An unsecured personal loan in Canada can be a fast way to access cash without putting your home or car at risk. At Financial Canadian, we’ve seen borrowers use these loans for everything from debt consolidation to home renovations.

But not every unsecured personal loan makes financial sense. This guide walks you through the real advantages, the hidden costs, and the strategies that actually work.

What Unsecured Personal Loans Actually Are

An unsecured personal loan is money a lender gives you without requiring you to pledge any asset as collateral. You don’t put your home, car, or savings on the line. The lender’s security comes entirely from your promise to repay and your creditworthiness. This means the approval process moves faster than secured loans-many lenders deliver decisions within minutes or a single business day.

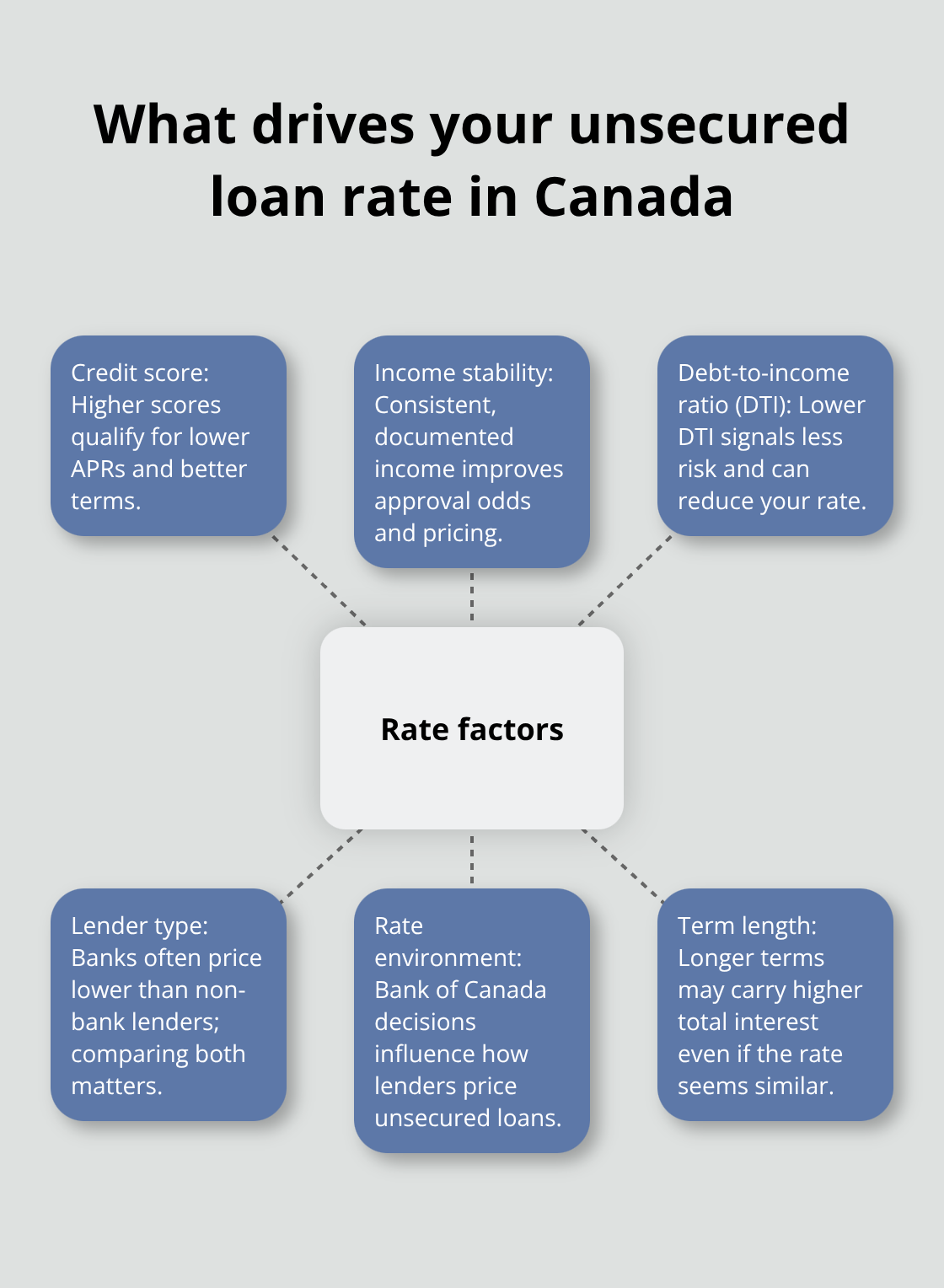

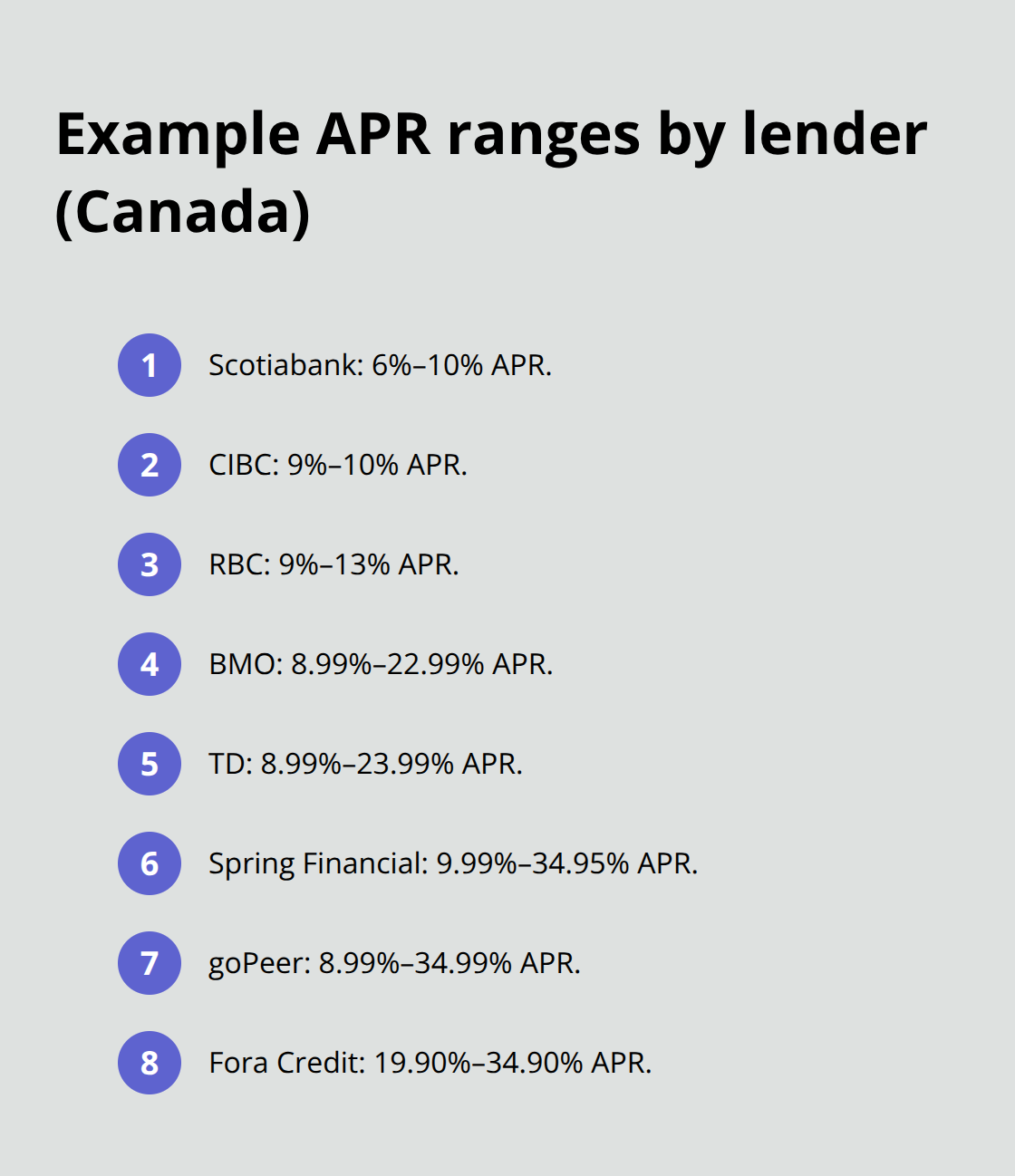

You can borrow anywhere from a few hundred dollars up to around $35,000 depending on the lender, with repayment terms typically ranging from six months to five years. The Bank of Canada held the overnight rate at 2.25% in January 2026, which influences how banks price these loans. Unsecured personal loan rates in Canada currently span from about 6% to 35% APR, though major banks like Scotiabank advertise starting rates around 6% to 10% for well-qualified borrowers, while non-bank lenders like Mogo charge 9.90% to 46.96%. Your actual rate depends heavily on your credit score, income stability, and debt-to-income ratio.

How They Differ from Secured Loans

The fundamental difference is collateral. Secured loans like mortgages or home equity lines of credit require you to pledge property or assets, which typically results in lower interest rates-often in the single digits. If you miss payments on a secured loan, the lender can seize your home or vehicle. Unsecured loans carry higher rates because the lender has no asset to recover if you default, but you also face no risk of losing your home or car. In Canada, secured loans typically offer rates in the single digits while unsecured loans often exceed 20%. The trade-off is clear: unsecured loans cost more but protect your assets. Secured loans may have longer repayment terms, which sounds appealing until you realize you’re paying more total interest over the life of the loan. Most Canadian borrowers choose unsecured loans for smaller amounts where the convenience and speed outweigh the higher cost. Non-bank lenders often price higher than banks, so comparing across both categories matters significantly when you shop for rates.

Major Lenders Offering Unsecured Loans

Canada’s unsecured loan market includes major banks and specialized non-bank lenders. The big five banks-Scotiabank, BMO, TD, CIBC, and RBC-all offer personal loans with varying rates and terms. Scotiabank starts at 6% to 10%, CIBC at 9% to 10%, and RBC at 9% to 13%, according to Ratehub data. BMO and TD both range from 8.99% to 22.99% and 8.99% to 23.99% respectively, showing substantial variance even among major institutions. Non-bank lenders like Spring Financial (9.99% to 34.95%), goPeer (8.99% to 34.99%), and Fora Credit (19.90% to 34.90%) fill gaps for borrowers with lower credit scores or non-traditional income. Credit unions also offer unsecured loans, often at competitive rates. You can also access peer-to-peer lending platforms, though these require careful vetting. The application process typically starts with comparing lenders, verifying your eligibility, and gathering documents like pay stubs and tax returns.

Most lenders check your credit score, income, and debt-to-income ratio-typically requiring a minimum income around $17,000 gross annually and a credit score around 600 or higher for reasonable rates. Your debt-to-income ratio matters more than most borrowers realize; keeping it below 30% significantly improves your approval odds and rate quotes. Understanding these lender differences and eligibility requirements sets the foundation for making a smart choice-which is why the next section walks you through the real advantages and hidden costs you need to weigh before applying.

Pros and Cons of Unsecured Personal Loans

Speed and Flexibility Come at a Price

Unsecured personal loans solve a genuine problem for Canadian borrowers who need cash fast without risking their home or vehicle. Most lenders approve applications within minutes or a single business day, which beats the weeks required for secured loans or mortgage refinancing. You also gain flexibility in how you use the money-debt consolidation, renovations, medical expenses, or any other purpose. This flexibility combined with no collateral requirement makes unsecured loans genuinely useful when you face time-sensitive financial needs.

However, the cost structure reveals why borrowing this way demands serious scrutiny. Unsecured personal loan rates in Canada vary significantly depending on your credit profile and lender. For comparison, a secured home equity line of credit typically costs far less because the lender’s risk is lower. On a $5,000 loan at 15% APR over three years, you’ll pay roughly $1,196 in interest alone. That same $5,000 borrowed through a home equity line of credit at 7% APR costs only $546 in interest-meaning you pay double for the convenience of an unsecured loan. Origination fees, which range from 0.5% to 8% of your loan amount, add another layer of cost that many borrowers overlook until they see the final amount disbursed.

When an Unsecured Loan Actually Makes Sense

An unsecured personal loan makes financial sense only when the alternative is worse. If you carry high-interest credit card debt at 19% to 21% APR and can qualify for an unsecured personal loan at 12% to 14%, consolidating that debt into a single loan payment reduces your total interest costs and simplifies repayment. This works because you pay less to borrow than you currently do. However, consolidation only works if you stop using credit cards afterward-otherwise you simply add new debt on top of existing obligations.

Unsecured loans also make sense when you need funds urgently and lack time to arrange a secured option. A home renovation project on a deadline or unexpected vehicle repair that affects your income-earning ability can justify the higher cost of speed. The critical mistake we see repeatedly is borrowers treating unsecured loans as a solution to underlying spending problems. If you lack an emergency fund and regularly run short before payday, a personal loan won’t fix that pattern-it will trap you in a debt cycle.

Assess Your Cash Flow Before You Apply

Calculate whether your monthly cash flow can comfortably absorb the loan payment without cutting essential expenses. If your debt-to-income ratio is already above 44% of your gross income, adding another monthly payment typically worsens your financial position rather than improving it. Your actual ability to repay matters far more than the advertised interest rate. A low rate on a loan you can’t afford to repay creates far more damage than a higher rate on a loan that fits your budget.

Understanding these trade-offs positions you to make the right choice for your situation. The next section walks you through the specific strategies that help you qualify for better rates and compare offers that actually work for your financial picture.

Best Practices for Getting and Managing Unsecured Personal Loans

Strengthen Your Financial Profile Before You Apply

Your credit score matters, but it’s not the only lever you can pull before applying for an unsecured personal loan. Lenders evaluate your entire financial picture, and understanding what they’re looking at gives you real control over the offers you receive. A credit score around 600 or higher typically qualifies you for reasonable rates, but scores above 700 unlock significantly better pricing. Check your credit report with Equifax Canada or TransUnion Canada before applying to catch errors that could artificially lower your score.

Your debt-to-income ratio directly influences approval odds and rate quotes, making it more important than most borrowers realize. Try to use less than 30% of your available credit before applying for a new loan. For example, if you carry $8,000 in credit card debt at 21% APR and earn $50,000 annually, your DTI is roughly 19%, which puts you in a strong position. Reduce that debt to $4,000, and lenders see you as significantly lower risk.

Lenders also want to see stable income and employment history, so avoid job changes within 90 days of applying if possible. Document your income with recent pay stubs and tax returns because self-employed borrowers face stricter scrutiny and may need two years of tax documentation. When you apply, consider using Ratehub’s LoanFinder tool, which shows personalized offers in about 60 seconds without a hard credit check or requiring a SIN.

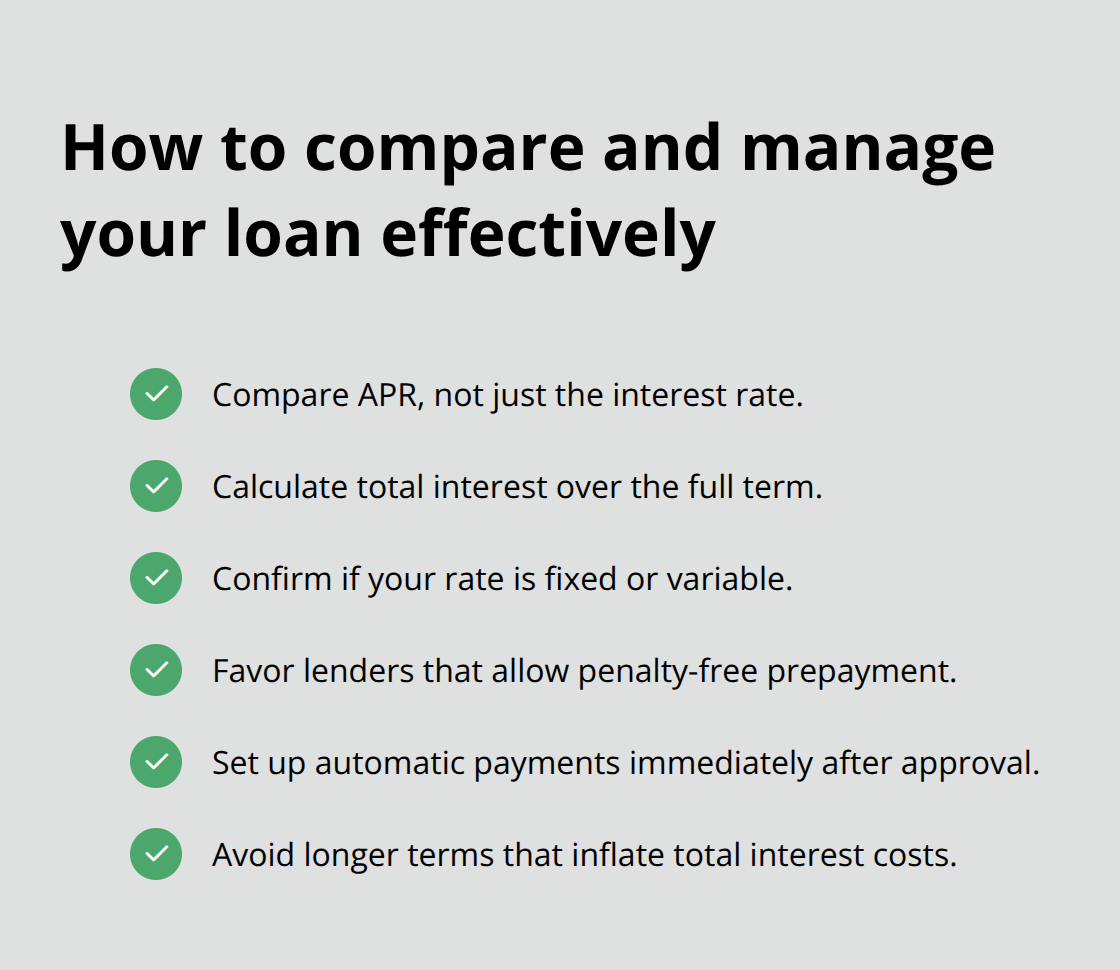

Compare Offers Using APR, Not Just Interest Rates

APR tells the real story because it includes the interest you can expect to pay on the loan, including the principal and any fees. A loan advertised at 10% APR with a 3% origination fee costs substantially more than a 12% APR loan with no origination fee, yet many borrowers focus only on the percentage. Calculate the total interest paid over the full term, not just the monthly payment, because a longer term lowers monthly payments but increases total interest costs significantly.

On a $10,000 loan at 12% APR, a three-year term costs roughly $1,977 in interest, while a five-year term costs $3,300 for the same principal and rate. Before signing any agreement, confirm whether your rate is fixed or variable because variable rates move with the Bank of Canada prime rate. If prime rises, variable-rate loan payments increase, which can strain your budget. Fixed rates offer predictability and let you lock in current pricing.

Verify Prepayment Terms and Set Up Automatic Payments

Verify prepayment flexibility because some lenders charge penalties if you pay off the loan early, while others allow extra payments or lump-sum prepayments without penalties. Paying off a personal loan faster saves significant interest, so a lender that permits penalty-free prepayment is genuinely worth more than a lower rate from a lender that penalizes early repayment. Once approved, set up automatic payments because missed payments trigger collections, legal action, and severe credit damage that costs far more than any interest savings.

Final Thoughts

An unsecured personal loan in Canada works best when you’ve completed the groundwork first. Pull your credit report, calculate your debt-to-income ratio, and honestly assess whether consolidating debt or accessing funds through this method actually improves your financial position. If your credit score sits below 650 or your DTI exceeds 44%, focus on strengthening those metrics before you accept unfavorable terms.

When you apply, use APR to compare offers across both major banks and non-bank lenders because the rate difference between Scotiabank at 6% and Mogo at 46.96% substantially reshapes your total borrowing cost. If you’re consolidating high-interest credit card debt, calculate the interest savings before you commit. If you need funds for a time-sensitive expense, verify that the monthly payment fits comfortably into your budget even if interest rates rise.

Contact a certified credit counsellor through Credit Canada at 1-800-267-2272 for a free debt assessment if you’re uncertain whether borrowing makes sense at all. We at Financial Canadian provide resources to help you make informed choices about borrowing, debt management, and building long-term financial stability. Your financial future depends on decisions you make today, so take the time to compare, calculate, and choose wisely.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment