Mortgage rates in Canada are shifting, and most homeowners don’t know how to navigate the options available to them. The difference between a fixed-rate and variable-rate mortgage can cost you tens of thousands of dollars over the life of your loan.

At Financial Canadian, we’ve created this guide to help you understand home loan rates Canada and make decisions that actually work for your financial situation. Whether you’re a first-time buyer or refinancing, the strategies in this post will show you how to secure better terms.

Where Canadian Mortgage Rates Stand Right Now

How the Bank of Canada’s Policy Rate Shapes Your Mortgage

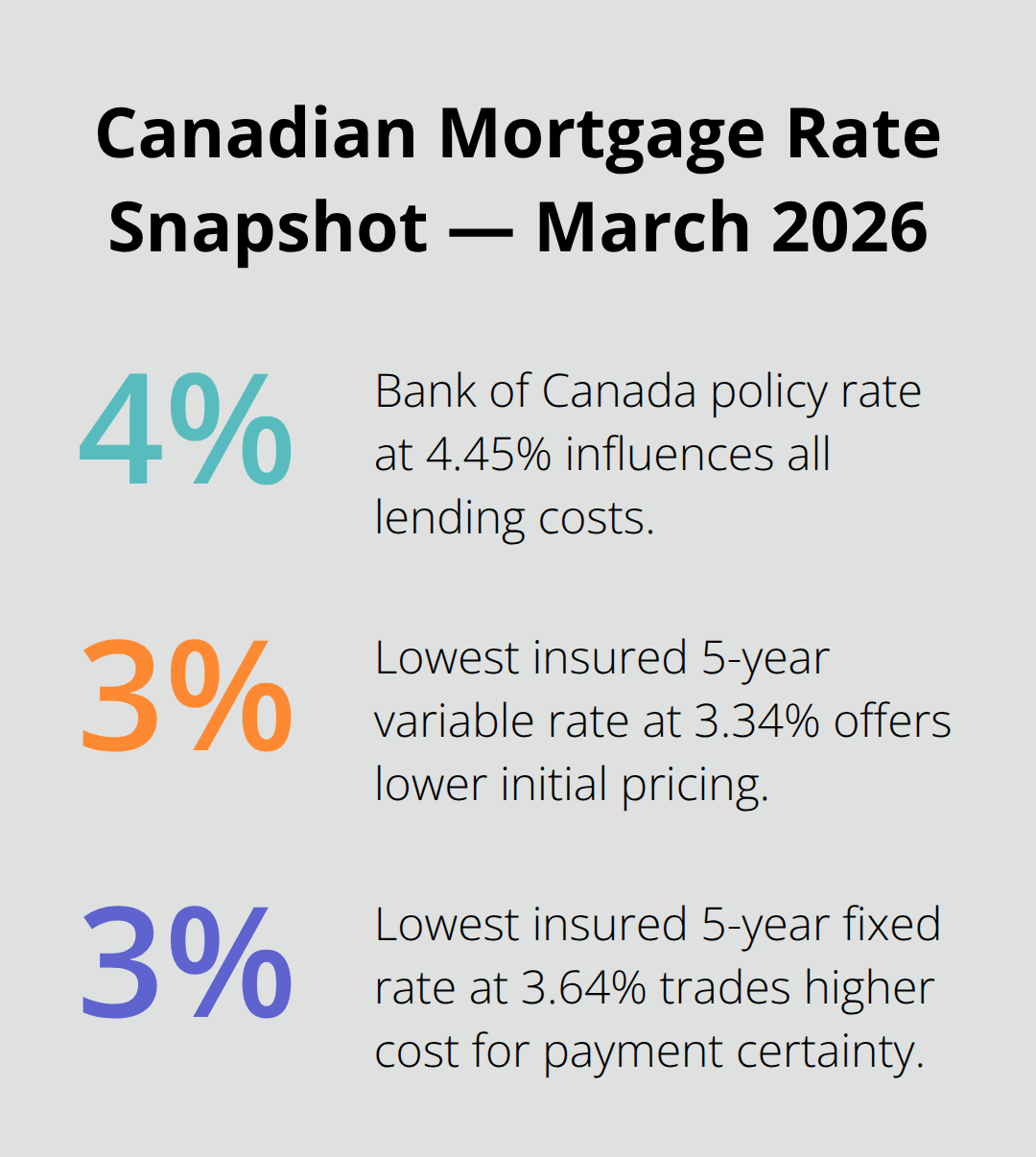

The Bank of Canada’s policy rate sits at 4.45% as of March 2026, and this single number ripples through every mortgage offer you’ll see. When the central bank adjusts its rate, variable-rate mortgages move almost immediately, while fixed rates respond to bond market expectations rather than direct policy changes. This distinction matters enormously because it determines whether your payment stays locked or fluctuates.

The lowest insured 5-year variable rate available is 3.34%, which undercuts the lowest insured 5-year fixed rate of 3.64% by 30 basis points. That gap exists because lenders price variable mortgages lower to offset the risk that rates could climb, and borrowers accept that uncertainty for immediate savings.

Fixed vs. Variable: The Rate-Setting Bet You’re Making

If you lock into a fixed rate today, you’re betting that rates won’t fall significantly before your term ends, while variable-rate borrowers are betting the opposite. Fixed rates protect you from payment shock if the Bank of Canada raises rates further, but they also lock you into higher costs if rates drop. Variable rates offer lower initial pricing, but your payment can increase if the policy rate climbs. The choice depends on your risk tolerance and financial flexibility rather than predicting where rates will go.

Why Your Term Length and Property Type Matter More Than Location

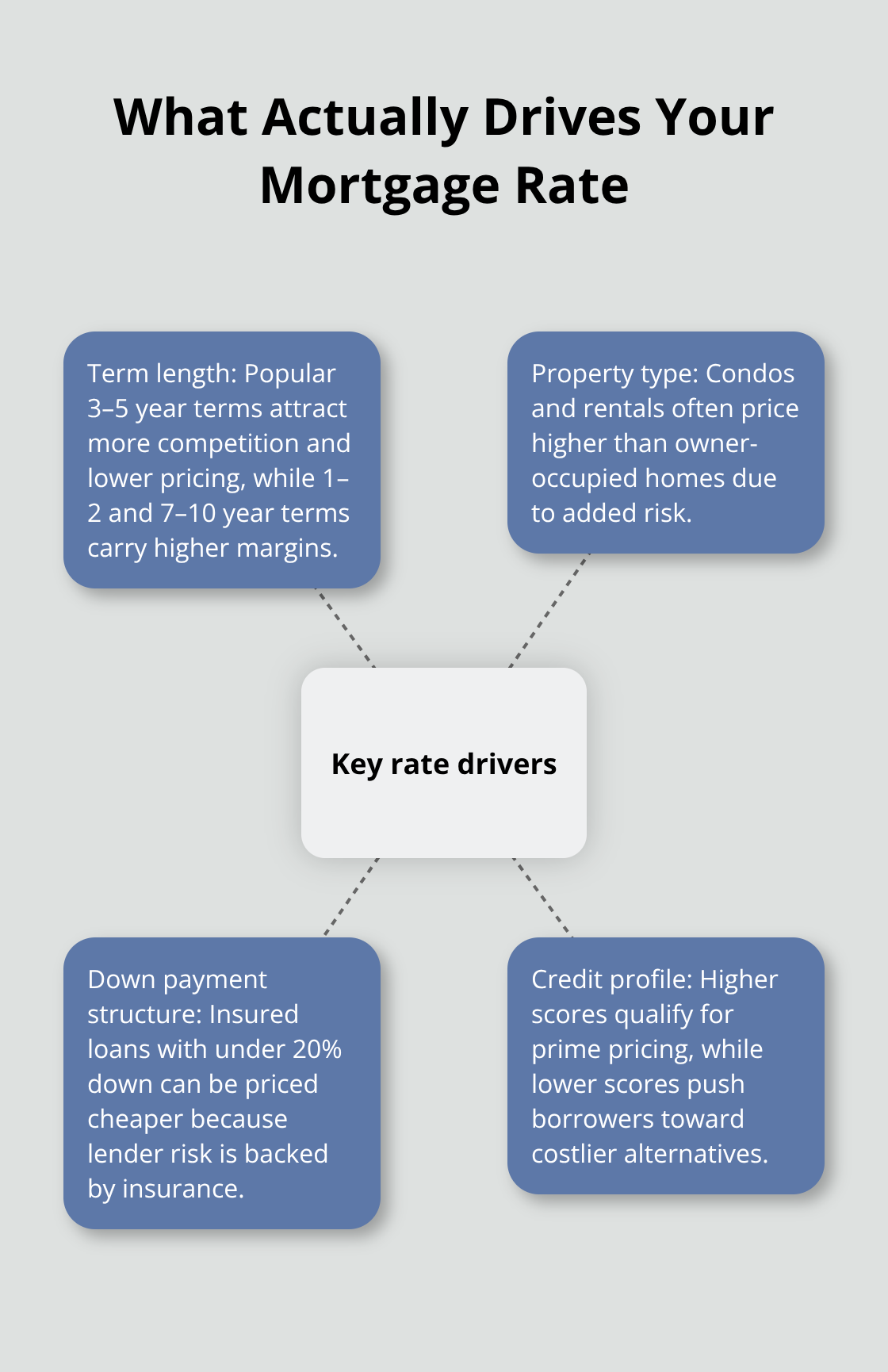

Regional differences in Canadian mortgage pricing are real but often overstated. While some provinces experience slightly higher rates due to market conditions and lender competition, the spread between regions typically ranges from 5 to 15 basis points rather than dramatic swings. Condos and rental properties face higher rates consistently, with condos seeing modest increases due to volatility concerns and rental properties adding 10 to 25 basis points above owner-occupied homes.

The most competitive rates exist in the 3 to 5-year term window, where lenders bundle multiple products and attract volume; shorter terms like 1 to 2 years and longer terms from 7 to 10 years carry higher margins because they’re less frequently shopped and harder to predict. Insured mortgages with down payments under 20% offer rates 10 to 25 basis points cheaper than uninsured mortgages because the insurance backs the lender’s risk, which is why first-time buyers with modest down payments often secure better pricing than well-capitalized borrowers.

What Actually Drives Your Rate

Your rate depends on term length, property type, down payment structure, and credit profile far more than your postal code. A borrower with a 720+ credit score, a 15% down payment on a primary residence, and a 5-year fixed term will see dramatically different pricing than someone with a 650 credit score, a 5% down payment on a condo, and a 2-year term. These factors compound, so improving even one of them can shift your offer meaningfully.

The practical path forward involves understanding which levers you can pull before you apply, and that starts with knowing exactly what lenders evaluate when they price your mortgage.

Choosing Between Fixed, Variable, and Hybrid Mortgages

Fixed-Rate Mortgages: Predictability at a Premium

Fixed-rate mortgages lock your interest rate for the entire term, so your payment stays identical whether the Bank of Canada raises rates to 6% or drops them to 2%. This certainty appeals to borrowers who want predictable budgeting and protection from payment shock, but you pay for that stability through higher initial rates. You sacrifice flexibility for peace of mind, which makes sense if a rate jump would strain your budget or if you’re financing near your maximum affordability. Fixed rates eliminate payment stress despite the higher cost, making them the safer choice for households without substantial financial buffers.

Variable-Rate Mortgages: Lower Costs With Built-In Risk

Variable-rate mortgages track the Bank of Canada’s policy rate, currently sitting at 4.45% as of March 2026, so your payment fluctuates as the central bank adjusts its benchmark. The lowest insured 5-year variable rate is 3.34%, compared to 3.64% for the equivalent fixed option, giving variable borrowers an immediate 30 basis point advantage. That gap reflects lender pricing strategy: they offer lower variable rates because they transfer rate risk to you. If you have emergency savings covering six months of expenses and your housing costs stay below 39% of gross income, variable mortgages can save you thousands if rates decline or stay flat. The real mistake is choosing based on rate predictions rather than your actual financial resilience. Most borrowers overestimate their ability to absorb payment increases, which is why variable mortgages work best for households with genuine financial flexibility.

Term Length: The Overlooked Rate Driver

The 3 to 5-year window offers the most competitive rates because lenders compete fiercely for volume in this popular range, while 1 to 2-year terms and 7 to 10-year terms carry higher margins because fewer borrowers shop them and lenders face greater uncertainty. A 5-year fixed at 3.64% insured will cost significantly less than a 2-year fixed at 4.29% even though the shorter term sounds cheaper, because you’re comparing rates across different competitive landscapes. Term length creates pricing dynamics that most borrowers ignore, yet this factor often matters more than the headline rate itself.

Hybrid and Alternative Mortgages: Specialized Solutions

Hybrid mortgages split fixed and variable components, allowing you to hedge against rate movements while maintaining some payment certainty. You might place 60% of your mortgage on a 5-year fixed rate and 40% on a variable rate, so payment increases affect only the variable portion if rates climb. This strategy works best when you expect rates to rise modestly rather than spike dramatically, and it requires comfort managing two separate accounts.

Alternative lenders and private mortgages enter the picture when traditional banks decline your application due to credit challenges, self-employment income, or non-standard properties like new builds or condos with high vacancy rates. These mortgages cost 100 to 200 basis points more than prime rates, plus broker fees around 1%, making them expensive bridges rather than long-term solutions. If a private lender is your only option, use that time to rebuild credit or improve your income documentation so you can switch to traditional financing at your next renewal and recapture thousands in annual savings.

Understanding which mortgage structure fits your situation sets the stage for the next critical step: actually securing the best rate available to you. Your rate depends on factors you control-credit score, down payment size, and term selection-and knowing how to optimize these levers before you apply separates borrowers who get premium pricing from those who overpay.

How to Lock in the Best Rate Before You Apply

Build Your Credit Score to Access Prime Rates

Your credit score determines whether lenders view you as prime or non-prime, and that classification alone can shift your rate by 100 to 200 basis points. A score of 680 or more opens access to the best rates with traditional lenders, while scores below 680 push you toward alternative lenders charging dramatically more. If your score sits below 680, spend 60 to 90 days before applying to pay down existing debt, ensure all bills arrive on time, and correct errors on your credit report through Equifax or TransUnion.

Paying down revolving debt like credit cards matters more than paying off installment loans, since credit utilization directly impacts your score. A borrower who reduces credit card balances from 80% of their limit to 30% can see a 30 to 50 point improvement within one or two reporting cycles. The math here is stark: improving your score can save thousands over a mortgage term.

Leverage Your Down Payment Size Strategically

Your down payment size compounds credit advantages because insured mortgages with less than 20% down offer 10 to 25 basis points cheaper rates than uninsured options when your credit is strong. A first-time buyer with a strong credit score and a 15% down payment will see dramatically better pricing than someone with a higher score and only a 5% down payment, because lenders price for both credit and insurance risk simultaneously. This means you can sometimes offset a lower credit score with a larger down payment, or vice versa, depending on your financial situation.

Shop Multiple Lenders to Uncover Hidden Savings

Comparing offers across multiple lenders reveals pricing gaps that most borrowers never see. Rate comparison sites collect mortgage rates three times daily from 50 or more lenders, sorting non-sponsored rates from lowest to highest so you can benchmark current offers without calling dozens of banks individually. Shopping across at least five lenders takes roughly two hours and typically uncovers 15 to 30 basis points of variation for identical mortgage profiles, which translates to significant five-year savings.

Mortgage brokers access a wider lender network than any single bank, and they negotiate on your behalf, sometimes securing better terms that you cannot access directly. Brokers receive compensation from lenders for prime mortgages, so using one costs you nothing if your application qualifies for standard lending. However, verify that your broker compared at least eight to ten lenders and didn’t simply place you with whoever offers the highest commission.

Evaluate Pre-Approval Offers With Skepticism

Pre-approval offers should never be accepted at face value because they lock your rate for only 120 to 180 days, and longer guarantees typically come with higher surcharges that offset apparent savings. A lender offering a 140-day rate hold at a lower advertised rate might actually cost more than a competitor providing a 120-day hold at a slightly higher rate once you factor in the surcharge. Negotiate the rate hold length based on your actual closing timeline rather than accepting the default, and ask specifically whether the rate includes any buy-down costs or surcharges.

Choose Your Term Length to Maximize Competitive Pressure

Term length drives pricing more than most borrowers realize, and selecting a 3 to 5-year fixed term puts you in the most competitive window where lenders fight for volume, whereas 1 to 2-year terms and 7 to 10-year terms carry higher margins because fewer borrowers shop them. Your application strength determines how much room you have to negotiate, so a borrower with a strong credit score, substantial down payment, and stable employment can push for better terms or rate reductions, while someone with a lower score and minimal down payment has less leverage and should focus on locking in whatever the best available offer is.

Final Thoughts

The path to securing better home loan rates Canada comes down to controlling what you can control before you apply. Your credit score, down payment size, term selection, and mortgage type determine your pricing far more than economic predictions or rate forecasts. A borrower who improves their credit to 720 or higher, saves for a 15 percent down payment, and selects a competitive 5-year term will access dramatically better rates than someone waiting for the perfect market moment while carrying a 650 credit score and minimal savings.

Shopping across multiple lenders remains non-negotiable because rate variation between lenders routinely exceeds 20 basis points for identical profiles. That difference compounds to thousands of dollars over five years, yet most borrowers accept the first offer they receive. Mortgage brokers can accelerate this process by accessing wider lender networks and negotiating on your behalf at no cost for prime mortgages, but verify they have compared at least eight to ten options rather than placing you with whoever offers the highest commission.

Your next step depends on your current situation. If your credit score sits below 680, allocate 60 to 90 days to pay down revolving debt and correct any errors on your credit report before applying. Visit Financial Canadian to explore resources that support your financial planning and mortgage decisions throughout your journey.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment