Finding the right mortgage can save you thousands of dollars over the life of your loan. At Financial Canadian, we know that mortgage comparison in Canada shouldn’t be complicated or time-consuming.

This guide walks you through how rates work, what to compare beyond interest rates, and the mistakes that cost borrowers real money.

How Mortgage Rates Work in Canada

The difference between a 3.69% mortgage rate and a 4.50% rate costs you roughly $200 per month on a $400,000 mortgage. Over 25 years, that’s nearly $60,000 in extra interest. Understanding what moves rates in Canada directly impacts your wallet.

Fixed vs. Variable Rate Mortgages

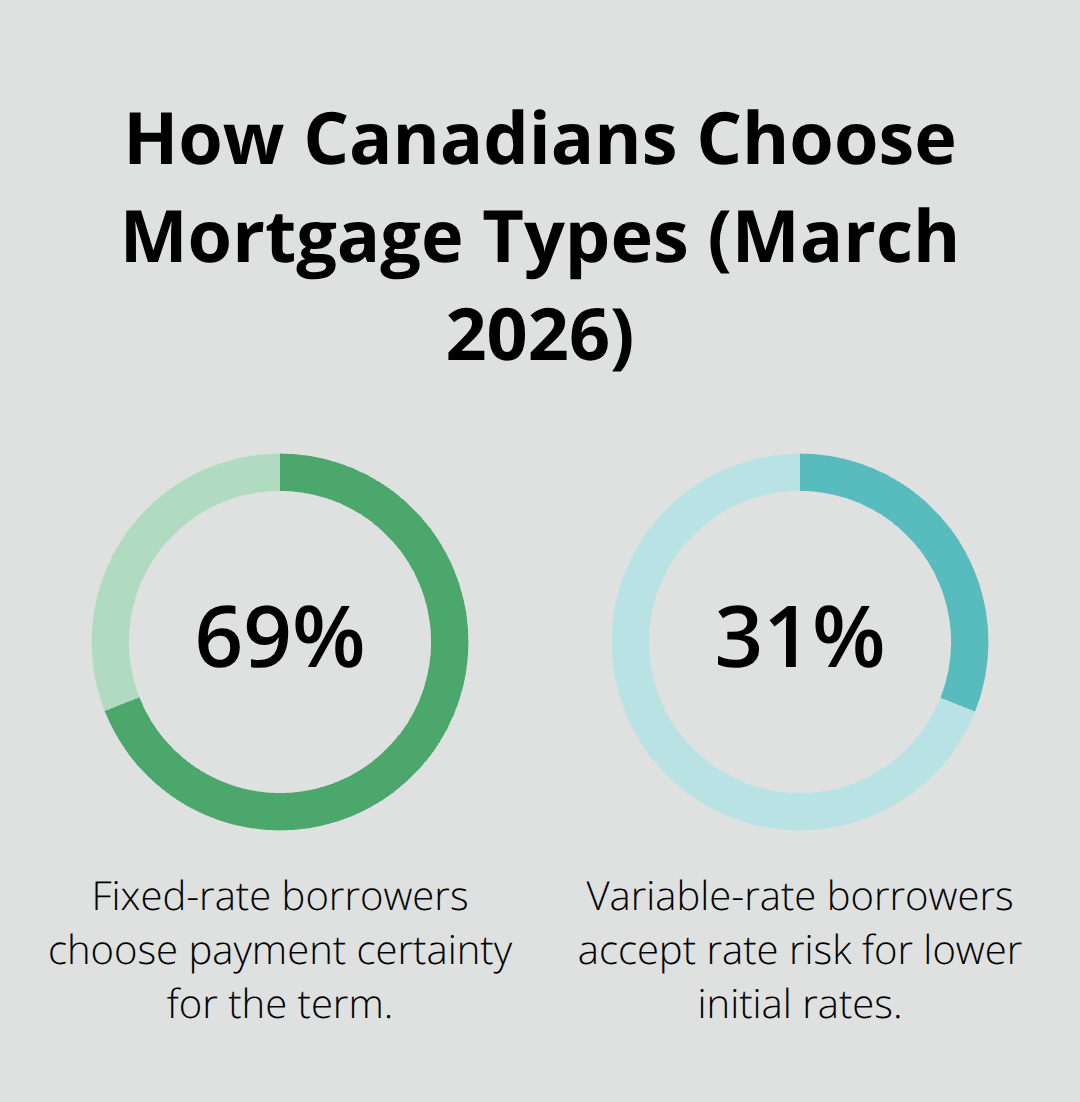

Fixed-rate mortgages lock your interest rate for the entire term, typically ranging from one to ten years. As of March 2026, the lowest five-year fixed rates sit around 3.69%, according to current market data. Variable-rate mortgages tie to the lender’s prime rate plus a spread, currently available as low as 3.35%. About 69% of Canadian borrowers choose fixed rates because they prefer payment certainty, while roughly 31% accept variable-rate risk in exchange for lower initial rates.

Fixed rates move with government bond yields, which shift based on inflation expectations, geopolitical events, and Bank of Canada policy signals. Variable rates follow the lender’s prime rate directly. The Big Six banks maintain a common prime rate of 4.45%, except TD which operates its own prime at 5.1%. When bond yields spike due to tension overseas or rising inflation, fixed-rate pricing climbs almost immediately. The five-year Government of Canada yield recently crossed 3%, pushing lender margins higher on comparable mortgages.

Personal Factors That Shape Your Rate

Your personal rate depends on factors beyond the market benchmark. A higher credit score around 680 or higher unlocks the best discounted rates, while lower scores push you toward higher pricing or alternative lenders. Down payment size matters significantly: larger down payments reduce lender risk and qualify you for better rates. Total debt payments should stay under 44% of household income to improve approval odds and rate competitiveness.

Insured mortgages (those with less than 20% down) carry government-backed protection, allowing lenders to offer lower discounts than uninsured loans. As of March 2026, insured discounted rates hover around 4.21%–4.51% while uninsured rates sit at 4.56%–4.66%, reflecting that lender risk difference. Whether you choose an open or closed mortgage also affects pricing: open mortgages allow penalty-free extra payments but carry higher rates, while closed mortgages offer lower rates with potential prepayment restrictions.

How Brokers and Rate Holds Work

Mortgage brokers access a wider lender network than direct bank applications and can negotiate on your behalf, often securing better terms than you’d find walking into a branch. Rate holds protect borrowers for 90-120 days after approval on purchases and renewals, or 60-90 days on refinances.

The Bank of Canada’s next rate decision comes March 18, 2026, with markets expecting a hold on the overnight rate. Without rate cuts, variable mortgage rates remain unlikely to move downward soon. The British Columbia Real Estate Association projects fixed rates to stay near current levels for most of 2026, suggesting stability rather than dramatic swings. Shopping with multiple lenders before committing generates at least three competing preapprovals, revealing your true options and negotiating leverage. This comparison process sets you up to evaluate what lenders actually offer beyond posted rates.

Where to Find Canada’s Best Mortgage Rates

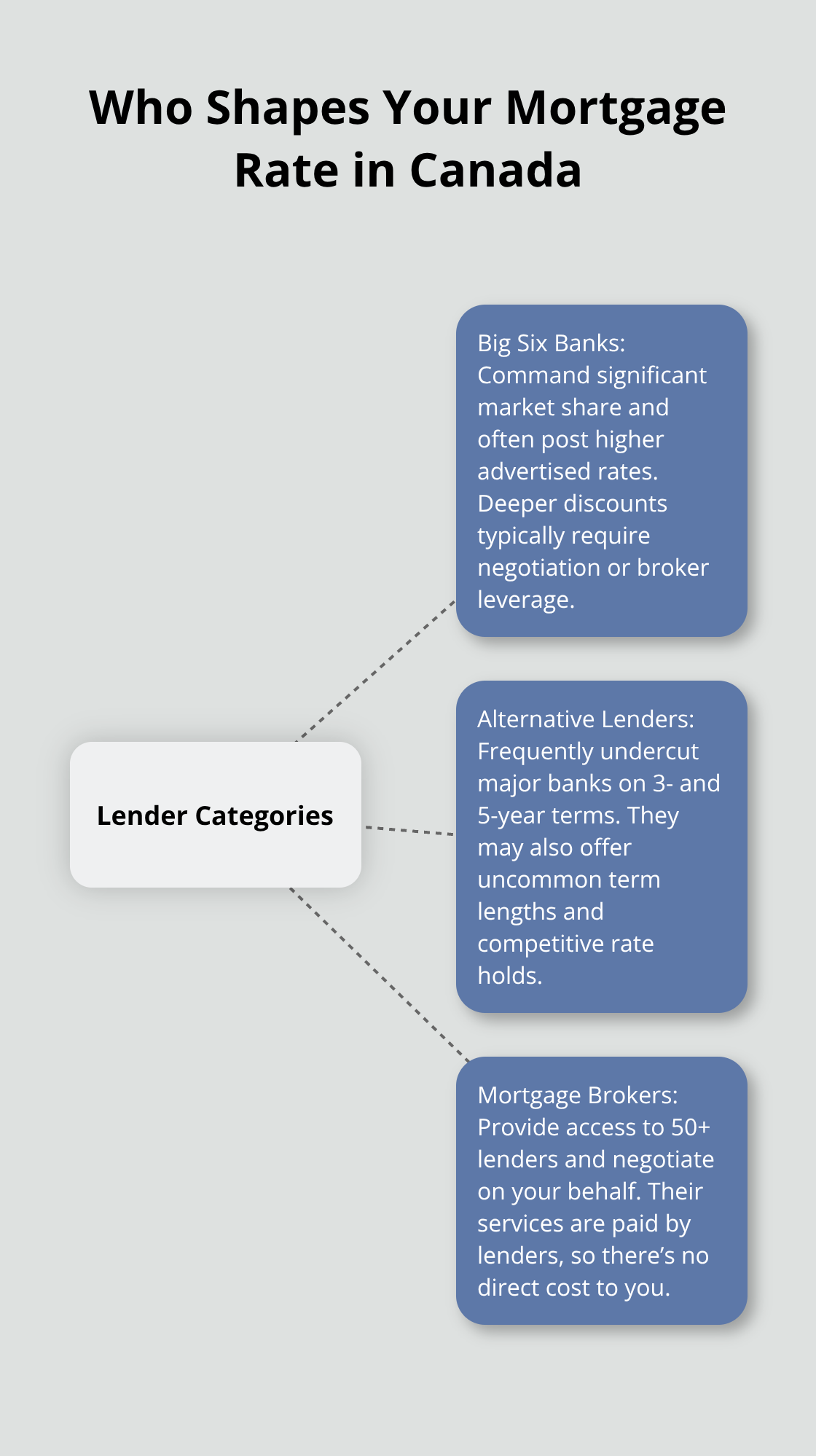

The Three Lender Categories That Shape Your Rate

Canada’s mortgage market splits into three distinct lender categories, and your choice directly affects the rates you’ll qualify for. The Big Six banks-RBC, TD, BMO, Scotiabank, CIBC, and National Bank-hold roughly 73% of all outstanding mortgages, but they rarely offer the lowest rates. These banks rely on posted rates that can run 0.50% to 1.00% higher than what brokers negotiate. RBC dominates by volume with about 17.5% of residential mortgages, yet competitive alternatives often beat their pricing substantially.

Alternative lenders like Alterna Bank, Laurentian Bank of Canada, and CMLS Financial consistently undercut the majors on 3- and 5-year fixed terms. CMLS Financial, operating independently after its acquisition by nesto, has built a reputation for rates below national averages with a 120-day rate hold. Laurentian Bank offers unusual term flexibility including 18-month and 4-year options that the Big Six rarely provide.

Why Mortgage Brokers Give You Real Leverage

Mortgage brokers form the third category and represent your strongest leverage point. Brokers access 50+ lenders including B lenders and private lenders, and they negotiate on your behalf. Lenders pay commissions to brokers, so you pay nothing for this service. A broker can show you products the banks won’t advertise, like specialized mortgages for self-employed borrowers or recent immigrants. This access matters because comparing only the Big Six limits your options to roughly 73% of the market.

What Actually Matters Beyond Interest Rate

When you compare across lenders, interest rate alone tells only half the story. Prepayment privileges determine how aggressively you can pay down principal without penalties-the best lenders offer 20% lump-sum payments annually plus unlimited payment increases, while others cap you at 10% per year. Rate holds vary from 90 to 130 days, affecting your timeline to complete a purchase or renewal.

Mortgage insurance costs differ based on lender and down payment size; a 10% down payment triggers CMHC insurance that can add $15,000–$25,000 to a $400,000 mortgage depending on the lender’s pricing. Cash-back incentives sound attractive but often hide higher rates-a $2,000 cash-back offer at 4.15% rarely beats a 3.85% rate with no cash-back. Term flexibility matters if you anticipate selling or refinancing within five years; open mortgages cost 0.30%–0.50% more but eliminate penalties entirely.

Tools That Reveal Your True Options

Online pre-approval speed varies dramatically-some lenders approve within hours while others require a phone call first. Ratehub.ca aggregates live quotes from Canada’s top lenders and has funded over $18 billion in mortgages, letting you compare rates from multiple sources simultaneously without applying separately. The platform maintains 4.9 out of 5 stars from over 11,000 reviews and lets you book phone appointments with mortgage experts to guide your application.

You should obtain at least three competing pre-approvals, which takes roughly one hour of your time and reveals your actual borrowing power. This comparison process strips away the marketing and posted rates that don’t reflect reality. Once you understand what three different lenders will actually offer you, you can move forward with confidence into the next stage of your mortgage search.

Common Mistakes When Choosing a Mortgage

Rate shopping stops too early for most Canadians, and this single mistake erases the savings you worked to find. You spent hours comparing lenders and found a 3.69% five-year fixed rate, but if you only looked at the posted rate without checking prepayment terms, you locked yourself into a mortgage that penalizes you for paying extra principal. A lender offering 3.69% with a 20% annual prepayment privilege costs substantially less over 25 years than 3.65% with only 10% prepayment allowed, yet posted rates hide this difference entirely.

Interest Rate Alone Tells Only Half the Story

Borrowers fixate on interest rate while ignoring closing costs, appraisal fees, and mortgage insurance premiums that can total $15,000–$25,000 on a $400,000 purchase. A cash-back offer of $3,000 at 4.15% sounds appealing until you calculate that the higher rate costs you $180 more per month than a competing 3.85% offer with no cash-back, erasing your bonus in roughly 17 months.

Mortgage insurance on mortgages with less than 20% down ranges from 2.8% to 4.0% of your mortgage amount depending on down payment size, adding a non-negotiable cost that varies between lenders.

Your actual monthly payment includes property tax, home insurance, and mortgage insurance if applicable, not just principal and interest, so comparing only the interest rate ignores 30%–40% of your true housing cost. Some lenders advertise low rates but bury higher insurance markups or appraisal fees that offset the savings. Open mortgages cost 0.30%–0.50% more than closed mortgages but eliminate prepayment penalties entirely, making them valuable if you anticipate selling or refinancing within five years.

Prepayment privileges Determine Your Real Savings

Prepayment privileges determine whether you can aggressively pay down principal without penalties, yet most borrowers never ask about this term. A mortgage with unlimited lump-sum prepayment saves roughly $40,000–$60,000 in interest over 25 years compared to one capped at 10% annually, assuming you have the cash flow to make extra payments. Some lenders advertise low rates but bury restrictive prepayment terms that prevent you from accelerating your payoff schedule.

Mortgage brokers access 50+ lenders and negotiate commission-based compensation, meaning you pay nothing for access to better terms, yet most borrowers never contact a broker and settle for Big Six bank rates that run 0.50%–1.00% higher than alternatives. A broker can reveal products the banks won’t advertise, like specialized mortgages for self-employed borrowers or recent immigrants, expanding your options far beyond posted rates.

Pre-Approval Locks Your Rate and Strengthens Your Offer

Shopping for homes without pre-approval weakens your negotiating position because sellers know you lack financing certainty. Pre-approval also reveals your maximum borrowing power so you avoid wasting time on properties outside your actual range. When you present an offer with pre-approval in hand, sellers take you seriously; without it, your offer competes against buyers who have already secured financing.

The third costly mistake happens before you even start house hunting: skipping pre-approval entirely. Without pre-approval, you cannot lock a rate, and you lack concrete proof of borrowing power when making an offer. Rate holds last 90–130 days depending on the lender, so locking your rate 120 days before closing protects you if bond yields spike due to geopolitical tension or inflation surprises. Obtaining three competing pre-approvals takes roughly one hour and reveals your true negotiating position; lenders compete directly when they know you have alternatives. The Bank of Canada held its overnight rate steady as of March 2026, meaning variable mortgage rates won’t move downward without rate cuts, so locking a fixed rate today protects you against future increases if economic conditions shift.

Final Thoughts

The difference between 3.69% and 4.15% costs you roughly $200 per month on a $400,000 mortgage, yet most borrowers never obtain three competing pre-approvals to reveal their true options. Mortgage comparison Canada works best when you evaluate prepayment privileges, rate holds, closing costs, and mortgage insurance alongside interest rates. A broker accessing 50+ lenders beats walking into a bank branch because lenders compete directly when they know you have alternatives, and you pay nothing for this service.

Your next step is obtaining pre-approval from at least three different lenders within the next week. This process takes roughly one hour, locks your rate for 90–130 days depending on the lender, and reveals your maximum borrowing power before you start house hunting. Pre-approval strengthens your offer when you find a property because sellers know you have financing certainty.

Contact a mortgage broker or use Ratehub.ca to compare rates from multiple lenders simultaneously without applying separately to each one. The Bank of Canada’s rate decision on March 18, 2026 will signal whether variable rates move downward, but fixed rates will likely remain near current levels for most of 2026 according to the British Columbia Real Estate Association. Locking a fixed rate today protects you against future increases if economic conditions shift.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment