When unexpected expenses hit, an emergency loan in Canada can be the difference between staying afloat and falling behind. Most Canadians don’t have enough savings to cover sudden costs, which is why knowing your borrowing options matters.

At Financial Canadian, we’ve put together this guide to help you understand emergency loans, qualify for one, and find a lender that actually works for your situation. You’ll learn what separates emergency loans from traditional options and how to access funds fast.

What Emergency Loans Actually Are

An emergency loan in Canada is simply borrowed money you access quickly when unexpected expenses arrive. Unlike traditional bank loans that take weeks to approve, emergency loans prioritize speed over lengthy application processes. According to the Financial Consumer Agency of Canada (FCAC), Canadians can access emergency funds through banks, credit unions, and licensed online lenders, though provincial regulations create different requirements depending on where you live. The real purpose here is straightforward: bridge the gap between when a crisis hits and when you can cover it with your own cash. Statistics Canada data shows that household debt remains elevated relative to disposable income, which is why many Canadians turn to emergency borrowing when car repairs, medical bills, or job disruptions occur without warning.

How Emergency Loans Differ from Regular Bank Loans

Traditional bank loans require 5–10 business days for approval and demand extensive documentation, credit checks, and employment verification. Emergency loans compress this timeline dramatically. Online lenders often provide instant decisions and can deposit funds within hours, according to FCAC research, making them genuinely useful when you need money today rather than next month. The trade-off is real though: emergency loans carry higher interest rates because lenders accept more risk by moving faster and lending to people with weaker credit profiles. A personal loan from a bank or credit union offers lower interest rates and clearer terms compared to payday loans or other high-cost emergency options, so the cheapest emergency loan isn’t always the fastest one. You need to decide whether speed or cost matters more for your specific situation.

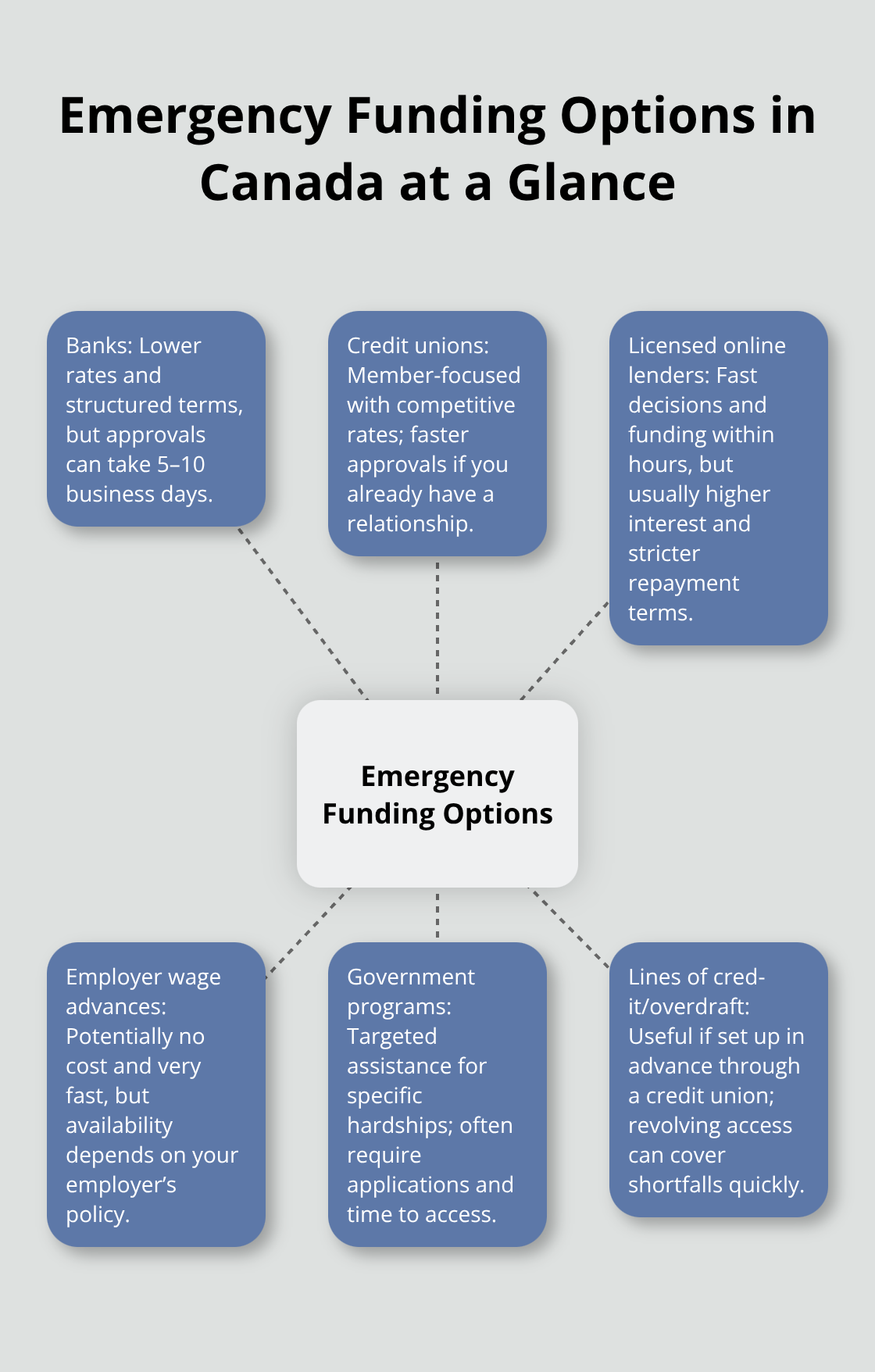

Types of Emergency Funding Available to You

Credit card cash advances deliver money within hours if you already have a card with available credit, but they charge fees and higher interest rates that make them expensive for anything beyond immediate emergencies. Personal loans from banks and credit unions provide lower rates and fixed repayment schedules, though approval takes several days. Licensed online lenders split the difference with faster approval than traditional banks but rates higher than credit unions. Some employers offer wage advances that cost nothing, and government programs exist in most provinces for specific hardships (though these require time to access). A credit union line of credit or overdraft protection works if you’re already a member and have established a relationship.

FCAC recommends starting with a precise amount you need, your repayment deadline, and a realistic plan to choose the option that’s actually cheapest and fastest for your circumstances rather than picking the first lender you find.

What Shapes Your Choice

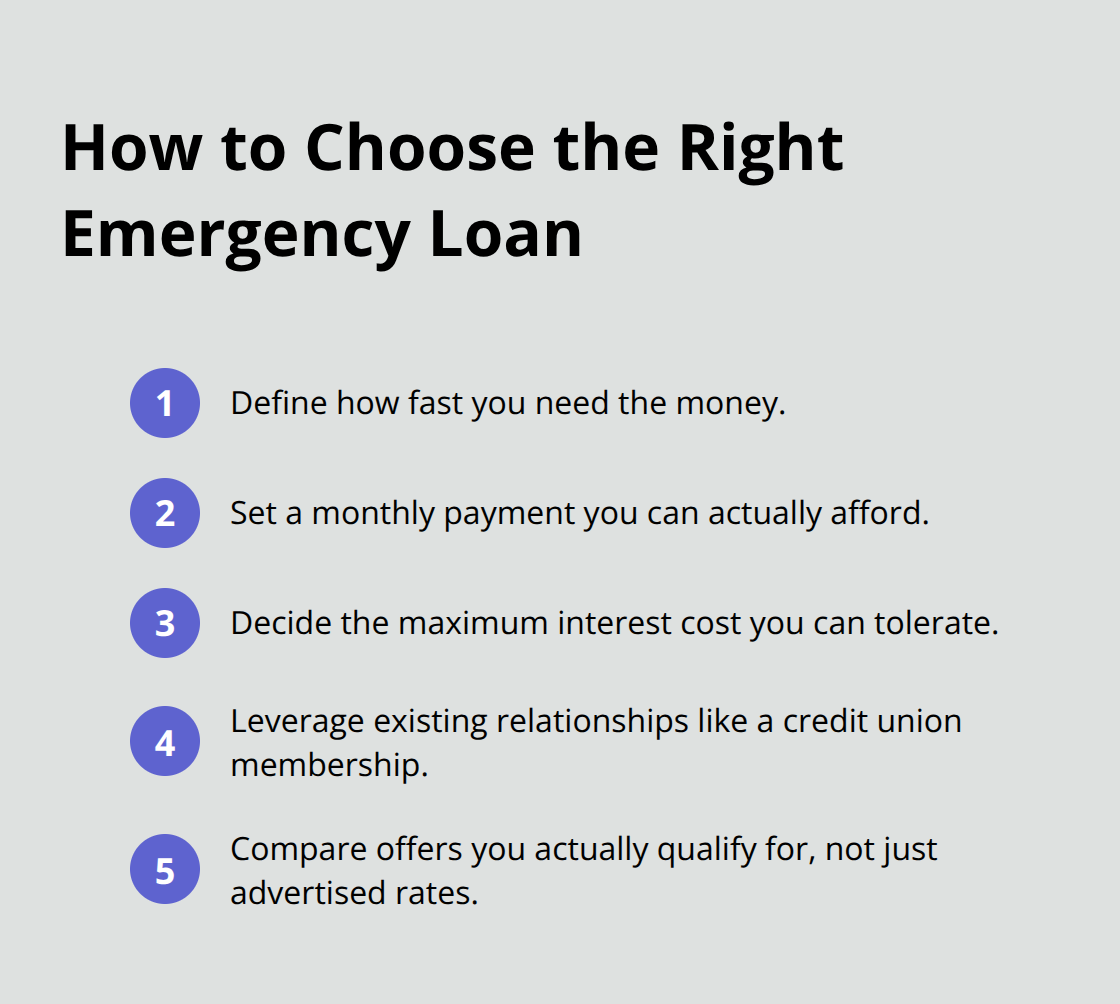

The decision between emergency loan types depends on three factors: how fast you need the money, how much you can afford to pay back monthly, and what interest rate you can tolerate. A credit card cash advance wins on speed but loses on cost. A bank personal loan costs less but takes longer. Online lenders (which operate under provincial licensing rules) land somewhere in the middle for both speed and expense. Your existing relationships matter too-credit union members often qualify faster and receive better rates than new applicants at traditional banks. The cheapest option today might not be available to you, so comparing what you actually qualify for beats chasing the lowest advertised rate.

How to Qualify for an Emergency Loan in Canada

Most emergency lenders in Canada focus on three core qualification areas: your ability to repay, your income stability, and basic documentation. Unlike traditional banks that scrutinize your credit history extensively, emergency lenders care most about whether you earn enough to handle monthly payments. FCAC research shows that lenders typically require proof of monthly income above a minimum threshold, though this varies by lender and province. Employment verification usually means a recent pay stub or employment letter rather than extensive background checks. Self-employed borrowers face stricter requirements and often need 2 years of tax returns or business financial statements to prove consistent income. If you’re unemployed or have zero monthly income, most emergency lenders will reject you outright, regardless of how bad your situation is.

Income and Employment Requirements

Lenders want proof that you can actually repay what you borrow. A steady paycheck matters far more than your job title or industry. FCAC data shows that salaried employees with consistent income qualify faster than contract workers or gig economy participants. You’ll need to provide recent pay stubs (usually from the last 30 days) that show your employer name, gross income, and deductions. Employment letters work too, especially if they confirm your position, start date, and expected salary. Self-employed applicants must submit 2 years of tax returns or business financial statements to demonstrate income stability. Seasonal workers sometimes struggle because lenders worry about income gaps during off-months. If your income fluctuates, lenders often average your earnings over the past year to calculate what you can borrow.

Credit Score Considerations

Your credit score matters less for emergency loans than it does for traditional bank products, but it’s not irrelevant. Borrowers with scores below 600 typically face higher interest rates or get declined by reputable lenders, forcing them toward predatory high-cost options. Online lenders often accept scores as low as 500, but rates climb dramatically at that level. A score between 650 and 750 opens access to reasonable rates from multiple lenders. Hard inquiries from loan applications temporarily dip your score by a few points according to credit bureaus, so avoid applying to five lenders in one week. Instead, pre-qualify with lenders that use soft inquiries, which don’t impact your score at all.

Documentation You’ll Need to Prepare

Lenders ask for straightforward paperwork: government-issued ID, proof of income (pay stub or tax return), proof of address (utility bill or lease), and bank statements showing you can manage the monthly payment. Some lenders request references or employer contact details. Gather these documents before you apply so you can move quickly when you find a lender. Having everything ready cuts approval time significantly. Lenders in different provinces may ask for additional provincial identification or proof of residency, so check your provincial regulator’s requirements before submitting your application.

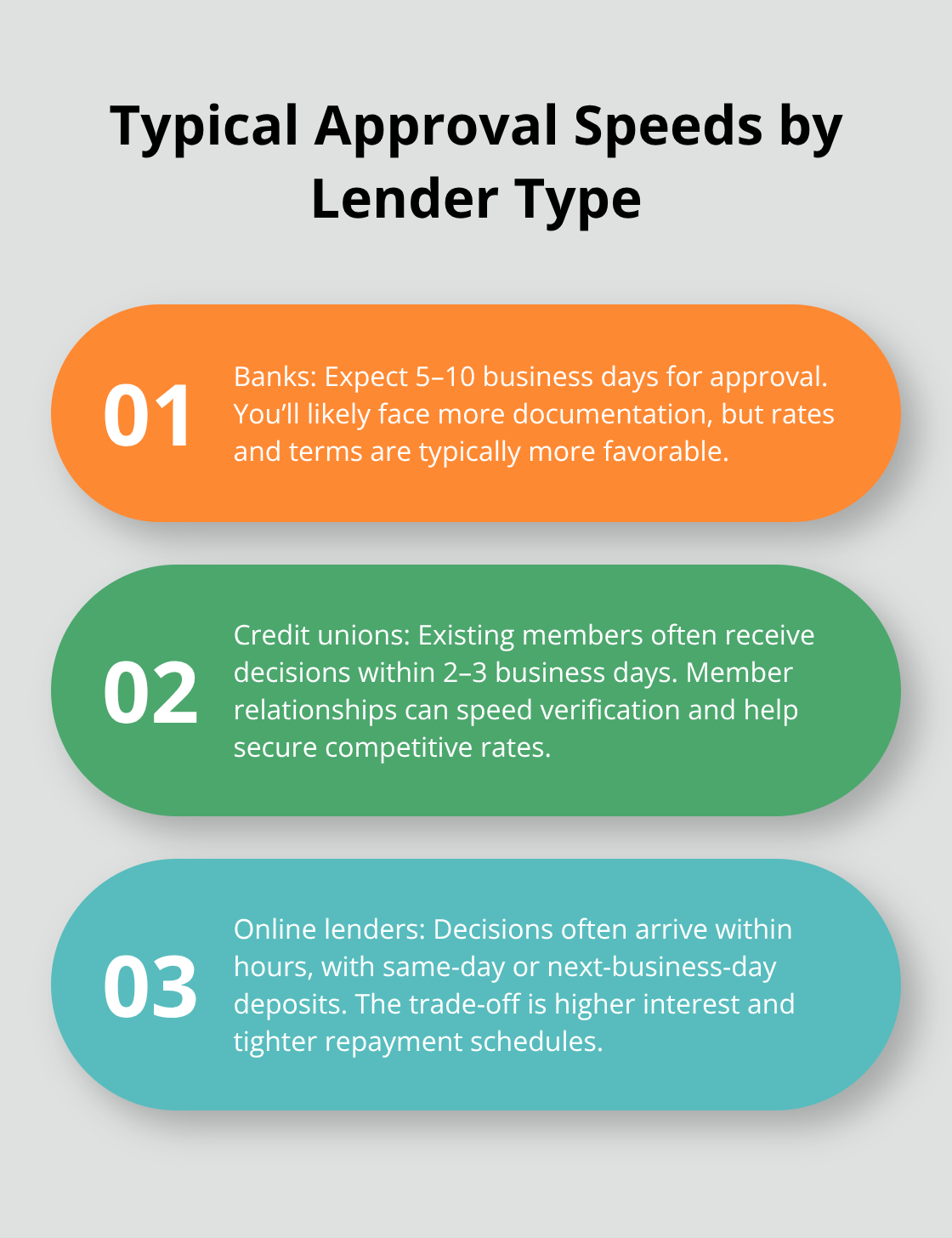

Timeline for Approval and Funding

Approval timelines vary sharply depending on lender type. Banks take 5–10 business days. Credit unions often move faster if you’re an existing member, sometimes within 2–3 business days.

Online lenders frequently provide decisions within hours and deposit funds the same day or next business day. The speed advantage of online lenders comes with a cost: higher interest rates and stricter repayment terms. If you need money within 24 hours, credit card cash advances remain the fastest option, though fees and rates make them expensive for anything beyond immediate emergencies. Once you understand what lenders actually check, the next step is finding the right provider for your specific needs and financial situation.

Finding the Right Emergency Loan Provider

Calculate Total Cost, Not Just Interest Rates

Interest rates alone tell you almost nothing because a 15% APR on a two-week loan costs far less than a 12% APR on a six-month loan. The Financial Consumer Agency of Canada recommends using a standardized comparison checklist that tracks total cost, monthly payment, term length, fees, and prepayment options for every lender you consider. Calculate the total amount you’ll repay, not just the interest rate. Enter the amount borrowed, the repayment term (number of months) and average interest rate you hope to be offered. The calculator returns a monthly payment.

Origination fees, prepayment penalties, and late payment charges add hidden costs that advertised rates never mention. Some lenders charge 5% origination fees upfront, others charge nothing. Some penalize you for paying early, which makes no sense when you’re trying to escape debt. Online lenders operating under provincial licensing rules must disclose all fees clearly, so compare the true cost across at least three lenders before committing. Avoid the temptation to pick the first lender that approves you. Speed matters when you need money today, but choosing a lender with a 25% APR because they fund in four hours instead of two days often costs you hundreds of dollars you don’t have to spend.

Verify Licensing and Check Reputation

Reputation and customer experience separate legitimate lenders from problematic ones. Check whether a lender holds valid provincial licensing through your province’s financial regulator, not just online reviews that anyone can fake. Customer reviews on independent sites like Trustpilot or Google show patterns in how lenders treat borrowers after approval. Look for complaints about sudden rate increases, aggressive collection practices, or difficulty accessing customer service when problems arise. The worst emergency lenders use aggressive collection tactics that damage your credit and cause stress when life gets difficult.

Verify licensing status directly with your provincial regulator before applying anywhere. If a lender won’t disclose their license number or doesn’t appear in your province’s registry, walk away immediately. Beware of lenders charging upfront fees before you receive any money, which is a hallmark of predatory lending. FCAC identifies this as a major red flag indicating a scam. Contact the lender early if repayment becomes difficult rather than ignoring the problem, because responsible lenders offer hardship options that can prevent your situation from spiraling into unmanageable debt.

Final Thoughts

An emergency loan in Canada offers multiple pathways to fast cash, each with distinct speed and cost trade-offs that you must weigh against your specific situation. Credit card cash advances move fastest but carry the highest fees, while personal loans from banks and credit unions cost less but require more time. Online lenders licensed in your province land somewhere in the middle for both speed and expense, making them a reasonable option when you need funds within hours rather than days. The choice that works best depends entirely on how quickly you need money and what monthly payment fits your budget.

When you select a lender, calculate total repayment cost across the entire loan term rather than fixating on the advertised interest rate (a lower APR over six months often costs more than a higher rate over two weeks). Verify that your lender holds valid provincial licensing and check customer reviews on independent platforms to spot patterns in how they treat borrowers after approval. Understand all fees upfront, including origination charges, prepayment penalties, and late payment costs that lenders sometimes hide in fine print, then compare at least three options side by side before committing to any single provider.

The strongest position you can build is an emergency fund covering three to six months of essential expenses, which reduces your dependence on emergency borrowing altogether. Until you reach that goal, knowing your options and choosing carefully when you do borrow keeps costs manageable and prevents debt from spiraling out of control. We at Financial Canadian help you make informed financial decisions through clear, practical guidance-explore our resources to support your financial health and decision-making process.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment