Payday loans trap thousands of Canadians in cycles of debt each year, with interest rates that can exceed 400% annually. At Financial Canadian, we’ve seen firsthand how borrowers struggle to escape this trap without a solid plan.

The good news is that payday loan repayment in Canada doesn’t have to feel impossible. This guide walks you through realistic strategies to break free from high-interest debt and rebuild your financial stability.

Understanding Payday Loan Costs and Why Canadians Turn to Them

How Payday Loans Work and Their True Cost

Payday loans operate on a deceptively simple model that masks their true cost. A lender provides you with cash upfront, typically between $300 and $1,500, and you repay the full amount plus fees by your next payday, usually within two weeks. In Ontario, the maximum fee is $14 per $100 borrowed, meaning a $300 loan costs roughly $42 in fees alone. This translates to an annual percentage rate near 400%.

Most Canadians don’t calculate the APR before borrowing, focusing instead on the immediate fee rather than the staggering annual cost. The regulations introduced on January 1, 2025, capped the maximum APR at 35% for loans in default, but standard payday loans still operate under the per-loan fee structure, which creates the astronomical rates. Lenders require either a post-dated cheque or pre-authorized debit from your account, giving them direct access to your funds on repayment day.

If your account lacks sufficient funds, you face a $20 dishonoured payment fee on top of the original loan cost, creating a cascade of charges that quickly spiral out of control. This fee structure means that missing a single payment can add hundreds of dollars to your total debt within weeks.

Why Canadians Turn to Payday Loans

Canadians turn to payday loans when traditional credit sources fail them or when emergencies demand immediate cash. Job loss, unexpected medical bills, car repairs, or missed rent payments force people to seek quick solutions without the time to apply for bank loans or credit cards. The approval process takes minutes rather than days, and lenders don’t care about your credit score, making payday loans accessible to people with poor credit histories.

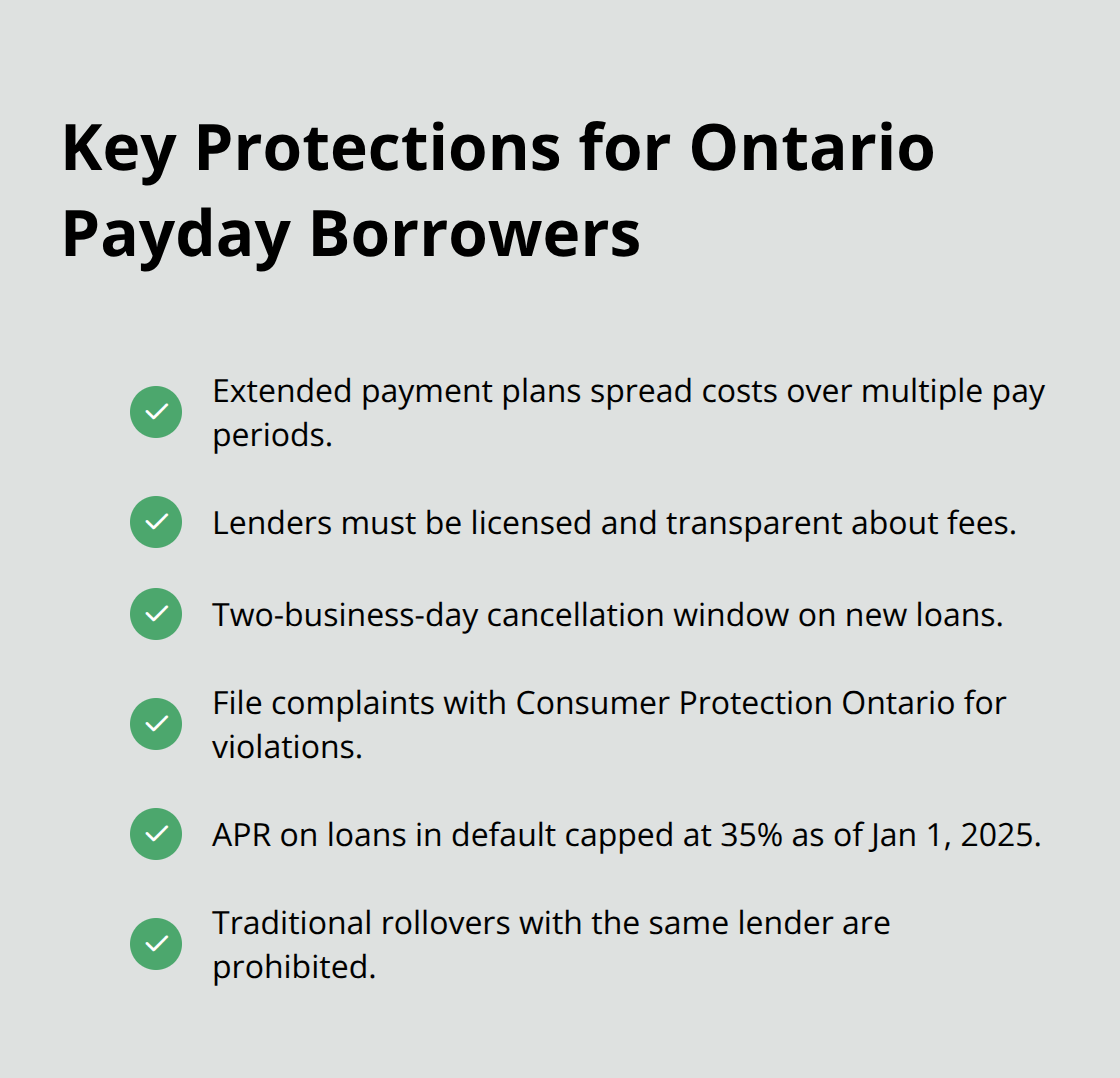

This accessibility creates the trap. About four in five loans are rolled over within 14 days, meaning borrowers can’t repay the full amount when it’s due and must borrow again, extending the debt cycle indefinitely. The Payday Loans Act in Ontario prohibits traditional rollovers with the same lender, but borrowers simply move to different lenders or take out extended payment plans, which spread costs across multiple pay periods.

The Extended Payment Plan Trap

Extended payment plans require equal installments across at least three pay periods for bi-weekly earners, with each payment capped at 35% of the loan plus borrowing costs. A $500 loan becomes a three-month commitment with accumulated fees that often exceed the original borrowed amount. The real damage occurs when borrowers realize they cannot escape without sacrificing essential expenses like groceries or utilities.

This cycle explains why so many Canadians struggle to break free from payday debt without a structured repayment strategy. Understanding these costs and traps is the first step toward building a realistic plan to escape this debt.

Building Your Payday Loan Repayment Plan

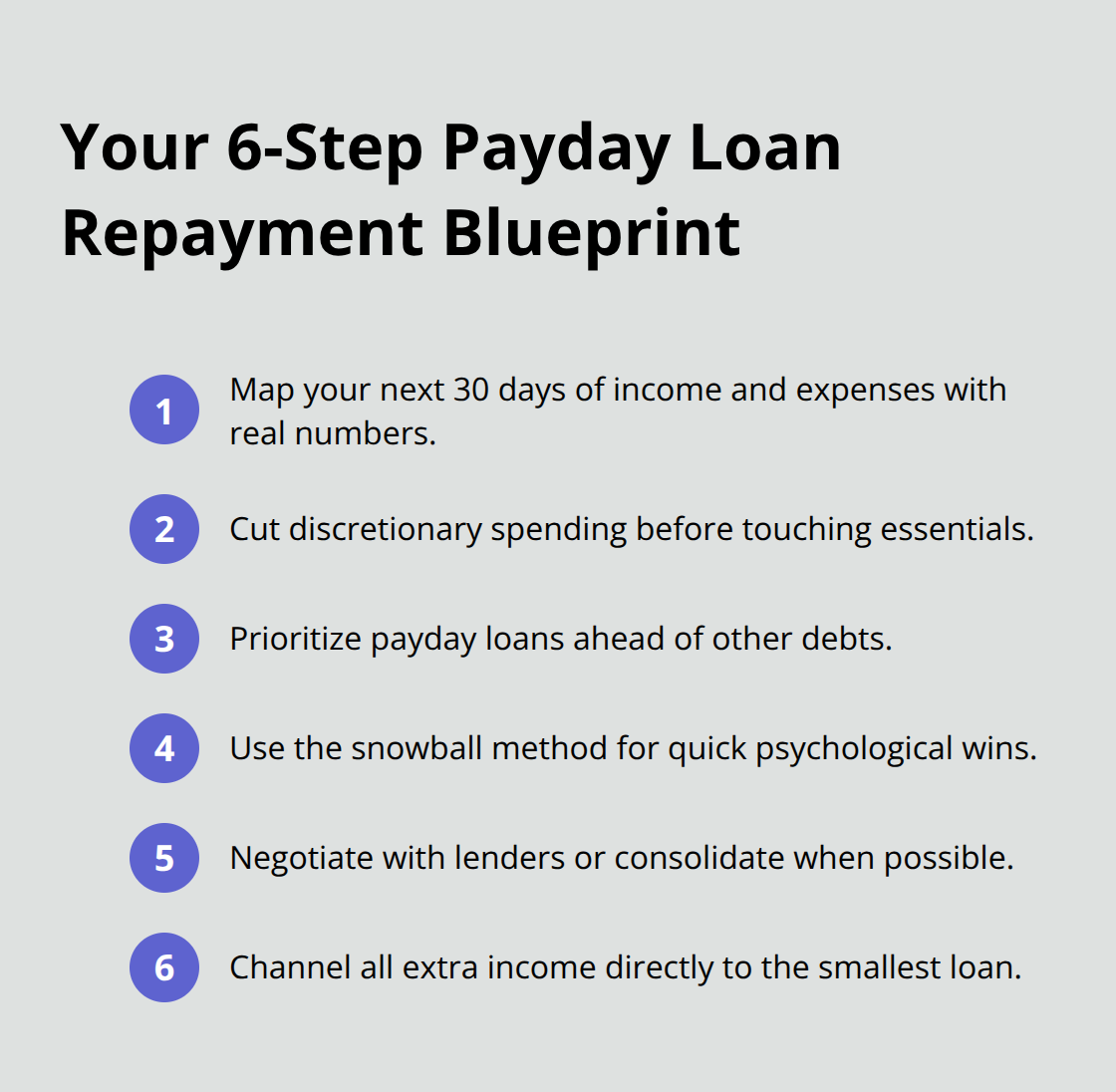

Map Out Your Real Cash Flow

List every dollar you earn and every dollar you spend over the next 30 days. Include your salary, side income, benefits, and fixed expenses like rent, utilities, groceries, and transportation. This honest assessment reveals how much cash you can realistically allocate to payday loan repayment without sacrificing necessities.

Most Canadians discover they have far less breathing room than they thought, which explains why payday loans felt necessary in the first place. The difference between this exercise and vague budgeting is that you work with actual numbers, not estimates. Once you see the real picture, you identify which expenses are truly fixed and which ones you can reduce.

Cut Discretionary Spending First

Eliminate streaming services, restaurant meals, and impulse purchases before you touch essential costs. This approach creates a buffer for payday loan payments without forcing you into further financial desperation. You’ll be surprised how much money accumulates when you stop these small leaks.

Prioritize Payday Loans Above Other Debts

Payday loans accumulate interest faster than credit cards or bank loans, so attack them first. If you carry multiple payday loans, target the smallest one while making minimum payments on the others. Paying off one loan completely gives you psychological momentum and frees up cash flow for the next loan.

Set a concrete repayment timeline, not a vague goal. If you have a $500 payday loan and can spare $150 monthly after essentials, you’ll pay it off in roughly four months plus fees. Write this date down and treat it like a non-negotiable appointment.

Negotiate or Consolidate Your Debt

Contact your lender directly and explain your situation before missing a payment. Many lenders prefer an extended payment plan over default because it guarantees eventual repayment. Ontario’s regulations require lenders to offer extended payment plans if you take three loans within 63 days, spreading repayment across multiple pay periods with capped installments.

If a lender refuses to work with you, explore debt consolidation through credit unions or nonprofit credit counseling agencies. A consolidation loan merges multiple payday debts into one payment at a lower interest rate, simplifying your repayment process and reducing total interest paid. Licensed Insolvency Trustees in Canada can also help structure a consumer proposal if payday debt has become unmanageable alongside other obligations.

Accelerate Your Payoff With Extra Income

The fastest way to escape payday debt is to increase the money you allocate toward repayment. Tax refunds, bonuses, or earnings from side work should go directly toward your smallest payday loan. Even an extra $50 monthly cuts months off your repayment timeline and saves hundreds in accumulated fees.

With your repayment plan in place, the next step involves choosing the right debt payoff method to maximize your progress and maintain momentum.

Accelerating Your Payday Loan Payoff

Choose the Right Debt Payoff Method

The debt snowball and debt avalanche methods offer two distinct frameworks for eliminating payday loans, though most Canadians apply them incorrectly or abandon them due to slow initial progress. The snowball method targets your smallest payday loan first, regardless of interest rate, and creates psychological wins that fuel momentum. The avalanche method attacks the highest-interest debt first, which minimizes total interest paid over time.

The snowball method works better for payday loans because the psychological boost of eliminating one loan within weeks keeps you committed when the debt feels overwhelming. A $300 payday loan paid off in four to six weeks provides tangible proof that your plan works, motivating you to attack the next loan. The avalanche method often takes longer to show results, and most people quit before experiencing that first victory.

Identify Hidden Money in Your Budget

Your real acceleration comes from identifying money you didn’t know you had. After mapping your cash flow, look for expenses that don’t align with your actual priorities. Restaurant spending, subscription services, and impulse online purchases typically consume $200 to $400 monthly for Canadians without providing lasting value. Redirecting even $150 monthly toward your smallest payday loan cuts your repayment timeline dramatically.

A $500 loan at $150 monthly disappears in roughly four months, freeing up that payment slot for your next loan. The compounding effect matters here: once the first loan vanishes, that $150 becomes available for loan number two, then three, accelerating your entire payoff schedule. This approach requires no sacrifice of necessities-only elimination of spending that doesn’t serve your financial goals.

Leverage Side Income for Faster Payoff

Side income offers the fastest route to freedom because it doesn’t require sacrificing necessities. Freelance work, gig economy jobs, or selling items you no longer use generates cash that goes entirely toward debt without touching your core budget. Even $100 weekly from side work eliminates a $500 payday loan in five weeks instead of four months, saving you hundreds in accumulated fees.

The advantage of side income lies in its separation from your essential budget. You don’t reduce groceries or utilities; instead, you add income that flows directly to payday loan elimination. This method maintains your financial stability while accelerating your escape from high-interest debt.

Final Thoughts

Payday loan repayment in Canada becomes manageable when you stop treating it as an impossible burden and start treating it as a solvable problem with a timeline. Your realistic plan begins with mapping actual cash flow, cutting discretionary spending, and targeting your smallest loan first for quick wins that fuel momentum. Prioritizing payday loans above other debts, negotiating with lenders, and exploring consolidation options give you control over a situation that initially felt hopeless.

Ontario’s regulations protect you in ways many borrowers don’t realize. Extended payment plans spread costs across multiple pay periods, lenders must be licensed and transparent about fees, and you have a two-business-day cancellation window on new loans. If a lender violates these rules through excessive contact or repeated unauthorized withdrawals, you can file a complaint with Consumer Protection Ontario.

Understanding these protections prevents you from being exploited further while you execute your repayment plan.

Resources exist to support your journey toward financial stability. Nonprofit credit counseling agencies provide free budgeting advice and debt management plans that reduce monthly payments, while Licensed Insolvency Trustees help structure consumer proposals if payday debt has become unmanageable alongside other obligations. Once you’ve eliminated your payday debt, redirect that monthly payment toward an emergency fund covering one month of essential expenses, and explore additional financial resources to prevent future emergencies from forcing you back into high-interest borrowing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment