Payday loans carry steep costs that can trap you in a cycle of debt if you’re not careful. At Financial Canadian, we’ve seen firsthand how borrowers overpay by thousands of dollars simply because they don’t know what to look for.

The good news is that Canada payday loan tips exist to help you minimize these costs. Whether you’re considering a payday loan or already committed to one, this guide shows you exactly how to pay less and explore smarter alternatives.

What Makes Payday Loans So Expensive in Canada

Payday loans in Canada operate on a simple but punishing premise: you borrow money today and repay it in full when your next paycheck arrives, typically within two to four weeks. The lender provides cash immediately, often without a credit check, which sounds convenient until you see the cost. As of January 1, 2025, Canada capped payday loan costs at $14 per $100 borrowed, which translates to roughly 14% APR. However, this cap only applies to regulated lenders in provinces with strict rules. Many borrowers still face higher rates when annualized, making payday loans the most expensive debt available in Canada by a significant margin.

To put this in perspective, credit cards typically charge between 19.99% and 25.99% APR, while auto loans average around 8.24%. The math is brutal: borrowing $500 for two weeks costs you $70 in fees alone. If you roll over that loan because you cannot repay it, the costs multiply rapidly.

How costs compound with rollovers

The real danger emerges when you cannot repay on time. Most borrowers roll their payday loans forward, paying another fee to extend the repayment date. The average payday borrower renews their loan multiple times annually, transforming a short-term emergency loan into a long-term debt trap. If you borrow $500 and roll it over five times, you pay $350 in fees on top of the original $500, nearly doubling your cost.

Provincial regulations create different cost levels

Provincial regulations vary significantly, so you should check your province’s specific rules and caps before borrowing. Some provinces like British Columbia and Ontario have stricter limits, while others remain less regulated. These differences mean that the same $500 loan costs you different amounts depending on where you live. Understanding your local rules helps you identify the cheapest option available to you.

When payday loans become a trap

Payday loans should only serve as a last resort for genuine emergencies, not as a regular financial tool. The moment you roll over a loan, you enter a cycle that becomes increasingly difficult to escape. The fees accumulate faster than you can pay down the principal, and each renewal pushes you further into debt. This pattern explains why so many borrowers find themselves trapped for months or years.

Before you commit to a payday loan, you should explore alternatives that cost significantly less and offer more flexible repayment terms.

How to Pay Less on a Payday Loan

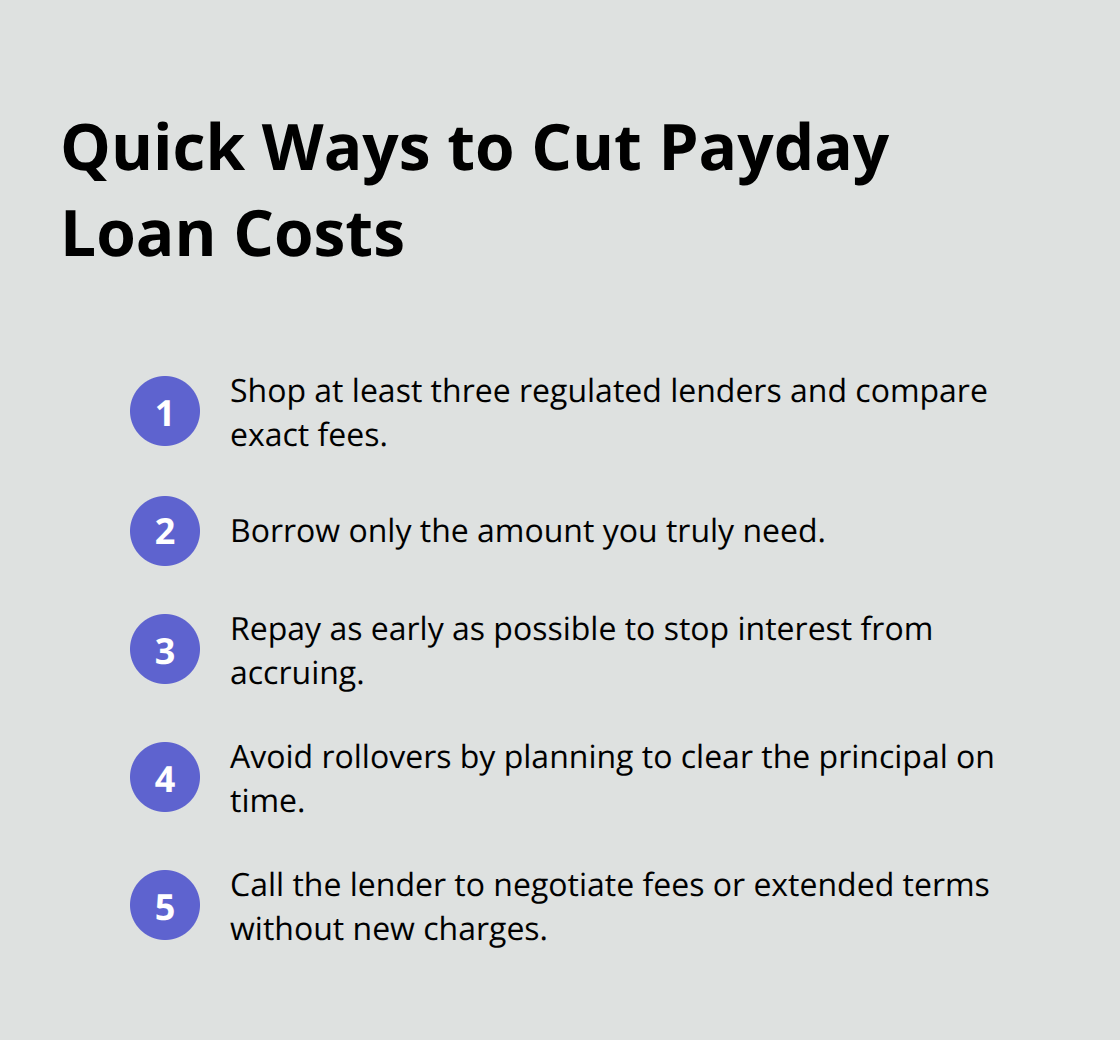

Payday loan rates vary between lenders, and most borrowers accept whatever terms a lender offers without questioning whether a better rate exists. This passivity costs you real money. The difference between a 14% fee and a 16% fee on a $500 two-week loan equals an extra $20 in costs. Over multiple rollovers, this gap widens significantly. Contact at least three regulated lenders in your province and compare their exact fees, not just the advertised APR. Some lenders offer slightly lower rates to borrowers with stable income or existing accounts, so mention your employment status during the application process-this occasionally yields better terms. Provincial regulators publish lists of licensed payday lenders, making this research straightforward and free. Once you identify the cheapest option, lock in that rate before accepting any loan.

Borrow only what you actually need

Most people borrow more than they actually need because payday lenders encourage larger amounts to generate higher fees. If you need $300 for rent but the lender suggests $500, resist the temptation. Every extra dollar borrowed costs you additional fees and extends your repayment burden. Calculate your exact shortfall before applying, then request only that amount. This discipline directly reduces your total cost and makes repayment more achievable on your next paycheck.

Repay early to cut total costs

If you can repay within seven days instead of fourteen, do it immediately. Some lenders offer reduced fees for early repayment, though you should verify this before borrowing. Even without a fee reduction, paying early stops interest from accruing on the remaining balance, saving you money over time.

The average daily balance formula multiplied by your interest rate multiplied by the number of days active, divided by 365, equals your total finance charge. Shorter loan terms and lower balances directly shrink this number.

Escape the rollover trap

The single most effective strategy is avoiding rollovers entirely, which requires planning beyond your immediate paycheck. If your paycheck covers the loan repayment plus your essential expenses, commit to paying it back on time without extension. If it does not, the payday loan was a mistake from the start, and you should have explored alternatives instead.

For borrowers already trapped in rollovers, the only exit strategy is attacking the principal aggressively. Allocate every dollar above your minimum expenses toward paying down the loan balance rather than renewing it. This approach feels painful short-term but breaks the cycle within weeks instead of months. Some borrowers negotiate directly with lenders to reduce fees or extend repayment without additional charges, particularly if they have a history of on-time payments with that lender. A brief phone call explaining your situation occasionally produces more flexibility than you expect, especially if you demonstrate intent to repay rather than abandon the debt.

When payday loans fail, alternatives offer relief

If you cannot repay your payday loan on time despite these strategies, you have entered dangerous territory. This is precisely when most borrowers roll over their loans and sink deeper into debt. However, other options exist that cost significantly less and provide more breathing room. Credit unions, personal loans from banks, and even credit card cash advances (while not ideal) typically offer lower rates and longer repayment terms than payday lenders. The key is recognizing when a payday loan has become the wrong tool and switching to a better solution before rollovers multiply your costs.

Better Alternatives That Actually Cost Less

Credit card cash advances and personal loans from banks sound less convenient than payday loans because they require more time and paperwork, but this friction saves you thousands of dollars over months. A credit card cash advance costs about $5 plus roughly 23% APR, compared to payday loans at 442% APR when annualized. On a $500 advance, you pay $5 upfront plus interest that compounds daily with no grace period, but even this punishing rate beats payday lenders by a massive margin. Personal loans from banks typically range from 8% to 35% APR depending on your credit score and income, with repayment terms stretching from three to sixty months. This flexibility transforms a two-week crisis into a manageable monthly payment that fits your actual budget. The catch is timing: bank loans take three to five business days to fund, which disqualifies them for true emergencies happening on Friday afternoon. However, if you have any advance warning about your financial shortfall, a bank loan is objectively superior to a payday loan in every measurable way.

Credit Unions Approve Bad Credit Faster

Credit unions deserve special attention because they approve borrowers with bad credit far more readily than traditional banks, and their rates consistently undercut payday lenders. Credit unions typically charge 18% to 35% APR for personal loans under $5,000, and many offer rates closer to 15% if you maintain an account with them for several months. The Credit Counselling Society reports that credit union members experience significantly faster approval processes and more willingness to work with borrowers facing temporary hardship. If you lack a credit union account, opening one takes less than an hour and qualifies you for better rates on future borrowing.

Lines of Credit Eliminate the Rollover Trap

Lines of credit from credit unions function like flexible payday alternatives: you access only the funds you need, pay interest solely on borrowed amounts, and avoid the pressure to borrow more than necessary. A line of credit at 18% APR costs you roughly $90 on a $500 two-week advance, compared to $70 in fees on a payday loan-only $20 more, but with zero rollover trap and actual repayment flexibility. This structure protects you from the compounding costs that make payday loans so dangerous.

Cash Advance Apps for Small Emergencies

For small emergencies under $750, cash advance apps like Bree offer interest-free access with no credit check and no hidden fees, making them the cheapest option available if you qualify. These apps fund within hours and eliminate the need to borrow from traditional lenders entirely. The trade-off is the borrowing limit, which works perfectly for genuine emergencies but falls short for larger financial gaps.

Choose Your Alternative Based on Timeline and Amount

The decision between these alternatives hinges on your timeline and borrowing needs. Cash advance apps work for same-day needs under $750, credit unions handle amounts up to $5,000 with slightly longer approval, and bank personal loans cover larger sums when you have several days to wait. Each option costs substantially less than a payday loan and offers repayment terms that match your actual financial capacity rather than forcing you into a two-week crisis cycle.

Final Thoughts

Payday loans in Canada serve one purpose: bridging a genuine financial emergency when no other option exists. If you have a true crisis happening today and need cash within hours, a payday loan from a regulated lender beats the alternatives. However, this scenario applies to far fewer borrowers than actually use payday loans. Most people borrow because they lack an emergency fund or have fallen behind on bills, situations that payday loans worsen rather than solve.

The Canada payday loan tips throughout this guide boil down to a single principle: minimize costs by borrowing less, repaying faster, and switching to cheaper alternatives whenever possible. Shopping between lenders saves you money on individual loans. Borrowing only what you need cuts your total fees. Repaying early stops interest from compounding. The real savings come from avoiding payday loans entirely by building financial resilience beforehand.

Better financial habits prevent the desperation that makes payday loans seem necessary. Start by tracking your spending for one month to identify where your money actually goes, then redirect those savings into a small emergency fund (even $25 weekly adds up to $650 within six months). If you already carry payday loan debt, attack it aggressively by negotiating with your lender, exploring credit union alternatives, or consolidating into a personal loan with a lower rate. We at Financial Canadian believe smart borrowing starts with understanding your options and choosing the path that costs you the least money-visit our resource center to connect with tools designed for Canadian borrowers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment