Your credit score determines whether lenders approve you for mortgages, car loans, and credit cards. At Financial Canadian, we’ve created this Canada credit score checklist to help you review your finances before you apply.

Most people don’t know what errors hide in their credit report or how their score is calculated. Taking an hour to verify your information now can save you thousands in interest rates later.

What Credit Score Range Do You Need in Canada

How Canadian Credit Bureaus Calculate Your Score

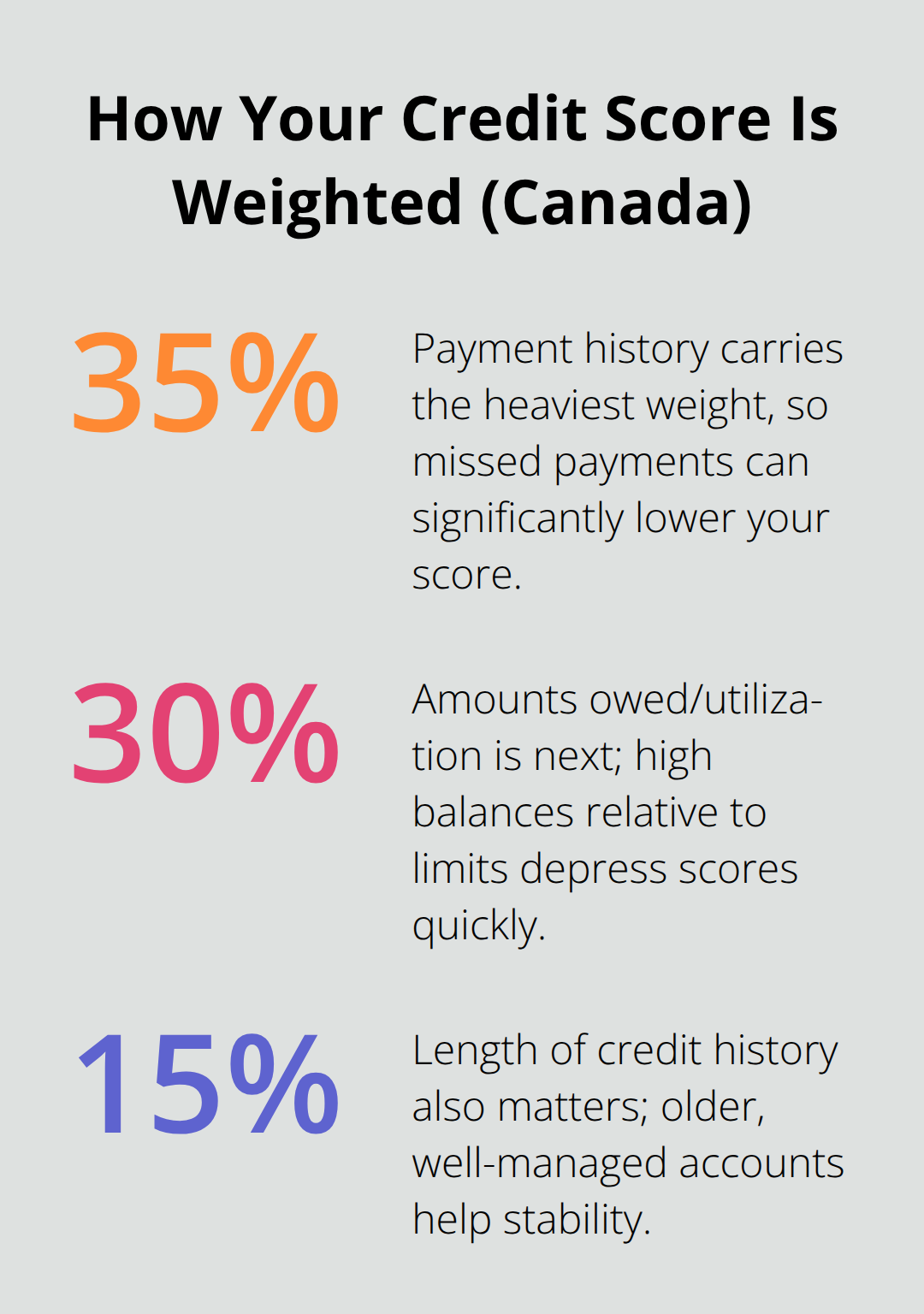

Equifax and TransUnion calculate your score based on five factors: payment history (35%), amounts owed (30%), length of credit history (15%), credit mix (10%), and new credit inquiries (10%). Payment history matters most, which means a single missed payment can drop your score by 100 points or more. If you missed a payment in 2021 and it still appears on your report, that event continues to damage your approval odds today.

Negative marks lose power over time. A late payment from 2021 has less impact now than when it first occurred, but it won’t disappear entirely until seven years pass from the date of the missed payment. Lenders weight recent behavior more heavily than distant history, so your actions over the next 12 months matter far more than what happened five years ago.

Understanding the 300 to 900 Score Scale

Canadian credit scores range from 300 to 900, and the difference between 650 and 720 can mean the gap between a mortgage denial and approval at a competitive rate. A score of 650 to 699 typically qualifies you for credit, but lenders charge higher interest rates because they see you as higher risk. At 700 to 749, you access better rates on mortgages and car loans. Above 750, you enter the tier where lenders compete for your business with their best offers.

For mortgages specifically, most Canadian lenders require a minimum score of 620, but scores below 680 trigger higher rates and stricter terms. The jump from 650 to 720 opens doors that remain closed at lower levels. Understanding where Canada’s average credit score sits helps you benchmark your own position.

Two Actions That Move Your Score Fastest

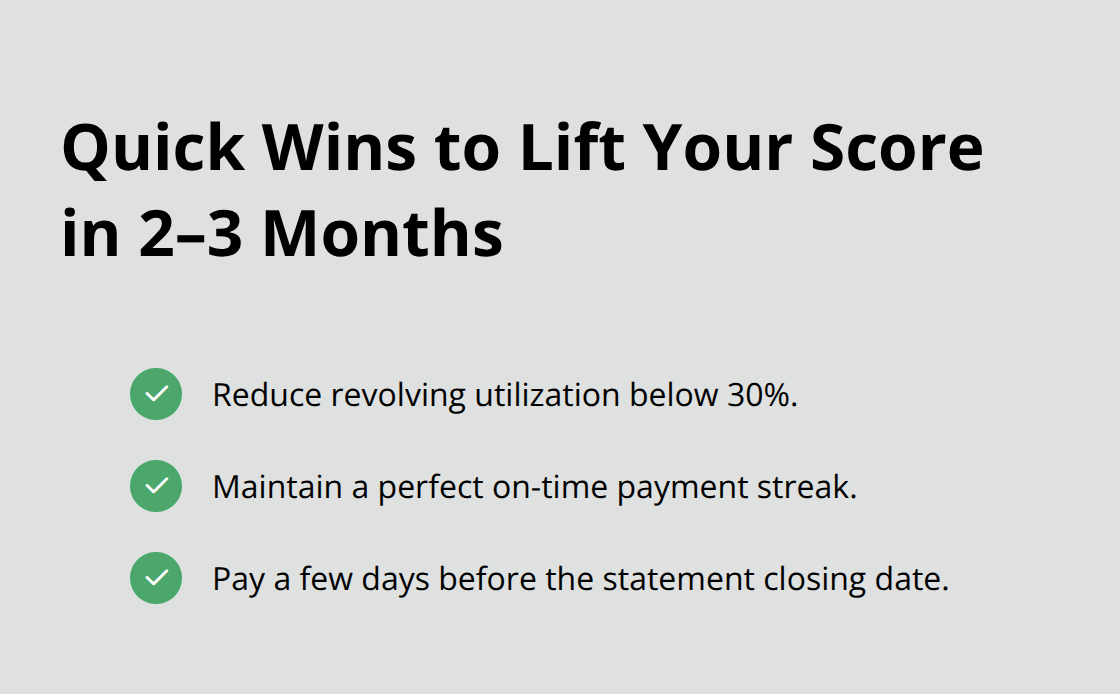

If you’re sitting at 650 and trying for a mortgage within a year, focus on two actions: reduce your revolving utilization to below 30% and maintain perfect payment history going forward. If your current utilization is 60% on a $10,000 credit limit, paying that balance down to $3,000 or less can lift your score by 50 to 100 points within two to three months (assuming the new balance reports to the bureaus).

The timing of your payment matters because credit card companies report balances on your statement closing date, not when you pay. Paying down your balance a few days before your statement closes ensures the lower amount reaches the bureaus, not your peak balance during the month. This single tactic costs nothing and produces measurable results quickly.

What Happens Next in Your Credit Review

Once you understand where your score stands and what moves it, the next step involves checking your credit report for errors that may be holding you back.

Finding and Fixing Errors on Your Credit Report

Errors on credit reports are a widespread issue that directly blocks financing. The frustrating part is that you won’t know if errors exist in your report unless you check it yourself.

Getting Your Free Credit Report

Getting your free annual credit report from Equifax and TransUnion takes 15 minutes online and costs nothing. Visit Equifax.ca or TransUnion.ca to request your report, or call them directly. You’ll need to verify your identity with personal information like your Social Insurance Number and address. Most reports arrive within days. Many people skip this step entirely, assuming their information is correct. That assumption costs them thousands in higher interest rates or outright loan denials.

Common Errors That Appear on Canadian Credit Reports

Personal information mistakes rank high on the list-incorrect names, addresses, dates of birth, or phone numbers can confuse lenders and hurt your approval odds. Creditors sometimes misreport account balances, showing you owe more than you actually do, which inflates your utilization ratio artificially. Incorrect payment histories appear frequently too; a payment you made on time gets recorded as late, or an account shows activity after you closed it.

Public records errors occur when courts, bankruptcy trustees, or collection agencies submit wrong information to the bureaus. Car dealers entering your information into their systems sometimes make typos that cascade into your credit file. Billing errors on service contracts like cellphone or internet plans can also damage your report if the provider reports them as delinquent. Identity theft and fraud create the most serious errors-unauthorized accounts or credit inquiries appearing under your name that you never opened.

The Correction Process That Actually Works

Start by gathering documentation that proves the error exists. If a payment shows as late but you have a bank statement or cancelled check proving you paid on time, that’s your evidence. Contact the creditor or service provider first and explain the error clearly; ask them to send a correction directly to Equifax and TransUnion. This step resolves many errors at the source before they reach the bureaus.

If the creditor won’t cooperate, contact the credit bureaus directly through their dispute process. Submit your supporting documentation along with a written explanation of why the information is wrong. The bureaus have 30 days to investigate and respond. Follow up with both the creditor and the bureaus after 30 days to confirm the correction went through. Many people submit a dispute and assume it’s handled, then never verify the fix actually appeared on their report. Check your report again two months later to confirm the error is gone.

What Happens When You Fix Errors Before Applying

Correcting errors before you apply for a mortgage can mean the difference between approval at a standard rate and rejection or approval at a penalty rate. Once your report is clean and your utilization is under control, you’re ready to assess the final piece of your credit profile before you submit any applications.

What to Fix First to Boost Your Approval Odds

Attack Your Utilization Ratio First

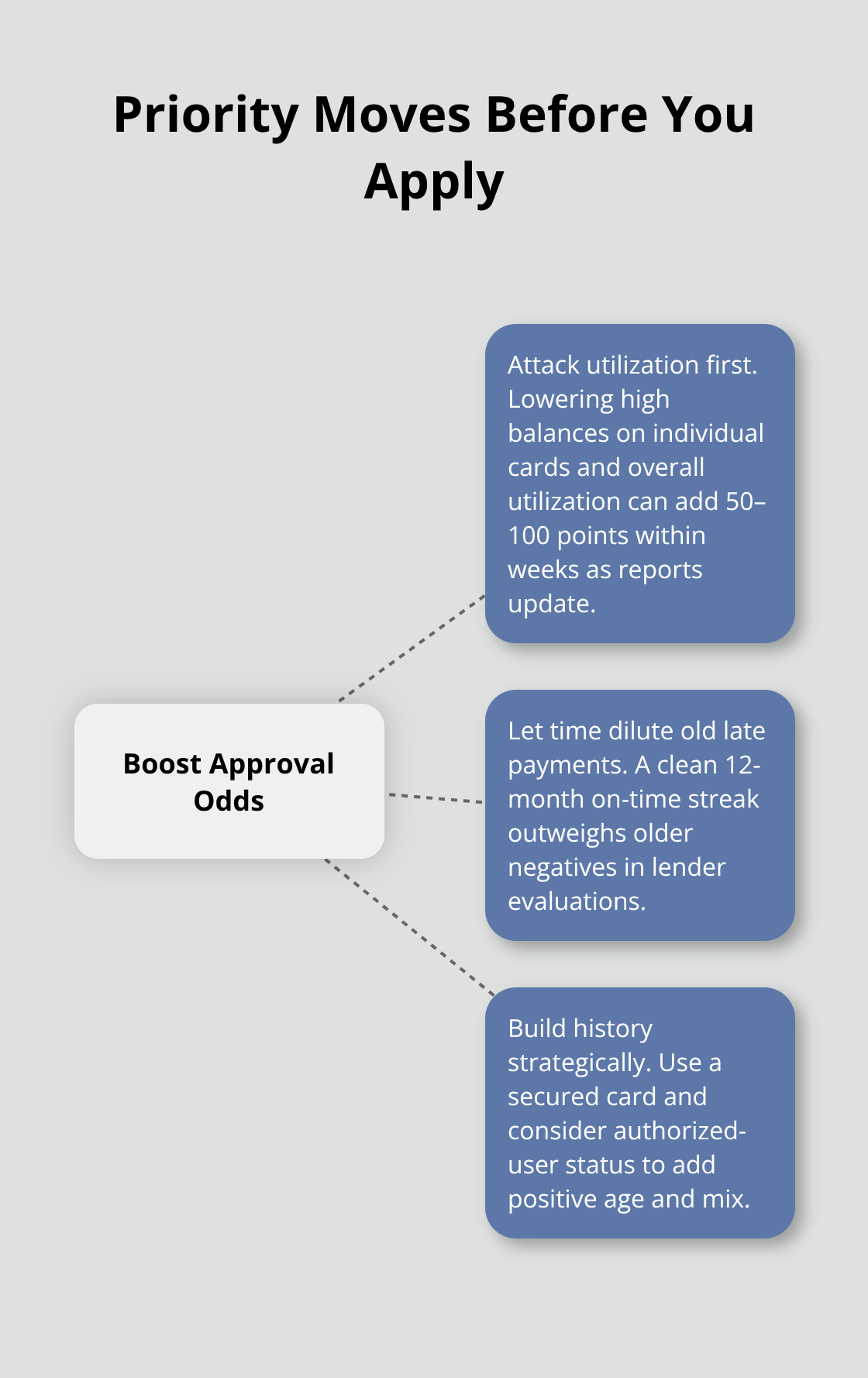

Your credit report is now clean, but your credit profile still needs work before you apply. The next phase focuses on three concrete actions that move your score and improve your mortgage qualification. Start with your utilization ratio because it’s the fastest lever you control. If you carry a 60% balance on a $10,000 limit, your utilization actively suppresses your score by 50 to 100 points. Dropping that to 30% or less takes weeks, not months, and produces measurable gains on your next credit report update.

The math is straightforward: paying down $3,000 on that $10,000 limit costs you nothing except the money you spend anyway, but it repositions you as a lower-risk borrower in the eyes of every lender. Don’t spread payments across multiple cards equally; attack the card with the highest balance first because utilization is calculated per account and across all accounts combined. A person with one card at 10% utilization and another at 50% scores better than someone with both cards at 30%, so prioritize the worst offender.

Time Works in Your Favor With Late Payments

Late payments and collection accounts require a different strategy because time works in your favor here. A missed payment from 2021 has already lost significant power compared to when it first hit your report, and every month that passes without a new late payment weakens its grip further. If you have an old collection account on your report, contact the creditor and ask about a pay-for-delete arrangement, though Canadian collection agencies increasingly resist removing accounts even after payment.

What matters more is establishing a clean payment record going forward because lenders weight recent behavior heavily. Make every payment on time for the next 12 months-this matters far more than erasing a five-year-old late payment. Your actions over the coming year will carry far more weight than historical events that fade with each passing month.

Build Credit History With Strategic Moves

If you have no credit history or very limited history, the path forward involves opening accounts strategically and using them responsibly. A secured credit card with a $500 deposit, used for small monthly purchases and paid off completely each month, builds credit without risk. Add yourself as an authorized user on someone else’s credit card with perfect payment history and low utilization; this tactic works because that account’s positive history transfers to your report without requiring you to qualify independently.

These moves take time to show results, but they establish the foundation you need for mortgage approval. Each account you open and manage responsibly strengthens your credit mix and demonstrates to lenders that you handle credit responsibly across different account types.

Final Thoughts

You now have a complete Canada credit score checklist to work through before you apply for any credit product. Correcting errors takes 30 to 60 days once the bureaus investigate, while reducing your utilization shows results within two to three months as credit card companies report updated balances monthly. Most people see a 50 to 100 point score increase within three months of lowering utilization and maintaining on-time payments, which opens mortgage doors that were previously closed.

That jump from 650 to 720 qualifies you for better rates on mortgages, car loans, and credit cards than you could access before. Start this checklist immediately if you’re targeting a mortgage application within a year, because every month of positive activity strengthens your position and compounds your gains. Compare offers from multiple lenders once your credit profile improves, since the difference between a 5.5% mortgage rate and a 5.0% rate saves you tens of thousands over 25 years.

We at Financial Canadian help you build a strong digital presence to support your financial goals. Whether you’re documenting your credit journey or managing your finances online, our web design service provides the tools and support you need for a seamless experience.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment