Mortgages are one of the biggest financial decisions you’ll make in Canada. Whether you’re a first-time buyer or refinancing, understanding your options matters.

We at Financial Canadian have created this guide to help you navigate the mortgage landscape. You’ll learn about different mortgage types, what affects your rates, and how to pick the right option for your situation.

Types of Mortgages Available in Canada

Fixed-Rate Mortgages Lock Your Payment in Place

Fixed-rate mortgages lock your interest rate for the entire term, typically 5 years in Canada. Your payment stays the same whether rates climb to 7% or drop to 2%. The trade-off is real: fixed rates run higher than variable rates at the start because lenders price in uncertainty. Right now, 5-year fixed rates hover around 4.5–5.2%, while variable rates sit closer to 6.5% tied to the Bank of Canada’s prime rate.

The fixed option wins if you plan to stay put, hate payment surprises, or believe rates will rise. It loses if rates fall sharply and you’re locked in, though some lenders allow you to blend your rate down if you renew early with them.

Variable-Rate Mortgages Move With the Bank of Canada

Variable-rate mortgages move with the Bank of Canada’s overnight rate, which means your payment can jump when the central bank tightens policy. CMHC data shows borrowers increasingly shifted toward variable and shorter-term mortgages as renewal pressures eased, signaling confidence in rate stability ahead.

The advantage: you capture immediate savings when rates drop, sometimes 0.5–1.5% below fixed. The danger arrives when rates spike; your payment climbs, and you must plan for that shock.

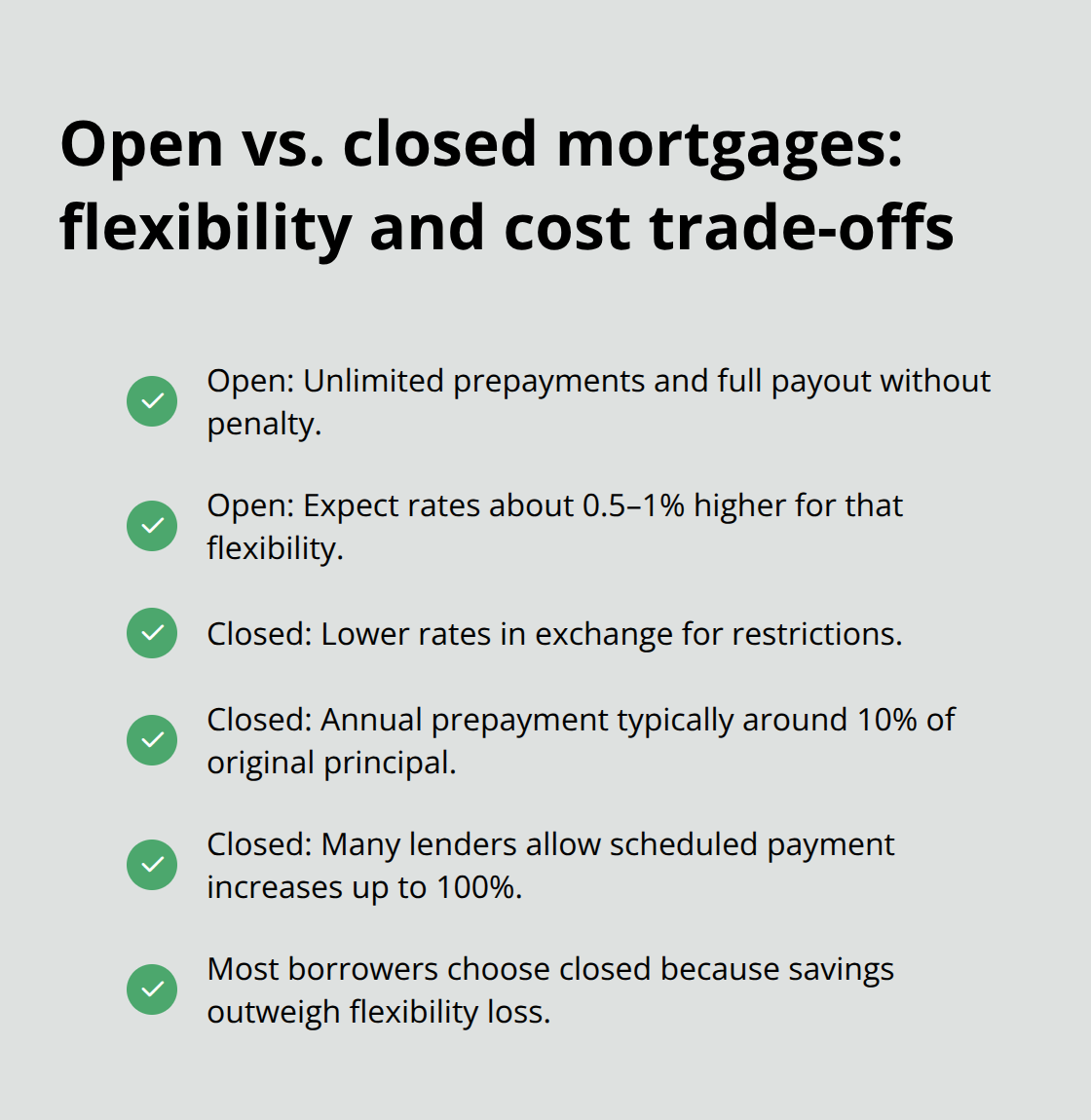

Open Versus Closed: Flexibility Comes at a Cost

Open versus closed mortgages represent a key trade-off in your financing structure. Open mortgages let you make unlimited extra payments or pay off the entire balance without penalty, but they charge 0.5–1% higher rates as compensation. Closed mortgages restrict annual prepayment to around 10% of the original principal, yet offer lower rates in return.

Most borrowers pick closed because the rate savings outweigh the flexibility loss-you can still pay extra up to your annual cap and increase scheduled payments by up to 100%. The real decision comes down to your comfort with rate risk and payment stability.

Matching Your Mortgage Type to Your Situation

If you value certainty and plan to hold the property long-term, fixed is your answer. If you can absorb payment increases and rates look like they’ll fall, variable makes financial sense. Your choice here directly shapes how much you’ll pay over time and how much stress you’ll feel when rates move-which is why the next step involves understanding what actually moves those rates in your favor or against you.

Key Factors That Affect Your Mortgage

Your Credit Score Opens or Closes Doors

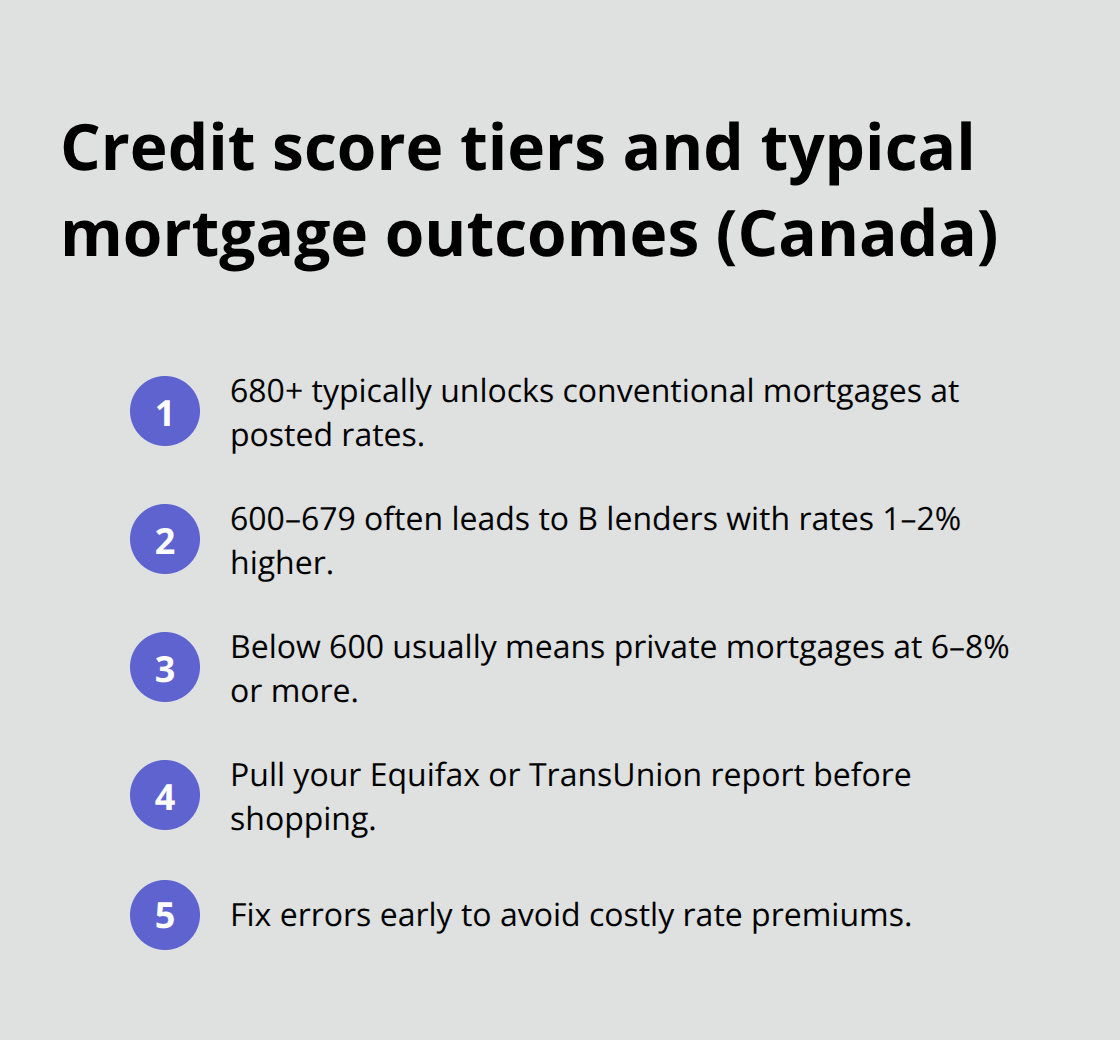

Your credit score acts as the first gatekeeper in mortgage qualification. Lenders pull your credit report and score to determine whether you qualify and at what rate. A score above 680 typically unlocks conventional mortgages at posted rates, while scores between 600 and 680 push you toward B lenders with rates 1–2% higher. Below 600, private mortgages become your only option, often costing 6–8% or more. Statistics Canada employment data from June 2026 showed joblessness at 6.5%, a tightening labour market that reinforces lender caution around credit risk.

You should pull your credit report now through Equifax or TransUnion before mortgage hunting. Fix errors immediately-they can cost you thousands in rate premiums.

Down Payment Size Controls Insurance Costs and Borrowing Power

Down payment size directly controls whether you need mortgage insurance and how much you’ll pay overall. Put down less than 20% and you enter high-ratio territory, triggering insurance premiums that add 2–4% to your loan balance depending on how low you go. A 5% down payment on a $600,000 home means $30,000 down and $570,000 borrowed; mortgage insurance then adds roughly $11,400–$22,800 to what you owe. Conventional mortgages with 20% down eliminate this cost entirely. The current market shows Royal LePage forecasting stronger national housing prices for 2026 as demand outpaces supply in several regions, which means negotiating a lower purchase price to boost your effective down payment percentage is harder now than it was two years ago. Try for at least 15% down if possible-it meaningfully reduces total interest paid and removes the insurance drag on your borrowing power.

Bank of Canada Policy Rate Expectations Shape Your Monthly Reality

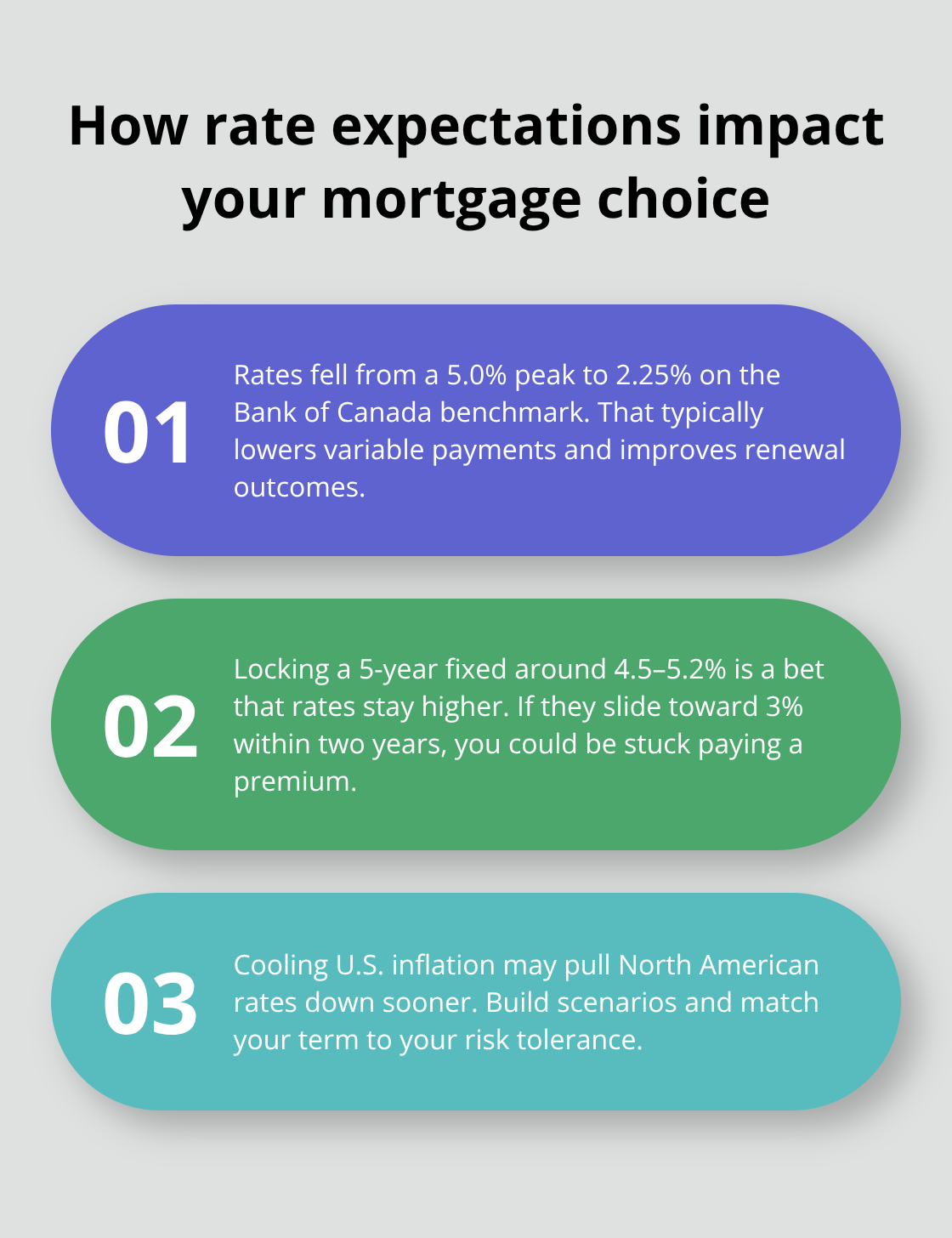

Bank of Canada policy rate expectations matter enormously. The Bank of Canada’s benchmark interest rate has dropped substantially to 2.25% from a high of 5.0%, which would lower variable-rate mortgages and improve renewal outcomes for borrowers. If you lock a 5-year fixed now around 4.5–5.2%, you’re betting rates stay elevated; if they fall to 3% within two years, you’re stuck paying the premium. U.S. CPI fell in June for the first time since 2020, signaling potential cooling in North American inflation that could trigger Bank of Canada cuts sooner rather than later.

You should calculate your payment under three rate scenarios-current, 1% higher, and 1% lower-to understand your true stress tolerance before committing. Shop multiple lenders because rate discounts of 0.25–0.5% are common, and that spread compounds significantly over a 25-year amortization.

The next step involves taking these rate and affordability factors and matching them to your personal situation-which is where the real work of choosing the right mortgage begins.

Which Mortgage Timeline and Lender Match Your Reality

Anchor Your Choice to Your Actual Timeline

Start with your real timeline, not wishful thinking. If you plan to sell or refinance within five years, a variable-rate mortgage or short-term fixed (3-year) makes mathematical sense because you avoid the penalty zone entirely and capture rate savings early. Statistics Canada employment data from June 2026 showed the jobless rate at 6.5%, tightening the labour market and making income stability a genuine concern-if your job security feels uncertain, lock a fixed rate now rather than gambling on variable savings. Conversely, if you’re buying to stay 10+ years and your income grows predictably, variable rates typically save you $40,000–$80,000 over the amortization because rate cycles eventually turn in your favor.

Test Your Payment Stress Tolerance

Pull your employment contract and mortgage documents side by side. Write down the exact month your term renews. Calculate your stress tolerance by testing payment increases of 1%, 2%, and 3% against your household budget. If a 2% rate increase breaks your monthly cash flow, fixed-rate mortgages eliminate that anxiety even though they cost more upfront. This single exercise separates borrowers who panic-sell or default during rate spikes from those who sleep at night.

Shop Multiple Lenders and Brokers for Rate Discounts

Shop at least three lenders and one mortgage broker because rate discounts of 0.25–0.5% are standard and non-negotiable. Chartered banks hold a significant share of Canada’s mortgage market according to OSFI data, but credit unions and mortgage finance corporations often beat their posted rates for qualified borrowers. Request a formal rate quote in writing from each lender specifying the exact term length, amortization, and any prepayment rules. Use a mortgage calculator to compare total interest paid across scenarios rather than fixating on the monthly payment alone-a lower rate saves far more than a slightly higher payment costs.

Calculate Your Stress Test Payment and Leverage Market Conditions

Calculate the stress test payment yourself: take your mortgage amount and apply the Bank of Canada’s benchmark rate plus 2% to confirm you qualify, then subtract your actual approved rate to see your real payment cushion. Royal LePage’s 2026 housing price forecast shows demand outpacing supply in several regions, which means sellers are less desperate to negotiate and lenders are confident in collateral value-use this leverage to demand rate discounts or closing cost coverage from your chosen lender. If a broker connects you with a B lender charging 1% more than your bank’s offer, walk away immediately; the convenience is never worth the extra cost unless conventional financing genuinely rejected you.

Final Thoughts

You now understand the core mortgage types available in Canada, what moves your rates, and how to match your financial situation to the right product. Fixed-rate mortgages offer payment stability at a higher cost; variable-rate mortgages capture savings when rates fall but expose you to payment shock when they rise. Your credit score, down payment size, and the Bank of Canada’s policy direction shape whether you qualify and what you’ll pay.

Pull your credit report and fix any errors immediately. Calculate your stress test payment and confirm you can absorb a 2% rate increase without breaking your budget. Shop at least three lenders and one mortgage broker for written rate quotes, comparing total interest paid rather than monthly payment alone, and request rate discounts of 0.25–0.5% as standard negotiation points.

Mortgage rates shift weekly, and your approval window closes if you delay. Lock your rate once you’ve chosen your lender and confirmed your term length and amortization. Visit Financial Canadian’s mortgage resources to explore tools that help you understand mortgages Canada explained in clear, actionable terms.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment