Need cash but don’t want to put your home or car at risk? Unsecured personal loans in Canada offer a way to borrow money without pledging collateral, making them an attractive option for many borrowers.

At Financial Canadian, we’ve seen firsthand how these loans can provide the flexibility people need. However, they come with trade-offs you should understand before applying.

What Unsecured Personal Loans Actually Are

How They Work

An unsecured personal loan is straightforward: you borrow money from a lender without putting up any asset as collateral. If you fail to repay, the lender cannot seize your home, car, or other property. Instead, they rely on your credit history, income verification, and your promise to repay. In Canada, unsecured personal loans typically range from $2,000 to $35,000, with repayment terms spanning 24 to 84 months. According to Ratehub.ca, current APRs generally range from about 6% to 35% depending on your credit profile, income, and the lender you choose. Major banks like CIBC, Scotiabank, and TD advertise starting rates around 6% to 10% for well-qualified borrowers, though most Canadians fall into the 9% to 24% range. The application process happens almost entirely online with minimal verification steps, and funding can arrive as early as one business day after approval.

Speed When You Need It

This speed matters when you face unexpected expenses or time-sensitive needs. You can check your personalized rate in under 60 seconds without impacting your credit score, allowing you to make faster decisions. Fixed interest rates and fixed monthly payments help you budget and predict your cash flow accurately. Early repayment carries no penalties, so you can save on interest if your financial situation improves.

Why Unsecured Loans Cost More

The fundamental difference between unsecured and secured loans comes down to risk. Secured loans require collateral-typically your home or vehicle-which gives lenders recourse if you default. This lower risk allows them to offer better rates; GICs and high-interest savings accounts currently offer 2.25% to 4.75%, reflecting the Bank of Canada’s overnight rate of 2.25%. Unsecured loans carry significantly higher risk because lenders have no asset to recover if you stop paying. That’s why they charge higher interest rates and cap borrowing limits.

According to Allied Market Research, unsecured personal loans carry higher interest rates than secured options specifically because lenders absorb more risk. This means lenders scrutinize your credit score heavily and may decline applications from borrowers with poor credit histories. They also evaluate your debt-to-income ratio carefully to confirm you can actually afford the monthly payments. For lenders, this higher risk justifies charging rates up to 35% APR-the legal maximum in Canada.

What This Means for You

In exchange, you avoid risking your assets, which makes unsecured loans genuinely valuable when you need flexibility without putting everything on the line. This trade-off-higher rates in exchange for no collateral-shapes every decision you’ll make when comparing lenders and evaluating whether an unsecured loan fits your situation.

Why Unsecured Loans Win When You Need Speed and Flexibility

Speed That Matters When Time Is Short

The real advantage of unsecured personal loans in Canada isn’t just the absence of collateral-it’s what that absence enables. When you don’t need to pledge your home or vehicle, lenders can approve your application quickly. Personal loan approval at a credit union may take one to three business days, and funding may take three or more business days. The online application process requires minimal verification steps, and you can check your personalized rate in under 60 seconds without any impact to your credit score. This speed creates genuine value for borrowers who can’t afford to wait through the lengthy appraisal and documentation processes that secured loans demand. You also avoid the stress of having your assets evaluated or risking foreclosure if circumstances change.

Complete Freedom in How You Spend the Money

Unsecured loans give you complete freedom in how you spend the money. These unsecured loans can be used to consolidate various types of debt, including credit card balances and medical bills, or for any other legitimate purpose. This flexibility extends to repayment as well-early repayment carries no penalties, meaning if your financial situation improves and you want to eliminate the debt faster, you can do so without paying extra fees.

Predictable Costs Throughout Your Loan Term

Fixed monthly payments and fixed interest rates mean your costs remain predictable throughout the loan term, which helps you budget accurately and plan your cash flow. Whether you borrow $2,000 for an unexpected car repair or $35,000 for a major life event, you know exactly what you’ll pay each month for 24 to 84 months. This combination of speed, freedom, and predictability makes unsecured personal loans a practical choice for Canadians who need straightforward access to capital without surrendering their assets or navigating complex approval processes.

However, this flexibility and speed come at a cost-and understanding those costs is essential before you commit to any lender.

What Costs You’ll Actually Pay

Interest Rates That Vary Widely Based on Your Profile

The speed and flexibility of unsecured personal loans come with a genuine price tag that extends far beyond the advertised interest rate. According to Ratehub.ca, current personal loan APRs in Canada generally range from 6% to 35% depending on your credit profile, income, and lender. Major banks advertise starting rates around 6% to 10% for well-qualified borrowers, but most Canadians fall into the 9% to 24% range. This matters because a 15% APR on a $15,000 loan over five years costs you roughly $4,900 in interest alone, while a 24% APR on the same amount costs nearly $8,000.

Origination fees add another layer of cost, typically ranging from 0.5% to 8% of the loan amount. Some lenders deduct these fees from your cash disbursement, meaning a $10,000 loan with a 5% origination fee might only put $9,500 in your account. When shopping for lenders, comparing APR rather than just the interest rate is essential because APR includes all fees and reflects your true cost.

The Legal Maximum and What It Means

The Bank of Canada established a criminal rate cap of 35% APR effective January 1, 2025, which is the legal maximum any lender can charge. Reaching that ceiling means your borrowing costs spiral quickly, so understanding where you fall on the rate spectrum matters significantly for your financial planning.

How Your Credit Score Determines Your Rate

Your credit score directly determines which rates you’ll qualify for, and this creates a harsh reality for many borrowers. Lenders pull your credit reports from Equifax Canada or TransUnion Canada and use them to assess eligibility and rate offers. If your credit score falls below 660, you’ll face higher rates or potential rejection from traditional banks, pushing you toward private lenders with rates exceeding 20% or 25%.

Debt-to-income ratio is another critical hurdle lenders evaluate carefully. If your monthly debt payments already consume 40% or more of your gross income, approval becomes difficult or impossible, regardless of your credit score. This stricter underwriting means unsecured loans simply aren’t available to everyone, and those with weaker profiles pay substantially more for the privilege of borrowing.

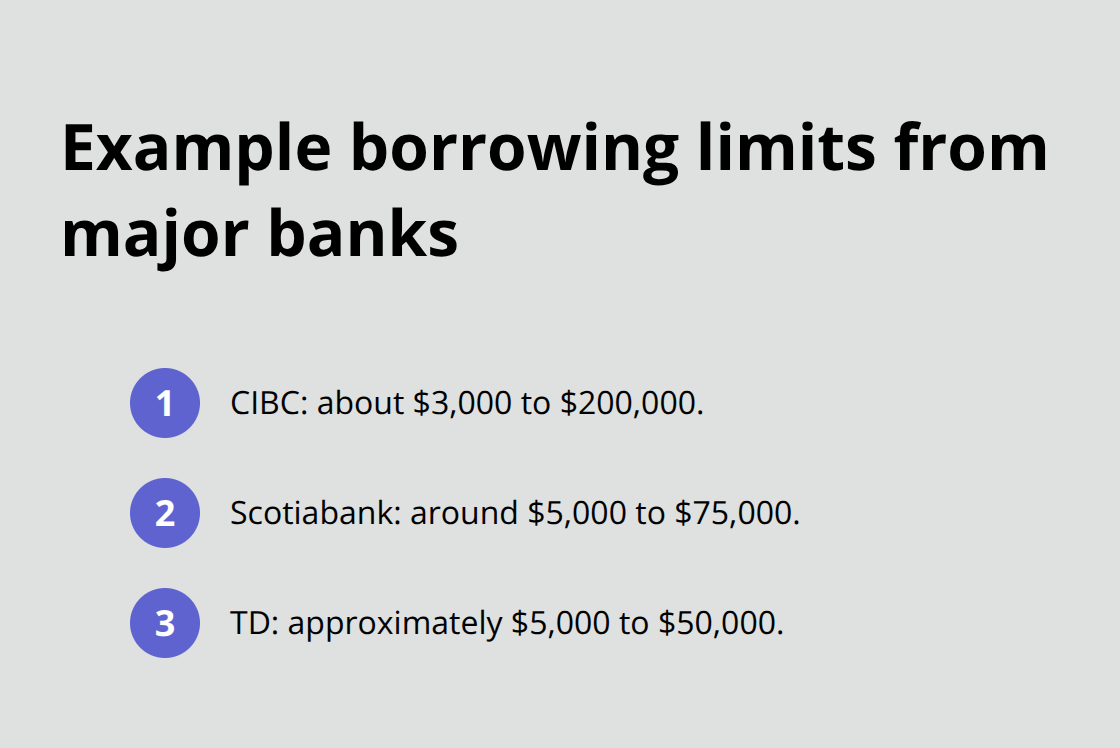

Borrowing Limits That Constrain Your Options

Maximum loan amounts reflect this risk calculus as well. While major banks offer ranges like CIBC at roughly $3,000 to $200,000, Scotiabank around $5,000 to $75,000, and TD approximately $5,000 to $50,000 according to Ratehub.ca, most borrowers with average credit qualify for far less. If you need $25,000 but your credit profile only qualifies you for $15,000, you’ll either need to find additional financing elsewhere or abandon part of your project, creating real constraints on what unsecured loans can accomplish for your situation.

Final Thoughts

Unsecured personal loans in Canada make sense when you need quick access to funds without risking your home or vehicle, but only if you understand the true cost. Focus on APR rather than advertised interest rates, since APR includes all fees and reflects your actual borrowing cost. Pull your credit reports from Equifax Canada or TransUnion Canada before applying so you understand where lenders will position you on their rate spectrum.

Calculate the total interest you’ll pay over your chosen term-a $15,000 loan at 15% APR over five years costs roughly $4,900 in interest, while the same loan at 24% costs nearly $8,000. Verify that early repayment carries no penalties so you can accelerate payoff if your situation improves. Major banks like CIBC, Scotiabank, and TD offer competitive starting rates for qualified borrowers, while online lenders and credit unions often provide faster approvals.

Take time to compare offers across multiple lenders, understand your actual costs, and borrow only what you genuinely need. At Financial Canadian, we help you make informed financial decisions through practical guides and rate comparisons that cut through the noise. Unsecured personal loans in Canada offer real flexibility when you shop carefully and understand the full picture before signing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment