Choosing the right mortgage lender can save you thousands of dollars over the life of your loan. The mortgage lenders Canada comparison process doesn’t have to be overwhelming-we at Financial Canadian have created this guide to help you navigate your options.

Banks, credit unions, and private lenders each offer different advantages. Understanding what sets them apart is the first step toward making a decision that fits your financial situation.

Who Lends Mortgages in Canada

The Big Five Banks and Traditional Lenders

Canada’s mortgage market is dominated by the Big Five banks, which hold 72% of all outstanding mortgages. However, this concentration masks a fragmented reality: chartered banks contribute about 80% of new mortgage originations, while non-bank lenders account for roughly 19%, giving you real alternatives. Banks like RBC, TD, and BMO offer standardized products with competitive advertised rates, but they apply the federal mortgage stress test to all uninsured renewals and new mortgages, which can restrict your borrowing power.

Credit Unions: A Different Model

Credit unions present a fundamentally different approach. There are about 700 credit unions across Canada, and they operate as member-owned, not-for-profit institutions that often hold mortgages in-house. This structure allows them to be more flexible on approval criteria, making it easier for self-employed borrowers or those with non-traditional income to qualify. Credit unions typically don’t apply the federal stress test, which can mean the difference between qualifying and being rejected. A 0.25% rate difference on a $500,000 mortgage over 25 years translates to over $20,000 in savings, and credit unions frequently negotiate lower rates than banks because they don’t carry the same overhead costs. They also tend to charge fewer fees and offer more personalized service with deeper local market knowledge.

Private Lenders and Mortgage Brokers

Private lenders and mortgage finance companies fill gaps that banks and credit unions won’t touch-borrowers with poor credit, self-employed individuals without traditional documentation, or those needing bridge financing. These lenders charge higher rates, sometimes 2–4% above prime, but they move faster and ask fewer questions. Mortgage brokers sit between you and all three types of lenders, accessing a wider pool than you could alone. Brokers receive payment from lenders, though some offer rate buy-downs by sacrificing part of their commission, effectively passing savings to you. The real advantage of using a broker is speed and leverage: they can shop your application across dozens of lenders simultaneously and negotiate terms on your behalf.

Making Your Choice

When comparing lenders, rate alone isn’t everything. Banks offer strong digital platforms and national accessibility but may be rigid on lending criteria. Credit unions offer flexibility and community reinvestment but smaller geographic footprints. Private lenders offer speed but at a premium cost. Your choice depends on whether you prioritize the lowest rate, approval flexibility, or fastest closing-and understanding these trade-offs will help you evaluate the specific factors that matter most to your situation.

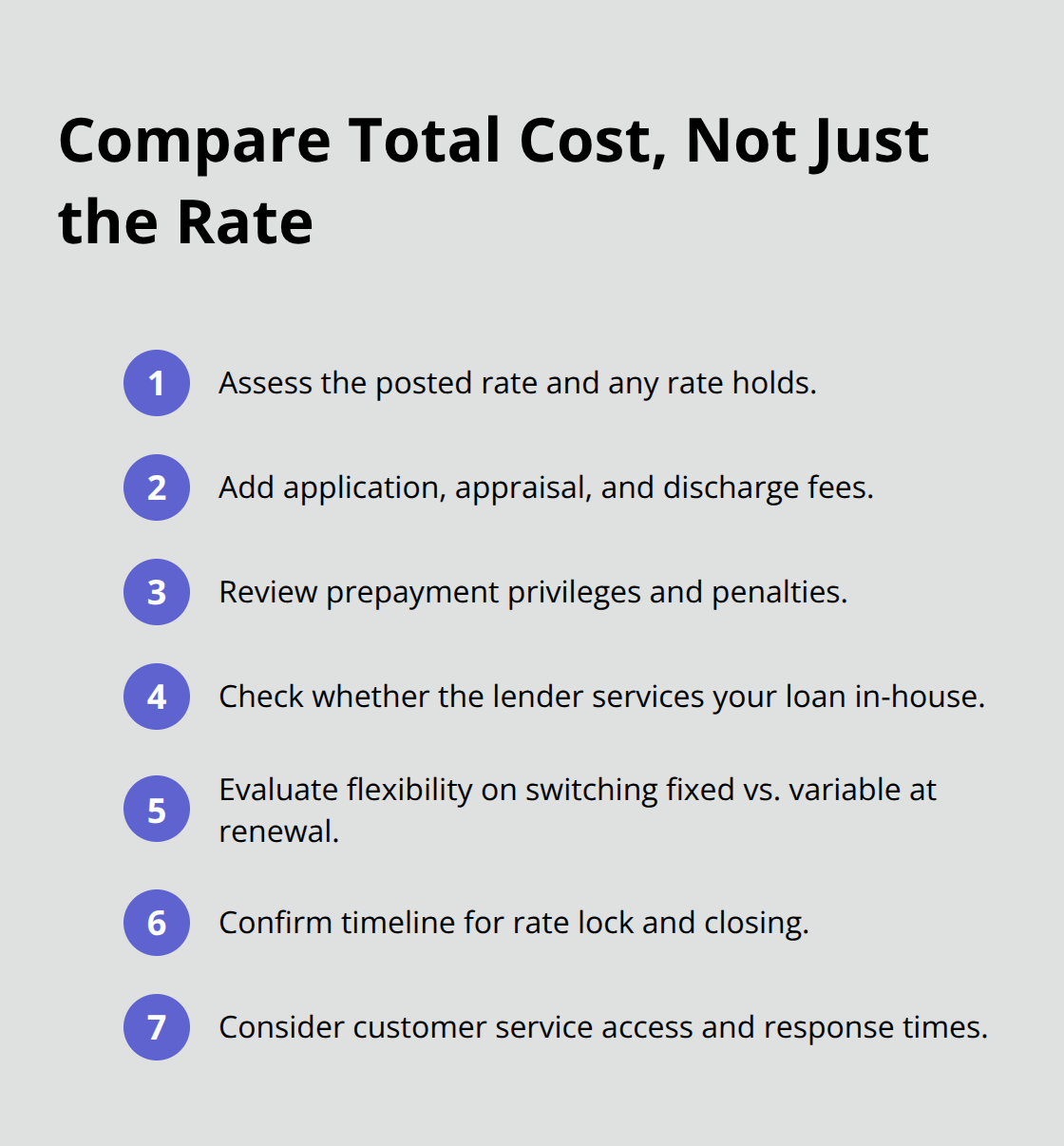

What to Actually Compare Beyond the Interest Rate

Interest rates grab attention, but they’re only one piece of the puzzle. As of March 2026, the lowest insured 5-year fixed rate sits at 3.64% while conventional 5-year fixed rates reach 3.79%, according to WOWA.ca’s daily rate tracking across fifty-plus lenders. However, a 0.25% difference on a $500,000 mortgage costs you over $20,000 across a 25-year amortization. This means that while rate shopping matters, the fees attached to that rate often matter more.

Banks Charge More in Fees Than Credit Unions

Banks typically advertise competitive rates but layer on higher fees-application fees ranging from $300 to $500, appraisal fees of $250 to $400, and discharge fees when you renew or switch. Credit unions charge significantly less because their not-for-profit structure eliminates the pressure to maximize fee revenue. When you compare offers, calculate your total cost, not just the posted rate. A lender quoting 3.50% with $2,000 in fees costs more than one quoting 3.75% with $500 in fees over the life of your mortgage.

Rate Locks Create Risk and Opportunity

Most lenders offer rate holds between 15 and 60 days, but this window creates real risk. Markets move fast-if rates drop after you lock in, you stay locked out. If they rise, you gain protection but miss better options. Credit unions typically offer more flexibility here, allowing you to switch between fixed and variable rates at renewal without penalty, while banks enforce stricter rules.

OSFI changed the stress test requirement for uninsured mortgage renewals with a new lender starting November 2024, which means you can now switch lenders at renewal with less financial pain. The national prime rate dropped from 4.70% in September 2025 to 4.45% in March 2026, showing how quickly conditions shift. If you hold a variable mortgage tied to prime, those swings directly hit your payments.

Ask each lender explicitly about their prepayment options-some allow you to pay down your mortgage penalty-free, others charge steep fees. This flexibility matters most if your income or life circumstances change.

Service Quality Separates Lenders When Problems Arise

Banks offer superior digital platforms and 24/7 phone support, but you may wait hours to reach a human who understands your specific situation. Credit unions provide faster callback times and relationship-based service where staff know your file personally. The difference becomes obvious during renewal or if you need to modify your mortgage. Private lenders move fastest but offer minimal ongoing support.

A 4.9-star rating from over 11,000 reviews signals strong service, but ratings don’t reveal response times or whether the lender actually holds your mortgage in-house or sells it to a servicer. Ask directly: who services your loan after closing, and how do you contact them? This determines whether you’ll spend 15 minutes resolving an issue or three weeks navigating a call center.

Local credit unions reinvest profits back into communities, which translates to staff incentives to solve problems rather than process applications quickly and move on. If you’re self-employed or have non-traditional income, this relationship-driven approach at credit unions often means the difference between approval and rejection, since staff can exercise discretion rather than rely on algorithmic decisions. Your next step involves assessing which lender type aligns with your financial profile and priorities.

Finding Your Ideal Lender Match

Match Your Situation to the Right Lender Type

Start by listing what matters most to you, then eliminate lenders that don’t fit. If you’re self-employed with variable income, credit unions immediately become stronger candidates because they skip the federal stress test and exercise human judgment on your application. If you need closing within two weeks, private lenders win despite higher rates. If you want the lowest possible rate and can document steady W-2 income, banks and brokers compete hardest on pricing. This clarity prevents wasting time on lenders that won’t serve your situation.

Self-employed borrowers should contact credit unions first rather than banks, since credit unions typically approve non-traditional income documentation that banks reject outright. The stress test exemption alone can mean qualifying for $50,000 to $100,000 more in mortgage debt at credit unions compared to banks.

Understand How Your Credit Score Affects Your Options

Your credit score matters significantly-scores above 700 unlock the best rates from all lenders, while scores between 620 and 680 push you toward credit unions or private lenders willing to work with imperfect credit. Pull your credit report from Equifax or TransUnion before approaching any lender so you know exactly what they’ll see and can address errors beforehand. This step takes 15 minutes and prevents surprises during the approval process.

Gather Multiple Pre-Approvals Within Your 45-Day Window

Pre-approval is non-negotiable, but the process carries real costs and timing constraints. A hard credit inquiry from pre-approval drops your score by a few points, but you have a 45-day window to gather multiple pre-approvals without additional score damage-the credit bureaus treat all inquiries within that window as a single inquiry. This means you should apply to three to five lenders simultaneously rather than sequentially.

Mortgage brokers handle this automatically, submitting your application to a dozen lenders at once and returning with competing offers. Request pre-approval letters that specify the rate, term length, and any conditions attached, then compare the total cost including fees, not just the rate itself. A broker charging $1,500 in fees but securing a 3.50% rate may cost less overall than a bank charging $500 in fees at 3.75%.

Ask each lender whether their quoted rate includes a rate hold and for how many days-60 days provides more breathing room than 15 days when coordinating inspections and appraisals.

Negotiate From a Position of Strength

Once you receive multiple offers, you can negotiate. Banks and brokers will match competing rates if you present them with proof, sometimes dropping fees by 10 to 25 percent rather than lose your business. Credit unions negotiate more flexibly on terms like prepayment penalties and rate lock periods (which determine how long your rate stays locked before closing). Private lenders rarely negotiate on rate but sometimes adjust closing timelines or accept lower documentation standards.

The key is having leverage-multiple offers create competition, and competition creates flexibility. A lender that sees three competing offers on your file suddenly becomes willing to move on price, fees, or terms. This negotiation phase typically lasts one to two weeks and directly impacts your total mortgage cost over 25 years.

Final Thoughts

The mortgage lenders Canada comparison process comes down to matching your financial situation with the lender type that serves it best. Banks dominate the market with 72% of outstanding mortgages and offer strong digital platforms, but their standardized approach and stress test requirements limit flexibility for self-employed borrowers or those with non-traditional income. Credit unions, operating across 700 locations nationwide, provide the opposite trade-off: lower fees, exemption from federal stress tests, and approval flexibility that banks won’t match, though with smaller geographic footprints.

Your next steps are straightforward. First, identify which lender type aligns with your priorities-lowest rate, approval flexibility, or fastest closing. Second, gather pre-approvals from three to five lenders within your 45-day credit inquiry window, comparing total costs including fees rather than rates alone. A 0.25% rate difference on a $500,000 mortgage costs over $20,000 across 25 years, but fees and prepayment penalties often matter more than the advertised rate itself.

Resources to guide your decision include rate comparison sites tracking daily updates across fifty-plus lenders and mortgage brokers who submit applications simultaneously to multiple lenders. Start your mortgage lender search today by pulling your credit report, listing your priorities, and requesting pre-approvals from lenders matching your situation. We at Financial Canadian recommend building a strong digital foundation for your financial planning, and our comprehensive web design service offers responsive designs and SEO best practices to help you research and compare lenders effectively online.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment