At Financial Canadian, we understand the challenges of securing a personal loan with a 600 credit score. Many borrowers in this situation often feel discouraged, but there are still options available.

In this guide, we’ll explore how to get a personal loan with a 600 credit score and provide practical steps to improve your chances of approval. We’ll also discuss various lenders and strategies that can help you secure the funds you need, even with fair credit.

What a 600 Credit Score Means for Your Loan Prospects

Understanding Your Credit Score

A 600 credit score places you in the “fair” credit category, which can present challenges when you apply for personal loans. This score results from a combination of positive and negative credit behaviors.

Your 600 credit score numerically represents your creditworthiness. Lenders calculate it using data from your credit reports, which track your borrowing and repayment history. The FICO scoring model (widely used by lenders) ranges from 300 to 850. With a score of 600, you fall just below the threshold for “good” credit, which typically starts at 670.

This score indicates you’ve experienced some difficulties managing credit in the past. You might have missed a few payments or carry high credit card balances. These factors can make lenders cautious, as they view you as a higher-risk borrower compared to those with scores above 670.

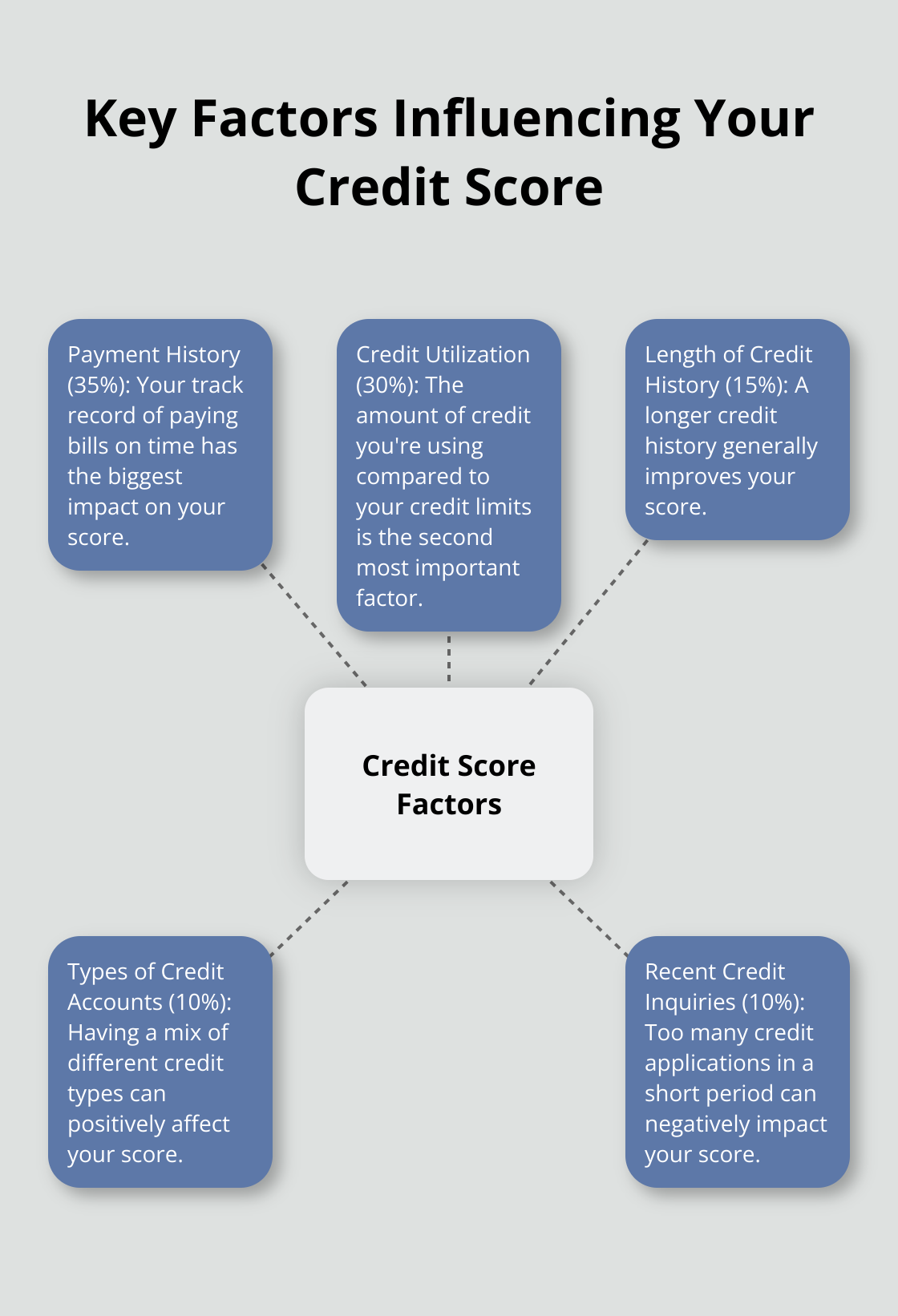

Key Factors Influencing Your Score

Several elements contribute to your credit score:

- Payment History (35% of FICO score): Late payments, even by a few days, can significantly impact your score.

- Credit Utilization (30%): This refers to how much of your available credit you use. High balances on credit cards can lower your score, even if you make payments on time.

- Length of Credit History (15%): A longer credit history generally improves your score.

- Types of Credit Accounts (10%): A mix of different credit types (e.g., credit cards, installment loans) can positively affect your score.

- Recent Credit Inquiries (10%): Too many credit applications in a short period can negatively impact your score.

How Lenders View a 600 Credit Score

When you apply for a personal loan with a 600 credit score, lenders consider you a moderate risk. This perception affects both your approval chances and the terms you receive.

Many traditional banks might hesitate to approve your application. However, online lenders and credit unions often have more flexible criteria. These institutions might work with you more readily, but you should expect higher interest rates and possibly lower loan amounts compared to borrowers with good or excellent credit.

Some lenders specialize in fair credit loans. These lenders understand that a 600 credit score doesn’t tell your whole financial story. They may consider other factors (such as your income and employment stability) when making lending decisions.

Improving Your Score for Better Loan Options

While a 600 credit score presents challenges, you can take steps to improve it:

- Pay all bills on time

- Reduce credit card balances

- Avoid applying for new credit unnecessarily

- Keep old credit accounts open (if they don’t have annual fees)

As you work on improving your credit score, you’ll open up more loan options with better terms. In the next section, we’ll explore specific personal loan options available to borrowers with a 600 credit score.

Where Can You Get a Personal Loan with a 600 Credit Score?

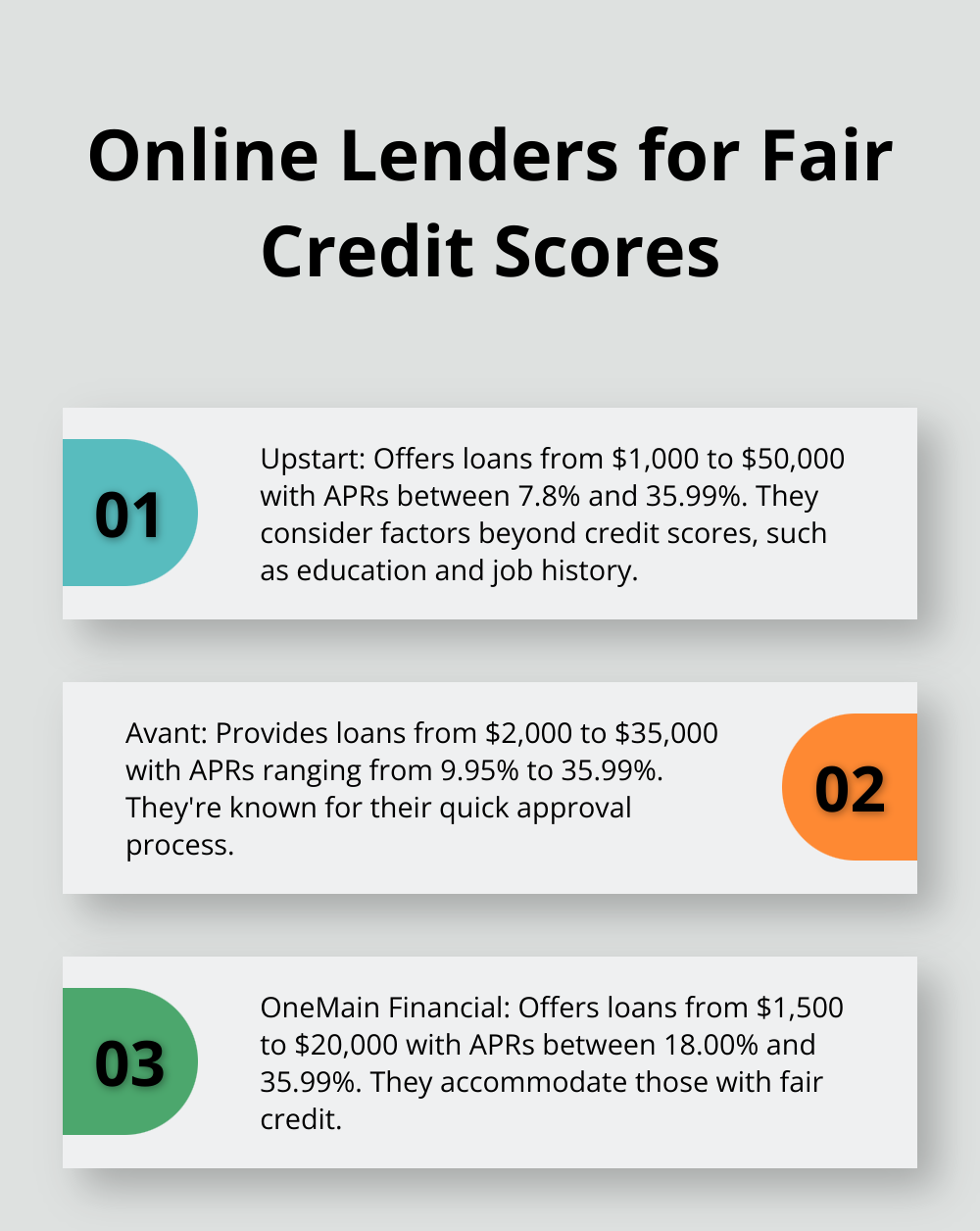

Online Lenders: Your Best Bet

Online lenders often have more flexible criteria than traditional banks. They use advanced algorithms to assess risk, which can work in your favor if you have a 600 credit score. Some online lenders to consider include those that accept applicants with credit scores below 670.

These lenders often provide pre-qualification, which allows you to check potential rates without affecting your credit score.

Credit Unions: A Community-Focused Alternative

Credit unions are non-profit organizations that often have more lenient lending criteria. They may offer lower interest rates and more personalized service. To borrow from a credit union, you typically need to become a member, which usually involves opening a savings account.

Some credit unions offer loans as low as $600. Before applying for a personal loan, it’s important to check your credit score.

Secured Personal Loans: Leveraging Your Assets

If you can’t get approved for an unsecured loan, consider a secured personal loan. These loans require collateral, such as a car or savings account, which reduces the lender’s risk. As a result, you may qualify for lower interest rates.

For example, if you own a car outright, you could use it as collateral for a secured personal loan. Be aware that if you default on the loan, you risk losing your collateral.

Peer-to-Peer Lending: Connecting with Individual Investors

Peer-to-peer (P2P) lending platforms connect borrowers directly with individual investors. These platforms often have more flexible criteria than traditional lenders. Popular P2P platforms include Prosper and LendingClub.

On these platforms, you create a loan listing explaining why you need the loan and how you plan to repay it. Investors then decide whether to fund your loan. This personal touch can work in your favor if you have a compelling reason for borrowing.

A 600 credit score presents challenges, but it doesn’t close all doors. You can find a personal loan that meets your needs by exploring these options and comparing offers. In the next section, we’ll discuss strategies to improve your chances of loan approval with a 600 credit score.

How to Boost Your Loan Approval Odds

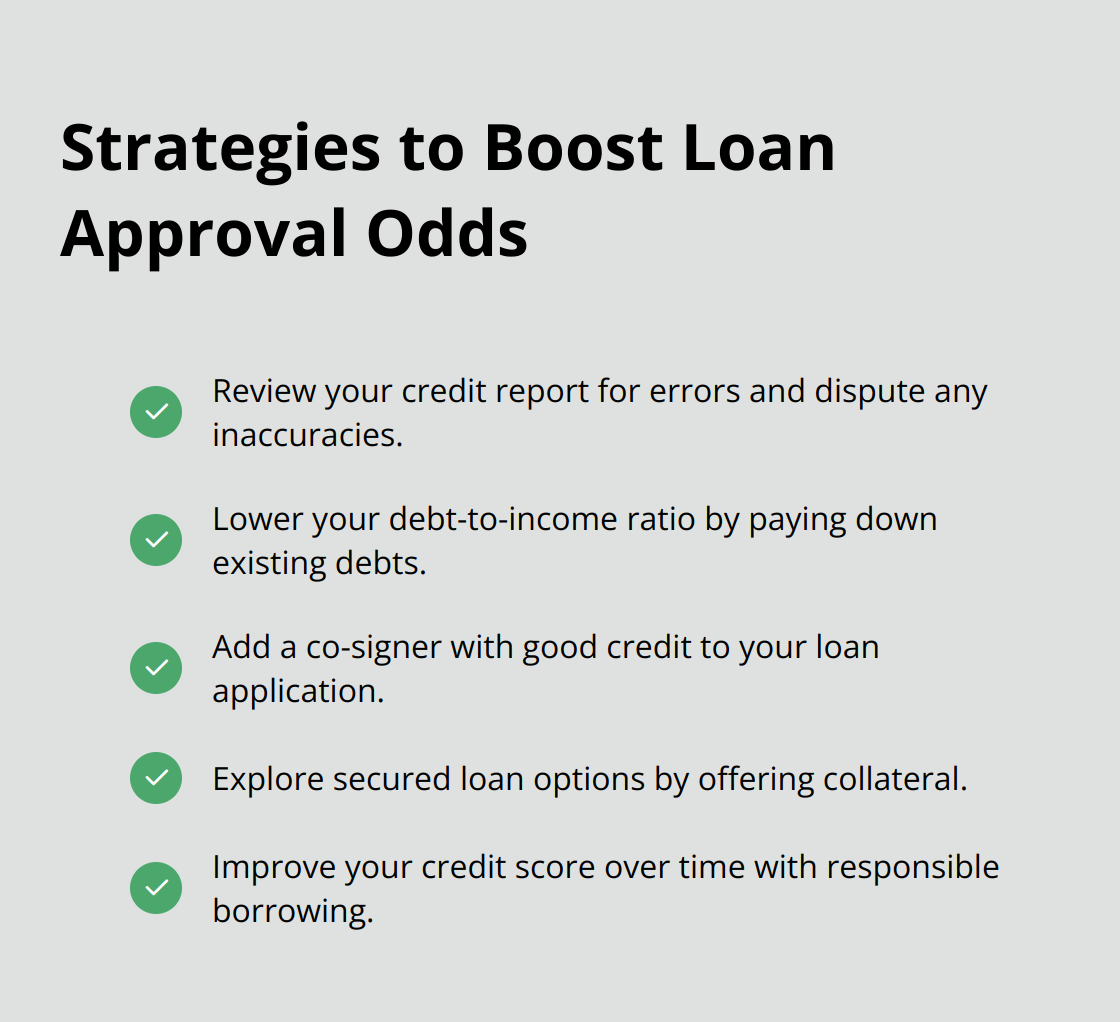

Review Your Credit Report for Errors

Start by obtaining a free copy of your credit report from Equifax and TransUnion. Check each entry for inaccuracies. The Federal Trade Commission reports that one in five consumers has an error on their credit report that could affect their credit scores.

If you find mistakes, dispute them with the credit bureaus immediately. This process takes up to 30 days, but removing errors can quickly boost your credit score. Even a small increase in your score can improve loan approval chances and interest rates.

Lower Your Debt-to-Income Ratio

Your debt-to-income ratio plays a significant role in qualifying for a loan. Lenders may not approve you if your ratio is beyond their maximum allowed. Try to keep your DTI below 43%, as this is often the highest ratio lenders accept for a qualified mortgage.

To lower your DTI:

- Pay down existing debts (focus on high-interest credit cards first)

- Increase your income through side gigs or asking for a raise at work

- Avoid new debt before applying for a personal loan

A lower DTI shows lenders you have more income available to make loan payments, which increases your approval chances.

Add a Co-signer to Your Application

If you struggle to get approved on your own, ask a trusted friend or family member with good credit to co-sign your loan. A co-signer with a strong credit profile can significantly improve your approval chances and help you secure better interest rates.

Understand the responsibilities involved. Your co-signer becomes equally responsible for the loan. If you miss payments, their credit score will also suffer. Make sure you can manage the loan payments comfortably before involving a co-signer.

Explore Secured Loan Options

If unsecured personal loans remain out of reach, consider secured loan options. Offering collateral reduces the lender’s risk, which can lead to easier approval and lower interest rates.

Common forms of collateral include:

- Savings accounts

- Certificates of deposit (CDs)

- Vehicles (if owned outright)

- Home equity (for homeowners)

Secured loans can be easier to obtain, but you risk losing your collateral if you default on the loan. Choose this option only if you’re confident in your ability to repay the loan.

Final Thoughts

Obtaining a personal loan with a 600 credit score presents challenges, but options exist. Online lenders, credit unions, and peer-to-peer platforms offer potential solutions for borrowers in this credit range. Responsible borrowing and timely repayments will improve your credit score over time, leading to better loan terms in the future.

Focus on paying bills promptly, reducing credit card balances, and avoiding unnecessary credit applications to enhance your creditworthiness. Regular reviews of your credit report (and disputing any inaccuracies) will help build a stronger credit profile. These steps take time, but the financial benefits make the effort worthwhile.

At Financial Canadian, we understand the importance of a strong online presence for businesses. Our web design services can create a visually stunning and functional website tailored to your needs. This approach will drive growth and establish a powerful online presence for your business, complementing your efforts to secure a 600 credit score personal loan.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment