Canadians carry an average of $22,000 in consumer debt, and most people have no clear strategy to eliminate it. At Financial Canadian, we’ve created this guide to show you exactly how to tackle your balances with debt reduction Canada tips that actually work.

The right approach depends on your situation-whether you need a structured repayment plan, want to accelerate payoff, or should explore consolidation options. We’ll walk you through each strategy so you can pick what fits your life.

Build Your Debt Payoff Strategy

Map Out Every Debt You Owe

The first step to eliminating debt is knowing exactly what you owe and at what cost. Pull together a complete list of every debt-credit cards, personal loans, car payments, student loans, anything with a balance. Write down the balance, interest rate, and minimum payment for each one. This isn’t optional; you can’t build a real plan without this information.

Statistics Canada reports that Canadian households held about 3.07 trillion dollars in total credit-market debt in Q1 2025, with average non-mortgage consumer debt per household at 26,415 dollars in 2025, up from 25,786 dollars in 2024. Your personal situation likely mirrors this trend-multiple debts at different rates, all pulling money from your monthly budget.

Calculate Your True Interest Cost

Once you have this snapshot, calculate your total interest cost if you only make minimum payments. A debt calculator shows you how long payoff will take and how much extra you’ll pay in interest. This number often shocks people into action, which is exactly what you need.

Choose Your Repayment Method

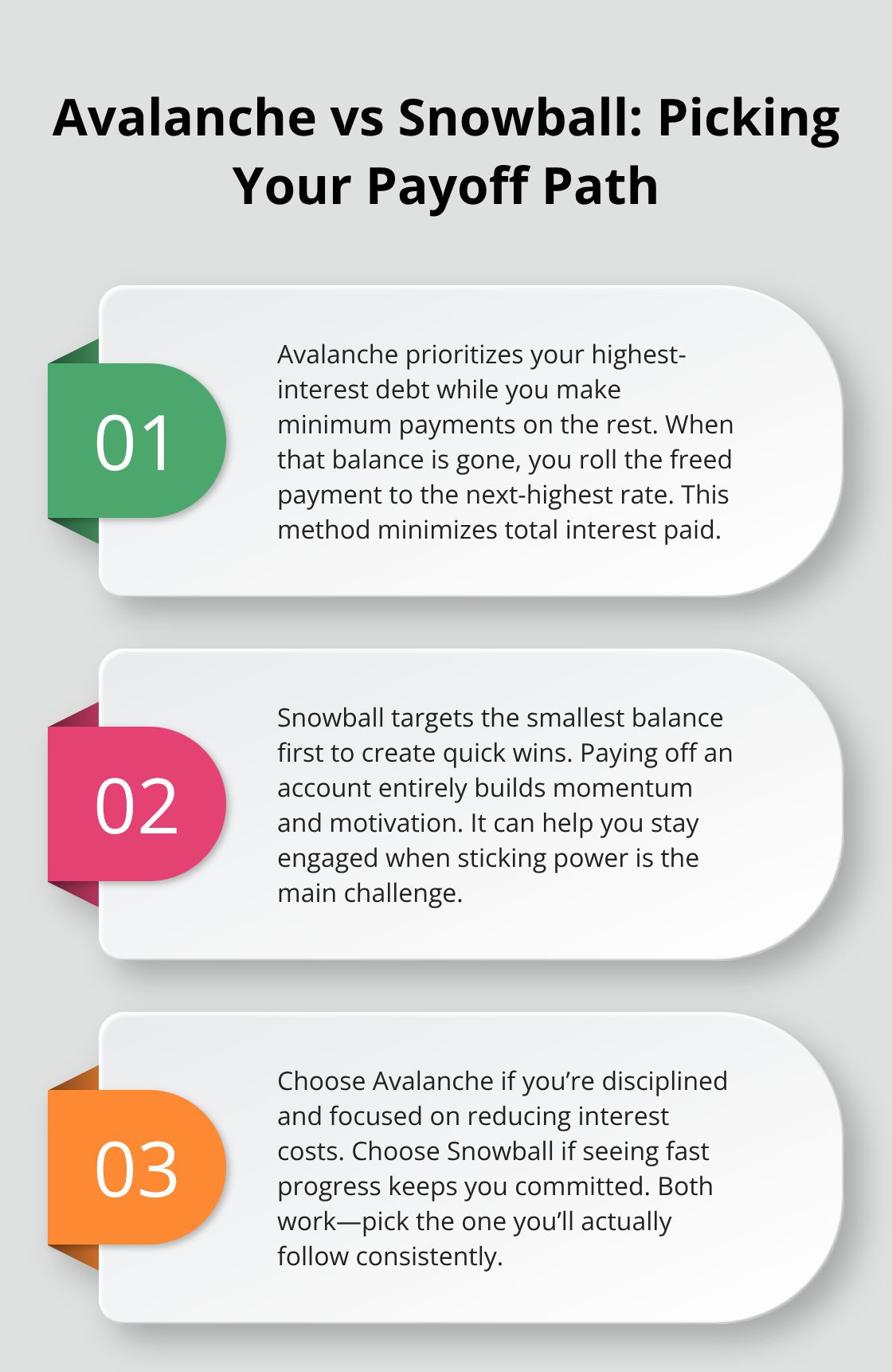

Now you select your method: the Avalanche or the Snowball. The Avalanche targets your highest-interest debt first while you make minimum payments on everything else. Once that debt disappears, you roll that payment amount to the next-highest-interest debt. This method saves the most money in total interest, which matters if you’re paying 21 percent on a credit card while carrying a 6 percent student loan.

The Snowball flips the strategy-you attack the smallest balance first regardless of interest rate. You get quick wins, pay off one debt entirely in a few months, and build momentum. Both methods work; the Avalanche is mathematically superior, but the Snowball keeps people motivated when they’re drowning. Choose Avalanche if you’re disciplined and focused on the math. Choose Snowball if you need visible progress to stay committed.

Set a Realistic Timeline

Then set your timeline and monthly target. If you owe 15,000 dollars total and can afford 500 dollars monthly toward debt, you’re looking at 30 months assuming no interest. Add interest into the calculation and you might hit 36 months or longer. Be honest about what you can actually pay each month, not what you wish you could pay. A realistic plan you stick to beats an aggressive plan you abandon after three months.

With your strategy locked in, the next move is to find extra money each month-whether that means cutting expenses, boosting your income, or both. If you’re struggling to find that extra cash or need guidance tailoring a plan to your situation, debt advice services can help simplify the process.

How to Find Extra Money for Debt Payoff

Finding an extra $100 to $500 monthly transforms your payoff timeline from years to months. Most people think they need to earn more or spend drastically less, but the reality is simpler: you need to redirect money that’s already flowing out of your account toward debt instead. The average Canadian household spends about $4,000 monthly on essentials and non-essentials combined. Within that spending, substantial room exists to redirect cash toward your payoff goal without feeling deprived.

Track Your Actual Spending

You must track every dollar you spend for one month. Not a budget estimate-actual spending. Use your bank and credit card statements, and categorize everything: groceries, subscriptions, dining out, utilities, insurance, transportation. You’ll find recurring charges you forgot about. Most Canadians discover $200 to $400 monthly in forgotten subscriptions, streaming services they don’t use, or inflated insurance premiums they never shopped around on.

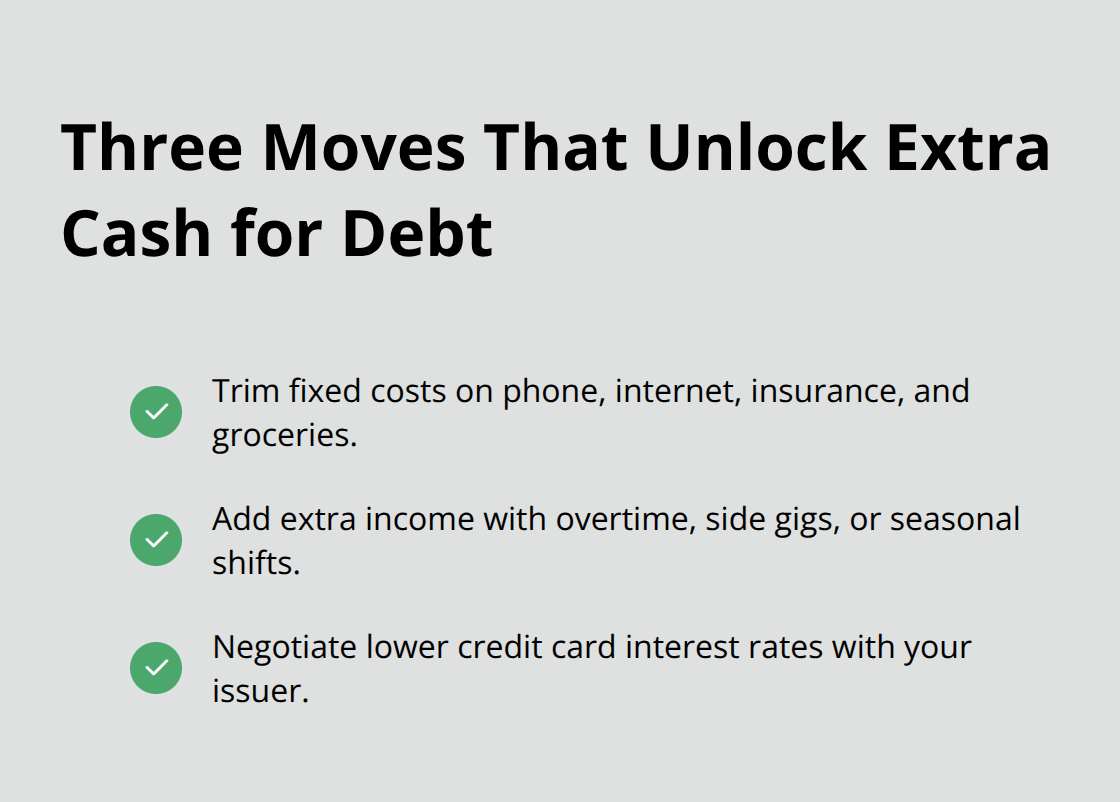

Cut Fixed Costs First

Reduce your phone bill by switching providers, cut your internet plan to a lower speed tier if you don’t need the fastest option, and call your insurance company to request quotes from competitors. These three moves alone typically save $50 to $150 monthly with zero lifestyle sacrifice. For groceries, families can cut spending by up to 25 percent annually by stockpiling during sales and skipping one shopping trip per month. That’s roughly $200 to $300 monthly for a family of four. Cut these areas first because they require no extra work-just smarter choices.

Increase Your Income

Once you’ve trimmed fixed costs and reduced discretionary spending, attack your income. A second job or extra shifts during peak seasons puts additional money directly toward debt without touching your primary income. Even temporary side work matters: four hours weekly at $20 per hour generates $320 monthly, which cuts your payoff timeline significantly. The Avalanche method means that extra $320 applied to your highest-interest debt saves thousands in interest charges over time. If a side hustle isn’t realistic, negotiate with your creditors directly.

Negotiate Lower Interest Rates

Call your credit card issuer and ask for a lower interest rate, especially if you’ve maintained on-time payments. Many creditors reduce rates by 2 to 5 percent simply because you asked, which compounds into substantial savings. A $10,000 balance at 19 percent costs $1,900 annually in interest; drop that to 14 percent and you save $500 yearly. Apply that savings to principal instead, and your payoff accelerates.

These three moves-trimming fixed costs, finding extra income, and negotiating rates-are concrete and measurable. Together, they typically generate $300 to $600 monthly in additional payoff capacity, which is the difference between drowning in debt for five years and being free in two. With this extra money identified, you can now evaluate whether consolidation or balance transfers make sense for your situation.

Consolidation, Balance Transfers, and Last-Resort Options

Consolidation loans and balance transfer cards both promise relief, but they work in fundamentally different ways and suit different financial situations. A consolidation loan wraps multiple debts into a single monthly payment at a lower interest rate, which simplifies your finances and reduces overall interest cost if you qualify. The catch is eligibility: lenders typically require a credit score above 650 and stable income. If your credit is damaged from missed payments, consolidation loans become unavailable or come with rates so high they barely improve your situation. Balance transfer cards offer 0 percent APR for 12 to 18 months, which buys time to attack principal without interest accruing, but only if you can pay down the balance before the promo period ends. Transfer the balance to a card with a 0 percent offer, then apply your $300 to $600 monthly debt payoff capacity directly to principal. The risk is obvious: if you don’t finish paying during the promotional window, the regular APR kicks in at 19 to 22 percent, and you’re worse off than before.

When Consolidation Actually Makes Sense

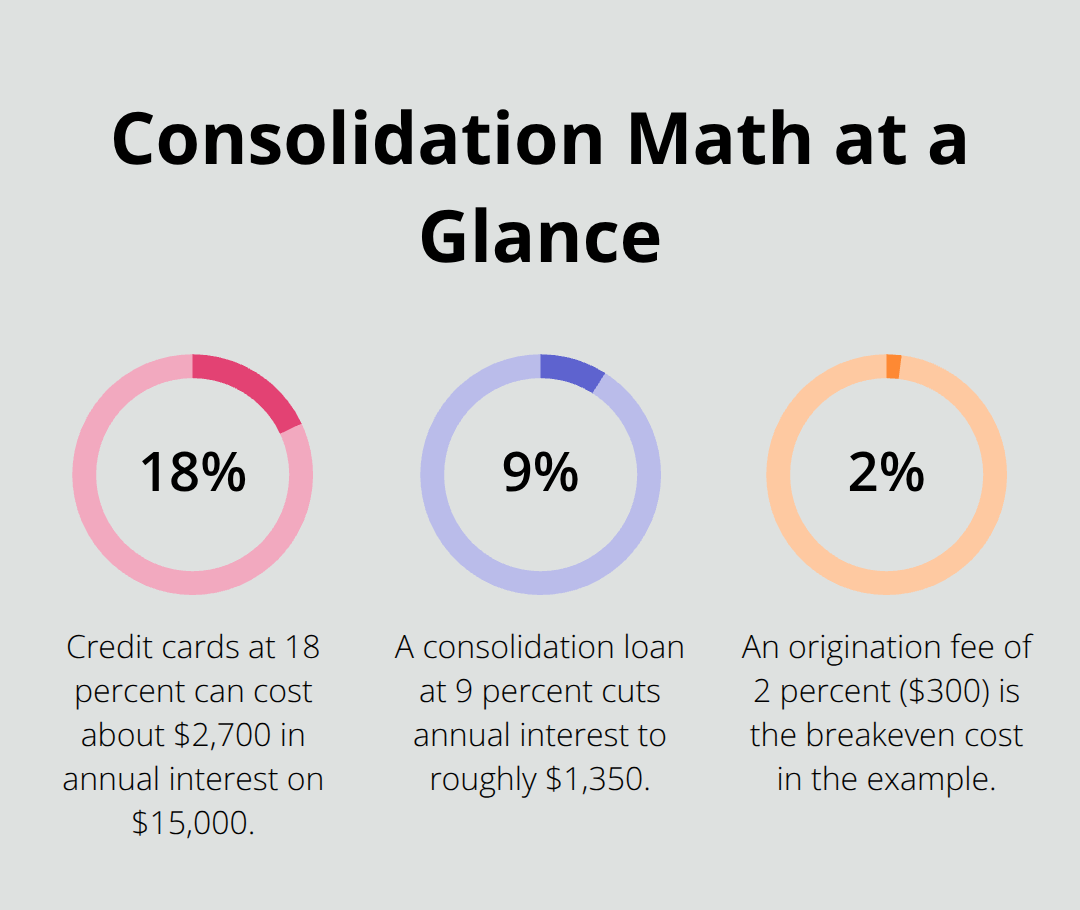

Consolidation loans make genuine sense only when your interest savings exceed the costs of the loan itself. A $15,000 debt spread across three credit cards at 18 percent costs roughly $2,700 annually in interest. A consolidation loan at 9 percent costs $1,350 yearly, saving $1,350. If the loan charges a 2 percent origination fee ($300), you break even in about three months and save real money after that.

Run the numbers before applying: use a debt calculator to compare total interest paid under your current situation versus the consolidation scenario. If savings don’t exceed loan fees and closing costs, skip consolidation and attack your debts using the Avalanche method instead.

Non-Profit Consolidation Programs

Debt Consolidation Programs offered by non-profit credit counselling agencies provide an alternative path. These programs negotiate directly with creditors to reduce interest rates and bundle unsecured debts into a single payment, typically targeting payoff within 48 months. You stop using credit cards during the program, but you avoid the credit damage of bankruptcy or consumer proposals. The trade-off is real: your credit takes a temporary hit, but recovery is faster than after bankruptcy, and you address debt without legal proceedings.

Consumer Proposals and Bankruptcy

Consumer proposals and bankruptcy represent last resorts when consolidation and accelerated payoff are impossible. A consumer proposal lets you pay a portion of what you owe or extend repayment over time, negotiated through a Licensed Insolvency Trustee. You might settle $20,000 of debt for $12,000 paid over five years. The credit impact lasts six years post-discharge and you lose negotiating power with creditors, but it beats bankruptcy. Bankruptcy itself should be your absolute final option: it wipes unsecured debt but destroys your credit score (R9 rating) for roughly six years, may require asset liquidation, and creates a public record. The emotional and financial consequences are severe and long-lasting.

Getting Professional Guidance

Before considering either option, speak with a certified credit counsellor from a reputable non-profit. Services offer free consultations and can explain whether a consumer proposal, consolidation program, or aggressive repayment plan fits your situation. If you’re unsure whether consolidation, a debt program, or bankruptcy applies to you, professional guidance clarifies the path forward without judgment or hidden costs.

Final Thoughts

Debt reduction Canada tips only work when you act on them. Track your total debt balance today, then record it monthly as payments reduce the amount owed. Watching that number shrink builds momentum and keeps you committed when motivation fades, and most people who succeed report that seeing tangible progress made the difference between staying the course and abandoning their plan after a few months.

Your plan will shift as life changes. A bonus arrives and you accelerate payments, or an unexpected expense forces you to pause for a month. Review your strategy every three months and adjust targets based on what actually happens in your life, not what you predicted six months ago. Flexibility keeps your plan realistic and sustainable, and consistency transforms debt reduction from a distant goal into a concrete reality.

Execute your plan by making minimum payments on time, applying extra funds to your target debt, and resisting new debt while you pay down existing balances. If you need professional guidance tailoring these debt reduction strategies to your specific situation, we at Financial Canadian can support your journey with personalized advice and resources. Start this week by calling your credit card issuer to negotiate a rate or tracking your spending for a month-small steps compound into real results.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment