Getting approved for a personal loan in Canada requires more than just filling out an application. Lenders want to see proof that you can repay the money, and they’ll examine your finances closely before making a decision.

At Financial Canadian, we’ve put together this guide to show you exactly what documentation and financial health lenders are looking for. By preparing ahead, you can significantly improve your chances of approval.

What Documents and Credit Health Lenders Examine

Government-Issued Identification and Proof of Address

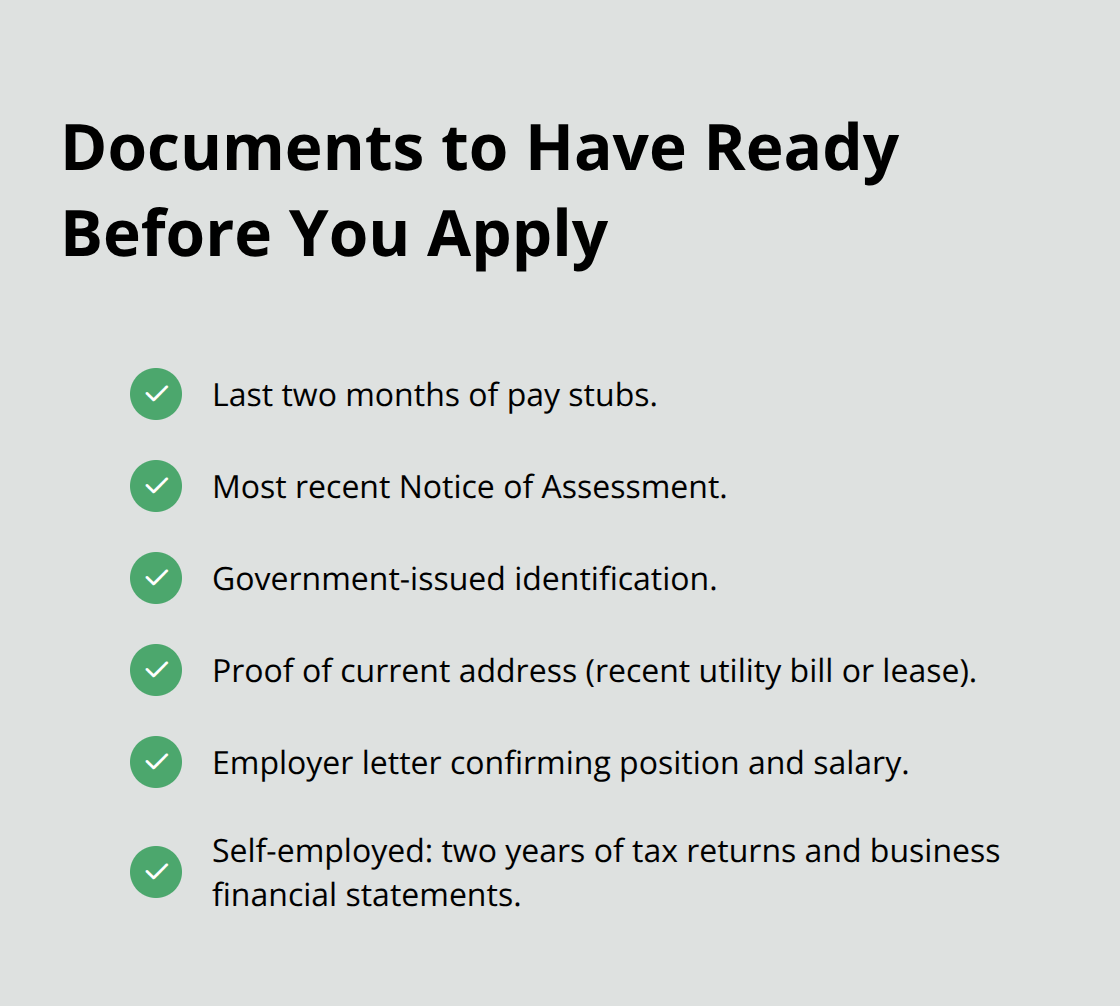

Lenders in Canada request specific documents before approving your personal loan, and submitting incomplete paperwork is one of the fastest ways to get rejected. You’ll need government-issued identification like a driver’s license or passport, your Social Insurance Number, and proof of your current address through a recent utility bill or lease agreement. These documents verify who you are and where you live, and lenders won’t move forward without them.

Income Documentation and Employment Verification

Most lenders require proof of income from the past two months, which can be recent pay stubs, T4 forms, or Notice of Assessment documents from the Canada Revenue Agency. If you’re self-employed, prepare your last two years of tax returns and financial statements to demonstrate consistent earnings. Employment verification matters more than you might think-lenders want to confirm you actually work where you claim to work, so having a letter from your employer stating your position, salary, and employment start date strengthens your application significantly.

Understanding Your Credit Score and Report

Your credit score determines whether lenders approve you and what interest rate you’ll receive. Scores between 600 and 659 are considered fair, and many lenders view scores of 600 and above as lower risk, making approval possible even without perfect credit. However, scores in the 300 to 599 range create serious obstacles for favorable loan terms and lower interest rates.

Obtain your credit report from Equifax or TransUnion to check for errors or fraudulent activity that could hurt your approval chances. Missed payments are a common reason for poor scores, so staying current on all obligations is essential. High balances on credit cards relative to your limits also lower your score, and applying for multiple loans within a short period damages your creditworthiness further.

Rising Delinquencies and Tightened Lending Standards

TransUnion Canada’s quarterly Credit Industry Insights Report, which analyzes data from over 30 million credit files covering nearly every credit-active consumer in Canada, shows that delinquency rates largely stabilized across major credit products in Q4 2025. This trend indicates that lenders are scrutinizing payment history more carefully than before and have tightened underwriting standards considerably. Documenting stable income and manageable debt is increasingly important for approval.

If you have weak credit, consider ongoing monitoring to spot fraud and assist with identity recovery before you apply. Lenders will check your credit report regardless, so understanding your score beforehand prevents surprises during the approval process and helps you identify what lenders will actually see when they review your file.

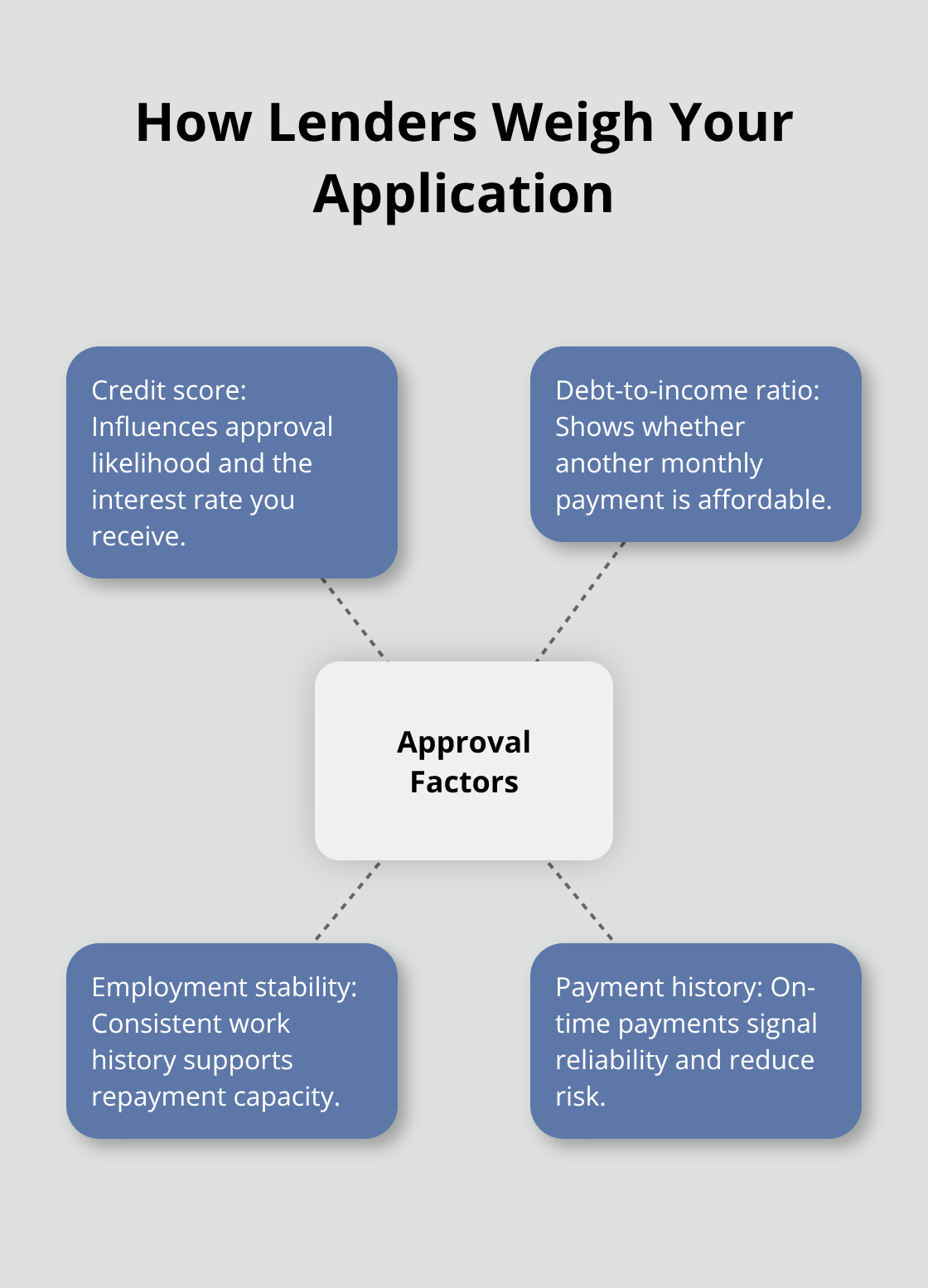

What Lenders Actually Look At During Approval

Your Debt-to-Income Ratio Determines Affordability

Lenders evaluate three interconnected factors that determine whether you receive approval and what interest rate you’ll pay. Your debt-to-income ratio reveals whether you can realistically afford another monthly payment alongside your existing obligations. If you spend more than 43% of your gross monthly income on debt repayment, most lenders will reject your application outright, regardless of your credit score.

Calculate this ratio by adding all monthly debt payments (credit cards, car loans, mortgages, student loans) and dividing by your gross monthly income. Someone earning $4,000 monthly with $1,500 in existing debt payments already sits at the 37.5% threshold, leaving minimal room for a personal loan payment. Try paying down credit card balances or waiting until your income increases to tighten this ratio before applying.

Employment History and Income Stability

Employment history matters more than job title or industry. Lenders want to see consistent work at the same employer for at least six months if employed full-time, though two years is required if you have variable incomes or are self-employed. Frequent job changes signal instability, even if you’ve remained continuously employed.

If you switched jobs within the past year, prepare documentation showing your new employer’s stability and your salary trajectory. Self-employed applicants face stricter scrutiny, requiring two years of tax returns and business financial statements to prove income consistency. This documentation directly influences whether lenders approve your application and at what rate.

Credit Accounts and Payment History

Examine your credit accounts and payment history closely before applying. Multiple recent credit applications within three months damage your score significantly because lenders interpret this as desperation for credit. The number of open accounts matters too-having too many open credit cards or too few accounts both send mixed signals to underwriters.

Lenders have tightened standards considerably, making payment history verification a primary approval factor. If you have any accounts showing late payments or collections activity, address these before submitting your application. Even one missed payment from years ago can haunt your file, so obtaining your credit report beforehand reveals exactly what lenders will see and gives you time to dispute inaccuracies.

How Lenders Use This Information

Lenders combine these three factors to assess your risk profile and repayment capacity. A strong employment history compensates for a slightly elevated debt-to-income ratio, while a perfect payment history can offset a lower credit score. However, weakness across multiple categories (high debt ratio, recent job changes, and payment problems) creates a difficult approval scenario that requires significant improvement before you apply.

Understanding how lenders weigh these factors helps you identify which areas need attention. Your next step involves taking concrete action to strengthen whichever category presents the biggest obstacle to approval.

Strengthen Your Financial Profile Before You Apply

Waiting to apply for a personal loan until you’ve addressed weak areas in your application dramatically improves your approval odds. Lenders use fixed criteria to evaluate risk, and you control several of these factors directly. The most effective approach focuses on three concrete actions that take weeks or months to execute properly, rather than rushing an application when lenders will immediately spot red flags.

Improve Your Credit Score First

Your credit score influences both approval likelihood and your interest rate. If your score sits below 660, you face significantly higher rates or rejection entirely. The fastest way to improve your score is to pay down credit card balances to below 30% of your limits. Someone with a $5,000 credit card limit holding a $3,500 balance should target reducing this to $1,500 or less before applying. This adjustment alone typically raises scores by 20 to 50 points within 30 to 60 days.

Avoid opening new credit accounts during this period because each application triggers a hard inquiry that temporarily lowers your score. If you’ve made late payments, these damage your score for up to seven years, but their impact weakens significantly after two years of on-time payments. Focus on making every payment on time moving forward because payment history comprises 35% of your credit score calculation.

For those with limited credit history, a secured credit card requires a cash deposit and reports to all three credit bureaus, helping you establish a positive track record within six months of consistent on-time payments.

Reduce Your Debt-to-Income Ratio

Your debt-to-income ratio represents the second priority because lenders automatically reject applications when this ratio exceeds 43%. If you currently carry $1,500 in monthly debt payments on a $4,000 gross income, you’re at 37.5% and have minimal room for a personal loan payment. Aggressively paying down existing debts before applying creates space in your budget and signals financial discipline to lenders.

Prioritize eliminating high-interest credit card debt first because this reduces both your ratio and your overall financial burden. Paying off a $3,000 credit card balance over three months requires roughly $1,000 monthly payments, but this effort directly improves your approval chances and reduces the interest you’ll ultimately pay on a new personal loan. Avoid taking on new debt during this period because additional car loans or credit accounts will damage your ratio further.

Organize Your Financial Documentation

Gather your complete financial documentation at least two weeks before submitting your application. Lenders request specific items, and missing documents delay approval or trigger rejection. Collect your last two months of pay stubs, your most recent Notice of Assessment from the Canada Revenue Agency, government-issued identification, proof of your current address through a recent utility bill, and a letter from your employer confirming your position and salary.

If you’re self-employed, prepare your last two years of complete tax returns and business financial statements. Request your credit report from Equifax or TransUnion beforehand to identify errors or fraudulent accounts that could harm your application. Disputing inaccuracies takes time, so address these issues weeks before you apply to prevent last-minute complications. Having organized, complete documentation ready demonstrates professionalism and removes obstacles that lenders use to reject applications.

Final Thoughts

Personal loans Canada approval hinges on three factors you control: your credit score, debt-to-income ratio, and employment stability. Start by obtaining your credit report from Equifax or TransUnion to identify which area presents the biggest obstacle. If your score sits below 660, pay down credit card balances to below 30% of your limits before applying; if your debt-to-income ratio exceeds 43%, eliminate high-interest debt over the next few months.

Gather your complete financial documentation at least two weeks before submitting your application, including pay stubs, your Notice of Assessment, government identification, proof of address, and an employment verification letter. Self-employed applicants should prepare two years of tax returns and business financial statements. Request your credit report beforehand to dispute any inaccuracies before lenders review your file, since missing documents delay approval or trigger rejection outright.

The effort you invest now in strengthening your application pays dividends through faster approval, better interest rates, and lower overall borrowing costs. Lenders have tightened underwriting standards considerably, making thorough preparation essential. Visit Financial Canadian to explore resources that support your financial goals.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment