Americans can legally purchase property in Canada without citizenship or permanent residency. The process involves specific tax obligations, documentation requirements, and financial considerations that differ significantly from domestic purchases.

At Financial Canadian, we’ve analyzed the key steps for how to buy property in Canada as an American. Foreign buyer taxes range from 15% to 25% depending on the province, while non-resident mortgage requirements typically demand 35% down payments.

What Legal Requirements Must Americans Meet?

Citizenship Status Won’t Block Your Purchase

Americans face no citizenship barriers when they purchase Canadian property. The Canadian government allows foreign nationals to buy real estate without permanent residency or citizenship status. This differs from countries like New Zealand or Singapore that restrict foreign ownership entirely. However, property ownership provides zero immigration benefits and creates no pathway to Canadian citizenship or permanent residency.

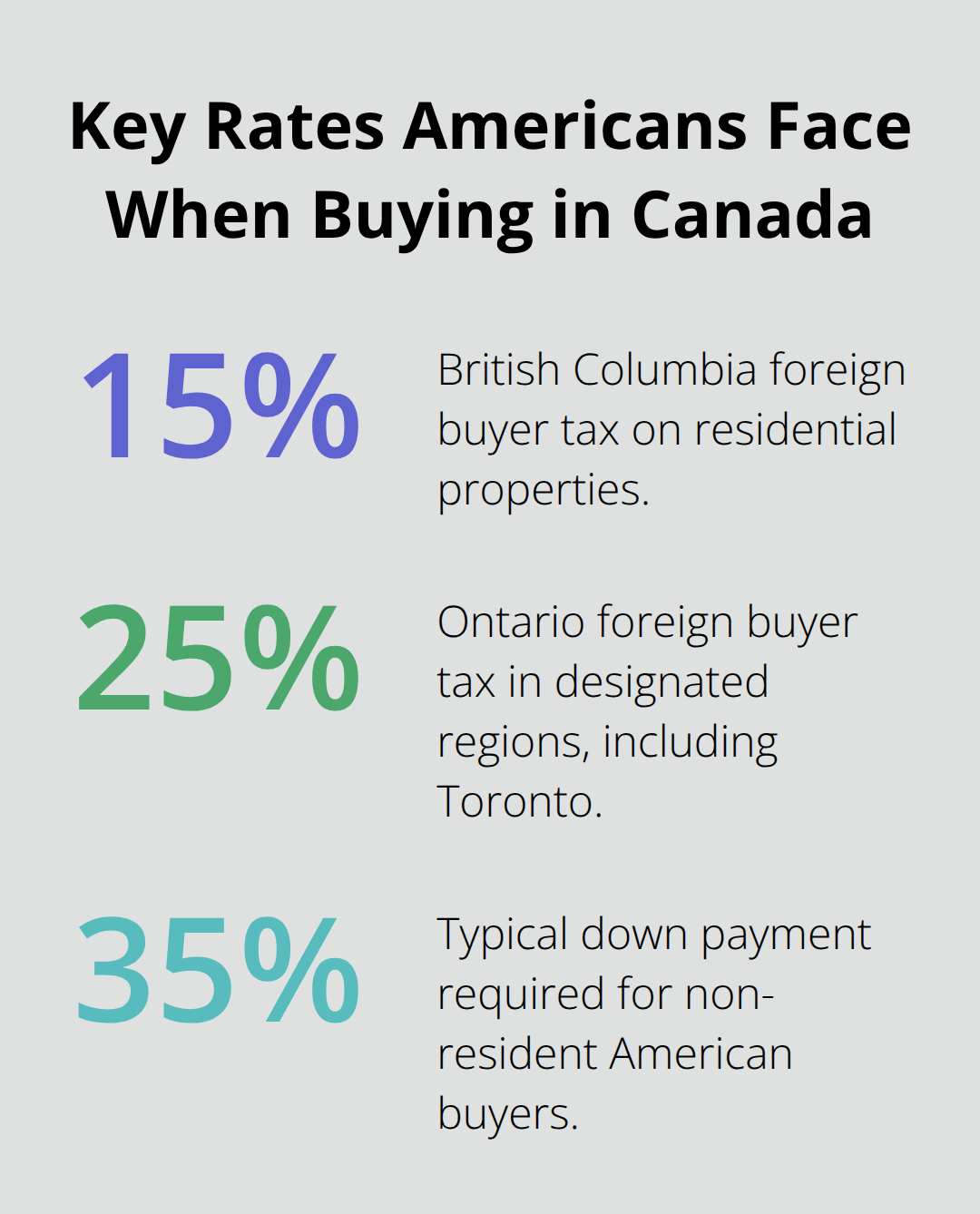

Provincial Foreign Buyer Taxes Hit Hard

Foreign buyer taxes represent the largest legal hurdle for American purchasers. British Columbia imposes a 15% foreign buyer tax on residential properties, while Ontario charges 25% in designated regions (including Toronto). These taxes apply to the total purchase price, not just the down payment.

Alberta eliminated its foreign buyer tax in 2024, which makes it more attractive for American investors. Prince Edward Island restricts foreign ownership to properties under five acres, while other provinces maintain minimal restrictions.

Documentation Requirements Are Extensive

Americans must provide specific documentation that Canadian residents don’t need. The Canada Revenue Agency requires non-residents to obtain an Individual Tax Number before they complete any property transaction. Banks demand two years of US tax returns, proof of employment, and verification of funds for the down payment. Property lawyers typically charge $2,500 to $4,000 for foreign buyer transactions due to additional compliance requirements. Americans must also demonstrate the source of their down payment funds through bank statements that span at least 90 days. Some provinces require additional provincial tax registrations before they close the transaction.

Federal Ban Creates New Restrictions

The Canadian government implemented the Prohibition on the Purchase of Residential Property by Non-Canadians Act, which prevents non-Canadians from purchasing residential property in Canada for 2 years. This federal ban affects properties in urban areas with populations over 10,000 residents. Americans can still purchase vacation homes, cottages, or properties outside these urban areas. The ban also allows purchases when Americans buy with a Canadian partner (spouse or common-law partner).

These legal requirements directly impact your financial planning and mortgage options, which vary significantly from standard Canadian resident purchases.

What Financial Hurdles Will You Face?

Down Payment Demands Are Steep

Non-resident Americans must provide significantly larger down payments than Canadian residents. Most Canadian banks require 35% down payments for foreign buyers, compared to the 5% minimum that Canadian residents pay on properties under $500,000. TD Bank and BMO typically demand 35% down payments for Americans, while some credit unions accept 20% when you demonstrate strong US credit history and income stability.

A $800,000 Toronto condo requires $280,000 upfront rather than the $40,000 a Canadian resident would pay. The Bank of Canada reports that average home prices reached $716,828 in 2024, which makes these down payment requirements a substantial financial barrier for most American buyers.

Major Banks Accept American Buyers

Several Canadian financial institutions actively work with American purchasers. TD Bank offers cross-border mortgage programs specifically for US citizens, while RBC provides dedicated US client services through their American offices. BMO operates branches in major US cities (Chicago and New York) to serve American clients who buy Canadian property.

Credit unions often provide more flexibility than major banks, with some that accept 20% down payments instead of the standard 35%. Mortgage approval typically takes 2-10 days in Canada compared to 45-60 days in the US, but Americans face higher interest rates. Current rates for non-residents range from 6.60% to 7.25%, approximately 0.5% higher than resident rates.

Currency Exchange Costs Add Up

Americans lose substantial money through currency conversion fees and exchange rate fluctuations. Traditional banks charge 2-4% in foreign exchange fees, which costs $16,000-$32,000 on an $800,000 property purchase. Currency specialists like Wise offer mid-market exchange rates with fees under 1%, which potentially saves thousands compared to bank transfers.

You should open a Canadian bank account before your purchase to establish local credit history and reduce transfer fees. The Canadian dollar typically fluctuates 5-15% annually against the US dollar, so the time when you convert your currency can impact your total purchase cost significantly.

These financial requirements create ongoing tax obligations that extend far beyond your initial purchase, which affects both your Canadian and American tax filings.

What Tax Burden Will You Face Long-Term?

Canadian Property Taxes Vary Dramatically

Property tax rates across Canada range from 0.5% to 2.5% annually based on assessed property values, with significant provincial differences that impact your long-term costs. Vancouver homeowners pay approximately 0.25% of assessed value, while Halifax residents face rates near 1.3%. Toronto property owners typically pay 0.6% to 0.7% of assessed value annually.

A $800,000 Toronto property generates roughly $5,200 in annual property taxes, while the same value property in Vancouver costs only $2,000 yearly. Municipal assessments occur every one to four years (location dependent), and reassessments can increase your tax bill substantially when property values rise. Americans must pay these taxes regardless of residency status, and late payments incur penalties of 1.25% monthly in most provinces.

US Tax Obligations Create Complex Requirements

The Internal Revenue Service requires Americans to report foreign property ownership through Form 8938 when total foreign assets exceed $50,000 for single filers or $100,000 for married couples. Rental income from Canadian properties must appear on Schedule E, while capital gains from property sales face US taxation at rates up to 20%.

Americans can claim foreign tax credits for Canadian taxes paid, but this requires detailed record maintenance and professional tax preparation. Professional tax preparation for cross-border property ownership typically costs $1,500 to $3,000 annually due to the complexity of dual-country reports.

Annual Maintenance Costs Add Up Fast

Property insurance costs typically range from $1,200 to $3,000 annually for standard coverage, while maintenance expenses average 1% to 3% of property value yearly. Winter heat costs in cities like Toronto average $150 to $300 monthly, significantly higher than most US regions.

Americans who rent their Canadian properties must withhold 25% of gross rental income for Canadian taxes, though proper tax filings can reduce this amount. These costs compound over time and require careful budget planning beyond your initial purchase price.

Final Thoughts

Americans who master how to buy property in Canada as an American face substantial financial commitments that extend well beyond the initial purchase price. The 35% down payment requirement, foreign buyer taxes up to 25%, and complex documentation processes create significant barriers that demand thorough preparation. Your total investment includes currency exchange costs, annual property taxes from 0.5% to 2.5%, maintenance expenses, and dual-country tax obligations.

The federal ban on foreign property purchases in urban areas restricts your options until 2027, but opportunities exist in smaller communities and vacation property markets. Professional guidance from Canadian real estate lawyers, tax specialists, and mortgage brokers becomes essential for cross-border transactions. Americans must maintain detailed financial records for both Canadian and US tax authorities while budgeting for higher interest rates and stricter lending requirements.

At Financial Canadian, we help businesses establish strong online presences when they make major financial decisions. Our comprehensive web design service creates SEO-optimized, responsive websites that drive growth and enhance customer engagement. Digital resources play a vital role in today’s competitive marketplace (especially for financial services companies).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment