At Financial Canadian, we understand that traditional mortgages aren’t always the best fit for everyone. That’s why we’re exploring creative ways to finance a home in today’s market.

From rent-to-own agreements to crowdfunding platforms, innovative solutions are emerging to help more people achieve homeownership. In this post, we’ll dive into these alternatives and government programs that can make your dream of owning a home a reality.

Why Traditional Mortgages Fall Short

The Rigid Nature of Conventional Mortgages

Traditional mortgages often fail to meet the needs of many potential homebuyers. These loans typically require a substantial down payment, often 20% of the home’s value. This requirement creates a significant barrier to homeownership for many Canadians. Canada’s national average home price increased to $678,331 in March 2025, marking a 1.5% increase from February 2025’s $668,097. This means a typical down payment could exceed $135,000 – a sum out of reach for many potential buyers.

Furthermore, these mortgages have strict credit score requirements. Lenders usually look for scores of 680 or higher to offer the best rates. This criterion excludes many Canadians who may have lower scores due to various life circumstances.

Income Verification Challenges

Traditional lenders also demand extensive income verification. This process creates problems for self-employed individuals, freelancers, or those with irregular income streams. The Canadian Federation of Independent Business reports that about 2.9 million Canadians are self-employed (representing a significant portion of the workforce). These individuals may struggle with conventional mortgage approval processes.

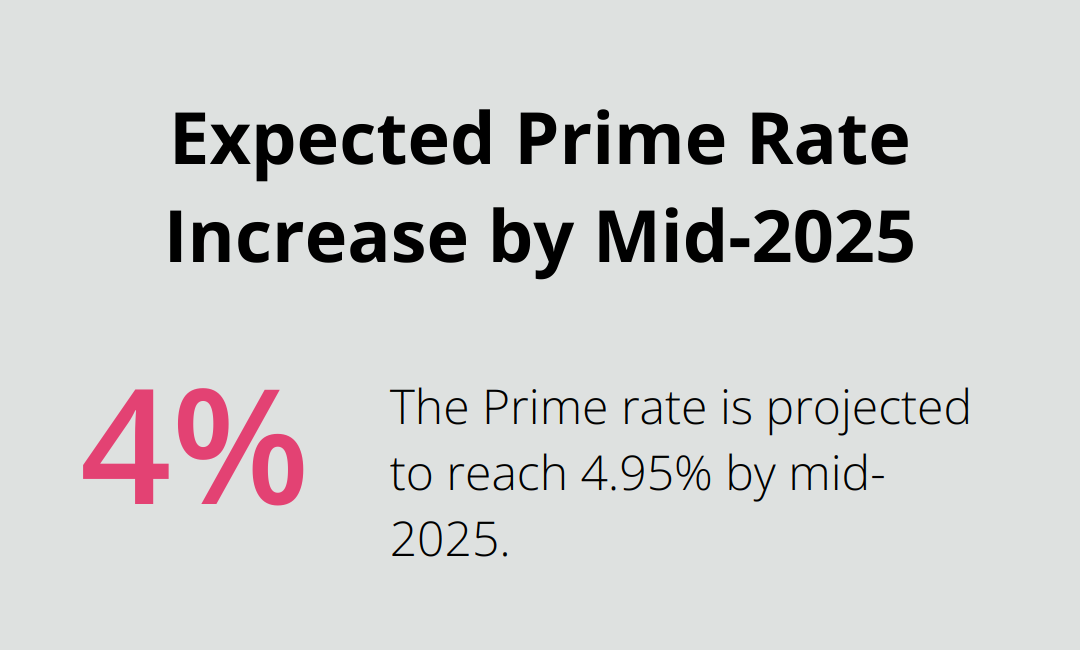

The Impact of Rising Interest Rates

As of May 2025, interest rates for conventional mortgages have been rising. The Prime rate is expected to reach 4.95% by the middle of 2025. This increase from the historic lows of recent years has made monthly payments significantly higher, pricing many potential buyers out of the market.

The Appeal of Creative Financing

Creative financing options offer more flexibility. For instance, rent-to-own agreements allow buyers to move into a home immediately while building equity over time. This option can be particularly appealing in hot real estate markets where prices rise quickly.

Seller financing has also become more common. It allows buyers to work directly with property owners, often resulting in more flexible terms and lower closing costs.

Crowdfunding platforms for real estate have emerged as an innovative solution. These platforms allow individuals to invest in properties collectively, making homeownership more accessible to a broader range of people.

These creative options often come with lower credit score requirements and more flexible income verification processes. This flexibility opens doors for many Canadians who might otherwise find themselves shut out of the housing market.

While traditional mortgages still have their place, the landscape of home financing continues to evolve. The next section will explore these innovative financing solutions in more detail, providing a comprehensive look at the alternatives available to Canadian homebuyers.

Innovative Financing Options for Homebuyers

In today’s challenging housing market, creative financing solutions have become more popular. These alternatives to traditional mortgages offer more flexibility and accessibility for many potential homeowners. Let’s explore some of these innovative options that could help you achieve your homeownership goals.

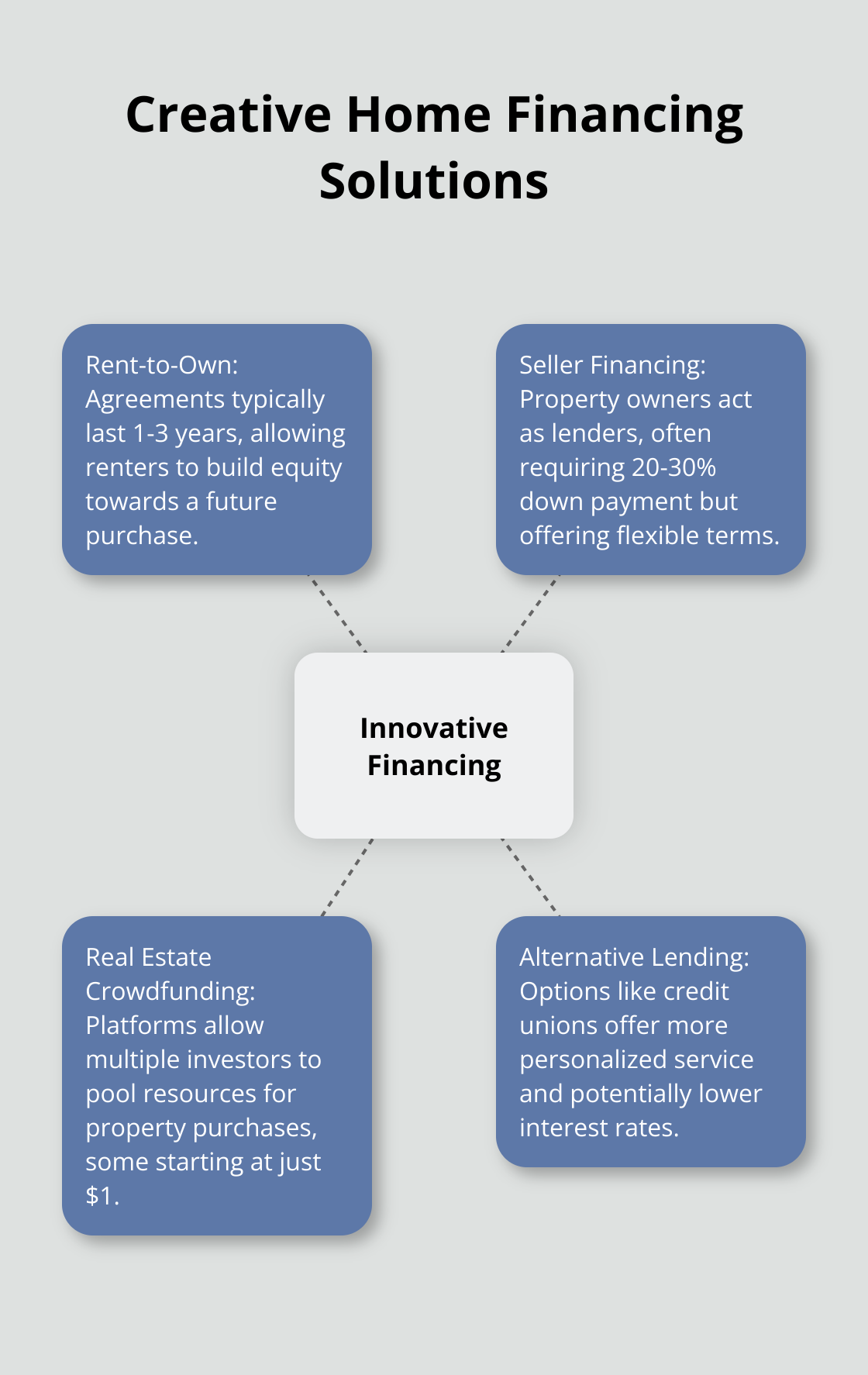

Rent-to-Own Agreements: A Path to Ownership

Rental agreements between a landlord and tenant are commonly referred to as a “lease”. In Canada, there are two types of rental agreements. These agreements allow you to rent a property with the option to buy it later. A portion of your monthly rent goes towards your future down payment, helping you build equity while you live in the home.

The Canada Mortgage and Housing Corporation (CMHC) states that rent-to-own agreements typically last 1-3 years. During this time, you can improve your credit score and save additional funds for a down payment. However, you must carefully review the terms of these agreements, as they can vary significantly between properties and sellers.

Seller Financing: Cutting Out the Middleman

Seller financing (or owner financing) involves the property owner acting as the lender. This option can benefit you if you struggle to qualify for a traditional mortgage due to credit issues or self-employment income.

The Canadian Real Estate Association reports that seller financing often comes with more flexible terms and potentially lower interest rates than bank mortgages. However, sellers typically require a larger down payment (often 20-30% of the purchase price) to mitigate their risk.

Real Estate Crowdfunding: Collective Homeownership

Real estate crowdfunding platforms have emerged as an innovative way to invest in property. These platforms allow multiple investors to pool their resources to purchase properties. While this method is more commonly used for investment properties, some platforms now focus on helping individuals become homeowners.

For example, some Canadian platforms allow individuals to invest in real estate for as little as $1. While this might not directly lead to homeownership, it can be a stepping stone to building the capital needed for a down payment on a traditional mortgage.

Alternative Lending Options

Alternative financing options in Canada include diverse options such as flexible loans and mortgages. These options often have more flexible lending criteria and can particularly help those with non-traditional income or credit challenges.

Credit unions, being member-owned financial cooperatives, often offer more personalized service and potentially lower interest rates. The Canadian Credit Union Association reports that credit unions hold about 7% of the residential mortgage market in Canada, showing their growing popularity as mortgage lenders.

As we move forward, it’s important to consider the role of government programs and incentives in making homeownership more accessible. These programs can complement or enhance the innovative financing options we’ve discussed, providing additional pathways to homeownership for Canadians.

Government Support for Homebuyers

The Canadian government offers several programs to support homebuyers, especially first-time buyers. These initiatives aim to make homeownership more accessible and affordable. Let’s explore some of the key programs available:

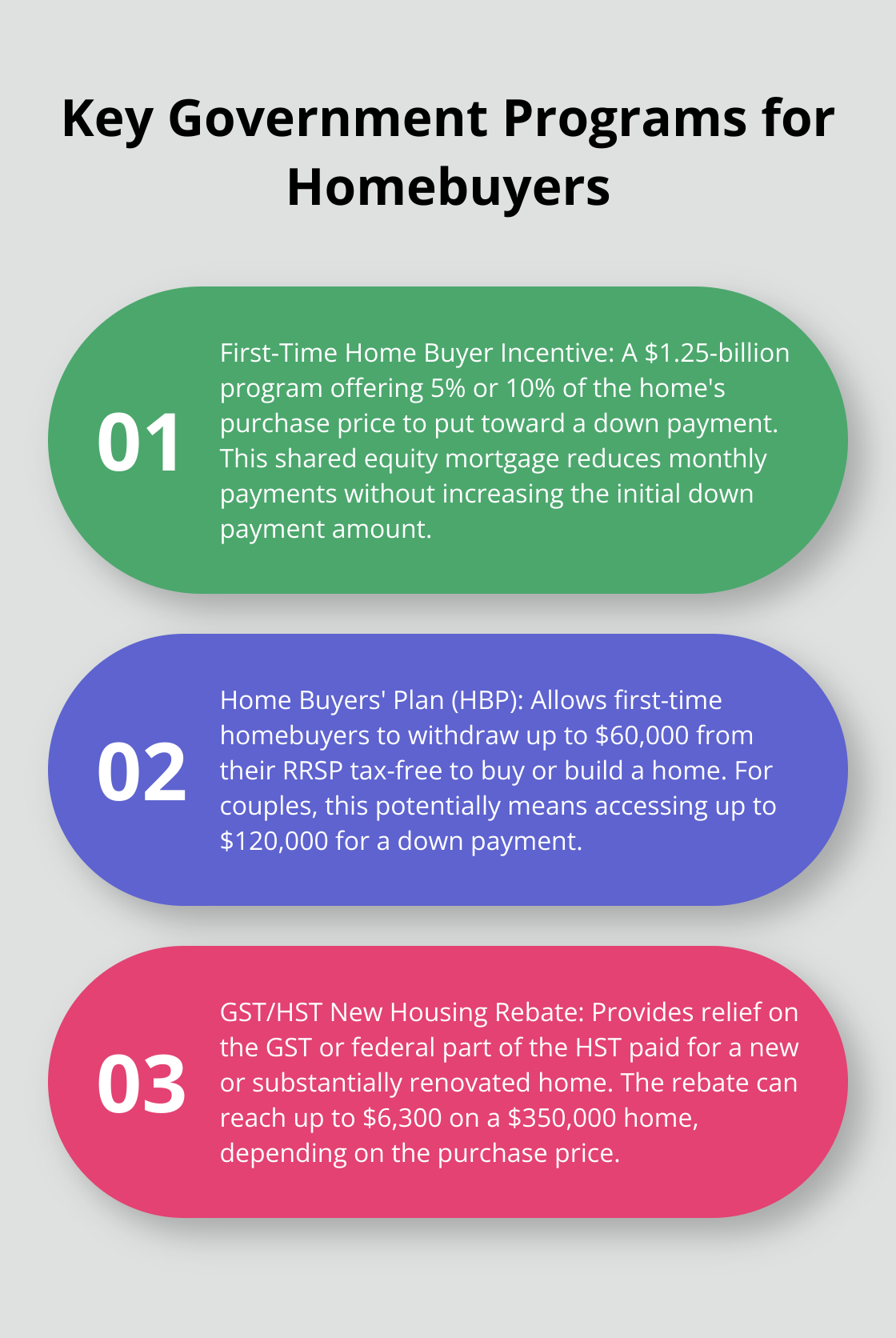

First-Time Home Buyer Incentive

The First-Time Home Buyer Incentive is a $1.25-billion program aimed at making homeownership more affordable by offering 5% or 10% of the home’s purchase price to put toward a down payment. This shared equity mortgage reduces monthly payments without increasing the down payment amount.

To qualify, you must be a first-time homebuyer with a household income under $120,000 and a minimum down payment of 5%. The mortgage and incentive amount cannot exceed four times your qualifying income. This program can significantly reduce monthly mortgage payments, making homeownership more affordable for many Canadians.

Home Buyers’ Plan (HBP)

The Home Buyers’ Plan allows first-time homebuyers to withdraw up to $60,000 from their Registered Retirement Savings Plan (RRSP) tax-free to buy or build a home. This limit applies to withdrawals made after April 16, 2024. For couples, this means potentially accessing up to $120,000 for a down payment.

You must repay the withdrawn amount within 15 years, starting the second year after the withdrawal. This program offers a valuable opportunity to boost your down payment without incurring additional debt or interest charges.

GST/HST New Housing Rebate

The GST/HST New Housing Rebate provides relief on the GST or federal part of the HST paid for a new or substantially renovated home. The rebate can reach up to $6,300 on a $350,000 home (depending on the purchase price). This program applies to both new builds and substantial renovations.

To claim this rebate, you must intend to use the property as your primary place of residence. You must submit the rebate application within two years of the closing date or, for new builds, within two years of construction completion.

Energy-Efficient Home Incentives

The Canadian government offers various incentives for energy-efficient homes. These programs aim to reduce energy consumption and lower homeowners’ utility bills. For example, the Canada Greener Homes Grant provides up to $5,000 for energy-efficient retrofits to your home.

To qualify, you must complete a pre- and post-retrofit EnerGuide evaluation. Eligible upgrades include insulation, air-sealing, windows and doors, thermostats, and heating equipment. This program not only helps reduce your carbon footprint but also can lead to significant savings on your energy bills.

These government programs offer substantial financial support for homebuyers. Each program has specific eligibility criteria and limitations. We recommend you consult with a mortgage professional or financial advisor to determine which programs best suit your situation and how to effectively leverage them in your home-buying journey.

Final Thoughts

Home financing has evolved beyond traditional mortgages, offering creative ways to finance a home. Rent-to-own agreements, seller financing, and real estate crowdfunding platforms provide opportunities for many Canadians who might struggle to enter the housing market. Government programs like the First-Time Home Buyer Incentive and Home Buyers’ Plan also play a significant role in supporting homebuyers.

We encourage you to explore these alternatives and find the solution that best fits your individual needs and financial situation. It’s essential to thoroughly research and understand each financing method before making a decision. Each option comes with its own set of benefits and potential risks.

At Financial Canadian, we’re committed to helping you navigate your financial journey. We specialize in web design services to boost your online presence. We also believe in empowering our clients with valuable information to make informed decisions in all aspects of their lives, including homeownership.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment