At Financial Canadian, we understand the unique challenges self-employed individuals face when seeking home financing. Navigating the mortgage landscape can be daunting, especially when your income isn’t as straightforward as a traditional employee’s.

This guide will explore the ins and outs of self-employed home financing, providing practical strategies to improve your chances of approval. We’ll cover everything from preparing your finances to exploring specialized mortgage options tailored for self-employed borrowers.

Self-Employed Home Buyers Face Unique Hurdles

Proving Your Income

Self-employed individuals often encounter significant obstacles when applying for a mortgage. One of the biggest hurdles is income verification. Unlike traditional employees with regular paychecks, self-employed individuals often have irregular income patterns. This makes it difficult to demonstrate a stable income to lenders.

Lenders typically require two years of tax returns to assess your income. However, these returns may not accurately reflect your current earnings, especially if your business has grown recently. A 2023 study by the Canadian Federation of Independent Business found that 68% of self-employed individuals reported difficulty in accurately representing their income to lenders.

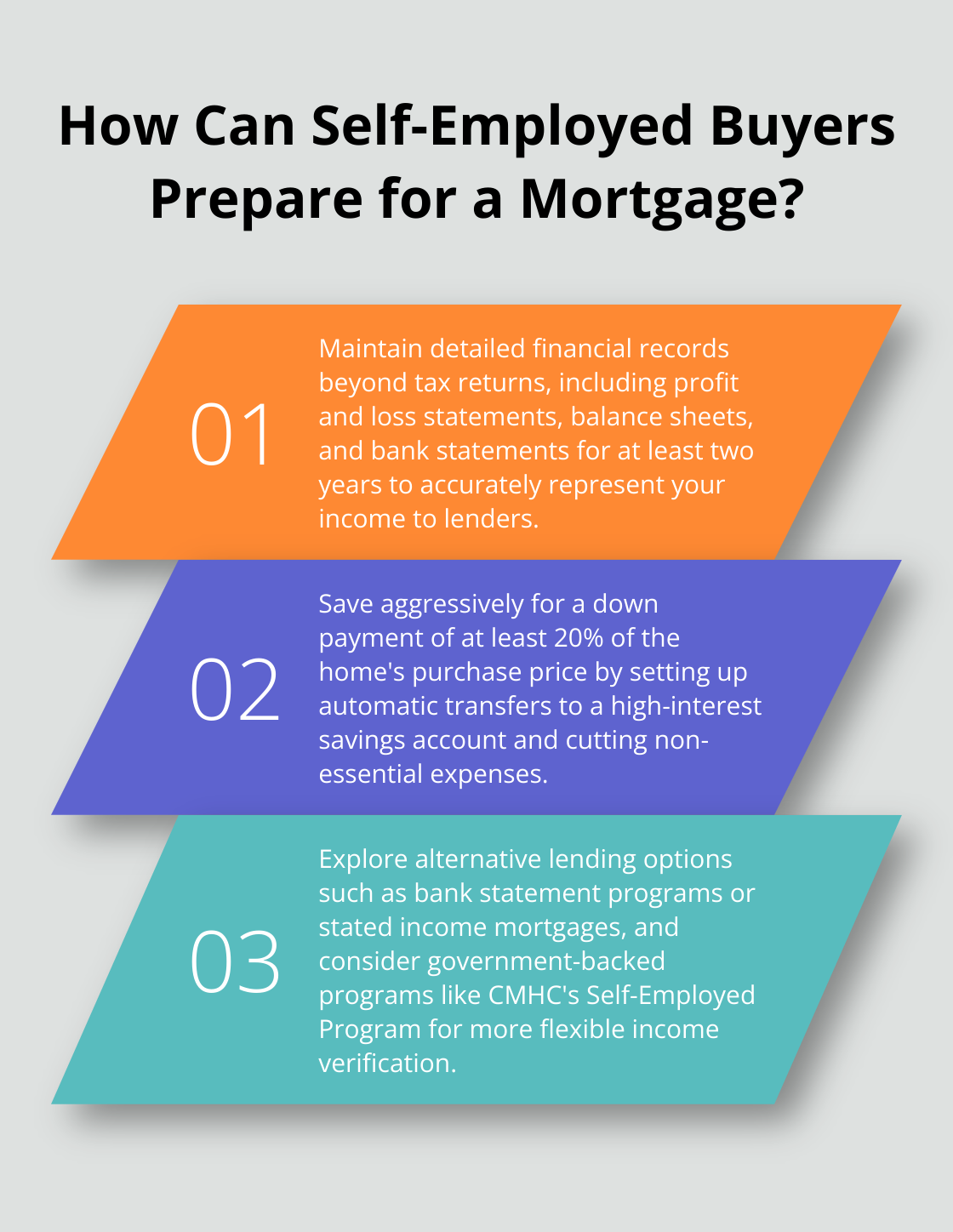

To overcome this, keep detailed financial records beyond just tax returns. This includes profit and loss statements, balance sheets, and bank statements. These additional documents can help paint a more accurate picture of your financial situation.

Dealing with Income Fluctuations

Self-employed income often fluctuates from month to month or year to year. This variability can make lenders nervous about your ability to consistently make mortgage payments.

A 2022 survey by the Bank of Canada found that 42% of self-employed Canadians experienced significant income fluctuations throughout the year. This unpredictability can lead to higher interest rates or even loan denials.

To mitigate this issue, consider building up a substantial emergency fund. Try to save at least six months of living expenses. This demonstrates to lenders that you can weather periods of lower income.

Overcoming the “High-Risk” Label

Many lenders view self-employed borrowers as higher risk due to the perceived instability of self-employment. This perception can lead to stricter lending criteria, higher interest rates, or larger down payment requirements.

A 2023 report from the Canada Mortgage and Housing Corporation (CMHC) revealed that self-employed borrowers were 1.5 times more likely to be denied a mortgage compared to traditional employees.

To combat this, focus on improving other aspects of your financial profile. Maintain a high credit score (aim for 700+), keep your debt-to-income ratio low (under 43% is ideal), and save for a larger down payment. These factors can help offset the perceived risk associated with self-employment.

Limited Employment History Documentation

Traditional employees can easily provide pay stubs and employment letters to verify their work history. Self-employed individuals, however, may struggle to provide similar documentation, especially if they’ve recently started their business.

Lenders often require a minimum of two years of self-employment history (though some may accept one year with additional documentation). This requirement can be a significant barrier for new entrepreneurs or those who have recently transitioned to self-employment.

To address this challenge, consider providing alternative forms of documentation. This might include contracts with clients, invoices, or business licenses. Additionally, if you have previous experience in the same industry as your current business, highlight this to demonstrate your expertise and potential for success.

As we move forward, it’s clear that self-employed home buyers face unique challenges. However, with proper preparation and financial organization, these hurdles can be overcome. In the next section, we’ll explore specific strategies to prepare your finances for a mortgage application as a self-employed individual.

How to Prepare Your Finances for a Self-Employed Mortgage

Keep Impeccable Financial Records

Accurate and detailed financial records are essential for self-employed mortgage applicants. Organize all your business and personal financial documents, including tax returns, profit and loss statements, balance sheets, and bank statements for at least the past two years.

Use accounting software like QuickBooks or Wave to streamline your record-keeping. These tools generate professional financial statements that lenders appreciate. Work with a certified accountant to ensure your financial statements are accurate and presented in a format lenders prefer.

Boost Your Credit Score

Your credit score significantly influences mortgage approval. TransUnion Canada provides answers to commonly asked questions about credit scores, credit reports, and related topics.

To improve your credit score:

- Pay all bills on time

- Keep credit card balances low (try to use less than 30% of your credit limit)

- Avoid applying for new credit in the months leading up to your mortgage application

Consider using a credit monitoring service to track your progress and identify areas for improvement.

Save Aggressively for a Down Payment

A larger down payment can offset the perceived risk associated with self-employment. Try to save at least 20% of the home’s purchase price to avoid mortgage insurance and potentially secure better interest rates.

Set up automatic transfers to a high-interest savings account dedicated to your down payment fund. Consider temporarily cutting non-essential expenses and redirect that money towards your savings goal.

Minimize Your Debt-to-Income Ratio

Lenders closely scrutinize your debt-to-income (DTI) ratio when assessing your mortgage application. For self-employed individuals, a low DTI is particularly important. Try to achieve a DTI of 43% or lower, as this is often the maximum allowed for many mortgage programs.

To reduce your DTI:

- Focus on paying down high-interest debt first

- Consider consolidating debts

- Negotiate with creditors for lower interest rates

- Avoid taking on new debt in the year leading up to your mortgage application

These strategies will significantly strengthen your financial profile and increase your chances of securing a mortgage as a self-employed individual. The next chapter will explore various mortgage options specifically tailored for self-employed borrowers, helping you find the best fit for your unique situation.

Exploring Mortgage Options for Self-Employed Canadians

Traditional Mortgages with Additional Documentation

Self-employed Canadians can qualify for traditional mortgages, but they need to provide extra documentation. This typically includes:

- Two years of personal and business tax returns

- Financial statements for your business

- Proof of business ownership

- Business license or registration

- Contracts with clients or vendors

This process takes more time, but it often results in better interest rates and terms.

Alternative Lending Options

For those who struggle to meet traditional mortgage requirements, alternative lending options provide a path to homeownership. This guide explains the requirements for self-employed mortgages, lender options, and tips for improving your chances of getting approved.

Bank statement programs allow lenders to use your bank statements to verify income instead of tax returns. This benefits individuals whose tax returns don’t accurately reflect their current income due to business deductions. However, these programs often come with higher interest rates.

Some lenders offer stated income mortgages, where you declare your income without extensive documentation. These loans typically require a larger down payment and have higher interest rates to offset the increased risk to the lender.

Credit unions often have more flexible lending criteria for self-employed borrowers. They may consider factors beyond just income and credit score, such as your overall financial picture and business potential.

Government-Backed Programs

Government-backed programs offer more favorable terms for self-employed borrowers. CMHC’s Self-Employed Program allows for more flexible income verification. This program requires documentation such as previous employment documentation based on type of income, recent account statements, business documentation, and signed contracts.

The First-Time Home Buyer Incentive (while not specifically for self-employed individuals) provides additional support. It offers 5% or 10% of the home’s purchase price to put toward a down payment, which helps self-employed individuals who struggle to save a large down payment.

We recommend exploring all these options to find the best fit for your situation. Each lender has different criteria, so don’t feel discouraged if one lender turns you down. Shop around and consider working with a mortgage broker who has experience with self-employed borrowers (this can help you navigate these options effectively).

Final Thoughts

Self-employed home financing presents challenges, but determined individuals can overcome them. Meticulous financial records, a strong credit score, and a substantial down payment will improve approval chances. Exploring various mortgage options, including traditional, alternative, and government-backed programs, can lead to success.

Preparation is essential for self-employed individuals seeking mortgages. Gather tax returns, profit and loss statements, and bank statements well before applying. At Financial Canadian, we understand the unique hurdles self-employed individuals face when pursuing homeownership.

Our web design services help businesses establish a strong online presence. A professional website can showcase your business effectively, potentially strengthening your financial profile for mortgage applications. Self-employed home financing requires extra effort, but with careful planning and persistence, you can achieve your homeownership goals.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment