Carrying multiple debts drains your finances and your peace of mind. At Financial Canadian, we’ve seen how the right debt consolidation Canada tips can transform a chaotic payment schedule into one manageable monthly bill.

This guide walks you through proven strategies to save money, avoid costly mistakes, and pick the consolidation method that actually fits your situation.

What Debt Consolidation Actually Does

Debt consolidation combines multiple debts into a single monthly payment, usually at a lower interest rate. You take out one new loan to pay off all your existing debts, then repay that single loan over time. In Canada, this works through consolidation loans, mortgage refinancing, or debt management programs with non-profit agencies. The real benefit isn’t just simplicity-it’s the interest savings. If you carry credit card balances at 19% to 21% interest alongside a personal loan at 8%, consolidating into a single loan at 6% to 8% reduces what you actually owe. According to Equifax Canada data, the average Canadian carries around $21,131 in non-mortgage debt, so consolidating that amount even one percentage point lower saves hundreds annually. The catch is discipline: consolidation only works if you stop accumulating new debt. Many Canadians make the mistake of paying off credit cards through consolidation, then running those cards back up, ending up with more total debt than before.

Three Main Consolidation Methods

If you own a home with equity, mortgage refinancing becomes an option. You borrow against your home’s value to pay off unsecured debts like credit cards and personal loans. The downside is serious: you convert unsecured debt into secured debt backed by your house. If you cannot pay, you risk losing your home.

A debt consolidation loan from a bank or lender does not require home equity but typically demands a credit score above 650 for decent rates. Non-profit debt consolidation programs, offered through agencies like Credit Canada or Credit Counselling Canada, work differently. These agencies negotiate with your creditors to reduce interest rates and create a repayment plan without requiring a new loan. This option works even with lower credit scores.

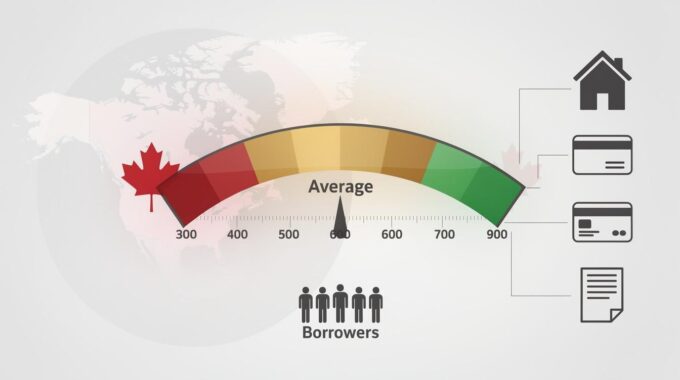

How Consolidation Affects Your Credit Score

Your credit score takes a temporary hit when you apply for consolidation because lenders perform hard inquiries, which lower your score by 5 to 10 points. However, consolidation can improve your score long-term if it reduces your overall debt and you maintain on-time payments.

The Financial Consumer Agency of Canada notes that credit scores in Canada range from 300 to 900, with 600 and above considered acceptable and 750 and above excellent.

After consolidation, focus on two critical actions: keep your credit utilization below 30% and make every payment on time. These two factors account for 50 of your credit score calculation and directly determine whether lenders offer you better rates in the future. Your next move involves understanding which consolidation method actually saves you the most money-and that requires comparing rates across lenders before you commit to anything.

Strategies to Maximize Savings When Consolidating Debt

Shopping for consolidation rates is non-negotiable if you want real savings. Most Canadians apply to one lender and accept whatever rate they’re offered, which is a costly mistake. Banks, credit unions, and online lenders price consolidation loans differently based on your credit score, income, and debt-to-income ratio. A rate difference of just 1% on a $20,000 consolidation loan over five years costs you roughly $1,000 extra in interest.

Compare Rates Across Multiple Lenders

Start by collecting rate quotes from at least three to five lenders without committing to any application yet. Hard inquiries from multiple lenders within 14 to 45 days typically count as a single inquiry on your credit report, so timing matters when you shop around. Compare not just the interest rate but also fees, prepayment penalties, and term length. Some lenders charge origination fees between 1% to 5% of the loan amount, which gets added to what you owe. Others offer no-fee consolidation but charge higher rates.

Calculate the total cost, not just the rate, because a lower advertised rate with steep fees often costs more overall than a higher rate with minimal fees.

Calculate Your Actual Savings Before Committing

Before signing anything, run the numbers on what consolidation actually saves you. Take your current debts and add up the total interest you’ll pay if you keep them separate and only make minimum payments. Most credit cards charge 19% to 21% annually, so a $5,000 balance paying minimums takes five to seven years to clear and costs $2,000 to $3,500 in interest alone. Now compare that to a consolidation loan at 7% to 9% over the same term. The gap between what you’re paying now and what you’ll pay after consolidation shows your real potential savings.

Use online debt calculators to model these scenarios rather than estimating in your head. The Financial Consumer Agency of Canada provides free debt payment calculators specifically for this purpose. One critical point: if your consolidation loan extends the repayment term beyond what you currently pay, the monthly payment drops but total interest paid can actually increase. A $15,000 debt at 8% over nine years instead of five years sounds easier monthly, but you’re paying thousands more in total interest. Run scenarios with different term lengths to find the sweet spot between manageable monthly payments and total interest cost.

Negotiate Better Terms with Creditors

Lenders expect negotiation, especially if you have decent credit. After collecting initial quotes, contact the lender offering the best rate and mention you have competing offers. Many lenders will match or beat a competitor’s rate to win your business, particularly if your credit score sits above 700. This works especially well with credit unions and smaller lenders who have more flexibility than major banks.

If your credit score is lower (around 600 to 650), negotiation becomes tougher, but non-profit credit counselling agencies like Credit Canada or Credit Counselling Canada can sometimes negotiate directly with creditors on your behalf to lower rates without requiring a new loan at all. That option often gets overlooked because people assume they need to take out a new loan to consolidate. These agencies negotiate interest rate reductions through debt management programs, which means you’re not borrowing more money-you’re just paying what you owe at better terms. This path avoids additional hard inquiries on your credit and keeps you from taking on more debt in the consolidation process itself. Understanding which mistakes derail consolidation plans helps you protect the savings you’ve worked to secure.

Common Mistakes to Avoid When Consolidating Debt

The moment you sign a consolidation agreement, your financial discipline faces a real test. Most Canadians sabotage their own consolidation plans within months by making one of three predictable errors.

Taking on New Debt While Consolidating

The first mistake is accumulating new debt while consolidating. You pay off credit cards through consolidation, then immediately start using those cards again. Equifax Canada data shows the average Canadian carries $22,147 in non-mortgage debt, and many of those people consolidated that exact amount before accumulating fresh balances. Running up your cards after consolidation means you now pay two sets of debt simultaneously: the consolidated loan plus the new credit card balances. This defeats the entire purpose of consolidation and leaves you worse off than before.

The solution is brutal honesty: freeze your credit cards or cut them up before consolidating. Do not apply for new credit for at least six months after consolidation closes. If you cannot trust yourself to stop using credit, consolidation alone will not fix your finances.

Choosing the Wrong Consolidation Method

The second mistake is selecting the wrong consolidation method for your specific situation. Mortgage refinancing looks attractive because rates are lower, but converting unsecured credit card debt into a mortgage means your home secures that debt. If you hit financial trouble, the lender can foreclose. For homeowners with unstable income or minimal emergency savings, this is reckless.

Non-profit debt consolidation programs through agencies like Credit Canada or Credit Counselling Canada work better for these situations because they negotiate with creditors without requiring you to take on new debt or risk your home. These programs often work even with lower credit scores, making them accessible when traditional consolidation loans are not.

Ignoring the Total Cost of Your Consolidation Loan

The third mistake is ignoring the total cost of your consolidation loan. Too many people focus only on the monthly payment and miss that extending your repayment term from five years to nine years adds thousands in interest charges. A $20,000 debt consolidated at 8% over five years costs roughly $4,400 in interest total, but stretched to nine years, that same debt costs $6,900 in interest. The monthly payment drops from about $405 to $250, but you pay $2,500 more overall.

Always calculate total interest cost across different term lengths before committing. The Financial Consumer Agency of Canada provides free debt payment calculators specifically for this purpose. Model these scenarios accurately rather than relying on what lenders suggest, because lenders naturally recommend longer terms that benefit them, not you.

Final Thoughts

Debt consolidation in Canada works only when you combine the right strategy with genuine discipline. The debt consolidation Canada tips throughout this guide boil down to three core actions: shop for rates across multiple lenders, calculate your total interest cost before committing, and stop accumulating new debt the moment you consolidate. Most Canadians fail at consolidation not because the strategy is flawed, but because they ignore one of these steps.

Your next move depends on your specific situation. If you own a home with equity and stable income, mortgage refinancing offers the lowest rates but carries real risk if your finances become unstable. If you lack home equity or prefer to keep your home separate from debt, a consolidation loan from a bank or credit union works well with a credit score above 650. If your credit score sits lower or you want to avoid taking on new debt entirely, contact a non-profit agency like Credit Canada or Credit Counselling Canada for a free consultation about debt management programs.

Before you apply anywhere, pull your credit report and check for errors that might be inflating your interest rates (obtaining your report is free and checking it does not affect your score). Then collect rate quotes from at least three to five lenders and compare total costs, not just advertised rates. Run the numbers through a debt calculator to see exactly how much you save over time.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment