Cashback credit cards turn everyday purchases into real money back in your pocket. The right card can put hundreds of dollars back into your budget each year.

We at Financial Canadian analyzed the best cashback credit cards in Canada to help you maximize your rewards. From grocery shopping to gas purchases, these cards offer serious earning potential for smart spenders.

Which Cards Deliver the Best Cashback Rewards

Tangerine Money-Back Credit Card Leads for Flexibility

The Tangerine Money-Back Credit Card stands out with its customizable 2% cashback on two categories you choose, plus 0.5% on everything else. You select from groceries, gas, restaurants, recurring payments, home improvement, furniture, hotels, and public transportation. This flexibility beats rigid category cards that force you into specific patterns that might not match your lifestyle.

The card charges no annual fee and requires no minimum income, which makes it accessible for most Canadians. Tangerine processes cashback monthly, so you see rewards faster than quarterly systems that competitors use.

Scotiabank Gold American Express Targets High Spenders

Scotiabank Gold American Express delivers 5 points on dining, food delivery, food subscriptions, and other eligible grocery stores, plus eligible entertainment purchases including movies and theatre. Gas purchases earn 2% with no cap. The $120 annual fee pays for itself when you spend $3,000 in bonus categories yearly.

This card works best for families who spend heavily on groceries and dine out frequently. American Express acceptance remains limited compared to Visa or Mastercard, particularly at Costco and some smaller retailers (which can limit your earning opportunities).

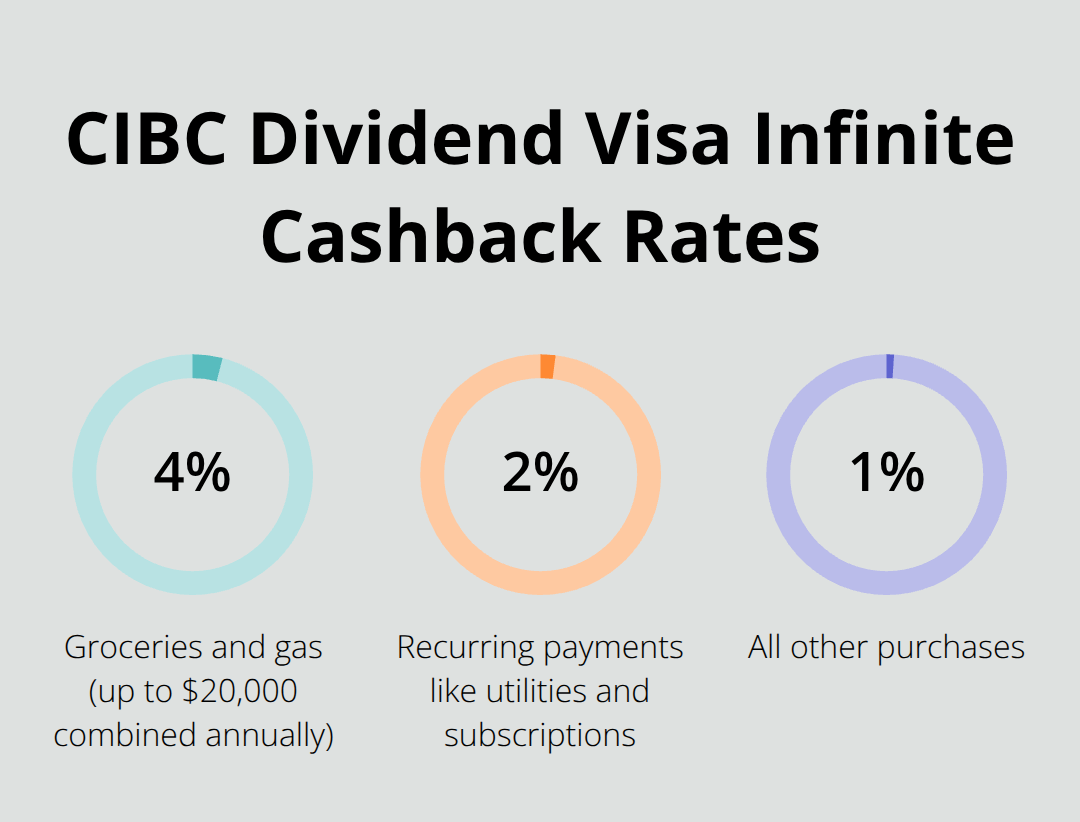

CIBC Dividend Visa Infinite Rewards Everyday Purchases

CIBC Dividend Visa Infinite offers 4% cashback on groceries and gas up to $20,000 combined annually, plus 2% on recurring payments like utilities and subscriptions. Other purchases earn 1%. The $99 annual fee breaks even at $2,475 in bonus category spending.

This card excels for households with consistent grocery and gas expenses but lower entertainment budgets. CIBC processes cashback annually, which delays gratification compared to monthly systems but simplifies tracking for tax purposes (since you receive one annual statement).

Neo World Elite Mastercard Maximizes Grocery Rewards

Neo World Elite Mastercard provides 1% cashback from gas and grocery, with rewards for everyday essentials and cashback offers at over 10,000 partners across Canada. The card requires a $80,000 household income but charges no annual fee. Neo caps grocery rewards at $250 monthly ($3,000 annually), which limits high-volume shoppers.

This card suits affluent households who want maximum grocery returns without annual fees. The income requirement excludes many Canadians, but qualified applicants get premium rewards rates that compete with fee-based cards.

Now that you understand the top cashback cards available, the next step involves choosing the right one for your specific spending habits and financial goals.

Which Cashback Card Fits Your Budget

Calculate Your Break-Even Point First

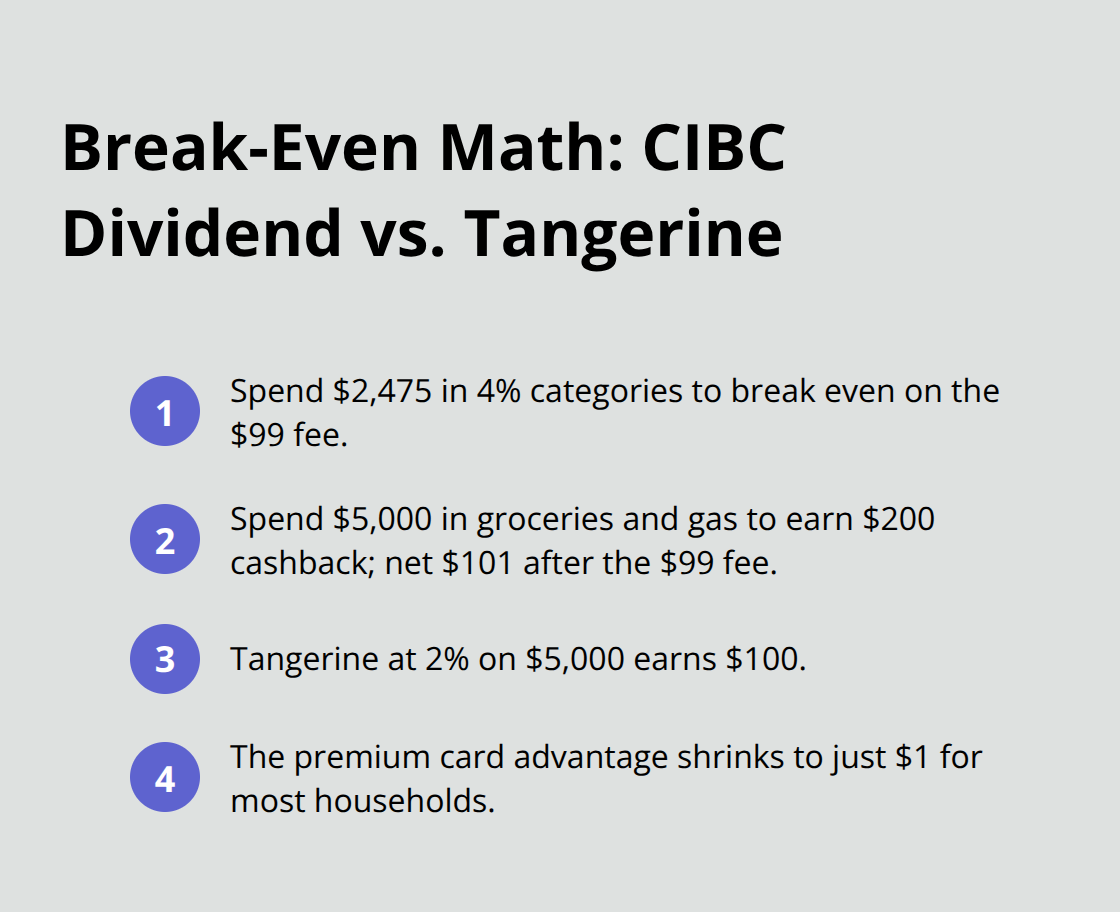

Annual fees only make sense when your rewards exceed the cost. The CIBC Dividend Visa Infinite charges $99 annually but offers 4% on groceries and gas. You need to spend $2,475 in these categories just to break even. Spend $5,000 annually on groceries and gas, and you earn $200 cashback minus the $99 fee, which nets $101. The no-fee Tangerine Money-Back Credit Card would earn $100 on that same amount with 2% rewards. The premium card advantage shrinks to just $1 for most households.

Higher-income families who spend $8,000+ annually on bonus categories see real value from fee-based cards. The Scotiabank Gold American Express becomes profitable at $2,400 in food and grocery expenses yearly, but its 5-point system complicates calculations compared to straight cashback percentages.

Match Cards to Your Actual Expenses

Track three months of expenses before you choose any card. Canadian grocery spending varies significantly by household, but your habits matter more than national averages. Heavy restaurant spenders benefit from cards that offer rewards on food purchases, while commuters need gas-focused benefits. The Neo World Elite Mastercard caps grocery rewards at $3,000 annually (which makes it useless for families who spend $6,000+ on food).

Category restrictions kill your potential faster than low rates. American Express acceptance problems cost you rewards at Costco and many small businesses. Choose Visa or Mastercard for maximum flexibility unless you never shop at restricted merchants.

Welcome Bonuses Boost First-Year Value

Sign-up offers can justify annual fees in year one, but sustainable rewards matter more long-term. The BMO CashBack Mastercard offers 5% cashback for three months on all purchases, potentially worth $300 if you time large expenses correctly. This temporary boost makes premium cards attractive initially, but base rates determine your value over time. Focus on cards where the permanent reward structure matches your expenses, then treat welcome bonuses as nice additions rather than decision drivers.

Once you identify cards that fit your budget and expenses, the next step involves strategic techniques to maximize every dollar you earn back.

How Do You Extract Maximum Value From Cashback Cards

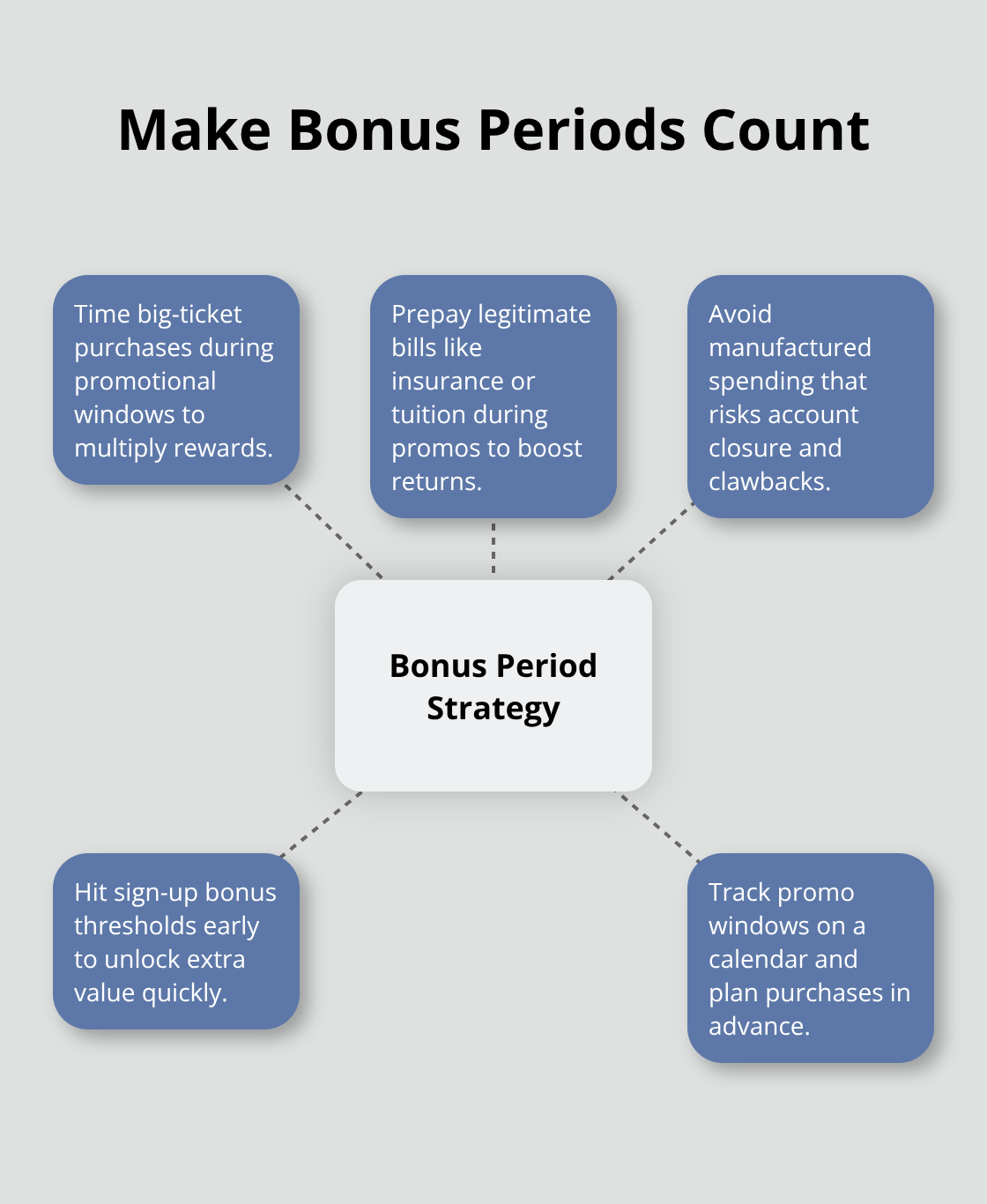

Time Large Purchases With Bonus Periods

Strategic timing transforms ordinary purchases into maximum rewards. The BMO CashBack Mastercard offers 5% cashback for three months on all purchases, which means a $6,000 home renovation generates $300 cashback instead of the standard $30. Plan major expenses like furniture, appliances, or car repairs during these promotional windows. The Scotiabank Gold American Express provides 10,000 bonus points after you spend $1,000 in the first three months (worth roughly $100 in statement credits).

Avoid manufactured spending schemes that violate card terms. Instead, prepay insurance premiums, property taxes, or tuition fees during bonus periods. These legitimate large expenses maximize your promotional rates without risking account closure.

Stack Cards Based on Category Strengths

Multi-card strategies multiply your earning potential when you execute them correctly. Use the CIBC Dividend Visa Infinite for groceries and gas at 4%, the Tangerine Money-Back Credit Card for restaurants and recurring payments at 2%, and the Neo World Elite Mastercard for its partner network bonuses. This combination captures optimal rates across all major spending categories.

Canadian households spend an average of $8,659 annually on food from stores according to the latest Statistics Canada data. Split this between grocery shopping on the CIBC card and dining out on the Tangerine card to maximize returns. The complexity increases your administrative burden, but organized spenders earn 30-40% more cashback than single-card users who accept suboptimal rates on major expense categories.

Monitor Category Caps and Rotation Schedules

Category limits destroy earning potential faster than low rates. The Neo World Elite Mastercard caps grocery rewards at $3,000 annually, which means heavy shoppers hit the limit by September and earn reduced rates for the remainder of the year. Switch to your backup card once you reach these thresholds to maintain optimal earning rates.

Some cards rotate bonus categories quarterly and require activation plus category tracking. The Discover it Cash Back offers 5% on rotating categories but requires manual activation each quarter. Miss the activation deadline and you forfeit bonus rates entirely. Set calendar reminders for rotation dates and activation requirements to avoid leaving money on the table through administrative oversights.

Track Your Spending Patterns Monthly

Monitor your expenses across all cards to identify optimization opportunities. Most card issuers provide detailed spending reports through their mobile apps (which break down purchases by category). Review these reports monthly to spot patterns where you might earn higher rewards with different cards.

Switch your primary card when your spending habits change seasonally. Holiday shopping periods often shift your expenses toward general purchases rather than specific categories, making flat-rate cards more valuable temporarily. Summer months might increase gas spending for road trips, making fuel-focused cards your best option during those periods.

Final Thoughts

The best cashback credit cards in Canada reward your specific expenses rather than offer generic benefits. Heavy grocery shoppers maximize value with the CIBC Dividend Visa Infinite at 4% on food purchases, while flexible spenders prefer the Tangerine Money-Back Credit Card’s customizable 2% categories. High-income households benefit from the Neo World Elite Mastercard’s premium grocery rates, and restaurant enthusiasts should consider the Scotiabank Gold American Express for rewards on food purchases.

Your annual expenses determine whether fee-based cards justify their costs. Calculate break-even points before you commit to premium options that charge $99-120 annually. Track your expenses for three months to identify your dominant categories, then select cards that align with these patterns (which maximizes your cashback potential).

Multi-card strategies work best for organized spenders who can manage category caps and rotation schedules effectively. Single-card users should prioritize flexibility over maximum rates to avoid administrative complexity. We at Financial Canadian help you make informed financial decisions through comprehensive financial guidance that supports your money management goals.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment