Student debt weighs heavily on millions of Canadians, with the average graduate owing $28,000 according to Statistics Canada. Many borrowers wonder: is there student loan forgiveness in Canada?

The answer isn’t straightforward. While Canada doesn’t offer blanket loan forgiveness like some countries, several targeted programs exist for specific professions and circumstances.

We at Financial Canadian will break down every available option, from federal programs to provincial initiatives, helping you understand what relief might be within reach.

Current Student Loan Forgiveness Programs in Canada

Federal Programs Target Healthcare Workers

The Government of Canada operates the most substantial forgiveness program specifically for family doctors and nurses who work in underserved communities. Family doctors can qualify for loan forgiveness for 5 years if they have a Canada Student Loan balance at the end of each year of service in an eligible community, while nurses and nurse practitioners qualify for up to $30,000 over the same period.

The government expanded eligibility in November 2024 to include communities with populations of 30,000 or less, which significantly broadened access. These amounts increased by 50% in November 2023, making the program more attractive for healthcare professionals who consider rural practice.

Provincial Programs Focus on In-Demand Occupations

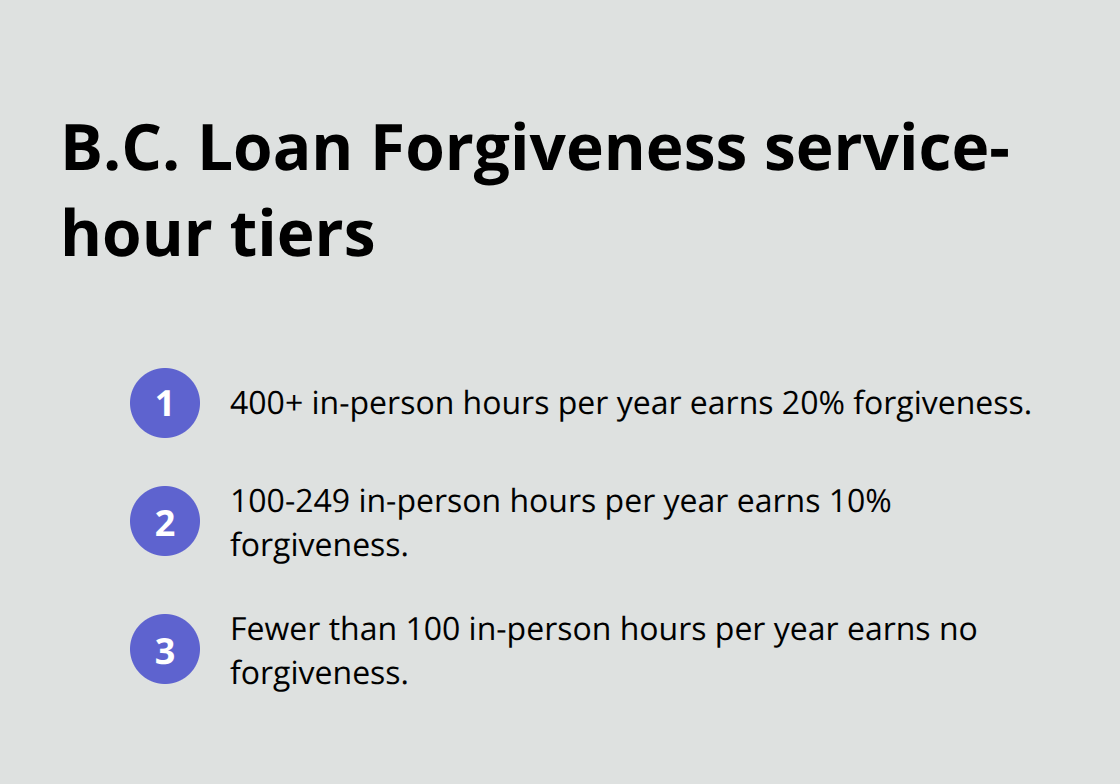

British Columbia runs the most comprehensive provincial forgiveness program, which targets graduates in healthcare and therapy roles. The B.C. Loan Forgiveness Program forgives up to 20% of student loans yearly for up to 5 years for those working in specific roles at public facilities in underserved communities.

Eligible occupations include medical laboratory technology, speech-language pathology, and various therapy specializations. Recipients must complete minimum in-person service hours annually: 400+ hours earns the full 20% forgiveness, 100-249 hours receives only 10%, and fewer than 100 hours receives nothing.

The program specifically targets workforce shortages in communities like Fort St. John, Prince Rupert, and 100 Mile House (areas that struggle to attract qualified professionals).

Long-Term Forgiveness Through Repayment Assistance

Students who enroll in the federal Repayment Assistance Plan can potentially qualify for complete loan forgiveness after ten years of participation. This timeline-based forgiveness represents the only path for non-healthcare professionals to achieve full debt elimination through government programs.

The RAP program reduced maximum payments from 20% to 10% of household income and introduced zero payment thresholds for low-income borrowers. These changes make long-term forgiveness more accessible than previous versions allowed.

Understanding these programs helps determine your eligibility, but qualification requirements vary significantly across different forgiveness options.

Who Qualifies for Student Loan Forgiveness

Healthcare Professionals Face Strict Geographic Limits

Family doctors and nurses working in communities with populations of 30,000 or less qualify for the federal forgiveness program. The government sets no income ceiling for these professionals, which means high-earning doctors in underserved areas can still receive up to $60,000 in debt relief over a period of 5 years. The program prioritizes service commitment over financial need.

Statistics Canada data reveals that only 18% of Canadian communities meet the population threshold. This restriction concentrates opportunities in rural and remote regions, effectively excluding major urban centers like Toronto, Vancouver, and Calgary (despite these cities facing healthcare shortages in specific neighborhoods). The November 2024 expansion broadened access but maintained the fundamental geographic barrier.

Employment Conditions Demand Full Commitment

The federal program requires continuous employment in eligible communities throughout the five-year service period. Healthcare professionals must submit annual verification of service hours and loan balances to maintain benefits. Those who leave their positions forfeit all future forgiveness benefits, which eliminates career flexibility during the commitment period.

British Columbia’s provincial program adds therapy professionals like speech-language pathologists and medical laboratory technologists to eligible occupations. However, recipients must work at publicly funded facilities and complete minimum 400 in-person service hours annually for full benefits. This requirement excludes part-time workers and those in administrative roles from maximum debt relief.

Income Thresholds Apply to Long-Term Forgiveness

The Repayment Assistance Plan offers forgiveness options for non-healthcare professionals through program participation. You can apply for repayment assistance as soon as you start to repay your student loans and anytime while in repayment, though you must re-apply every 6 months. The government reduced maximum payments from 20% to 10% of household income and introduced zero payment thresholds for low-income borrowers. Single borrowers with family income below $25,000 qualify for zero payments, while families of four qualify with income below $40,000.

These income requirements create accessibility challenges for middle-income graduates who earn too much for zero payments but struggle with standard repayment amounts. The program helps those most in need while leaving moderate earners with limited relief options beyond standard repayment assistance.

Beyond traditional forgiveness programs, several alternative debt management strategies can provide substantial relief for borrowers who don’t qualify for complete loan elimination.

Alternatives to Student Loan Forgiveness

Repayment Assistance Plans Reduce Monthly Payments

The Repayment Assistance Plan represents the most accessible debt relief program for Canadian graduates who don’t qualify for professional forgiveness programs. The government eliminated interest accumulation on all Canada Student Loans in April 2023, which means RAP participants see their loan balances decrease with every payment rather than fight compound interest. Single borrowers who earn under $25,000 annually qualify for zero monthly payments, while families of four with household income below $40,000 face no payment obligations. The program caps payments at 10% of family income, down from the previous 20% threshold that trapped many middle-income graduates in unaffordable payment cycles.

Interest Relief Provides Immediate Financial Relief

Students who face temporary financial hardship can apply for interest relief periods that pause both payments and interest accumulation for up to six months at a time. Medical and parental leave extends this relief up to 18 consecutive months without interest charges, which provides substantial savings during life transitions. The National Student Loans Service Centre processes these applications within 30 days, and borrowers can reapply multiple times throughout their repayment period. This option works particularly well for recent graduates who navigate job market uncertainty or those who experience income disruption from career changes.

Bankruptcy Offers Last Resort Debt Elimination

Student loans become dischargeable in bankruptcy seven years after you stop being a student, though a hardship provision reduces this to five years if you can prove good faith use of loan funds for educational expenses. One-third of graduates repay their loans within three years according to government data, but those who struggle with multiple debt sources often benefit from consumer proposals that can include student loans after seven years from study completion. Licensed insolvency trustees report that graduates with combined government and private student debt (averaging $56,000) frequently choose consumer proposals over bankruptcy to preserve credit ratings while they achieve debt reduction.

Payment Deferrals Bridge Financial Gaps

The National Student Loans Service Centre allows borrowers to defer payments for up to six months when they face temporary financial difficulties. This option differs from interest relief because interest continues to accumulate during deferral periods, but it prevents loans from going into default status. Borrowers must demonstrate financial hardship through income documentation, and the service centre typically approves deferrals within two weeks of application submission. This strategy works best for graduates who expect income recovery within the deferral period rather than those facing long-term financial challenges.

Final Thoughts

Student loan forgiveness in Canada exists but targets specific professions and circumstances. Healthcare workers in underserved communities access the most generous federal programs, with family doctors who receive up to $60,000 and nurses who receive up to $30,000 over five years. Provincial programs like British Columbia’s initiative expand options for therapy professionals, though geographic restrictions limit access to rural areas.

The question “is there student loan forgiveness in Canada” has no simple answer for most graduates. Only 18% of Canadian communities qualify for federal healthcare forgiveness programs, and long-term RAP forgiveness requires ten years of participation (which many borrowers find impractical). Most borrowers benefit more from repayment assistance plans, interest relief, or payment deferrals than complete debt elimination.

We at Financial Canadian recommend that you start with RAP applications for immediate payment reduction, then explore professional forgiveness if you work in eligible healthcare roles. Consider bankruptcy only after seven years from study completion when other options prove insufficient. For comprehensive financial planning resources and expert guidance on student debt management, visit Financial Canadian to access our financial education tools and services.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment