Buying your first home is one of the biggest financial decisions you’ll make. First-time mortgages in Canada come with their own rules, rates, and requirements that differ from other countries.

We at Financial Canadian have created this guide to walk you through each step, from understanding mortgage types to closing on your new home. You’ll learn what lenders actually look for and how to avoid costly mistakes.

How Mortgages Work in Canada

A mortgage is a loan secured by your home, meaning the lender holds the right to take the property if you stop paying. In Canada, mortgages typically run for 25 to 30 years, though you choose the amortization period when you apply. The Bank of Canada’s overnight rate directly influences what you’ll pay-when it rises, variable-rate mortgages increase monthly, while fixed-rate mortgages lock in your payment for the entire term, usually between one and ten years.

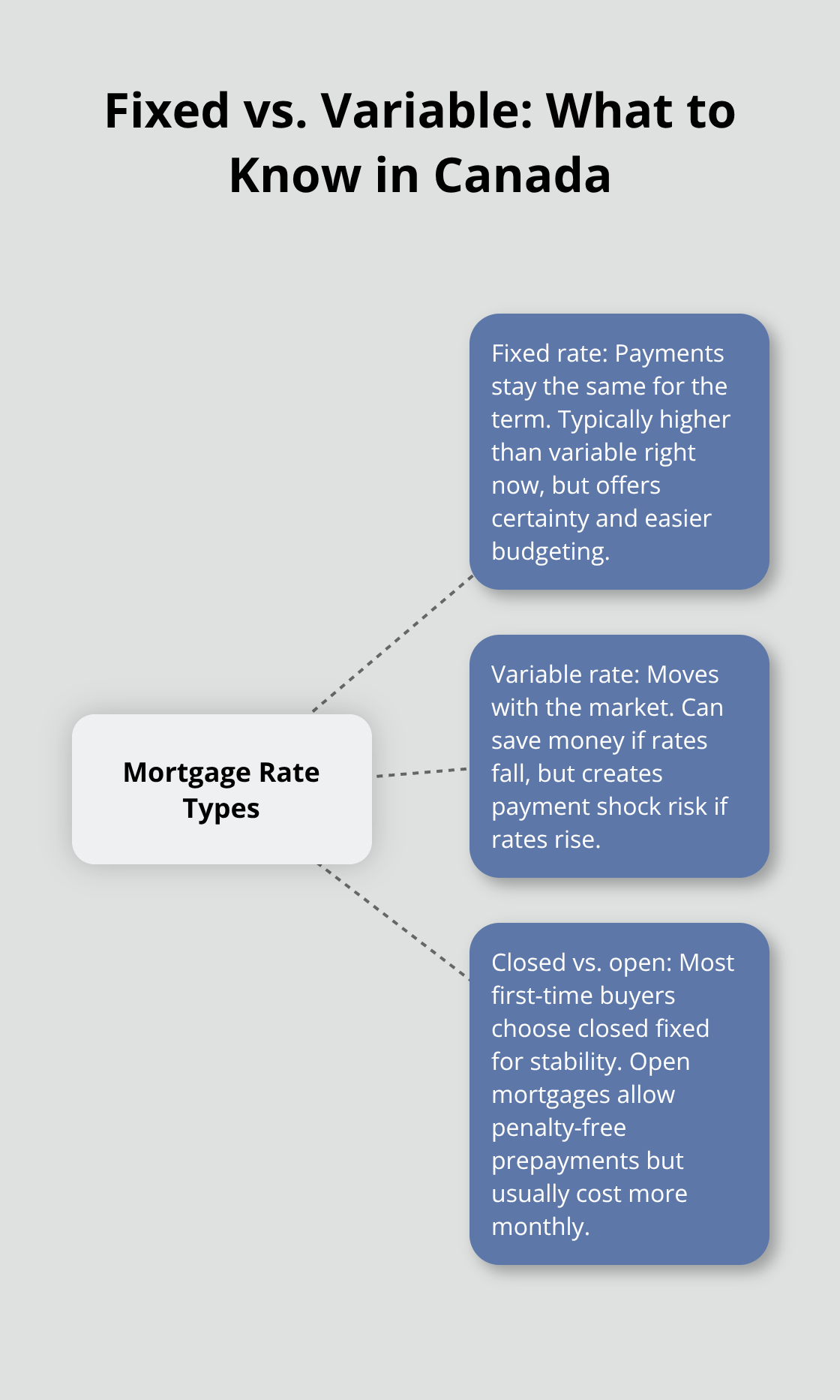

Fixed vs. Variable Rates

Fixed rates currently sit higher than variable rates, but they offer payment certainty. Variable rates fluctuate with the market and can save you thousands if rates fall, but they expose you to payment shock if rates climb. Most Canadian first-time buyers choose closed fixed-rate mortgages because they provide stability and lower rates than open mortgages, which allow penalty-free prepayment but cost more monthly.

The 20% Down Payment Threshold

Canada divides mortgages at the 20% down payment threshold. Put down less than 20%, and you’ll need mortgage insurance from Canada Mortgage and Housing Corporation (CMHC) or a private insurer-this protects the lender, not you, but it lets you enter the market faster. CMHC enables homebuyers to purchase a home with a minimum down payment of 5% from flexible sources, and for a $400,000 home with 10% down, you’d pay roughly $40,000 upfront and carry insurance costs added to your mortgage balance, increasing your total borrowing.

Government-Backed vs. Conventional Mortgages

Government-backed mortgages through CMHC include the First-Time Home Buyer Incentive, which lets you borrow up to 10% of the purchase price from the government interest-free for up to 15 years, reducing your mortgage amount and monthly payments. Conventional mortgages require that 20% down payment but eliminate insurance costs entirely and offer slightly lower rates. The choice between government-backed and conventional mortgages depends on your savings-if you have 20% ready, conventional mortgages cost less over time, but if you’re short, CMHC insurance gets you into homeownership sooner without waiting years to save. Understanding which path fits your financial situation sets the stage for the next critical step: preparing your finances before you apply.

Preparing Your Credit and Finances

Check Your Credit Score and Report

Your credit score determines whether lenders approve your mortgage and what rate you’ll qualify for. A score of 620 or higher typically allows mortgage qualification in Canada, but lenders reserve their best rates for borrowers above 740. Pull your credit report from Equifax or TransUnion before applying-these reports often contain errors that tank your score unnecessarily, and correcting them takes weeks. If your score sits below 700, spend three to six months paying down existing debt and making all payments on time; each missed payment stays on your report for six years and signals risk to lenders.

Understand Your Debt-to-Income Ratio

Your debt-to-income ratio matters equally to your credit score. Lenders calculate this by dividing your total monthly debt payments by your gross monthly income, and most won’t exceed a ratio of 44% combined with other debts. If you carry credit card balances, car loans, or student debt, paying these down before applying strengthens your position significantly and can lower the rates you qualify for.

Save for Your Down Payment

Down payment size directly affects your borrowing costs and timeline. You need a minimum of 5% down to qualify for CMHC insurance, but saving 10% to 15% reduces insurance premiums substantially-a $400,000 home with 5% down costs roughly $20,000 upfront plus insurance premiums around $15,200, while 15% down ($60,000) cuts insurance to approximately $8,800. Most first-time buyers overlook closing costs, which typically run 1.5% to 4% of the purchase price and include legal fees, inspections, appraisals, and title insurance. On a $400,000 home, expect $6,000 to $16,000 in closing costs alone.

Get Pre-Approved Before House Hunting

Pre-approval from a lender or mortgage broker locks in your rate for 120 days and shows sellers you’re serious, but pre-qualification only estimates what you might borrow without rate protection. Get pre-approved before house hunting-it reveals exactly what price range suits your finances and prevents wasting time on unaffordable properties. Lenders assess your income, employment history, and assets during pre-approval, so gather recent pay stubs, tax returns from the last two years, and proof of down payment savings before meeting with them. Once you understand what you can afford, you’re ready to move forward with comparing mortgage options and selecting the right lender for your situation.

The Mortgage Application Process

Gather Your Documentation

Once you have pre-approval locked in, the real work starts. You’ll need specific documents that lenders require, and this is where most first-time buyers stumble. Lenders want recent pay stubs from the last 30 days, tax returns for the past two years, and proof that your down payment comes from legitimate sources-not borrowed money. If you’re self-employed, you’ll provide two years of financial statements and possibly a notice of assessment from the Canada Revenue Agency. You’ll also need proof of employment, bank statements showing your savings history, and documentation of any other debts you carry.

Many lenders now use automated systems to verify this information directly, but delays happen when documents are incomplete or outdated. Start gathering these items immediately after pre-approval; don’t wait until you’ve made an offer on a home. One mistake first-time buyers make is assuming their pre-approval means the lender won’t re-verify their finances. Lenders absolutely will pull your credit report again right before closing, and if you’ve taken on new debt or missed a payment, your approval can vanish.

Keep your finances static during this period-don’t finance a car, open new credit cards, or make large purchases. Your lender monitors your financial activity closely, and unexpected changes signal risk.

Choose Your Lender or Mortgage Broker

Choosing between a mortgage broker and a lender directly shapes your rates and terms significantly. Banks and credit unions are direct lenders, meaning they offer their own mortgages, but they typically show loyalty to existing customers and may not offer their most competitive rates to new applicants. Mortgage brokers access multiple lenders and can shop your application across 10 to 20 different options, often uncovering rates 0.25% to 0.5% lower than what a bank would quote you directly.

For a $320,000 mortgage at 5% over 25 years, a rate difference saves you money on your monthly payments and over the full amortization. Brokers charge nothing upfront-lenders pay them a commission-so there’s zero cost to using one. However, not all brokers are equal. Ask your broker which lenders they work with and whether they can access A lenders like RBC, TD, or Scotiabank, or if they’re limited to B lenders and private lenders who charge higher rates.

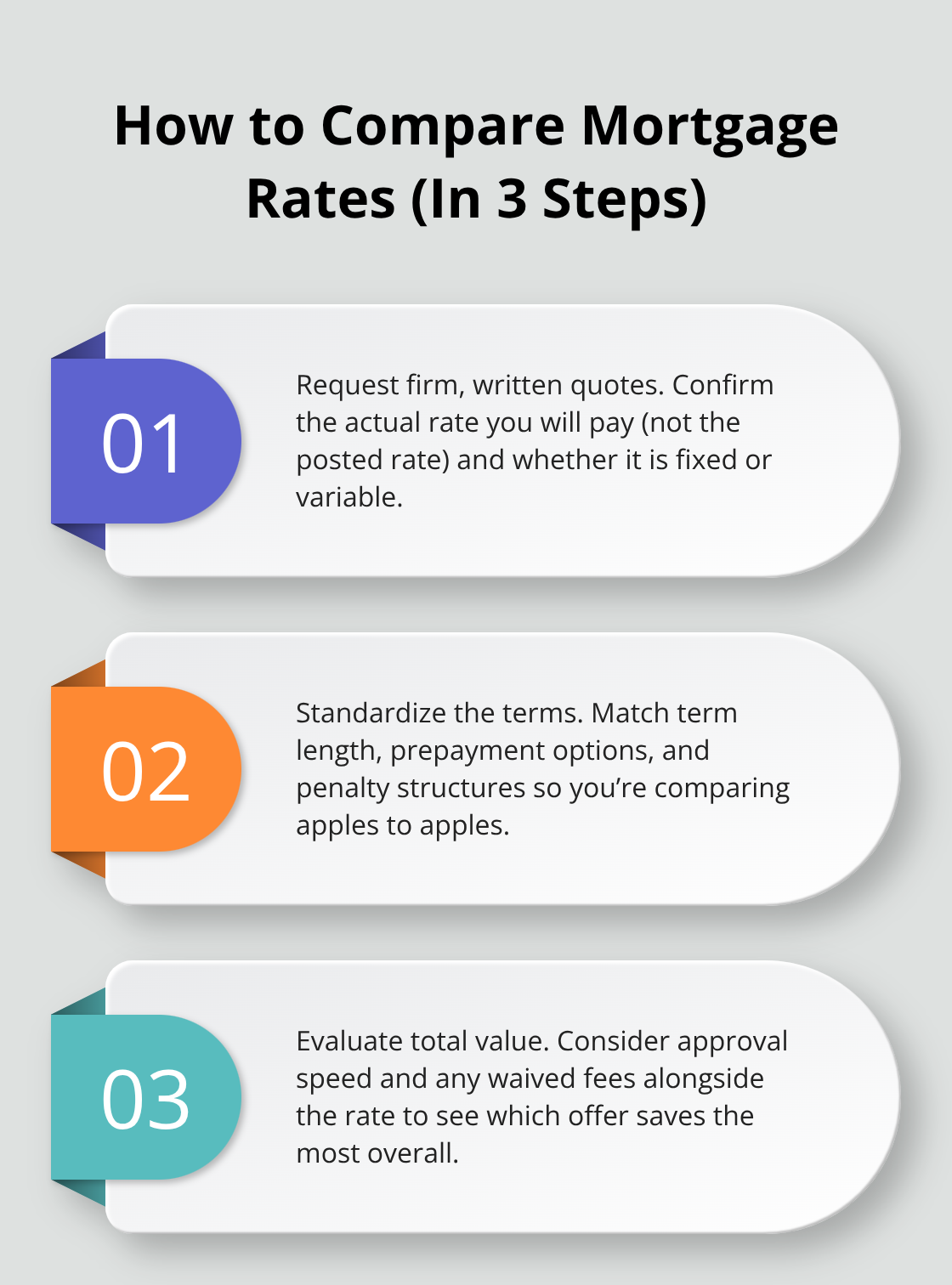

Compare Mortgage Rates and Terms

Comparing mortgage rates means understanding what you’re comparing: a posted rate of 5.5% might come with a discount that brings it to 4.99%, while another lender quotes a lower posted rate but offers no discount. Always compare the actual rate you’ll pay, not the posted rate. Request rate quotes in writing and confirm whether rates are fixed or variable, what the term length is, and whether prepayment penalties apply.

Most first-time buyers qualify for closed mortgages with standard terms of one to five years. You should compare at least three different options before committing (this takes roughly one to two hours and can save thousands). Each quote reveals different strengths-one lender might offer a lower rate, another might provide faster approval, and a third might waive certain fees.

Final Thoughts

First-time mortgages in Canada require you to master three core areas: understanding your financial position, preparing documentation early, and comparing options before you commit. Start by checking your credit score and debt-to-income ratio months before you apply, then save aggressively for your down payment while gathering tax returns and pay stubs. Pre-approval locks in your rate and establishes your budget, but lenders will re-verify everything at closing, so you must avoid taking on new debt or making large purchases during this window.

First-time mortgage applicants commonly fail by assuming pre-approval guarantees funding, by comparing only posted rates instead of actual rates, or by selecting the first lender they contact instead of shopping across multiple options. Many also underestimate closing costs and arrive at closing unprepared for the additional 1.5% to 4% of the purchase price required for legal fees, inspections, and title insurance. Financing a vehicle or opening new credit cards between pre-approval and closing can trigger a credit re-check that disqualifies you entirely.

Connect with a mortgage broker or lender and request written rate quotes from at least three sources to move forward with your first-time mortgages Canada application. Compare the actual rates you’ll pay, confirm the term length and whether prepayment penalties apply, and ask about any fees being charged. Visit our mortgage resources to explore additional guidance that strengthens your financial foundation as you move toward homeownership.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment