A financial emergency can hit without warning-job loss, medical bills, or urgent home repairs drain your savings fast. When you need cash immediately, emergency payday options in Canada range from quick loans to government assistance.

At Financial Canadian, we’ve mapped out the fastest ways to bridge cash gaps, from online lenders to alternatives that might save you money. This guide walks you through what qualifies as an emergency and which funding solution fits your situation.

What Counts as a Financial Emergency

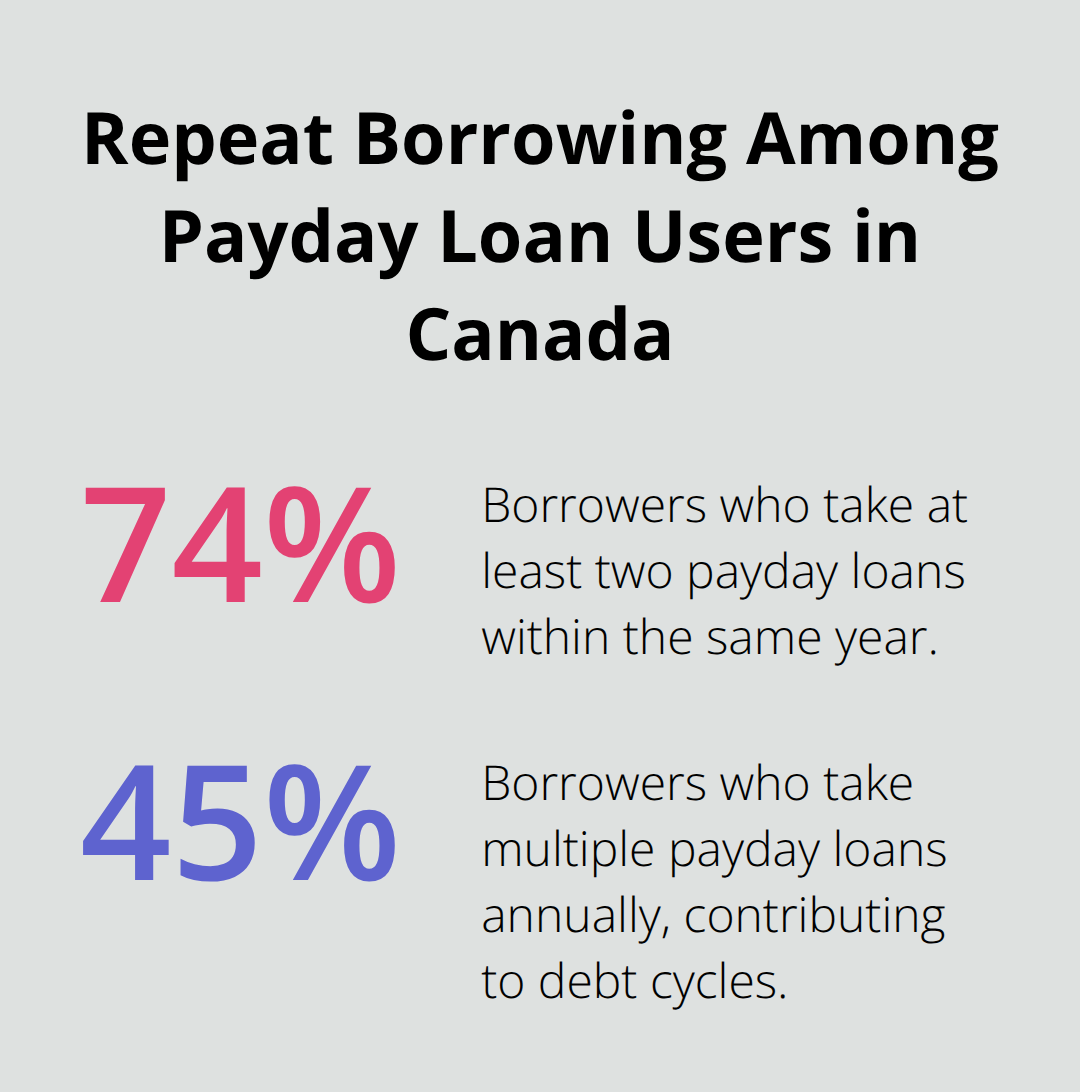

Job loss hits differently than a missed car payment. A genuine financial emergency drains your savings or income within days, forcing you to scramble for essentials like rent, utilities, or food. Statistics show nearly 2 million Canadians use payday loans each year, and roughly 74% of borrowers take out at least two loans within the same year-a sign that most initial emergencies aren’t isolated events. Job loss, medical bills, vehicle breakdowns, and urgent debt obligations create immediate cash shortfalls that can’t wait for standard loan approval.

Income Gaps Drive the Crisis

Unexpected income reduction-whether from reduced hours, contract work drying up, or seasonal employment gaps-forces households to cover fixed expenses with depleted paychecks. Medical expenses rank among the hardest to predict; a hospital visit, dental work, or prescription medication can cost hundreds or thousands without warning. Home and vehicle repairs often can’t be delayed; a furnace failure in winter or a brake system failure makes these emergencies non-negotiable.

The defining factor in a financial emergency isn’t the type of expense-it’s whether your current cash flow covers it. A household earning $1,590 monthly with essential expenses around $1,100 to $1,135 has virtually no buffer for unexpected costs. When a $400 vehicle repair or $300 medical bill arrives, that household must choose between covering it or skipping a utility payment. This gap is precisely why payday loans attract borrowers; the speed matters more than the cost when you face eviction or disconnection.

Job loss creates the most severe gap because income stops entirely while expenses continue. A two-week gap between paychecks during a job transition, reduced hours at work, or a delayed first paycheck from a new employer forces people to borrow immediately. Medical emergencies compound the problem because they often coincide with reduced income-time off work for recovery means less pay while bills still arrive.

Debt Payments That Escalate Costs

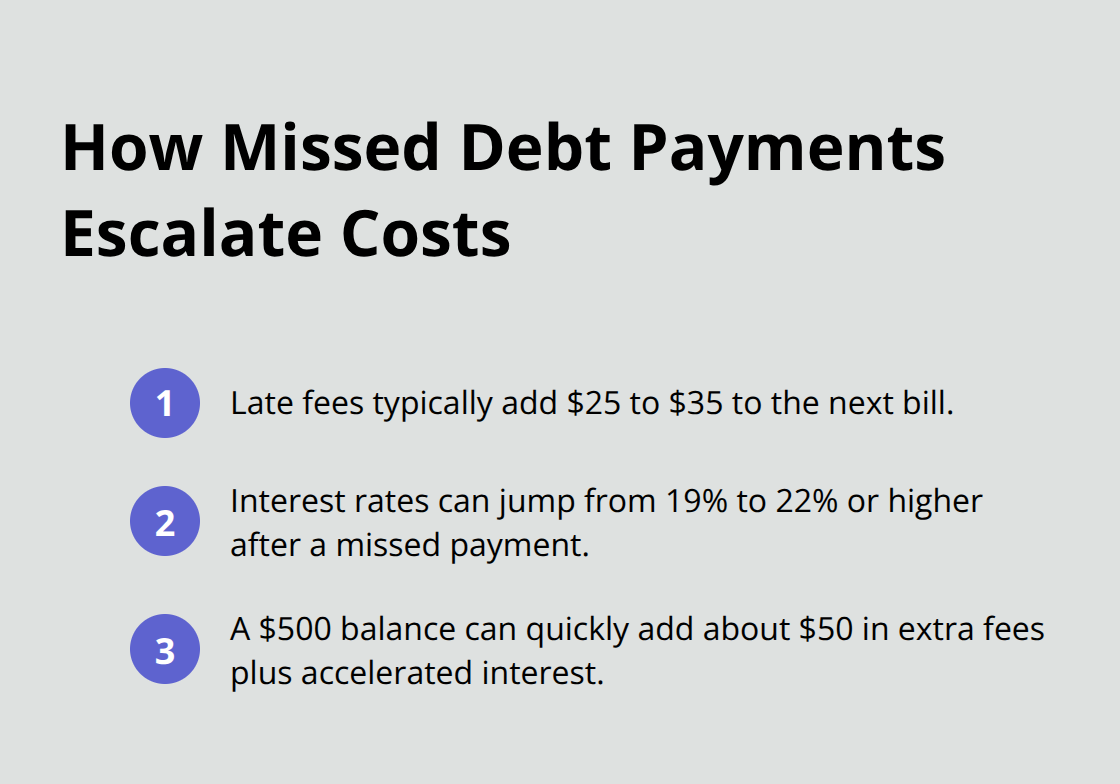

Existing debt payments become emergencies when income shrinks because missing them escalates costs rapidly. Credit card minimums, loan instalments, and mortgage payments don’t pause for job loss or medical recovery. Missing a credit card payment triggers a late fee of $25 to $35, plus interest rates that can jump from 19% to 22% or higher. A $500 credit card debt with a missed payment suddenly costs an extra $50 in fees plus accelerated interest charges.

This dynamic traps borrowers; they borrow via payday loan to make the debt payment, then struggle to repay the payday loan on the next paycheck. Over half of Ontario bankruptcies involve payday loans and high-interest debt. Understanding what qualifies as an emergency helps you identify which funding solution actually fits your situation-and which options might trap you in a worse financial position than the emergency itself.

Where to Find Quick Cash When You Need It Most

Online Payday Lenders: Speed Over Cost

Online payday lenders dominate the Canadian emergency borrowing market because they move fast and ask few questions. Most lenders fund e-transfers within hours of approval, sometimes within the same day. A typical online application takes 15 minutes, requires proof of income and bank authorization, and delivers a decision within 24 hours. The cost is steep: around $15 to $20 per $100 borrowed means a $500 emergency loan costs $75 to $100 in fees alone. For someone facing eviction or a utility disconnection, that speed matters more than the cost.

However, the real danger emerges when the loan comes due. About 2 million Canadians take payday loans annually, and 74% of borrowers take at least two loans within the same year. This pattern reveals a harsh truth: the first payday loan rarely solves the underlying problem, so borrowers return repeatedly, stacking fees on top of fees until a $500 emergency becomes $1,000 or more in total debt.

Credit Unions and Employer Programs: Cheaper Alternatives

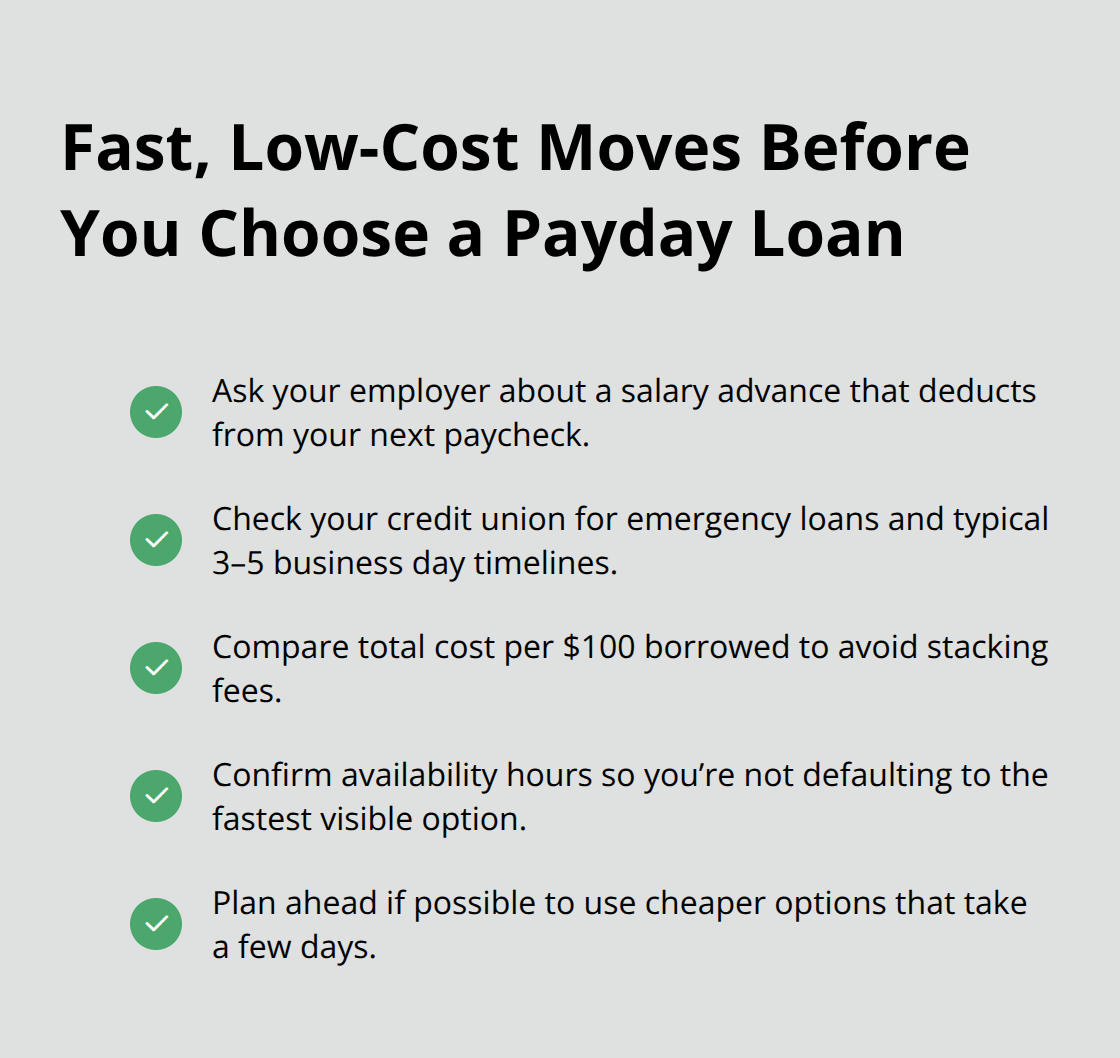

Credit unions and employer programs offer slower but substantially cheaper alternatives that most borrowers overlook. Credit unions typically charge 5% to 8% interest on emergency loans instead of the 35% APR that payday lenders impose, and approval takes three to five business days rather than hours. Employer salary advance programs are even better when available; many companies offer zero-interest advances deducted directly from your next paycheck, eliminating both the lender markup and the risk of missed payments.

Lines of credit from traditional banks work similarly, though qualification requires existing creditworthiness that emergency borrowers often lack. The gap between these options matters enormously: a $500 emergency funded through a payday lender costs roughly $100 in fees, while the same amount through a credit union costs $20 to $40 in interest. Over two paychecks, that difference compounds significantly.

Why Speed Trumps Savings in Emergencies

The real issue is access. Payday lenders operate 24/7 with minimal documentation requirements, while banks and credit unions require applications, employment verification, and decisions that take days. For someone with a furnace failure in January and a paycheck arriving in five days, the speed of a payday lender feels like the only option. Yet asking your employer about a salary advance takes five minutes and costs nothing.

Checking whether your credit union offers emergency loans takes another ten minutes.

These steps rarely happen because the psychological pressure of an immediate emergency pushes people toward the fastest visible solution, not the cheapest one. The payday lender sits online, ready to fund within hours. Your credit union’s loan officer works business hours only. Your employer’s HR department may not advertise salary advances. This visibility gap (not actual availability) drives borrowers toward expensive payday loans when cheaper options exist but remain hidden until you search for them. Understanding which lenders operate in your province and what your employer actually offers transforms your emergency response from panic-driven to strategic.

What Actually Works Better Than Payday Loans

Government assistance programs exist in every province, but most people facing emergencies don’t know they exist or assume they won’t qualify. Ontario offers the Emergency Assistance Program through social services, which covers rent, utilities, food, and emergency repairs for people in crisis-no loan repayment required. Alberta’s Income Support program functions similarly, providing immediate cash grants rather than loans that trap you in debt cycles. British Columbia, Manitoba, and Saskatchewan operate comparable programs with different names and eligibility rules. The barrier isn’t availability; it’s visibility. These programs require applications that take days or weeks to process, which feels impossibly slow when your furnace fails today. Yet if you’re facing a payday loan spiral where approximately 45% of borrowers take multiple loans annually, waiting five business days for a grant that doesn’t require repayment beats paying $15 to $20 per $100 borrowed every two weeks. Contact your provincial social services office or search your province’s government website for emergency assistance-most programs accept applications online and by phone.

Credit Counselling Stops the Bleeding

Credit counselling services, often free through nonprofit organizations like Credit Counselling Canada, address the root problem that payday loans ignore: your budget doesn’t work. A counsellor reviews your actual income, fixed expenses, and debt obligations to identify where money actually goes. This matters enormously because people trapped in payday loan cycles often don’t realize they spend $300 monthly on fees alone. Debt management plans consolidate multiple payday loans into a single payment with lower interest rates-sometimes reducing monthly payments from $575 to $145 on the same debt, according to real borrower data. Your creditors may accept reduced payments if you work through a legitimate counselling agency, and this approach avoids bankruptcy while actually moving you toward payoff. Many employers offer free counselling through employee assistance programs; check your benefits package before paying for private services.

Banks and Credit Unions Offer Real Alternatives

Personal loans from traditional banks carry interest rates between 6% and 12%, vastly cheaper than payday loans but requiring existing creditworthiness that emergency borrowers often lack. Credit unions take a different approach: they’re more willing to approve borrowers with imperfect credit if you have a savings account or stable income. A $500 emergency loan from a credit union at 7% costs roughly $18 in interest over three months, compared to $75 to $100 from a payday lender. The approval timeline matters less if you plan ahead-most credit union emergency loans take three to five business days, which works if you catch the emergency early. Family or friend loans work when you structure them with written terms: specify the amount, repayment schedule, and whether interest applies. This clarity prevents resentment and legal disputes that damage relationships far more than the money itself. Many people avoid asking family for help because they feel shame about the emergency, yet borrowing from someone who cares about you costs zero interest and carries zero risk of wage garnishment or collections.

Final Thoughts

When a financial emergency hits, your first instinct pushes you toward the fastest solution available. Online payday lenders promise funding within hours, which feels like your only option when rent arrives or a repair cannot wait. Yet this guide reveals a critical reality: speed and cost rarely align in emergency borrowing, and a $500 payday loan costs $75 to $100 in fees while the same amount through a credit union costs $20 to $40. That difference multiplies when you borrow repeatedly, which 74% of payday borrowers do within a single year.

Your actual best choice depends on your timeline and circumstances. If you have five business days before the crisis hits, contact your credit union or employer about salary advances-both offer dramatically cheaper rates than payday lenders. If the emergency strikes today, check whether your province offers emergency assistance grants through social services; these programs provide cash without requiring repayment, though processing takes longer. For ongoing financial strain, credit counselling addresses the root problem by restructuring your budget and consolidating debt into manageable payments.

Emergency payday Canada options exist across a spectrum from expensive to free, but visibility determines which one you actually use. Payday lenders advertise aggressively and operate around the clock, while government programs, credit union emergency loans, and employer salary advances sit quietly in the background. We at Financial Canadian help borrowers navigate these options through clear financial guidance, so you can find real alternatives instead of defaulting to expensive payday loans when panic strikes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment