Mortgage rates in Canada are shifting, and homeowners need to understand what’s happening right now in 2026. At Financial Canadian, we’ve tracked how these changes affect your wallet and your options.

Whether you’re renewing soon or planning ahead, the decisions you make today will shape your financial reality for years. This guide walks you through what’s driving rates, where they’re headed, and exactly how to prepare.

Where Canadian Mortgage Rates Stand Right Now

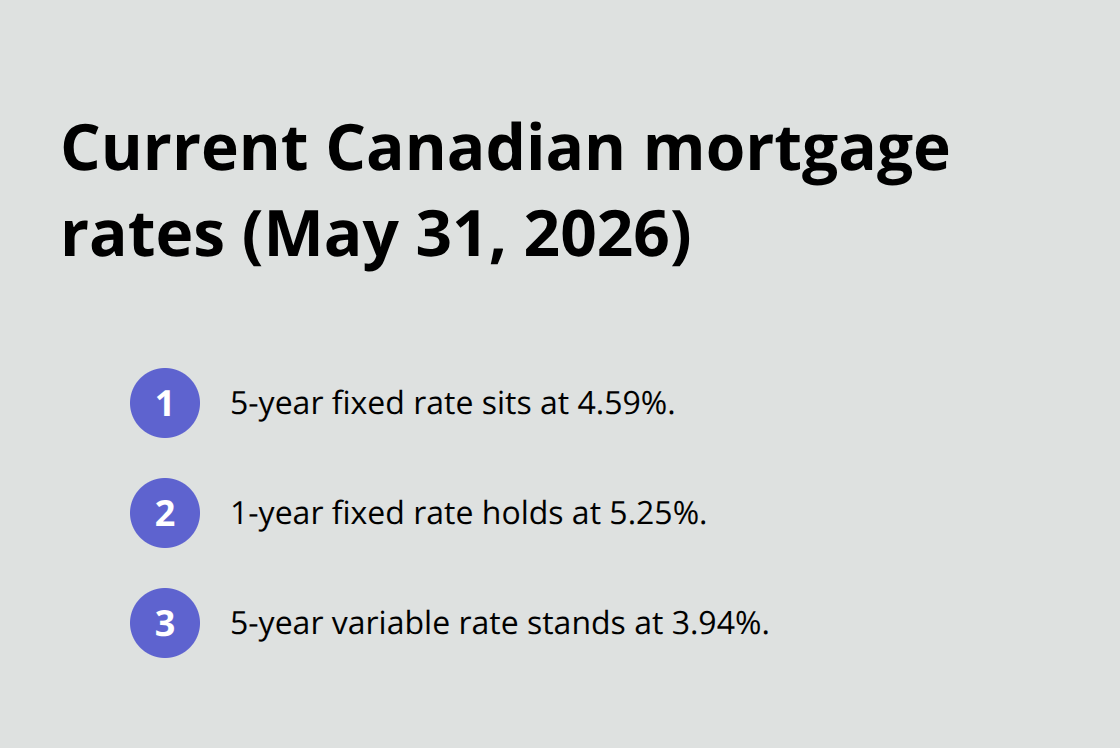

As of May 31, 2026, Canada’s mortgage landscape shows relative stability with modest movement across terms. The 5-year fixed rate sits at 4.59%, down slightly from earlier in the year, while 1-year fixed rates hold at 5.25% according to the WOWA rate table that tracks major lenders like RBC, TD, Scotiabank, BMO, CIBC, National Bank, Desjardins, nesto, Tangerine, and First National. The 5-year variable rate stands at 3.94%, offering a 65 basis point discount to fixed alternatives.

This pricing reflects the Bank of Canada’s policy rate locked at 2.25% and the prime rate at 4.45%. What matters more than the absolute numbers is what these rates mean for your wallet: a typical $520,000 mortgage at 4.2% over 25 years costs roughly $2,790 monthly, representing approximately 45% of median after-tax household income. That affordability squeeze is real, and it’s why rate selection matters intensely right now.

Fixed Rates Lock Your Payment; Variable Rates Offer Savings Today

Fixed-rate mortgages lock your payment in place regardless of what the Bank of Canada does, making budgeting straightforward but potentially expensive if rates fall. The trade-off is security: you pay more upfront to eliminate the risk of payment shock. Variable-rate mortgages track the lender’s prime rate, currently sitting 2.2 percentage points below the 2024 peak, meaning variable rates have room to move higher before hitting recent highs. Most variable mortgages hold payments constant while the interest-to-principal split shifts when rates change, so you pay more interest and less principal as rates rise. The forward rate curves from CORRA-based projections suggest the policy rate may drift toward 2.75% by late 2026 or 2027, which would push variable rates higher. If you’re risk-averse and plan to stay in your home beyond five years, fixed rates eliminate guesswork. If you believe rates will stay low or you can handle payment increases, variable rates save you money today. Don’t choose based on rate alone-lenders’ prepayment flexibility, portability, and penalty structures often matter more to total cost than the headline rate itself.

Regional Markets Show Divergent Cooling Trends

Vancouver and Fraser Valley experienced pronounced cooling from 2021 to 2025, with Vancouver detached homes declining from approximately $1.91 million to $1.88 million while condos dropped from $761,800 to $710,000. Fraser Valley detached homes fell from roughly $1.50 million to $1.39 million. Inventory levels remain elevated: Vancouver listed about 65,335 homes in 2025 and Fraser Valley about 37,963, with homes taking months to sell rather than weeks. Sales activity reflects this shift too-Vancouver saw approximately 23,800 sales in 2025 compared to 44,000 in 2021, while Fraser Valley dropped from 28,000 to 12,224. The Vancouver Real Estate Board economist Andrew Lis forecasts around 27,000 sales for Vancouver in 2026, suggesting modest recovery but nothing approaching the 2021 frenzy.

Renewal Pressure Hits Hard Across Canada

This regional context matters because it affects renewal timing. CMHC mortgage renewals forecast 1.15 million in 2026 across Canada, with Vancouver experiencing pronounced pressure from borrowers who locked in 2% rates in 2021 and now face rates near 4.6%. A typical renewal could see monthly payments rise by about 26% if rates moved from 2% to 4%, creating genuine budget stress for households that didn’t plan for this scenario. The renewal wave will test whether Canadian homeowners can absorb these payment shocks or whether they’ll need to extend amortization periods, consolidate debt, or explore other relief options. Understanding your renewal date and rate environment now positions you to make informed decisions rather than scrambling when your term expires. The next section examines the economic forces that will shape whether rates climb further or stabilize through the remainder of 2026.

What’s Driving Mortgage Rates Higher in 2026

The Bank of Canada’s Balancing Act

The Bank of Canada held its policy rate at 2.25% in April 2026, but this pause masks real tension underneath. April inflation climbed to 2.8% year-over-year while core inflation cooled to 2.1%, creating a mixed signal that keeps the central bank cautious. Energy prices surged roughly 19% and gasoline jumped about 29% year-over-year, driven partly by geopolitical risk in the Middle East. This energy-driven inflation matters directly to your mortgage rate because persistent price pressure could force the Bank of Canada to raise rates again, pushing your renewal costs higher.

The unemployment rate rose to 6.9% in April 2026 with 17,700 fewer jobs added that month, signaling economic softening that might normally support rate cuts. However, wage growth held firm at 4.5% year-over-year, which keeps inflation expectations sticky and prevents the central bank from easing aggressively. Canada’s first-quarter GDP contracted 0.1% annualized, with Q4 2025 revised down to -1.0%, raising genuine questions about whether the economy has enough strength to justify holding rates steady much longer.

What Rate Forecasts Tell Us

The forward rate curves based on CORRA projections suggest the policy rate could drift toward 2.75% by late 2026 or early 2027, but major banks remain split on timing. RBC expects rates near 2.25% through 2026 then up to 3.25% by end-2027, while TD projects the rate staying at 2.25% through 2027 and Scotiabank forecasts 2.75% by 2027. This disagreement among major lenders tells you that rate direction remains genuinely uncertain, which is why locking in a fixed rate now has real value if you’re renewing soon.

Tariffs and Global Pressures Complicate the Picture

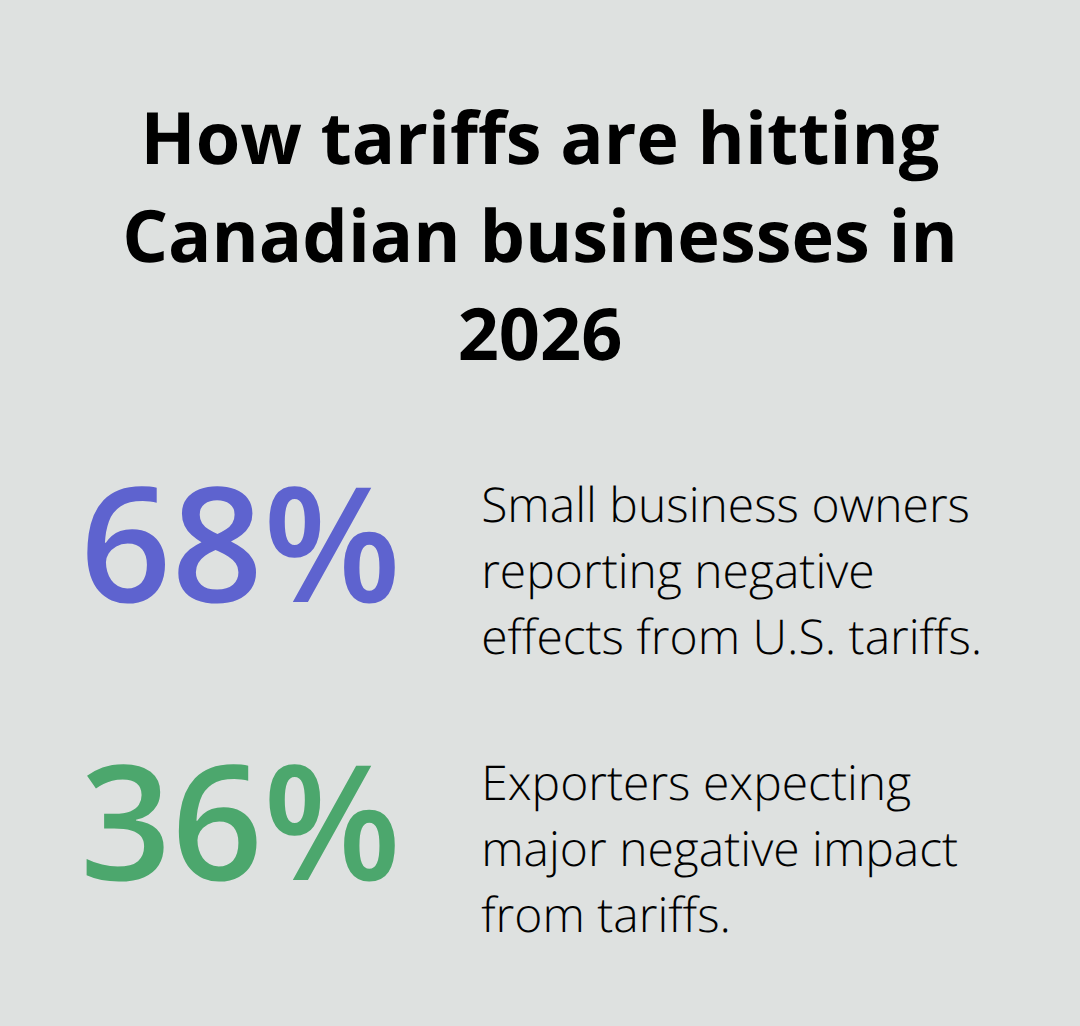

Global conditions are making this uncertainty worse, not better. Tariffs on non-CUSMA goods contribute measurably to inflation, with 68% of Canadian small business owners reporting negative effects from U.S. tariffs. Thirty-six percent of exporters expect tariffs to have major negative impact on their operations, which filters through to wage pressures and inflation expectations.

The 2026 CUSMA review will likely be lengthy and contentious, adding prolonged uncertainty that could keep long-term yields elevated.

The 5-year Government of Canada bond yield stood at 2.75% as of March 20, 2026, and this yield directly influences your fixed mortgage rate. If bond yields ease because inflation pressures soften or the U.S. economy slows, fixed mortgage rates could move slightly lower. Conversely, if tariff-driven inflation persists or energy prices spike further, bond yields will climb and your mortgage renewal rate will follow upward.

How to Monitor What Matters

Monitoring Statistics Canada CPI releases and Bank of Canada announcements matters more than checking rates daily. The neutral rate, where policy is neither stimulative nor restrictive, sits somewhere in the 2.25% to 3.25% range according to the central bank, meaning rates have room to move in either direction depending on how inflation and growth evolve. Your practical move right now is to run rate scenarios for your renewal assuming rates could reach 3.5% to 4.0%, then assess whether you can handle those payments or need to extend your amortization period to bridge the gap. Understanding these economic forces positions you to make strategic decisions about your renewal timing and rate type, which we’ll explore in the next section.

Securing Your Rate Before Uncertainty Deepens

The smartest move right now is to lock in your rate if you’re renewing within the next six months, and here’s why the math supports acting now rather than waiting. If you hold a variable rate mortgage and rates climb to 3.5% or 4.0% by late 2026, your payments won’t spike immediately, but your interest-to-principal split shifts dramatically-you pay more toward interest and less toward building equity. A $520,000 mortgage at 3.94% versus 4.6% costs roughly $170 more monthly, which compounds to over $2,000 annually on a five-year term. Major banks expect the overnight policy rate to stay at 2.25% in 2026 and rise to 3.25% by end-2027, creating genuine urgency for borrowers whose terms expire in the next 12 months.

Shop Around With a Mortgage Broker

Don’t wait for certainty that won’t come. Instead, shop around with a mortgage broker rather than accepting your bank’s renewal offer directly. Brokers access rates across multiple lenders including RBC, TD, Scotiabank, BMO, CIBC, National Bank, Desjardins, nesto, Tangerine, and First National, often securing rates 0.25% to 0.50% lower than what your current lender offers. The difference on a $520,000 mortgage over five years adds up to thousands in savings.

When comparing offers, ignore the advertised rate and focus on penalties, portability, and prepayment flexibility instead. A low headline rate with brutal penalties or zero portability costs you far more than a slightly higher rate with genuine flexibility. If your renewal would spike payments by more than 25%, discuss extending your amortization period with your broker now rather than accepting whatever your lender proposes at renewal. Extending from 25 years to 30 years eases monthly pressure but increases total interest paid, so this is a tactical bridge, not a permanent solution.

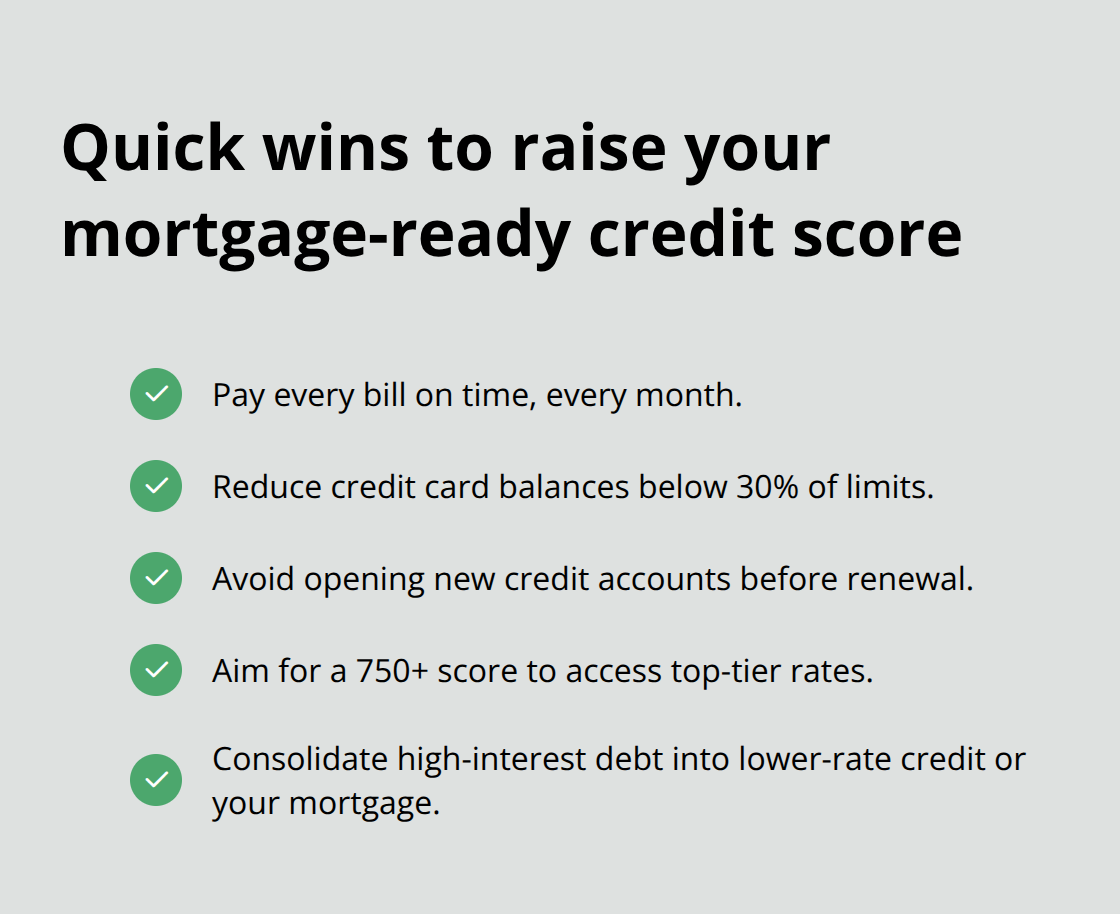

Improve Your Credit Score Now

Your credit score directly influences which rates you qualify for, and improvement takes time, so act now if yours sits below 750. Lenders view scores above 750 as low-risk, unlocking their best rates, while scores between 650 and 749 attract rate premiums of 0.25% to 0.75% depending on the lender. Raising a 700 score to 760 takes roughly three to six months of disciplined behavior: pay all bills on time, reduce credit card balances to below 30% of your limits, and avoid opening new accounts before your renewal.

On a $520,000 mortgage, a 0.50% rate improvement saves roughly $130 monthly or $7,800 over five years. If cash flow is tight ahead of renewal, consolidate high-interest debt like credit cards into your mortgage or a line of credit at lower rates to reduce effective costs immediately. A credit card charging 19% interest becomes a mortgage-backed debt at 4.6%, cutting your rate in half. This consolidation strategy matters more than chasing minor rate improvements elsewhere.

Test Your Affordability at Higher Rates

Run detailed affordability scenarios assuming rates reach 4.0% on your renewal and calculate whether you can sustain those payments without cutting other expenses. Test your affordability at higher rates to determine your capacity before your term expires. If you can’t, extending amortization or consolidating debt now prevents scrambling later when your term expires and options narrow. The households that weather 2026’s renewal wave successfully are those making strategic decisions today, not those hoping rates fall or that their lender extends flexibility at renewal time.

Final Thoughts

The mortgage rates Canada 2026 environment demands action, not passivity. You face a renewal wave that will test household budgets across the country, with 1.15 million mortgages renewing this year alone. The Bank of Canada’s cautious stance at 2.25% masks real uncertainty about inflation, tariffs, and economic growth, meaning rate direction remains genuinely unpredictable.

Borrowers who lock in rates now, shop with brokers rather than accepting bank offers, and improve credit scores before renewal will navigate 2026 successfully. Those who wait for certainty or hope rates fall will face narrower options and higher costs when their terms expire. The households managing payment shock extend amortization strategically, consolidate high-interest debt into mortgages, and run affordability scenarios at 4.0% rates now rather than scrambling later.

Contact a mortgage broker within the next 30 days if you’re renewing within six months and request quotes across multiple lenders. We at Financial Canadian understand that navigating mortgage decisions requires reliable information and strategic planning, which is why we deliver responsive designs and SEO optimization to help financial professionals and homeowners build digital resources that support informed decision-making.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment