Personal loans Canada rates vary significantly depending on who you borrow from and your financial situation. At Financial Canadian, we’ve seen borrowers pay anywhere from 6% to 21% annually, and the difference often comes down to factors within your control.

This guide walks you through current rates, what lenders actually look at when pricing your loan, and concrete steps to secure the best deal available to you.

Current Personal Loan Rates in Canada

Average Rates Across Major Lenders

Major Canadian banks advertise starting rates between 6% and 10% APR for borrowers with solid credit. Scotiabank, for example, sits at the lower end of this range. These advertised rates apply only to borrowers with excellent credit scores and stable income-not the average person applying for a loan.

Online lenders and non-bank alternatives operate in a completely different pricing universe. Easyfinancial charges between 9.90% and 46.96% APR, while MDG Financial ranges from 29.78% to 44.80% APR, also per Ratehub.ca. The gap between bank rates and alternative lenders isn’t minor; it’s the difference between paying $2,000 and paying $15,000 in interest on a $10,000 loan over five years.

Factors That Influence Rate Pricing

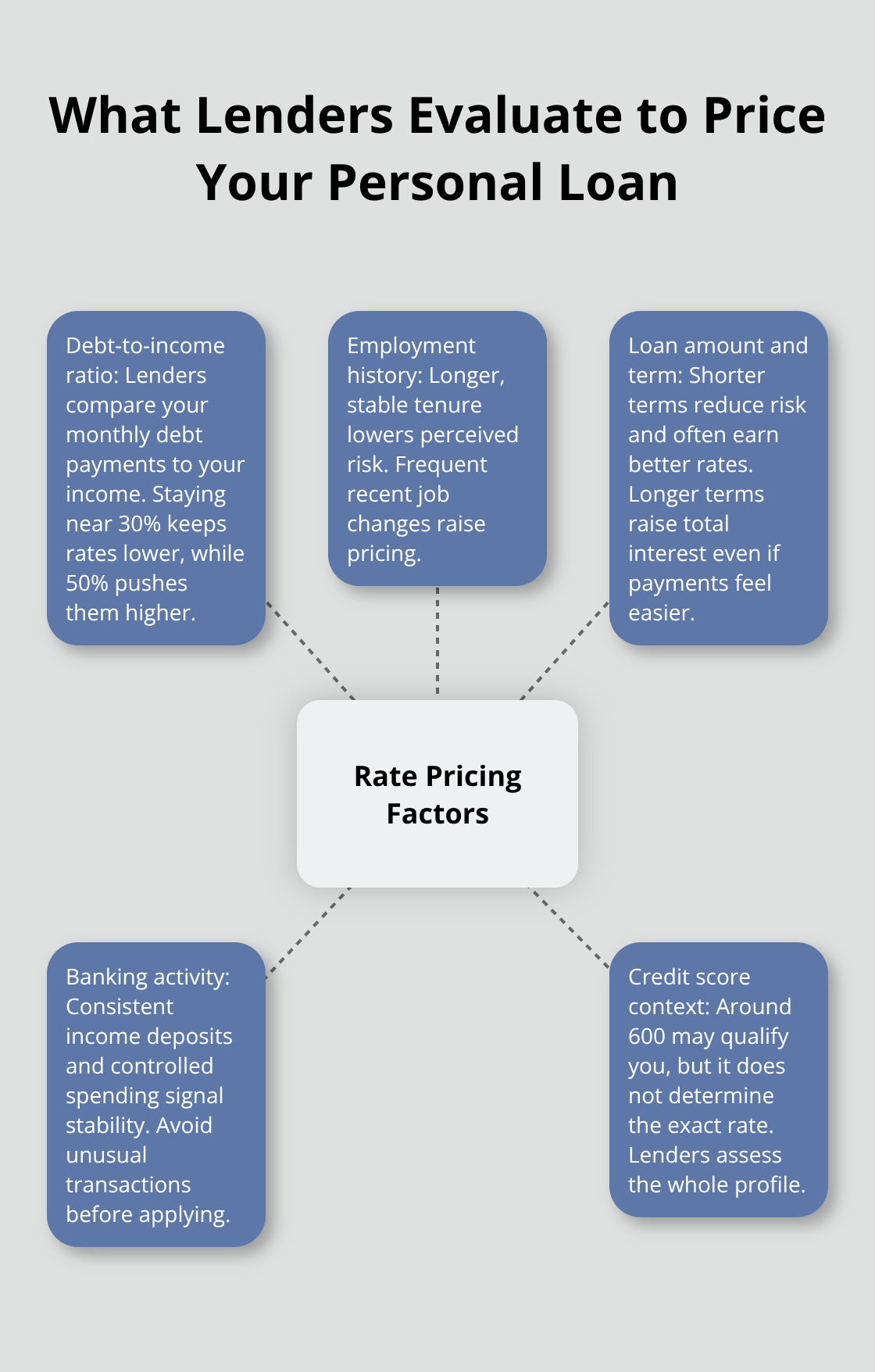

Lenders price loans based on risk, and they measure risk through multiple factors beyond your credit score. Your debt-to-income ratio-the percentage of your monthly income that goes toward existing debt-directly influences what you’ll pay. A borrower with a DTI below 30% typically qualifies for better rates than someone carrying debt equal to 50% of their income.

Employment history also matters significantly. Lenders view someone employed at the same company for five years as lower risk than someone who changed jobs three times in two years. Loan amount and term length affect your rate too. Shorter terms reduce the lender’s risk exposure, often resulting in lower rates, while longer terms increase total interest costs even if the monthly payment feels manageable.

APR includes all fees-origination fees typically range from 0.5% to 8%-so comparing APRs rather than just interest rates gives you the true cost picture.

How Rates Compare to Other Borrowing Options

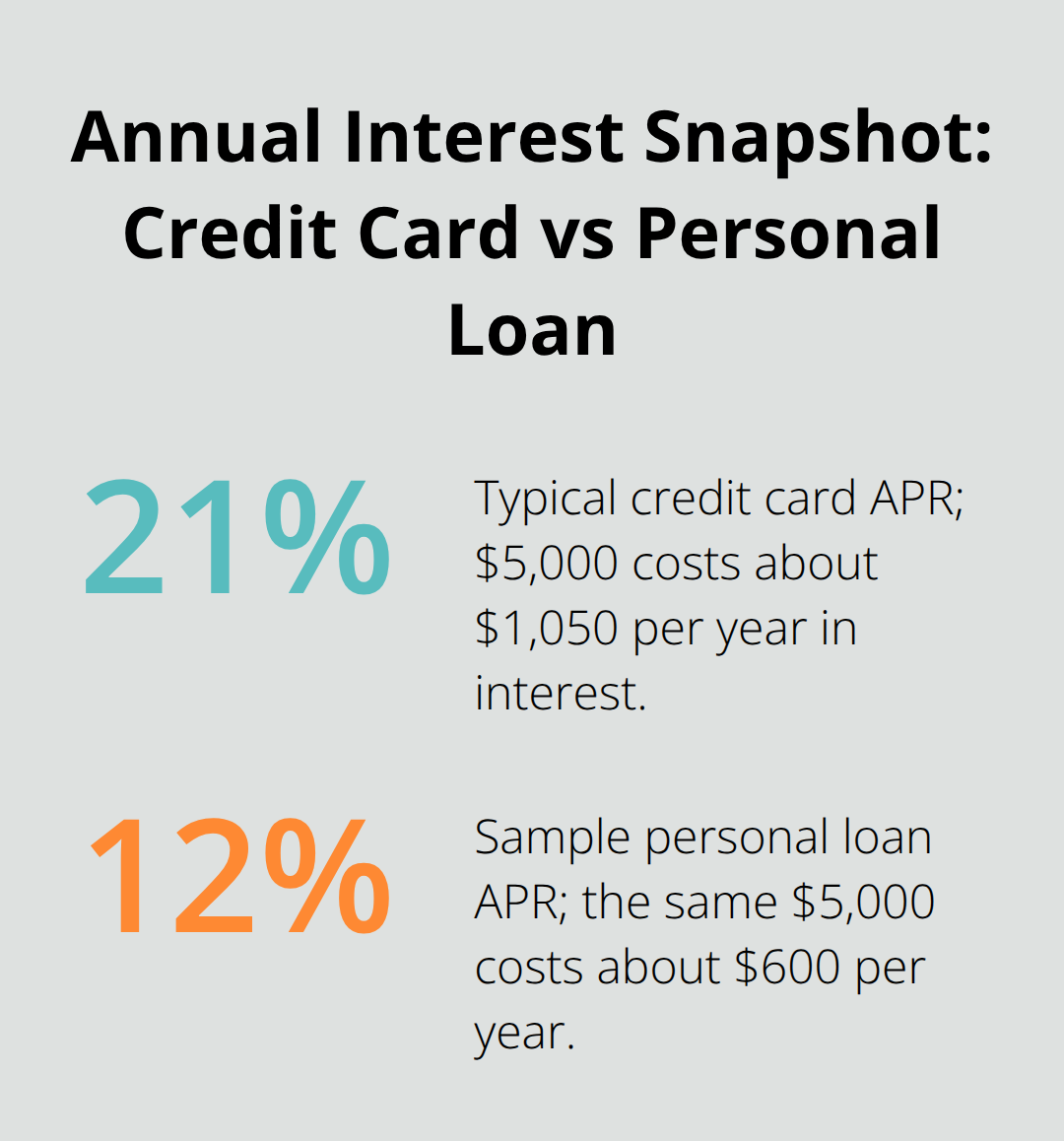

Credit cards currently carry average interest rates around 20% to 21% in Canada, making personal loans the obvious choice for anyone carrying a balance. A $5,000 credit card balance at 21% costs approximately $1,050 annually in interest alone; the same $5,000 borrowed through a personal loan at 12% costs $600.

Lines of credit sit somewhere between personal loans and credit cards, typically ranging from 7% to 10% for prime borrowers, but they’re revolving debt-meaning you can borrow against them repeatedly, which creates the temptation to accumulate more debt. Personal loans force discipline through fixed payments and defined end dates. You know exactly when you’ll be debt-free.

This structure makes personal loans particularly effective for debt consolidation, where you replace multiple high-interest debts with a single fixed payment. Understanding your actual rate-not just the advertised number-requires knowing what lenders actually evaluate when they assess your application.

What Affects Your Personal Loan Rate

Credit Score Tells Only Part of the Story

Your credit score isn’t the only number that determines your personal loan rate-and treating it as if it is causes most borrowers to miss opportunities for better pricing. Lenders evaluate your entire financial picture, and understanding what they measure lets you position yourself strategically before applying. A credit score around 600 qualifies you for approval, but that doesn’t reveal what rate you’ll actually receive. Your debt-to-income ratio matters as much as your credit history. If you carry $2,000 monthly in debt payments and earn $5,000 monthly, your DTI sits at 40%-already above the 30% threshold where rates start climbing noticeably.

Reduce Debt Before You Apply

Reducing existing debt before you apply for a personal loan directly improves your pricing power. Pay down credit card balances or consolidate smaller debts first, then apply. This tactical sequence costs nothing and can save you hundreds in interest. Employment stability ranks equally high in lender assessments. Someone who holds the same position for five years presents dramatically lower risk than someone who switched jobs twice in eighteen months. If you’ve recently changed employers, wait three to six months before you apply if your situation allows.

Lenders also scrutinize your banking activity-they want to see consistent income deposits and controlled spending patterns. Avoid major account changes or unusual transaction patterns in the two months before you apply. Your loan amount and term length work together to influence your rate in ways most borrowers misunderstand.

A $15,000 loan over two years carries lower risk than the same amount spread across five years, so lenders typically quote better rates for shorter terms.

Match Your Term to Your Budget Reality

However, the monthly payment on a two-year term might stretch your budget uncomfortably, which defeats the purpose of borrowing. The real strategy involves calculating what payment you can sustain during a difficult month-not a normal month-and working backward from there. If a $400 monthly payment would stress your finances when income drops, choose the longer term and accept the higher rate. This approach prevents missed payments, which damage your credit far more than paying slightly higher interest.

Compare APRs, Not Interest Rates

According to Ratehub.ca, origination fees ranging from 0.5% to 8% are included in your APR, so comparing the full APR across lenders reveals the true cost difference between options. A lender advertising 9% interest but charging a 5% origination fee costs substantially more than one quoting 10% with no origination fee. Request APR quotes from at least three lenders, verify the loan amount and term match across all quotes, and compare the actual dollar cost over the life of the loan-not just the monthly payment or headline rate. This comparison process exposes which lenders actually offer competitive pricing and which ones hide higher costs behind lower advertised rates. Once you understand your rate, the next step involves finding the lenders that will actually approve you and comparing their specific offers side by side.

How to Find the Best Rate Without Wasting Time

Start Your Search Early and Strategic

Start your search at least two weeks before you need the funds. This timeline lets you compare offers without rushing into a bad deal, and lenders view applications submitted within a short window differently than scattered applications over months. Request APR quotes from two to three lenders simultaneously rather than applying one after another. Each application triggers a hard inquiry on your credit report, and multiple inquiries within 14 days typically count as a single inquiry for credit scoring purposes according to Equifax Canada and TransUnion Canada. Space applications beyond two weeks apart, and each one damages your score independently.

Choose Your Lenders in the Right Order

Contact major banks first-Scotiabank, TD, and RBC all publish their current rates online, and their approval processes move quickly for qualified borrowers. If banks reject you or quote rates above 15%, move to online lenders like Easyfinancial or Nyble. Nyble occasionally offers promotional 0% APR periods, though eligibility restrictions apply. Request the full loan agreement before committing, and read every page. Lenders often bury prepayment penalties in dense contract language, and some charge fees if you pay off the loan early-a cost that makes no sense for your situation.

Understand Fixed Versus Variable Rates

Fixed-rate loans lock your payment for the entire term, making budgeting straightforward and protecting you if the Bank of Canada raises rates. Variable-rate loans move with the central bank’s decisions, and since the Bank of Canada held rates at 2.25% on January 28, 2026, stability appears likely short-term, but variable rates still carry uncertainty. Choose fixed unless your lender offers a substantially lower initial rate and you can absorb payment increases.

Calculate Total Cost, Not Monthly Payment

When you receive offers, the monthly payment isn’t what matters-the total cost over the loan’s life is. A $10,000 loan at 12% over three years costs approximately $1,970 in total interest, while the same loan at 12% over five years costs approximately $3,280. The monthly difference might seem small, but the total difference is substantial. Calculate both scenarios and pick based on what you can afford during a difficult month, not during normal circumstances.

Negotiate and Verify All Costs

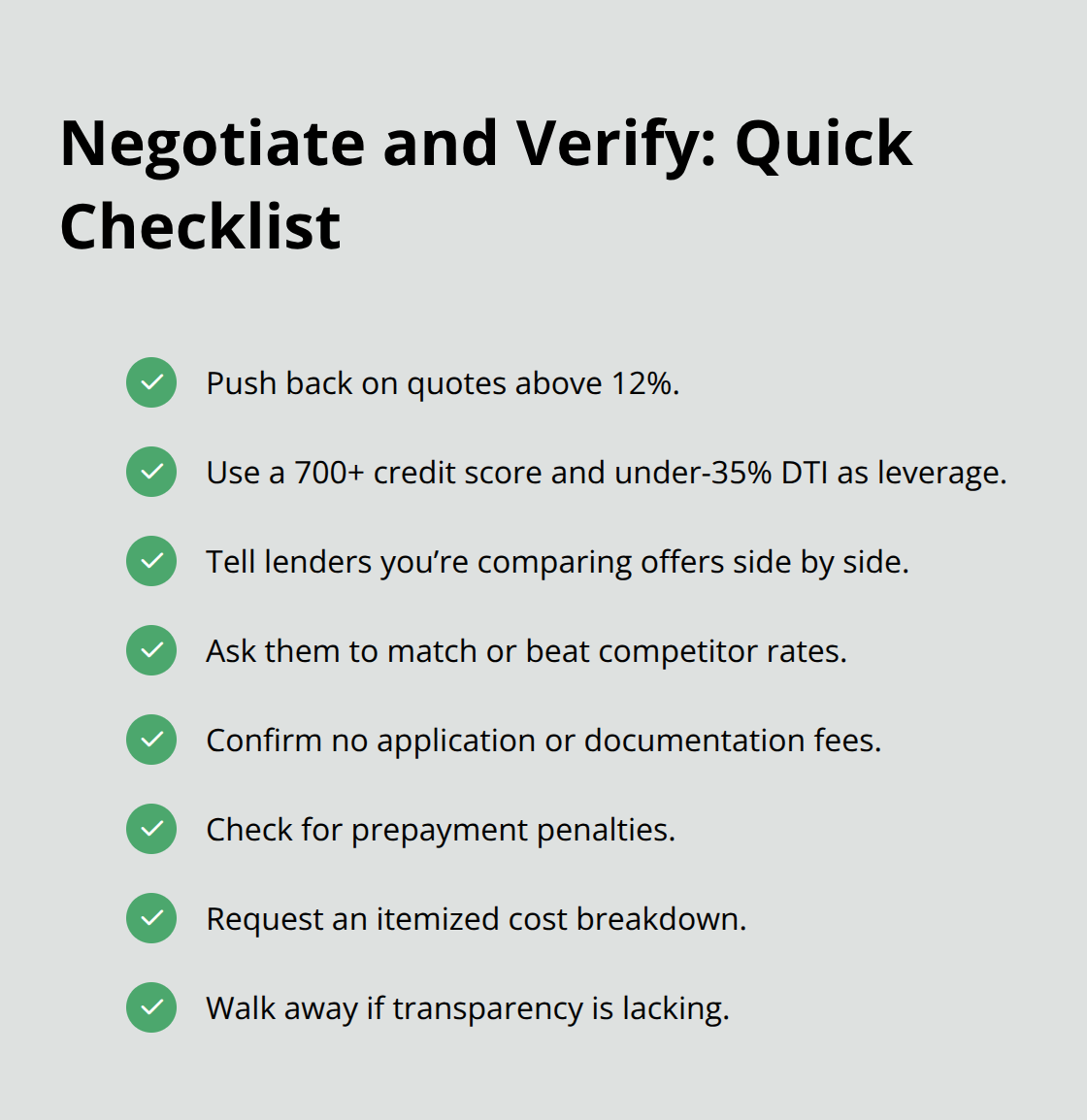

Negotiate aggressively with lenders who quote rates above 12%. If your credit score exceeds 700 and your debt-to-income ratio sits below 35%, you have leverage. Tell the lender you’re comparing their offer against others and ask them to match or beat competitor rates. Large banks sometimes reduce rates by one to two percentage points when borrowers push back.

Before signing, verify there are no application fees, documentation fees, or early repayment penalties. Some lenders charge $50 to $300 just to process your application, and these fees sometimes appear separately from origination fees. Request an itemized breakdown of all costs, and if a lender refuses to provide one, walk away.

Final Thoughts

Personal loans Canada rates range from 6% to 46% depending on your lender and financial profile, but the actual rate you receive depends entirely on decisions you control. The most important takeaway is this: your rate isn’t fixed until you sign the agreement, and understanding what lenders evaluate gives you real power to negotiate better terms. Before you apply, reduce your debt-to-income ratio by paying down existing balances, wait three to six months after changing jobs if possible, and request APR quotes from two to three lenders within a 14-day window to minimize credit report damage.

Read every page of the loan agreement and ask for an itemized breakdown of all fees, including origination costs and prepayment penalties. Calculate the total interest you’ll pay over the loan’s life, not just the monthly payment, and choose a term you can afford during a difficult month, not a normal one. When comparing offers, ignore advertised interest rates and focus exclusively on APR, which includes all fees-negotiate aggressively if your credit score exceeds 700 and your debt-to-income ratio sits below 35%, since major banks sometimes reduce rates by one to two percentage points when borrowers push back.

The difference between a 9% rate and a 15% rate on a $10,000 loan over five years is roughly $3,600 in total interest, which justifies spending two weeks on comparison shopping. Start your search today, even if you don’t need funds immediately, because early comparison shopping removes pressure and prevents rushed decisions. We at Financial Canadian help you build a strong financial foundation with resources and guidance tailored to your situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment