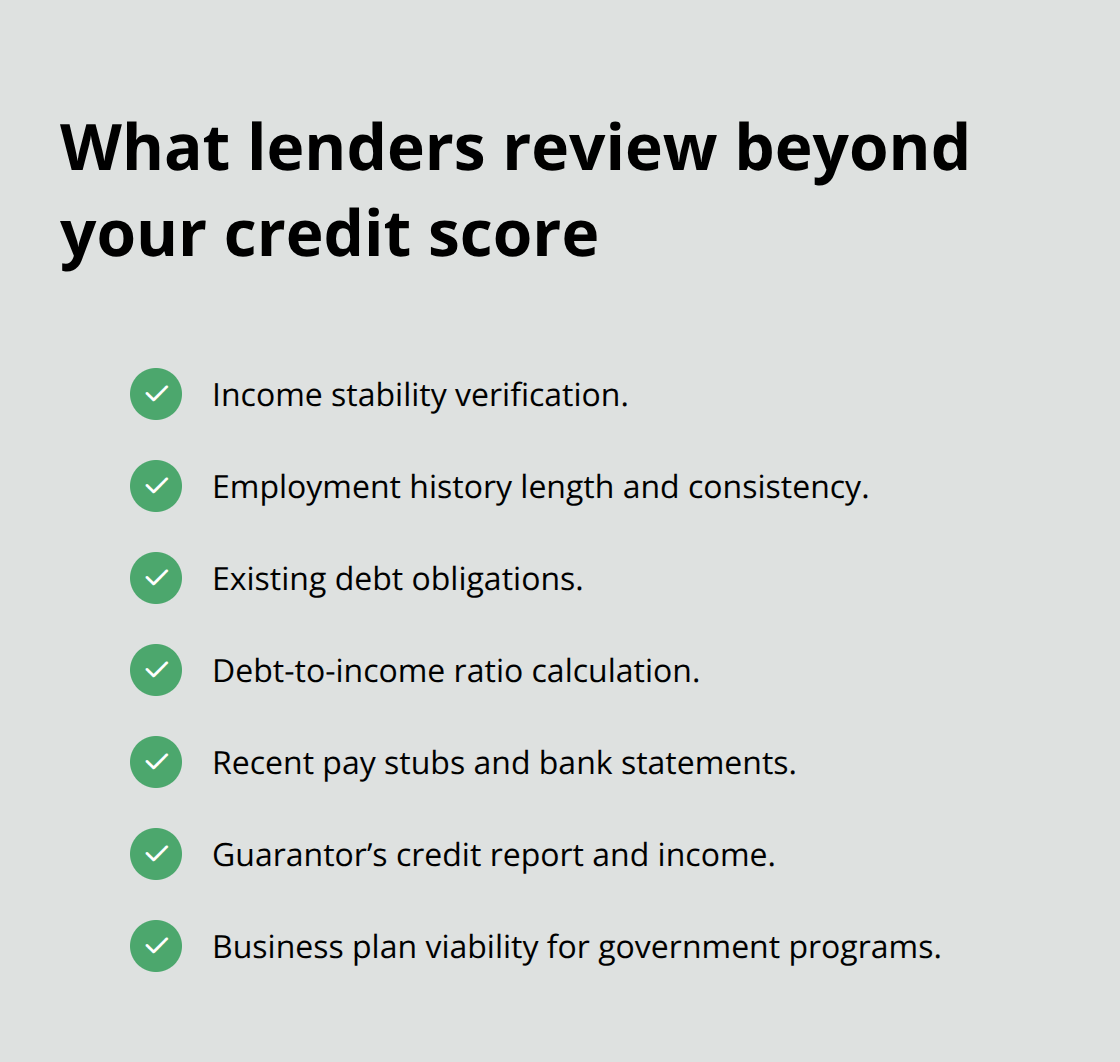

What Lenders Actually Examine Beyond Your Credit Score

Lenders examine far more than your credit score when you apply for a guaranteed loan. They assess your income stability, employment history, existing debt obligations, and your ability to repay on schedule. If you have a personal guarantor, they pull that person’s credit report and verify their income too. Government-backed loan guarantee programs like the Canada Small Business Financing Program use their own assessment criteria, often focusing on your business plan viability rather than perfect credit.

Lenders weight multiple factors beyond your credit history. A person with a 550 credit score but steady employment and a strong guarantor often receives approval faster than someone with a 650 score but inconsistent income. Many alternative lenders in Canada now prioritize income verification and debt-to-income ratios over credit scores. Your employment letter, recent pay stubs, and bank statements matter as much as your credit file.

Personal Guarantees: How They Work

Personal guarantees are the most common type. A family member, friend, or business partner signs a legal document stating they’ll cover your debt if you can’t. They take on full liability, so their credit and finances face risk if you miss payments. This arrangement works best when you have someone trustworthy willing to back you. The guarantor’s strong credit profile and stable income significantly improve your approval chances and often lower your interest rate.

Government-Backed Guarantees and Secured Options

Government guarantees operate differently than personal ones. Programs like the Small Business Loans Act guarantee a portion of a loan amount, reducing the lender’s exposure substantially. These programs suit small business owners who meet specific criteria. Secured guarantees tie the loan to an asset you own-your home, vehicle, or business equipment serves as collateral. If you default, the lender can seize that asset. Unsecured guarantees (whether personal or government-backed) don’t require collateral, but they carry higher interest rates to offset the lender’s increased risk.

The Canada Revenue Agency also offers loan guarantee programs for specific purposes like equipment purchases or working capital. Provincial programs vary significantly. Ontario’s Ontario Small Business Support Program and British Columbia’s Community Futures Program each have different guarantee structures and eligibility rules.

Matching the Right Guarantee Type to Your Situation

Secured guarantees make sense if you have assets and want lower interest rates. Government guarantees suit small business owners who meet specific program criteria. Personal guarantees work best when you have someone trustworthy willing to back you. Your choice depends on what assets you control, who can support your application, and which programs you qualify for. Understanding these distinctions helps you move forward with confidence toward the right lender and guarantee structure for your needs.

When Guaranteed Loans Actually Help Your Financial Situation

Guaranteed loans solve specific financial problems, but they’re not right for everyone. The real question is whether your situation matches what guaranteed loans deliver. If you’re stuck in a credit trap, need access to larger amounts, or launching a business with limited personal history, guaranteed loans can work. If you’re simply looking for the cheapest possible rate, they won’t be. Honesty about when these loans make sense prevents costly mistakes.

Credit damage and rebuilding strategies

A damaged credit score feels like a permanent barrier, but guaranteed loans create a legitimate path forward. Your score dropped because of missed payments, high utilization, or collections, and traditional lenders won’t touch you. A guaranteed loan from an alternative lender paired with a strong guarantor changes that calculation entirely. The guarantor’s solid credit profile reduces the lender’s risk substantially, which means you qualify despite your past mistakes.

Statistics Canada data shows roughly 6 million Canadians carry credit scores below 650, yet most of them can still access financing through guarantees. Once you secure the guaranteed loan, making on-time payments for 12 to 24 months begins rebuilding your score immediately. Each payment reported to Equifax and TransUnion strengthens your history. After two years of perfect payments on a guaranteed loan, many borrowers see their scores improve by 80 to 120 points, which opens doors to better rates on future borrowing.

The strategy works only if you treat the guaranteed loan as a rebuilding tool, not another source of quick cash you can’t repay. Your commitment to on-time payments matters more than the loan amount itself.

Larger Amounts Become Accessible When You Have a Guarantor

Traditional banks cap unsecured personal loans around $15,000 to $25,000 for borrowers with weak credit, and they often deny applications outright. A guarantor changes those limits dramatically. Lenders view the guarantor’s income and assets as backup repayment sources, which means they’ll approve loans of $30,000, $50,000, or higher depending on the guarantor’s financial strength.

This matters for real situations like consolidating $40,000 in high-interest credit card debt or covering a major home repair that costs $35,000. Without a guarantor, you’d be stuck with payday loans at 365% APR or credit cards charging 21% annually. With a guarantor, you access rates between 12% and 22%, which saves thousands in interest over the loan term.

The guarantor’s income matters more than yours at this stage because the lender treats their earnings as the primary repayment source. If your guarantor earns $65,000 annually and has a debt-to-income ratio below 44%, lenders typically approve significantly larger amounts than your solo income would support. This structure works best when the guarantor is genuinely willing to back you and understands their legal liability.

Business Launches Need Government Backing, Not Personal Guarantors

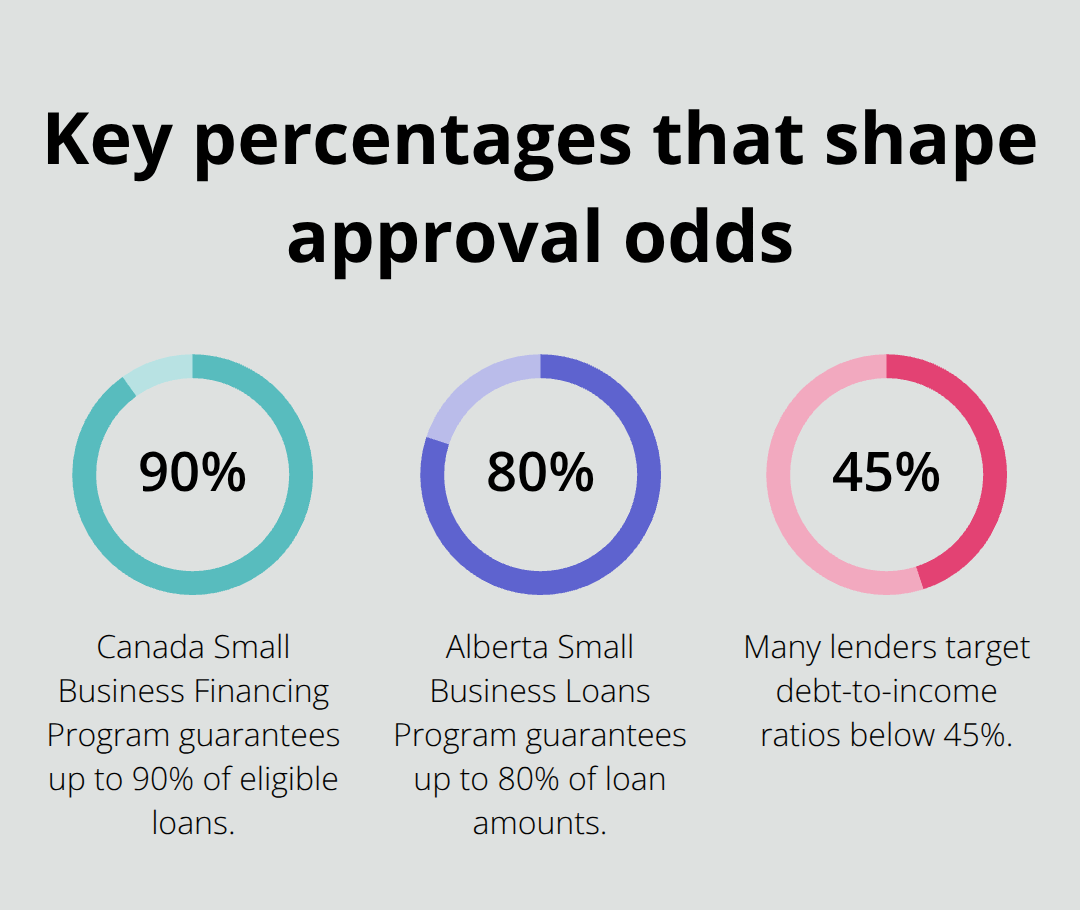

Starting a business with minimal personal credit requires government-backed guarantees, not personal ones. The Canada Small Business Financing Program guarantees up to 90% of loan amounts up to $1 million for eligible businesses, which means the government absorbs most of the lender’s risk. This program exists specifically because banks won’t lend to first-time business owners without established track records.

Your personal credit score barely matters under this program because the lender focuses on your business plan’s viability, market research, and cash flow projections. Qualification requires a detailed business plan, proof of business registration, and a minimum 10% equity stake in the business. The government guarantee covers the lender’s risk, not yours, which means you still repay the full loan amount.

Interest rates typically run between 6% and 8%, far below what you’d pay without the guarantee. Provincial programs like Ontario’s Ontario Small Business Support Program offer similar structures with slightly different criteria and guarantee percentages. If you’re launching a business and your personal credit sits below 650, pursuing a government-backed guarantee beats trying to find a private lender willing to take the risk.

Understanding which guarantee type matches your situation positions you to move forward with the right lender and loan structure. The next section examines the specific guaranteed loan products and providers available across Canada, helping you identify which options align with your financial goals.

Guaranteed Loan Products Available Across Canada

The Canada Small Business Financing Program remains the dominant government-backed option, guaranteeing up to 90% of loans reaching $1 million for eligible businesses. Participating banks and lenders administer this program, so you apply directly to a financial institution rather than the government. Interest rates typically fall between 6% and 8%, substantially lower than private alternatives. The program requires a detailed business plan, proof of business registration, and minimum 10% equity in your venture. Processing timelines range from two to four weeks once you submit a complete application. If your business operates in manufacturing, retail, services, or professional sectors, this program likely applies to you. However, the program excludes certain industries like real estate investment and lending businesses, so verify your sector’s eligibility before investing time in the application.

Provincial Programs Offer Location-Specific Advantages

Provincial programs add another layer of options depending on where you operate. Ontario’s Ontario Small Business Support Program guarantees portions of loans for businesses meeting specific criteria, while British Columbia’s Community Futures Program targets rural and smaller communities with tailored guarantee structures. Alberta’s Alberta Small Business Loans Program operates similarly, guaranteeing up to 80% of loan amounts. These provincial variations mean your approval odds and rates shift significantly based on location. A business owner in rural British Columbia might qualify for better terms through Community Futures than through the federal program alone.

Private Lenders Provide Flexible Guarantee Products

Private lenders offering guaranteed products include Spring Financial, which provides personal loans up to $35,000 with APRs between 9.99% and 34.95%, and easyfinancial, offering unsecured loans from $500 to $20,000 with more flexible income requirements than traditional banks. Fairstone extends unsecured loans up to $25,000, while homeowners can access secured loans up to $150,000 at lower rates. GoPeer, a peer-to-peer lender, offers loans up to approximately $35,000 with rates starting around 8.99% and funding within roughly one week.

Comparing Rates, Timelines, and Eligibility Across Providers

Comparing these options requires examining three specific factors: your interest rate relative to your credit profile, the actual funding timeline, and whether the lender’s assessment criteria match your financial situation. A borrower with a 580 credit score qualifies more easily with easyfinancial’s income-focused approach than Spring Financial’s credit-weighted model. If you need funds within days rather than weeks, GoPeer’s week-long timeline beats the two to four weeks typical for government programs.

Debt-to-Income Ratios Determine Your Approval Odds

Your debt-to-income ratio matters heavily across all providers, with most targeting ratios below 45%. This means if you earn $4,000 monthly, keeping total monthly debt payments under $1,760 significantly improves approval odds and rates. Lenders treat this metric as a primary qualification threshold because it demonstrates your capacity to absorb a new loan payment without financial strain.

Final Thoughts

Guaranteed loans in Canada solve a real problem that traditional banks ignore: lenders won’t approve you without a safety net, but that safety net exists and is accessible. Whether you’re rebuilding credit after past mistakes, accessing larger amounts than your solo income supports, or launching a business with minimal personal history, guaranteed loans Canada provide a legitimate financing path when traditional banks say no. The decision to pursue one comes down to honest self-assessment about whether your situation matches what these loans deliver.

If you’re stuck with damaged credit and need to rebuild, a guaranteed loan with on-time payments over 12 to 24 months genuinely improves your score by 80 to 120 points. If you need $40,000 to consolidate high-interest debt and a guarantor can back you, rates between 12% and 22% beat payday loans at 365% APR. If you’re starting a business, government-backed programs guarantee up to 90% of loans, making approval possible despite thin personal credit.

Calculate your debt-to-income ratio by dividing your total monthly debt payments by your gross monthly income, and identify which guarantee type matches your situation (personal guarantor for larger personal loans, government programs for business financing, or secured guarantees if you own assets). At Financial Canadian, we help borrowers understand their financing options through clear, practical guidance about loans and credit strategies. Start your search by gathering your financial documents, identifying potential guarantors or programs you qualify for, and contacting lenders directly with your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment