A same day loan in Canada can be the difference between covering an unexpected expense and falling behind on bills. We at Financial Canadian understand that emergencies don’t wait for traditional banking timelines.

This guide walks you through how same day loans work, their real costs, and where to find them across Canada. You’ll learn when they make sense and when other options might serve you better.

How Same Day Loans Get Approved and Funded

Same day loan providers in Canada operate with a fundamentally different approach than traditional banks. Most lenders offer fully online, paperless applications available 24/7, so you can apply at midnight on a Sunday when an emergency strikes. You provide basic personal information, proof of income, and bank account details, then verify your identity. Some lenders request bank statements or pre-authorized debit uploads if automation fails, but most handle the heavy lifting for you. The entire application process takes 10 to 15 minutes, a stark contrast to traditional banks that demand extensive documentation and multiple office visits.

What Lenders Actually Check

Same day loan providers focus on income verification rather than credit scores, which is why they approve applicants with poor credit histories. They accept various income types including employment, pensions, disability benefits, and child tax credits, though employment income typically requires a minimum of two months on the job. If you’ve been in a new position for less than two months, you should wait until you hit that milestone before applying. The lender verifies your income through bank deposits and employment records-a process that takes minutes rather than days.

They use bank-level encryption to protect your personal information, a security standard maintained since 2005 by major providers in this space. Approval happens in minutes because lenders have automated most verification steps and made high approval rates their business model.

Funding Speed and Methods

Once approved, funds hit your account remarkably fast. Most lenders deposit money via bank transfer or Interac e-Transfer within minutes after approval, though e-Transfers typically arrive within 1 to 2 minutes depending on your bank’s processing speed. Some institutions move slower than others, but you can expect funds available on the same day in nearly all cases. The loan amounts range from a few hundred to $1,500 depending on the lender and your province, with terms ranging from 42 to 62 days depending on where you live.

Understanding the Real Costs

Provincial loan fees are standardized at $14 per $100 borrowed, so a $300 loan for 14 days costs $42 in fees for a total repayment of $342. This transparency means you know the exact cost before committing, with no hidden fees buried in the fine print. The high costs are real though: a 14-day loan carries an APR of 365%, while a 62-day loan drops to approximately 82.4% APR, making these products expensive ways to access quick cash despite their speed advantage.

Now that you understand how same day loans work and what they actually cost, the next step is weighing whether this option makes sense for your situation or if alternatives might better serve your financial health.

The Real Trade-Off: Speed Against Cost

Why People Turn to Same Day Loans

Same day loans solve one problem brilliantly while creating another. When your car breaks down and you need $500 for repairs to get to work, a same day loan delivers funds in minutes while a bank loan takes days you don’t have. The speed genuinely matters in emergencies. A 2022 Ontario insolvency study by Hoyes, Michalos & Associates found that more than half of insolvencies involved payday loans, suggesting people turn to these products when traditional options fail them.

The Approval Speed Comes With a Cost

What makes same day loans attractive is also what makes them dangerous. Lenders approve applications because they don’t check your credit score or verify employment beyond basic deposits. They bet on your ability to repay within weeks, not months, which works fine if the emergency truly is temporary. But here’s the brutal reality-fewer than half of payday loan borrowers were able to repay their loan with their next paycheque, and many take out multiple loans in succession.

This pattern emerges because payday loans carry extremely high interest rates, meaning you pay roughly $14 in interest for every $100 borrowed. A $500 emergency becomes $570 in total repayment within two weeks.

When that next unexpected bill arrives, you’re already stretched thin and the cycle repeats. The trade-off between convenience and cost is real, and you need to calculate the total interest you’ll pay over the full term, not just focus on the advertised rate.

The Credit Score Impact You Should Know About

The credit score impact matters less than you’d think initially because most same day lenders don’t report to credit bureaus. They don’t help your score, but they don’t hurt it either if you repay on time. The real danger is the debt trap that forms when you can’t repay. Missing a payment triggers direct debit withdrawals, NSF fees from your bank, and collections action that does destroy your credit score. One missed payment can spiral into thousands in accumulated fees and legal costs.

When Same Day Loans Actually Make Sense

The better move is recognizing same day loans as a true emergency tool only, not a regular source of cash. If you’re considering one, ask yourself whether you can repay the full amount plus fees within the loan term without borrowing again. If the answer is no, explore alternatives like credit unions or debt consolidation services that can dramatically reduce monthly payments and help you escape the cycle entirely.

Alternatives Worth Exploring First

Same day loans work when the emergency is genuine and temporary, but they fail when they become a recurring solution to ongoing financial shortfalls. Before you apply for a same day loan, understanding what other options exist in Canada can help you make a decision that protects your long-term financial health rather than creating new problems.

Where to Find Same Day Loans in Canada

Online Lenders Offer Speed and Transparency

Online lenders combine accessibility with clear pricing. Money Mart operates 360+ branches across the country while also offering fully online applications through their website and mobile app, allowing you to apply at 2 AM from your couch or during lunch break at work. Money Mart funds loans up to $1,500 through Interac e-Transfer within minutes of approval, with their system handling most paperwork automatically. If you prefer in-branch funding, Money Mart deposits money via Interac e-Transfer within two hours for applications approved Monday through Friday during business hours. The online application process takes roughly 10 to 15 minutes, and you’ll know your approval status before you finish your coffee.

Other online providers like iCash and Cash Money operate similarly across Canada, though availability varies by province. Alberta, British Columbia, Nova Scotia, Ontario, Saskatchewan, and Manitoba have the most competitive online lending markets, while Newfoundland and Labrador, New Brunswick, and Quebec have fewer options available. The key advantage of online lenders is transparency on total costs. Money Mart clearly discloses all fees upfront, so you know exactly what you’ll repay before clicking approve.

Comparing Costs Across Provinces Matters

For a $500 loan in Ontario for 14 days, you’ll pay $70 in fees for total repayment of $570, representing a 365% APR. In Alberta, the same $300 loan for 42 days costs less overall because the term is longer, dropping the APR to 121.67%. This is why comparing loan terms matters more than chasing the lowest rate. Provincial regulations set fees at $14 per $100 borrowed, but the APR changes dramatically based on how long you borrow the money.

Banks and Credit Unions Require Planning Ahead

Traditional banks and credit unions represent your escape route from same day loans, though they require planning ahead. Banks like TD, RBC, and CIBC offer newcomer-focused financing products and secured credit cards that help you build credit history while accessing affordable borrowing at rates far below payday lenders. Credit unions across Canada typically offer personal loans starting at $500 with APRs in the single digits, but approval takes 3 to 5 business days, making them useless for true emergencies.

Debt Consolidation and Credit Counselling Services

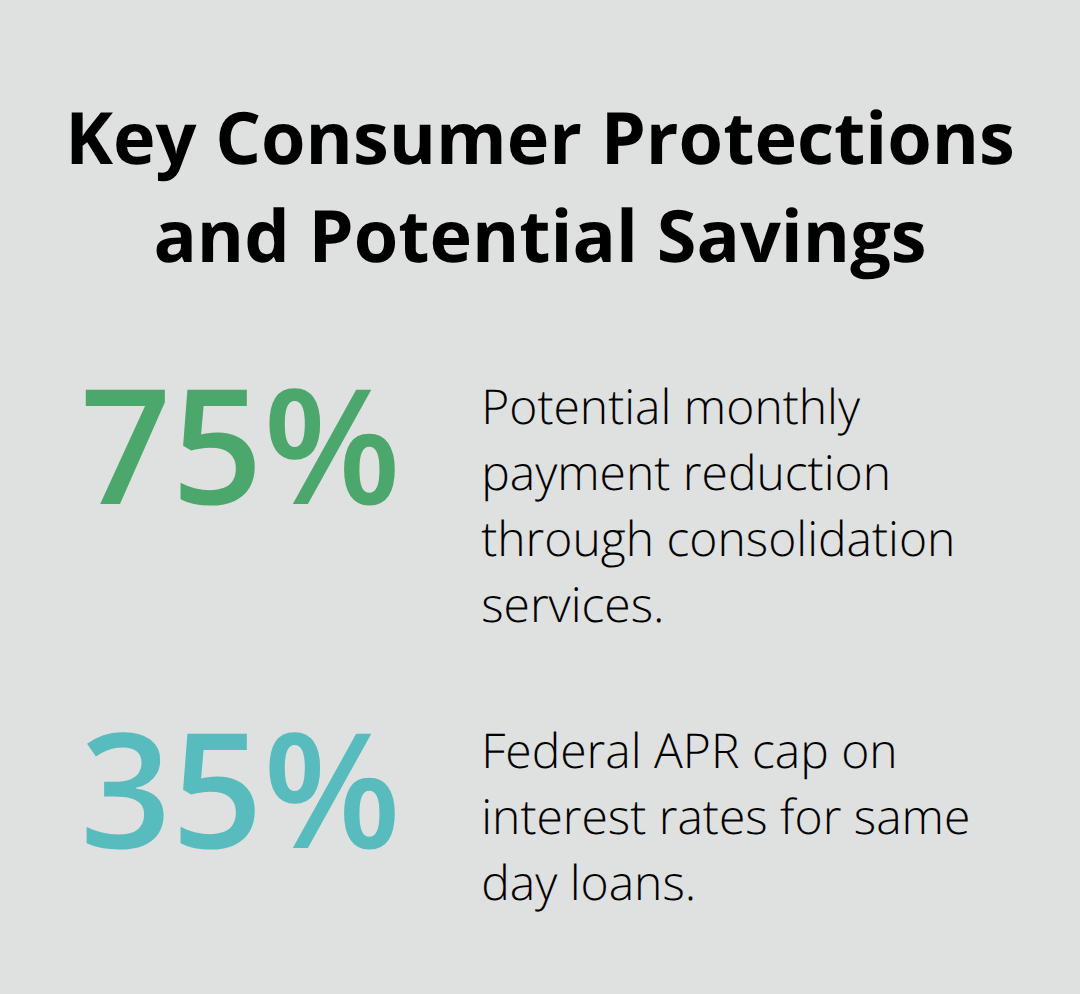

The real alternative is debt consolidation through services that restructure existing payday loan debt into manageable monthly payments. One example from debt consolidation services shows monthly payments dropping from approximately $575 down to $145 through consolidation, helping borrowers escape the cycle entirely. Credit Counselling Canada provides free debt repayment assistance and negotiates with lenders on your behalf, costing nothing while protecting your credit score.

Specialized Lenders for Poor Credit Situations

Windmill Microlending serves borrowers with poor credit or limited history, offering amounts up to $3,000 with approval in 24 to 48 hours. The Government of Canada caps same day loan APR at 35% federally and sets lending fees at $14 per $100 borrowed to protect consumers, but provincial regulations vary slightly. If you’re a newcomer lacking Canadian credit history, the Centre for Newcomers in Calgary offers free financial coaching to help you understand alternatives before turning to expensive lenders.

Final Thoughts

Same day loan Canada options exist because traditional banking fails people in genuine emergencies, and the speed is real when you need funds within hours. You can repay the full amount plus fees within the loan term without needing another loan, making the cost justified for true one-time emergencies. A $300 car repair that you’ll cover with your next paycheck represents a legitimate use case, while borrowing $500 repeatedly because your income doesn’t cover expenses creates a trap that destroys your financial stability.

Credit unions offer personal loans at single-digit APRs if you can wait three to five business days, and debt consolidation services restructure existing payday loan debt into manageable payments that sometimes cut monthly costs by 75 percent. Secured credit cards and credit-builder loans from major banks provide pathways forward for borrowers building credit history or facing barriers to traditional lending, without the predatory costs of same day lending. The Government of Canada caps APR at 35 percent federally to protect consumers, but even capped rates cost far more than alternatives available to you.

Your financial health depends on making intentional choices about debt, and we at Financial Canadian help you understand your options so you can build a strong strategy for your financial future. Visit Financial Canadian to explore resources that support your long-term financial planning and decision-making.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment