Building credit in Canada can feel impossible when you have no credit history. Banks often reject applications for traditional credit cards, leaving many Canadians stuck in this frustrating cycle.

A secured credit card in Canada offers a proven solution. We at Financial Canadian will show you exactly how to get approved, choose the right card, and use it to build strong credit fast.

How Does a Secured Credit Card Actually Work

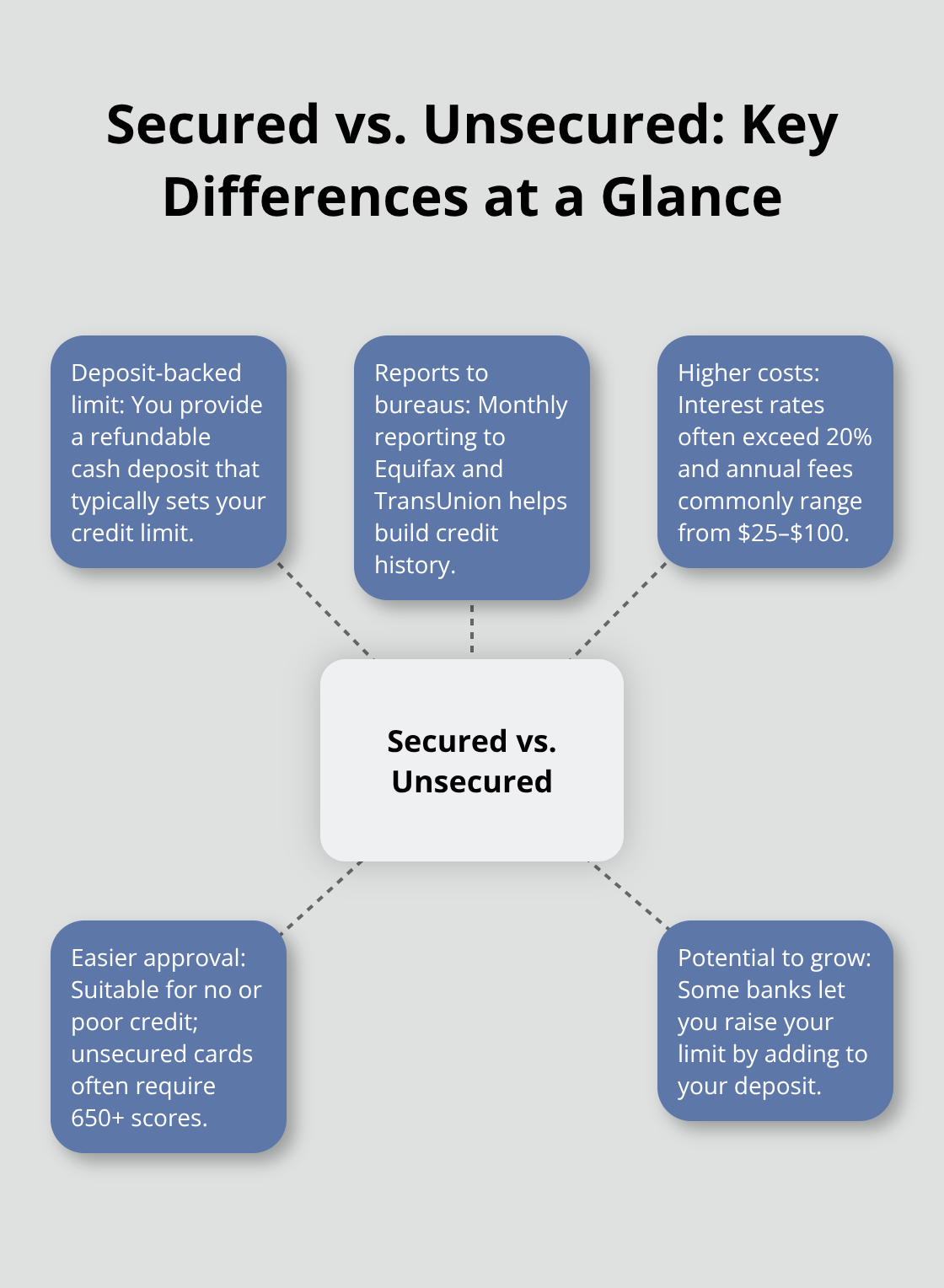

A secured credit card functions as a regular credit card with one major difference: you provide a cash deposit upfront that becomes your credit limit. Most Canadian banks require deposits between $200 and $1,000, with TD Canada Trust and RBC typically setting minimums at $500. This deposit stays in a separate account and earns no interest while you hold the card.

Your Deposit Sets Your Credit Limit

The security deposit amount directly determines your credit limit. Put down $500, get a $500 limit. Capital One’s Guaranteed Secured Mastercard allows deposits up to $10,000, which gives you flexibility to choose your spending power. Your deposit remains untouched unless you miss payments or close the account. Banks like BMO and Scotiabank will increase your credit limit if you add more money to your security deposit after approval.

Secured Cards Build Credit Through Bureau Reports

Unlike prepaid cards, secured credit cards report your payment history to Equifax and TransUnion every month. This monthly report makes secured cards powerful credit-building tools, not just spending alternatives. Most major Canadian banks report to both credit bureaus (always confirm this before you apply since some smaller lenders skip this step).

How Secured Cards Differ from Regular Credit Cards

Secured cards charge higher interest rates than unsecured cards, often exceeding 20% annually compared to 11-15% for prime credit cards. Annual fees range from $25 to $100, while many unsecured cards offer fee-free options. However, secured cards approve applicants with poor or no credit history, while unsecured cards require good credit scores above 650 for approval.

Now that you understand how secured cards work, let’s examine the best options available from Canadian banks and what features matter most for your situation.

Which Secured Credit Cards Should You Choose

Capital One’s Guaranteed Secured Mastercard stands out as the top choice for most Canadians who rebuild credit. This card accepts applicants with bankruptcies and consumer proposals, which makes it the most accessible option available. The annual fee sits at $59, while the interest rate reaches 22.9%. Capital One reports to both Equifax and TransUnion monthly and offers potential upgrades to unsecured cards after 12 months of responsible use. The minimum deposit starts at $75, with maximum limits that reach $10,000 for those who want higher credit limits.

Major Bank Options Lack Competitive Value

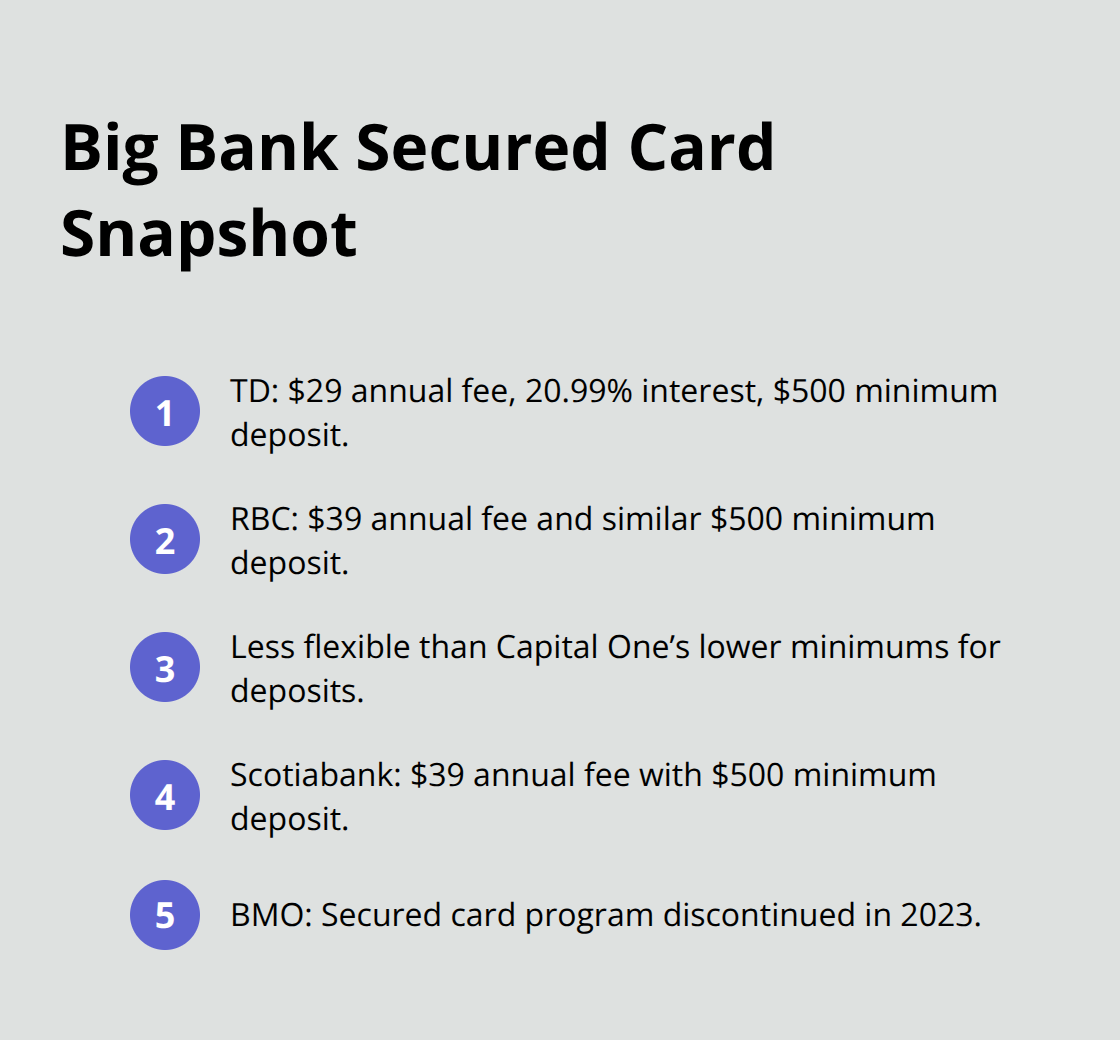

TD’s Secured Credit Card charges $29 annually with a 20.99% interest rate and requires minimum deposits of $500. RBC’s Secured Visa demands similar deposit amounts but adds a $39 annual fee. Both banks offer solid credit reports but lack the flexibility of Capital One’s lower minimum requirements. Scotiabank’s secured option requires $500 minimum deposits and charges $39 yearly, which makes it less attractive for budget-conscious applicants.

BMO discontinued their secured card program in 2023 (this left fewer big bank alternatives for consumers).

Neo Financial Provides Superior Rewards Structure

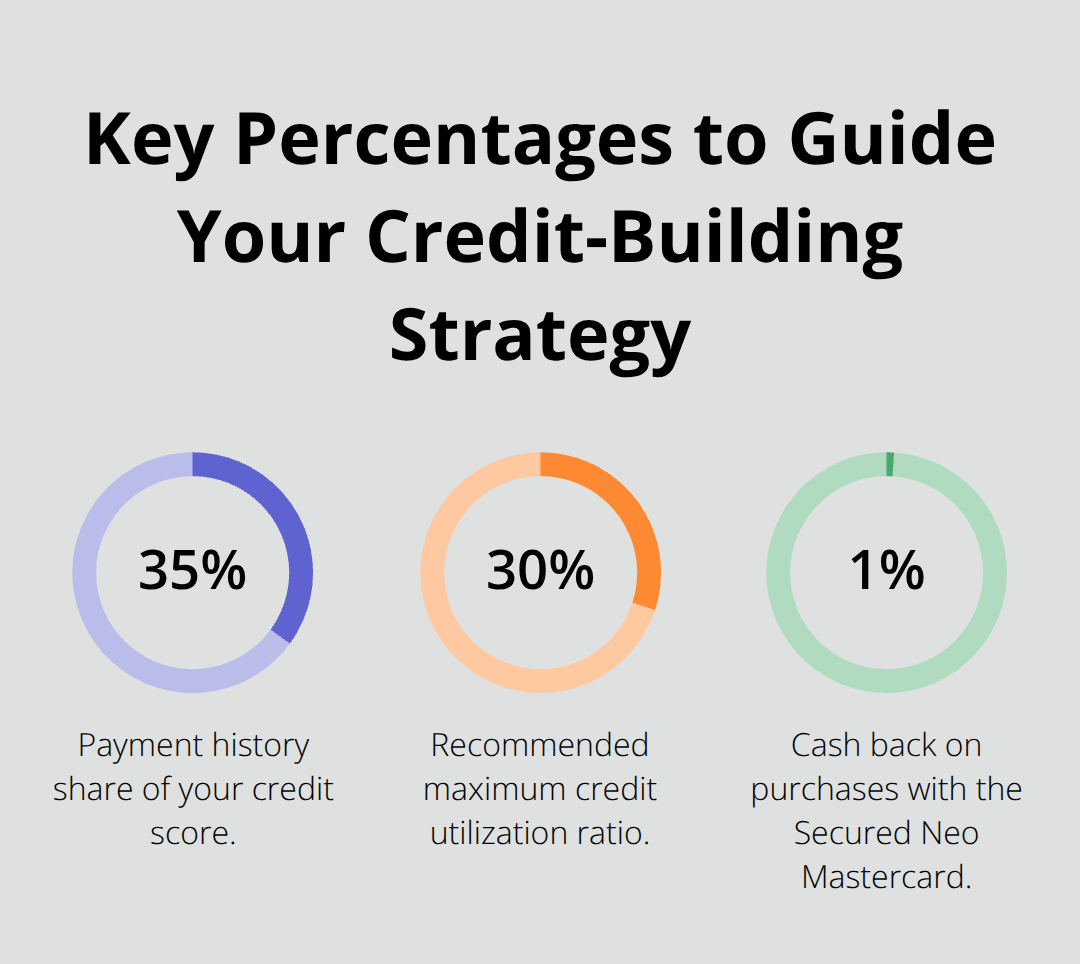

The Secured Neo Mastercard breaks the mold with 1% cash back on purchases while it builds credit. Neo charges no annual fee and requires refundable security funds and the Build membership ($7.99/month, with ways to get it for free) to get features to help strengthen your credit. The card reports to major credit bureaus and provides mobile app access for expense management. Interest rates match industry standards at 22.99%, but the rewards program sets it apart from traditional secured cards that offer no benefits beyond credit development.

Home Trust Offers Low-Interest Alternative

Home Trust Secured Visa provides an 11.25% interest rate that beats most competitors significantly. This card charges no annual fee and requires $500 minimum deposits. Home Trust reports to both major credit bureaus monthly and allows balance transfers from other cards. The lower interest rate saves money for cardholders who carry balances month to month (though we recommend you pay balances in full).

Once you identify the right secured card for your needs, you’ll want to understand the application process and requirements that banks expect from new cardholders.

How to Apply for Your Secured Credit Card

Banks approve secured credit card applications in 15-30 minutes when you prepare the right documents. Submit your application online during business hours Monday through Friday for the fastest processing times. You need valid government-issued photo identification, proof of Canadian address from the last 90 days, and employment verification or income documentation. Social Insurance Number verification is mandatory for all applications. Most banks accept recent pay stubs, tax returns, or employment letters as income proof. Bank statements from the past three months help demonstrate financial stability even with poor credit scores.

Choose Your Security Deposit Strategically

Consider your budget, spending habits and financial goals to help you choose the best security deposit amount. Lower amounts like $200 or $300 create restrictive credit limits that hurt your credit utilization ratio when you make regular purchases. Higher deposits above $1,000 tie up excess cash unnecessarily since credit score improvements plateau after consistent six-month payment histories regardless of credit limit size. Capital One allows you to increase deposits later, but TD and RBC require new applications for limit increases. Your deposit must come from Canadian bank accounts and cannot include cash, money orders, or international transfers.

Expect Instant Decisions and Quick Card Delivery

Major Canadian banks provide instant approval decisions for most secured credit card applications. Applications rejected instantly usually indicate insufficient income documentation or invalid identification rather than credit score issues. Approved applicants receive cards within 7-10 business days through regular mail. Expedited delivery costs $25-40 but reduces delivery time to 2-3 business days (though most people find standard delivery adequate). Your security deposit processes immediately upon approval through pre-authorized debit or online transfer. Account activation happens within 24 hours of receipt of your physical card.

Verify Credit Bureau Reports Before You Apply

Check your credit report with Equifax and TransUnion before you submit any application. Errors on your credit report can delay approval or result in higher security deposit requirements. Dispute any incorrect information at least 30 days before you apply for your secured card. This step takes minimal effort but can save you from unnecessary complications during the application process. Most Canadians can access one free credit report annually from each bureau (additional reports cost $15-25 each).

Final Thoughts

Secured credit cards in Canada provide the fastest path to credit improvement when traditional cards remain out of reach. Your payment history accounts for 35% of your credit score, which makes consistent monthly payments your most powerful tool for improvement. Most Canadians see credit score increases of 30-50 points within six months of responsible secured credit card Canada use.

Keep your credit utilization below 30% of your limit and pay balances in full each month to avoid interest charges. Set up automatic payments to prevent missed due dates, which can damage your credit progress. Monitor your credit report quarterly to track improvements and catch any errors early (this prevents future complications).

After 12-18 months of on-time payments, most banks offer upgrades to unsecured cards with better rates and rewards. Your security deposit returns when you close the account or upgrade, provided you maintain good standing. We at Financial Canadian help businesses establish strong digital foundations through our comprehensive web design service that creates visually stunning, responsive websites with SEO optimization.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment