Managing your money effectively requires the right digital tools. Personal finance Canada software has evolved significantly, offering Canadians powerful features for budgeting, investment tracking, and tax preparation.

We at Financial Canadian have tested dozens of financial management platforms to identify the best options for Canadian users. The right software can transform how you handle your finances, from simple expense tracking to comprehensive wealth management.

Which Personal Finance Software Works Best for Canadians

The wrong software choice can derail months of financial progress. Three solutions dominate the Canadian market, each serving distinct user needs with proven track records.

Mint Provides Free Comprehensive Tracking

Mint connects to over 17,000 financial institutions and offers the most robust free budget tracking available to Canadians. The platform automatically sorts transactions into categories and delivers monthly insights that reveal spending patterns without subscription fees. Credit Karma’s recent integration has modified some original Mint features, but the core functionality remains strong for users who want detailed expense analysis without ongoing costs.

YNAB Teaches Financial Discipline Through Structure

YNAB charges $109 annually but transforms how users approach money through its four-rule methodology. Canadian users save $600 the first month and $6,000 the first year according to user surveys. The software requires users to assign every dollar before they spend it, which creates proactive habits that prevent overspending. YNAB excels for Canadians with irregular income or serious debt elimination goals, as it emphasizes money aging and financial flexibility.

Quicken Manages Advanced Investment Portfolios

Quicken Premier costs $155 annually but delivers investment tracking capabilities that basic apps cannot match. The software connects with major Canadian brokerages and monitors portfolio performance, dividend income, and capital gains for tax purposes. Users can project financial scenarios up to 30 years ahead, making it valuable for retirement planning and wealth accumulation. The platform handles multiple currencies and investment types, from individual stocks to mutual funds.

Each software addresses different financial complexity levels, from basic expense tracking to sophisticated portfolio management. Your choice depends on whether you prioritize cost savings, financial education, or investment sophistication.

What Features Make Finance Software Worth Using

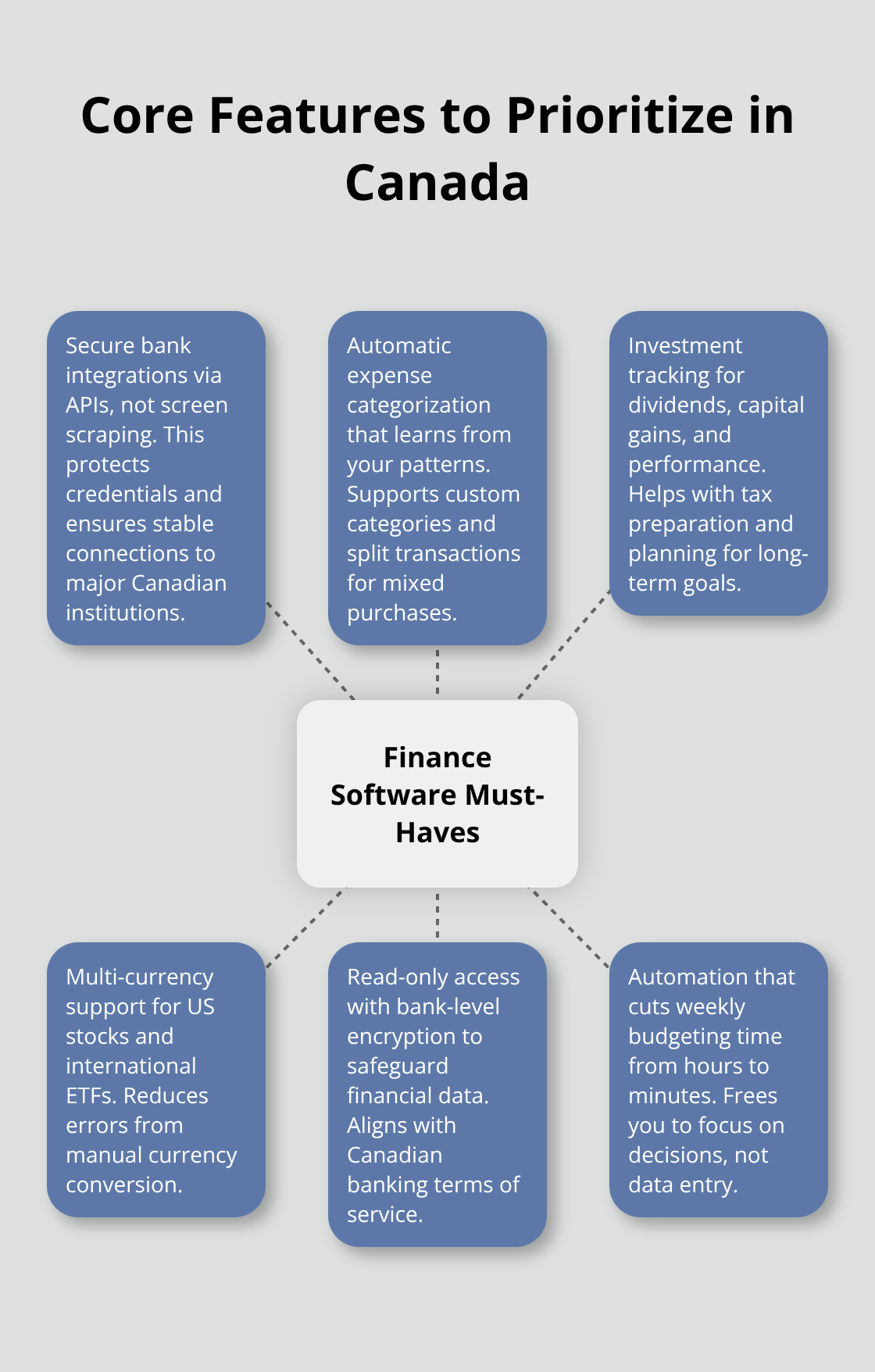

Canadian Bank Integration Protects Your Financial Data

Canadian bank integration stands as the most important feature when you select personal finance software. Statistics Canada reports that 55% of Canadians use digital financial tools, but many struggle with connectivity issues. The best platforms connect to major Canadian institutions including RBC, TD, Scotiabank, and BMO through secure APIs rather than screen scraping. Mint supports over 17,000 institutions while YNAB connects to most major Canadian banks through Plaid technology.

Screen scraping requires you to share login credentials, which violates most bank terms of service and creates security vulnerabilities. Look for software that uses read-only access and bank-level encryption to protect your financial data.

Automatic Transaction Categories Transform Raw Data

Automatic expense categorization transforms scattered spending data into actionable insights. Canadian households have varying spending patterns across categories like food, clothing, shelter and transportation, which makes category tracking essential for identifying savings opportunities. Advanced software learns from your spending patterns and assigns categories like groceries, transportation, and entertainment automatically. Manual categorization takes 2-3 hours weekly for most users, while automated systems reduce this to 15 minutes of verification. Choose platforms that allow custom category creation and split transactions, since Canadian users often have mixed purchases that span multiple budget categories.

Investment Tracking Eliminates Portfolio Management Gaps

Investment tracking within your budgeting software provides comprehensive financial visibility that separate tools cannot match. Quicken connects with major Canadian brokerages and tracks dividend income, capital gains, and portfolio performance in real-time. This integration helps with tax preparation since the software calculates adjusted cost basis and tracks foreign withholding taxes on international investments (particularly important for US stocks). The best financial apps can simplify your financial life during tax season when investment data syncs automatically with tax preparation software. Multi-currency support becomes essential for Canadians holding US stocks or international ETFs, as manual currency conversion creates calculation errors that affect investment decisions.

These core features separate professional-grade software from basic apps, but your specific financial situation will determine which capabilities matter most for your money management strategy.

How Do You Pick the Perfect Finance Software

Your financial situation determines which software features matter most, not marketing promises or popular recommendations. Start with your monthly income complexity – salaried employees with simple expenses need different tools than freelancers who manage irregular income streams and business expenses. Canadians who earn under $60,000 annually often succeed with free platforms like Mint, while those with investment portfolios that exceed $100,000 require advanced features that justify Quicken’s $155 annual cost. YNAB works best for users with debt elimination goals or those who struggle with overspending, since its zero-based budgeting methodology forces intentional spending decisions.

Subscription Costs Reveal Software Value

Free software like Mint generates revenue through credit card recommendations and financial product advertisements, which can influence the advice you receive. YNAB’s $109 annual fee eliminates conflicts of interest but requires commitment to justify the expense – users who don’t engage with the software daily waste their subscription money. Quicken Premier costs $155 yearly but saves investment-focused users hundreds in portfolio management fees compared to financial advisors who charge hourly rates.

Most Canadians underestimate the time investment that effective budgeting requires – free software demands 3-4 hours weekly for manual data entry and categorization, while premium platforms reduce this to 30 minutes through automation. Trial periods matter more than advertised features since personal finance habits vary significantly between users.

Customer Support Quality Affects Long-Term Success

Canadian users face unique challenges with US-based software companies that don’t understand provincial tax differences or Canadian banking regulations. YNAB provides extensive educational resources and community forums that teach budgeting principles, which makes it valuable for users who want to develop financial skills beyond basic tracking. Quicken offers phone support during business hours but struggles with Canadian-specific investment account types like RRSPs and TFSAs – RRSPs are for retirement with tax-deductible contributions and taxable withdrawals, while TFSAs are for any purpose with tax-free withdrawals and non-deductible contributions.

Mint relies primarily on online help articles and user forums, which creates frustration when bank connectivity issues arise. Choose software with Canadian customer service representatives who understand local financial institutions and tax implications, since generic support cannot resolve region-specific technical problems that affect account synchronization and data accuracy.

Final Thoughts

Personal finance Canada software transforms money management from guesswork into data-driven decisions. Mint serves budget-conscious Canadians who want comprehensive expense tracking without subscription fees. YNAB works for users committed to debt elimination and disciplined spending habits through its structured approach. Quicken suits investment-focused individuals who need advanced portfolio tracking and tax reporting capabilities.

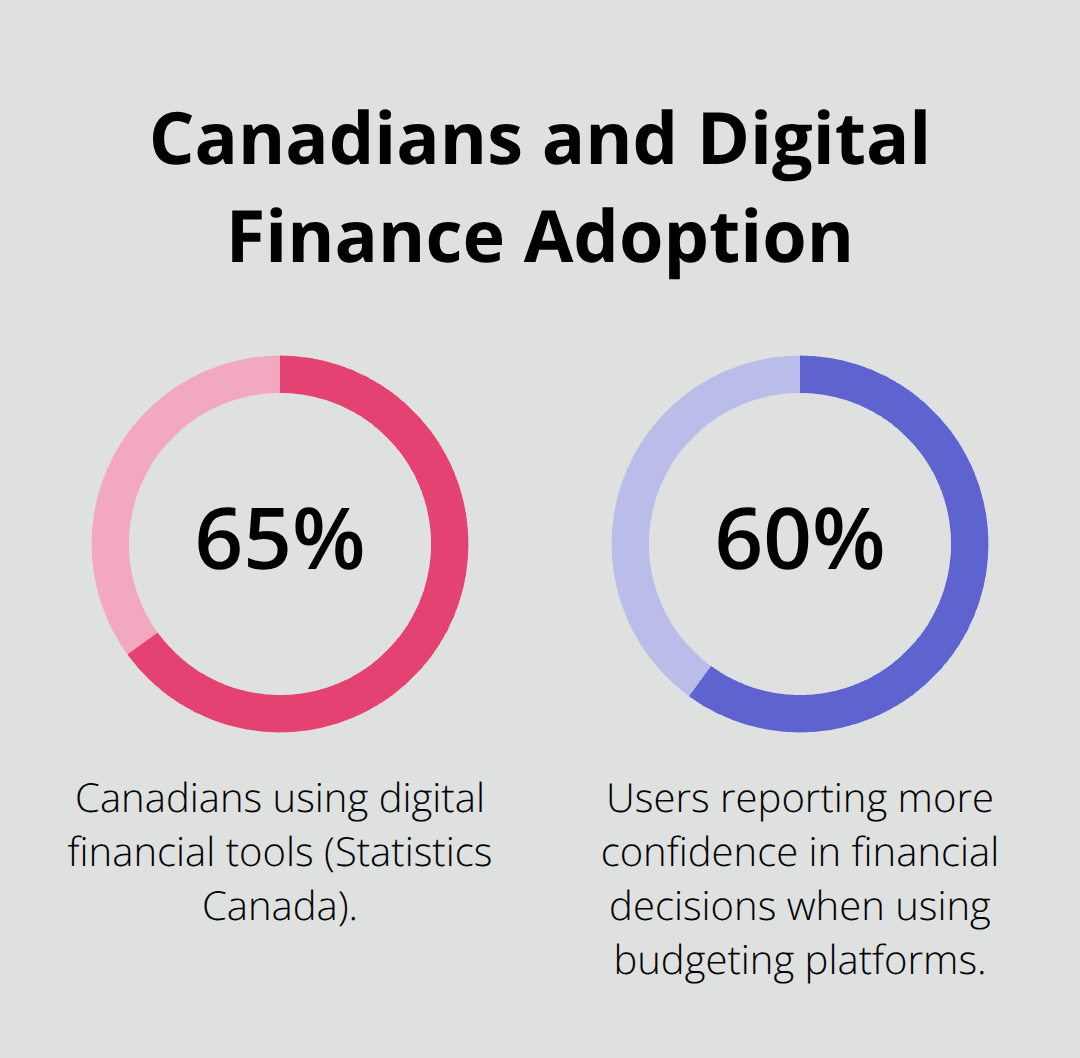

Statistics Canada shows 65% of Canadians use digital financial tools, yet many still struggle with overspending and inadequate savings. The right software addresses these challenges through automated expense categorization, spending insights, and multiple account connections in one dashboard. Users report 60% more confidence about their financial decisions when they use dedicated budgeting platforms.

Download free trials from your top software choices and connect one checking account initially to test transaction import accuracy. Spend two weeks to track expenses before you commit to annual subscriptions (most Canadians see improved spending awareness within the first month of consistent use). We at Financial Canadian help businesses establish strong online presence through our comprehensive web design service with responsive designs and SEO optimization.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment