Your credit score shapes nearly every major financial decision you’ll make. From mortgage rates to credit card approvals, this three-digit number determines how much you’ll pay and what opportunities you’ll access.

At Financial Canadian, we’ve seen how understanding credit scores in Canada transforms people’s financial outcomes. This guide walks you through exactly how your score works and what you can do to strengthen it.

How Canadian Credit Scores Get Calculated

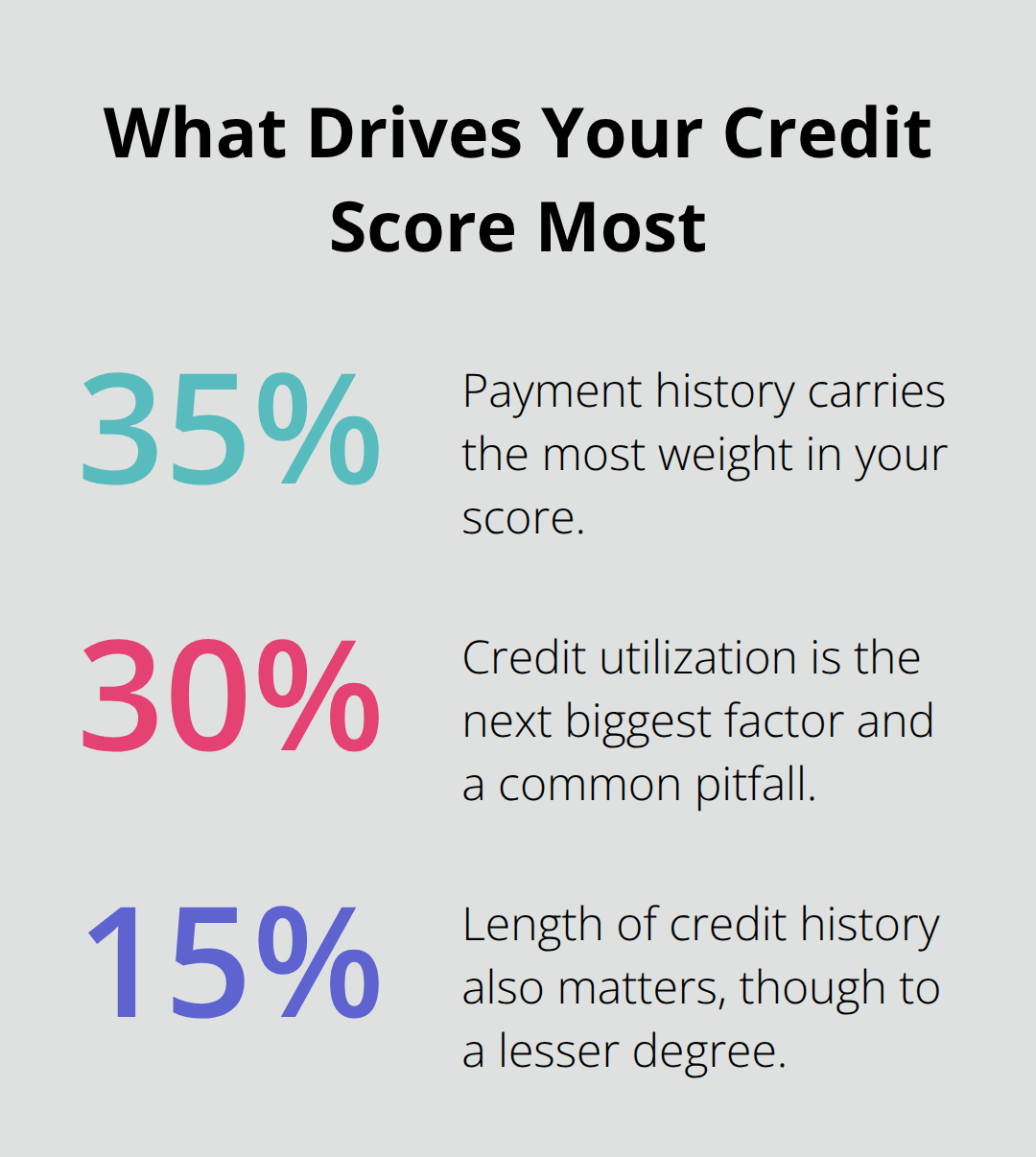

Canadian credit scores range from 300 to 900, and Equifax Canada and TransUnion Canada are the two bureaus that determine yours. These scores don’t appear out of thin air-they’re built on five specific factors that lenders care about. Payment history carries the most weight at roughly 35% of your score, which means a single missed payment from 2021 still drags down your current rating, though its damage weakens over time. Credit utilization makes up about 30% of your score, and this is where most people slip up. If you carry a 6,000 dollar balance across 10,000 dollars in available credit, you sit at 60% utilization-well above the ideal 30% threshold that lenders prefer. That single lever alone can be your fastest path to improvement.

Length of credit history accounts for about 15%, new credit inquiries another 10%, and credit mix the final 10%. Here’s what matters most: closing old accounts actually hurts you because it shrinks your average account age and reduces your total available credit, which tanks your utilization ratio. Keeping older accounts open costs nothing and helps your score climb.

Your Payment History Is Non-Negotiable

Payment history isn’t just about avoiding late payments-it’s about consistency. Lenders scrutinize whether you paid on time across credit cards, personal loans, and other accounts over the past two years. One clean stretch of on-time payments after a late mark shows you’ve changed your behavior, and that story matters to mortgage lenders. Set up automatic payments or phone reminders right now; there’s no excuse for missing a due date in 2026. If you have two credit cards and a small personal loan, managing payments across all three is manageable, and doing it flawlessly demonstrates reliability to any lender reviewing your file.

Credit Utilization Is Your Fastest Win

Reducing your reported credit utilization from 60% to below 30% can lift your score within weeks to months, not years. Request a credit limit increase on your existing cards-yes, this may trigger a hard inquiry that temporarily dips your score, but the utilization drop that follows outweighs that small hit. Alternatively, pay down balances aggressively before your billing cycle closes. The score improvement you’ll see translates directly into lower mortgage rates and real money saved over decades. A move from a 650 score to 720 can mean the difference between qualifying for a lender’s best mortgage tier or getting stuck with a higher rate. Understanding how these two factors work sets the stage for what comes next: seeing exactly how your score translates into real financial outcomes when you apply for mortgages, credit cards, and loans.

How Your Credit Score Opens or Closes Financial Doors

A 650 credit score and a 720 credit score look similar on paper, but lenders treat them like different applicants entirely. The gap between these two numbers can cost you tens of thousands of dollars over your lifetime, which is why understanding how lenders actually use your score matters far more than knowing the mechanics behind it.

Mortgage Lenders Use Your Score as a Filtering Tool

When you apply for a mortgage, lenders don’t just glance at your score and approve or deny you. They use it as a filtering tool. A score below 660 puts you in the subprime category, meaning you’ll face higher interest rates, larger down payment requirements, or outright rejection from many traditional lenders. At 720 and above, you access the best mortgage tiers available. The difference between a 5.5% mortgage rate and a 4.5% mortgage rate on a 500,000 dollar home adds up to roughly 150,000 dollars in extra interest over 25 years. That’s not theoretical math-that’s real money leaving your pocket.

Mortgage lenders also care about your payment history over the past two years. A late payment from 2021 still appears on your report, but if you’ve maintained perfect payments since then, lenders see you as someone who corrected course.

Credit Card Companies Set Limits Based on Your Score

Credit card companies operate differently. They approve or deny applications based on your score, but they also use it to set your credit limit. A 700 score might get you approved with a 5,000 dollar limit, while a 750 score could yield 10,000 dollars. This matters because it directly affects your utilization ratio-the same factor that dragged your score down in the first place.

Auto Insurance Premiums Connect to Your Credit

Auto insurers also pull your credit information, and some provinces allow them to factor it into your premium. Higher scores can lower your insurance costs depending on the insurer. This connection between credit and insurance isn’t universally advertised, but it’s a real financial consequence most people never see coming.

Your Action Plan for the Next 12 Months

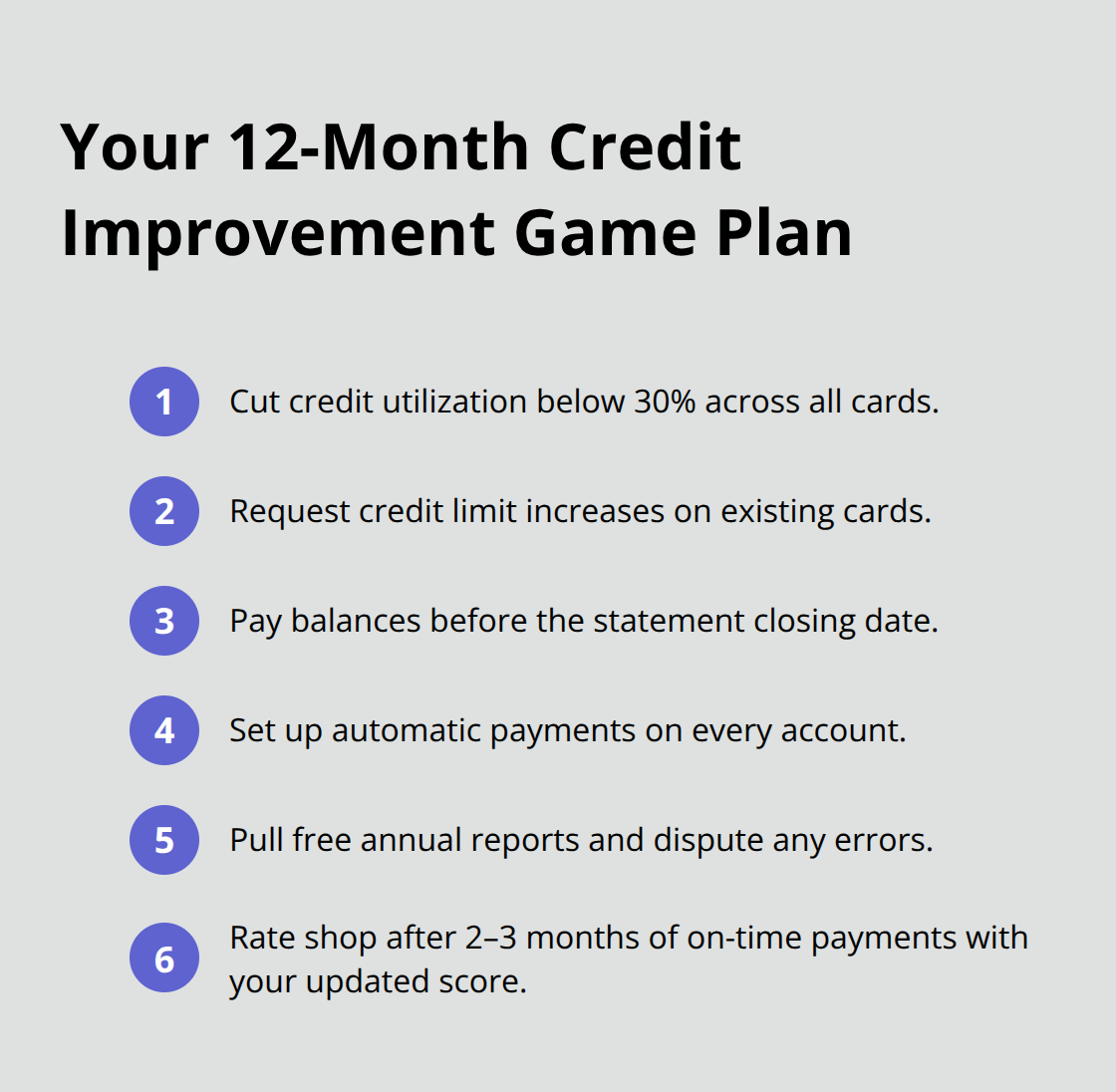

Improving your score from 650 to 720 within the next year should be your financial priority if you plan to borrow money. Start by reducing your credit utilization below 30 percent across all cards within the next one to two billing cycles. Request a credit limit increase on your existing cards, or pay down balances aggressively before statements close.

Second, set up automatic payments on all accounts so you never miss a due date. Third, check your credit reports from Equifax Canada and TransUnion Canada for errors-you’re entitled to free annual reports from both bureaus. If you spot inaccuracies, dispute them immediately; errors can artificially lower your score and cost you real money when you apply for credit.

For a mortgage application within the next 12 months, plan your rate shopping strategically. Once you’ve reduced utilization and maintained on-time payments for two to three months, request your updated score. The improvement compounds faster than most people expect. A move from 60 percent to 20 percent utilization can lift your score 30-50 points within weeks. That 50-point jump translates directly into better mortgage terms, lower insurance premiums, and higher credit limits-tangible financial wins that start the moment you take action. With your score trajectory now clear, the next step involves understanding exactly which mistakes actively damage your credit and how to avoid them.

How to Fix Your Credit Score Fast

Set Up Automatic Payments Across All Accounts

Improving your credit score requires action, not patience. Start with automatic payments across every account you hold. A single missed payment costs you far more than the convenience of automation is worth. Set up autopay through your bank for at least the minimum payment on each credit card and loan, then add a calendar reminder to pay extra toward balances before your statement closes. This dual approach keeps your payment history spotless while actively reducing utilization.

Equifax Canada and TransUnion Canada both track payment consistency, and lenders scrutinize this history heavily. One late payment from 2021 still appears on your report, but twelve consecutive months of perfect payments demonstrate you’ve changed your behavior. That narrative matters when a mortgage lender reviews your file. The financial payoff is substantial: a single missed payment can drop your score 100 points, while consistent on-time payments lift it steadily. You cannot afford to skip this step.

Target Your Credit Utilization Directly

Your second move targets utilization directly, and this is where rapid improvement happens. You currently carry 60 percent utilization across your available credit, and dropping this to 30 percent or below can add points to your score within weeks. Call your credit card issuers and request a credit limit increase on your existing cards. Yes, this triggers a hard inquiry that temporarily dips your score by a few points, but the utilization reduction that follows outweighs that small hit entirely.

If they deny the increase, pay down your balances aggressively before each billing cycle closes. Timing matters here: the balance your issuer reports to the bureaus is typically the one on your statement, so paying down balances after the statement closes but before the due date doesn’t help your reported utilization. Pay before the statement closes instead. This single lever can move your score within weeks.

Review Your Credit Reports for Errors

Your third move involves reviewing your credit reports from both Equifax Canada and TransUnion Canada for errors. You’re entitled to free annual reports from both bureaus, and you should pull them now. Look for accounts you don’t recognize, incorrect payment history, or balances that don’t match your records. Errors happen regularly, and disputing inaccuracies with the bureaus can lift your score instantly if they remove false marks.

Contact the bureau in writing with documentation of the error, and they must investigate within 30 days. These three actions together can move your score from 650 to 720 within one year if you execute them consistently. A move from 60 percent to 20 percent utilization can lift your score within weeks, and that improvement translates directly into better mortgage terms, lower insurance premiums, and higher credit limits.

Final Thoughts

Your credit score isn’t a static number that defines you forever-it’s a financial tool you control through consistent action. Reducing your utilization from 60% to below 30%, maintaining flawless payment history, and correcting errors on your credit reports form the foundation of score improvement that translates into real savings. A move from 650 to 720 within twelve months isn’t ambitious; it’s achievable when you target the factors lenders actually care about.

That 70-point jump opens access to mortgage rates that save you tens of thousands of dollars, credit limits that reduce your utilization further, and insurance premiums that reflect lower risk. Understanding credit scores Canada means recognizing that your score reflects behavior, not destiny. Late payments fade in impact over time, high utilization drops within weeks when you take action, and errors disappear when you dispute them.

Check your credit reports from Equifax Canada and TransUnion Canada right now, set up automatic payments this week, and request a credit limit increase or pay down balances before your next statement closes. These moves drive real results, and Financial Canadian helps you navigate every step of your financial journey with practical guidance tailored to your situation. Your financial future depends on the actions you take in the next thirty days, not the score you hold today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment