Credit card interest rates in Canada range from 8.99% to 29.99%, making the right choice worth hundreds of dollars annually. Finding the lowest interest credit cards Canada offers requires understanding different card types and their fee structures.

We at Financial Canadian have analyzed dozens of low-interest options to help you secure the best rates. This guide walks you through proven strategies to find and qualify for Canada’s most competitive credit card offers.

Which Low Interest Credit Card Types Should You Consider

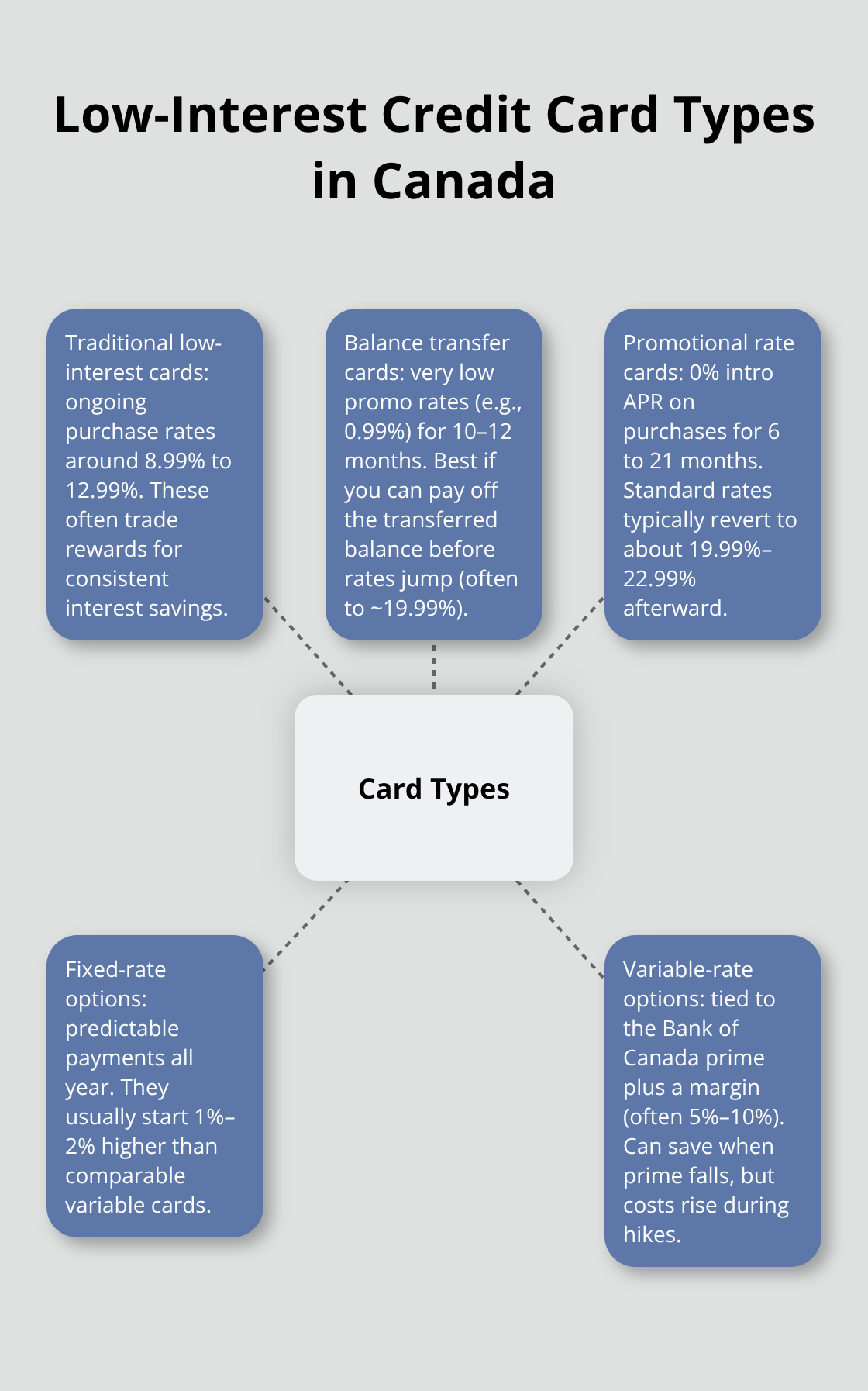

Three distinct categories of low-interest credit cards dominate the Canadian market, each serving specific financial situations. Traditional low-interest cards offer ongoing rates between 8.99% and 12.99%, making them ideal for Canadians who regularly carry balances. The Scotiabank Platinum American Express Card leads this category with a 9.99% rate, while the RBC Visa Classic Low Rate Option provides 12.99% with a modest $20 annual fee. These cards sacrifice rewards for consistent savings on interest charges.

Balance Transfer Cards Reduce Existing Debt Costs

Balance transfer cards target debt consolidation with promotional rates as low as 0.99% for up to 10 months. The MBNA Platinum Plus Mastercard offers 0.99% for 10 months on transfers, though it charges a 3% transfer fee. CIBC Select Visa provides similar terms but extends the promotional period to 12 months. These cards work best when you can pay off transferred balances during the promotional window, as rates jump to 19.99% afterward.

Promotional Rate Cards Maximize Short-Term Savings

Promotional rate cards feature 0% introductory APR periods that last 6 to 21 months on purchases. The Capital One Guaranteed Mastercard offers 0% for 6 months with no annual fee, while premium options extend promotional periods to 15 months. These cards excel for large purchases like home renovations or wedding expenses when you can repay within the promotional timeframe. Standard rates typically range from 19.99% to 22.99% once promotions end (making timely repayment essential for maximum benefit).

Fixed vs Variable Rate Options

Fixed-rate cards maintain the same interest rate year-round, providing predictable monthly payments regardless of market changes. Variable-rate cards start with lower initial rates but fluctuate with the Bank of Canada’s prime rate. Most low-interest cards in Canada use variable rates tied to prime plus a margin (typically 5% to 10%). Fixed rates offer stability, while variable rates can provide savings when prime rates drop but increase costs during rate hikes.

Understanding these card types helps you identify which option matches your spending patterns and repayment timeline. The next step involves comparing specific features and costs to find the best value for your financial situation.

What Should You Check Before Applying for Low Interest Cards

Low-interest credit cards require examination of three cost components that determine your total expense. The advertised interest rate represents only part of your actual costs. Annual fees and transaction charges often add $50 to $200 yearly to your total expense.

The TD Emerald Visa Card advertises 12.99% interest but charges a $120 annual fee. This makes it more expensive than the no-fee Capital One Guaranteed Mastercard at 19.99% for balances under $2,000. Calculate your break-even point: divide the annual fee by the interest rate difference, then multiply by 100 to find the minimum balance where the low-rate card saves money.

Interest Rate Structures Differ Across Transaction Types

Purchase rates, cash advance rates, and balance transfer rates vary substantially on the same card. Cash advances typically cost 22.99% to 24.99% regardless of your purchase rate. The RBC Visa Classic Low Rate Option charges 12.99% on purchases but 22.99% on cash advances (creating a 10-percentage-point gap).

Variable rates fluctuate with the Bank of Canada overnight rate through monetary policy adjustments made on eight fixed dates annually. A card advertised at prime plus 9% costs 12.75% today but could reach 15.75% if rates rise 3%. Fixed rates provide payment predictability but typically start 1% to 2% higher than comparable variable options.

Hidden Fees Add to Your True Cost

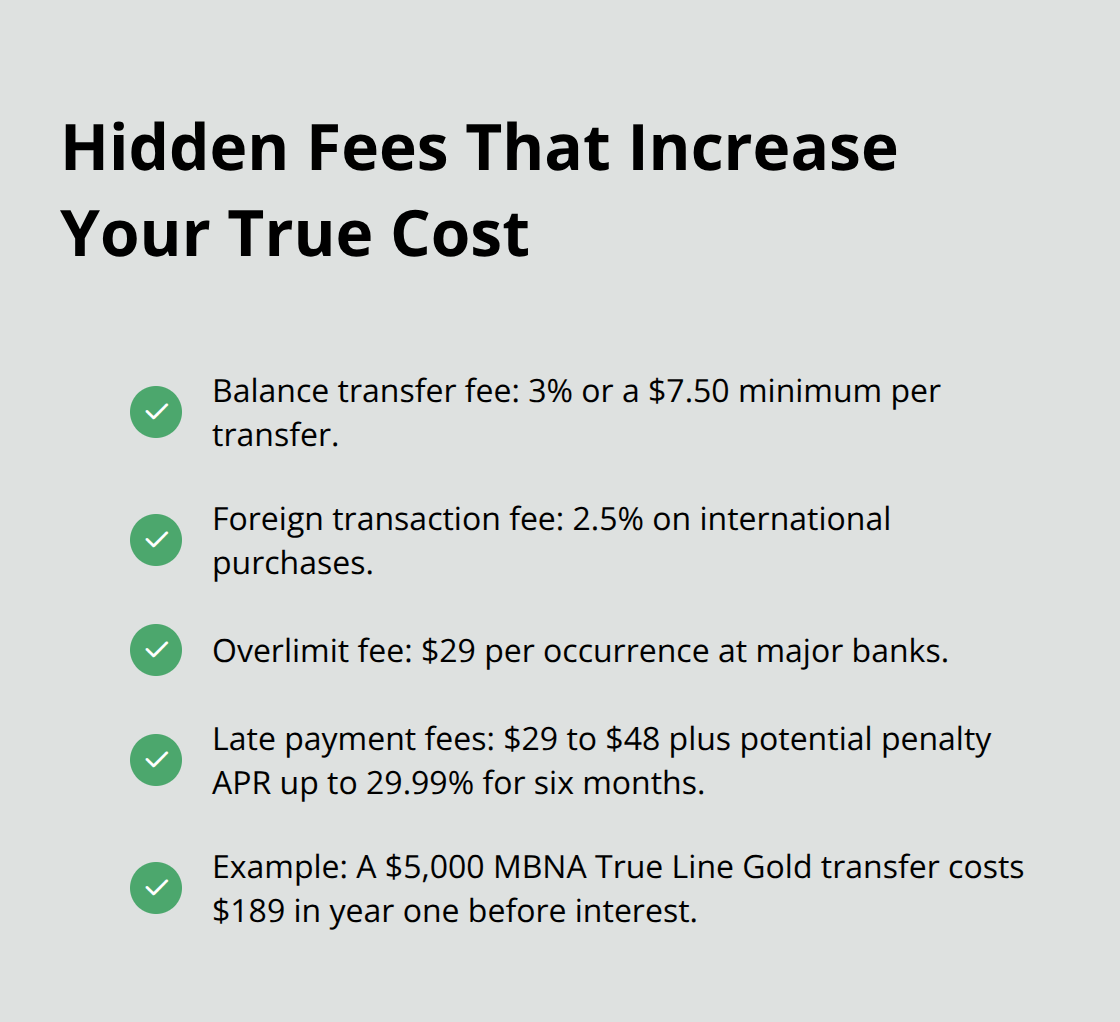

Most Canadian cards charge 3% or $7.50 minimum per transfer for balance transfers. Foreign transaction fees add 2.5% to international purchases, while overlimit fees cost $29 per occurrence at major banks.

Late payment penalties trigger both fees ($29 to $48) and penalty interest rates up to 29.99% for six months. The MBNA True Line Gold Mastercard charges $39 annually plus 3% balance transfer fees. A $5,000 transfer costs $189 in the first year before interest charges begin.

Terms and Conditions Contain Important Details

Credit agreements specify grace periods, minimum payment calculations, and rate change notifications. Most cards offer 21-day grace periods on purchases when you pay your full balance monthly. Minimum payments typically equal 2% to 3% of your outstanding balance or $10 (whichever is greater).

Card issuers must provide 45 days’ notice before increasing your interest rate on existing balances. Some promotional rates apply only to new purchases, not existing debt. Understanding these terms helps you avoid unexpected charges and maximize your card’s benefits as you develop strategies to secure the most competitive rates available.

How Can You Secure the Lowest Interest Rates

Your credit score directly determines which low-interest cards approve your application and at what rate. Scores above 750 unlock prime-plus-5% rates, while scores between 650-699 typically qualify for prime-plus-8% options. TransUnion data shows Canadian credit scores average 760, meaning most applicants have access to better rates than mid-tier options.

Improve Your Credit Score Before You Apply

Pay down credit card balances below 30% utilization before you submit applications. A $5,000 credit limit requires balances under $1,500 to optimize your score. Pay existing balances strategically: multiple cards at 29% utilization hurt your score more than one card at 60%. Focus payments on high-utilization cards first to maximize score improvements within 60 days.

Target Promotional Periods for Maximum Savings

Major Canadian banks launch promotional campaigns quarterly, typically in January, March, September, and November to coincide with fiscal periods and holiday spending. The BMO CashBack Mastercard offered 0.99% balance transfers for 12 months during their September 2024 promotion but returned to standard 3.99% rates by December.

Monitor bank websites and financial newsletters for promotional announcements. Banks process applications submitted within the first two weeks of promotions with priority and offer better approval odds. These early applications often receive the most favorable terms before banks tighten their criteria.

Negotiate Based on Your Banking Relationship

Banks reduce rates for customers with substantial deposits, mortgages, or investment accounts. RBC offers rate reductions up to 2% for clients who maintain $25,000 in combined accounts. Call the retention department, not general customer service, to request rate reductions.

Mention competing offers specifically: state that Scotiabank offered you 9.99% when you request a rate match. Threaten account closure only if you prepare to follow through (as banks track these requests). The optimal negotiation window occurs 6-12 months after account opening when you demonstrate responsible usage patterns and establish your value as a customer.

Final Thoughts

Canada’s lowest interest credit cards require systematic comparison of rates, fees, and terms across different card categories. Traditional low-interest cards work best for ongoing balances, while promotional and balance transfer options excel for specific debt management goals. Your credit score above 750 opens access to prime-plus-5% rates, which makes score improvement your first priority before you apply.

Calculate total annual costs that include fees rather than focus solely on advertised rates. A $120 annual fee card needs substantial balances to justify its lower rate compared to no-fee alternatives (especially for balances under $2,000). Time your applications during quarterly promotional periods when banks offer their most competitive terms and approval rates.

Successful rate negotiations depend on your relationship strength and specific competing offers. Banks reduce rates up to 2% for customers with significant account balances or multiple products. We at Financial Canadian help you navigate these decisions through our comprehensive financial guidance, where Canadians can access clear information about credit products that match their needs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment