Personal loan rates in Canada vary wildly depending on who you borrow from and your financial profile. Most borrowers overpay simply because they don’t know what fair pricing looks like.

At Financial Canadian, we’ve built this guide to help you spot the difference between competitive rates and predatory ones. You’ll learn exactly what to look for and how to negotiate better terms.

Current Personal Loan Rate Landscape in Canada

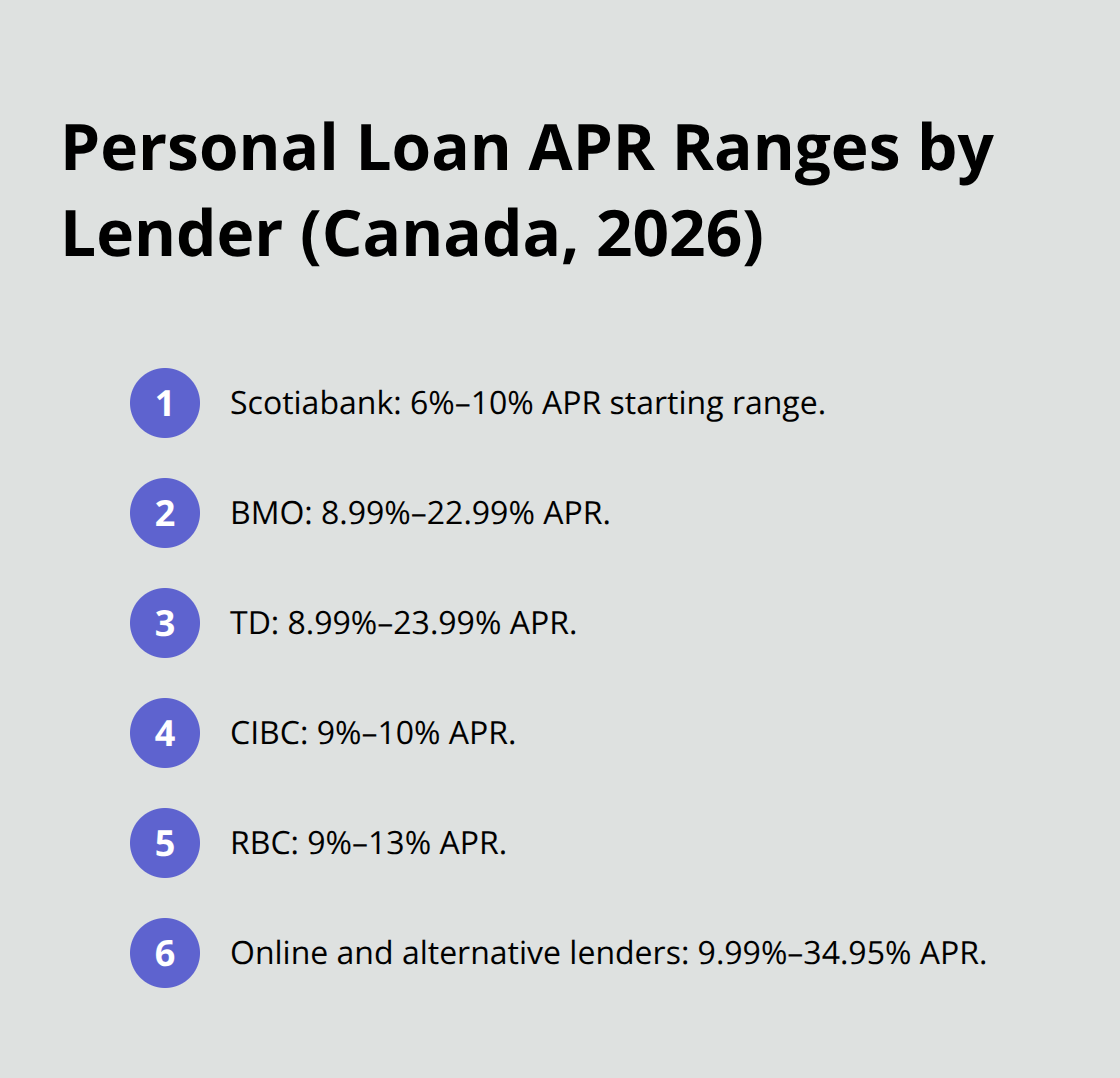

The personal loan market in Canada has fractured into distinct pricing tiers, and knowing where you fall determines whether you pay fair rates or get gouged. Major banks advertise starting APRs around 6% to 10% for well-qualified borrowers, but those rates rarely materialize for average Canadians.

Scotiabank quotes 6% to 10%, BMO sits at 8.99% to 22.99%, TD ranges from 8.99% to 23.99%, CIBC offers 9% to 10%, and RBC spans 9% to 13%. Online and alternative lenders cast a wider net with rates between 9.99% and 34.95%, though some climb higher depending on risk assessment.

The Bank of Canada’s overnight rate has held steady at 2.25% since January 2026, and economists surveyed by Reuters expect this pause to continue through the year. This stability means your personal loan rate won’t swing dramatically due to policy shifts, but your credit profile will determine everything. Lenders price individual risk aggressively in 2026 because Canadian households carry significant debt loads relative to income, making them hypersensitive to rate movements. The criminal rate cap of 35% APR, set in January 2025, creates a hard ceiling, but reaching those extremes signals your credit situation is dire.

Credit Score Controls Your Price

Your credit score determines personal loan rate approval and functions as a financial ID badge that lenders scan before quoting rates. Borrowers with excellent credit above 760 qualify for approximately 7.99% APR, while those in the 700 to 759 good range see around 10.99%. The fair credit band of 640 to 699 hits 15.99%, poor credit from 600 to 639 lands at 22.99%, and anything below 600 climbs toward 29% to 35%. On a standardized $20,000 loan over 60 months, moving from poor credit at 22.99% to good credit at 10.99% cuts your monthly payment from $565 to $435 and saves approximately $7,800 in total interest.

Equifax Canada and TransUnion supply these scores to lenders, so checking your own report before applying matters enormously. Small improvements pack outsized returns because each percentage point reduction compounds across the loan term. Fixing errors on your credit report or paying down revolving debt can push your score up 40 to 60 points, which translates to real savings measured in thousands. If your credit is severely damaged, second chance loans with guaranteed approval exist as a backstop option, though they carry higher costs.

Fixed Rates Lock Stability, Variable Rates Gamble on Tomorrow

Fixed-rate personal loans ignore Bank of Canada policy moves entirely once you sign, meaning your 12.99% rate stays locked whether rates rise or fall. This predictability appeals to borrowers who hate surprises and want to budget with certainty. Variable-rate personal loans track prime plus a spread, so if the BoC cuts rates further, your payment drops accordingly.

Currently, with the overnight rate at the low end of the neutral band and economists expecting it to stay put through 2026, variable-rate loans offer minimal upside while still carrying downside risk if macro conditions shift. The Reuters poll shows 75% of economists expect rate stability, but trade policy uncertainty from the USMCA review in July creates tail risks that could push rates up unexpectedly. Fixed rates eliminate that anxiety for borrowers who can’t absorb payment increases.

In practical terms, try fixed if you value certainty and can comfortably afford the payment at today’s rates. Try variable only if you have financial flexibility and genuinely believe rates will fall more than your spread advantage disappears. Your choice between these two structures shapes not just your monthly payment but also your ability to weather unexpected economic shifts-which is why comparing offers across multiple lenders becomes your next critical step.

What Qualifies as Fair Pricing

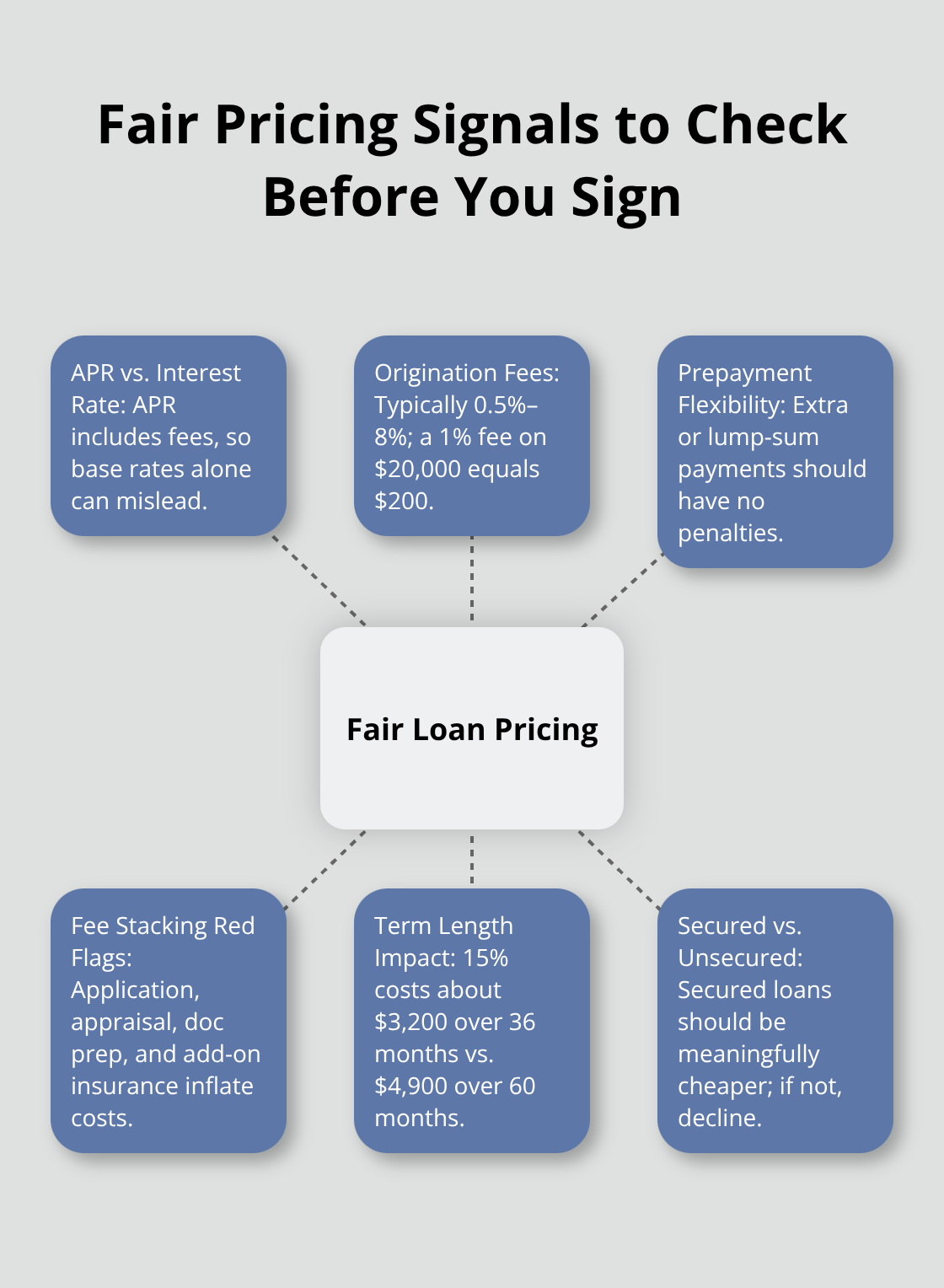

A fair personal loan rate reflects your actual credit risk, not what lenders hope you’ll accept out of desperation. APR matters far more than the advertised interest rate because APR includes origination fees, which typically run from 0.5% to 8% of your loan amount. These fees either get deducted upfront or added to your balance, and two lenders might quote identical base rates while one charges 5% origination and the other charges nothing. The APR figure always reveals the true cost.

On a $20,000 loan, a 1% origination fee equals $200 in hidden costs that a low-sounding interest rate can mask entirely.

Credit Score Determines Your Fair Rate Range

Your credit score tier establishes what fair pricing actually means for your situation. Borrowers scoring above 760 should reject anything higher than 8.5% APR from major banks, while those in the 700 to 759 range deserve rates under 11.5%. Fair credit borrowers between 640 and 699 should question anything above 16.5%, as this suggests the lender is padding margins beyond reasonable risk compensation. The poor credit band of 600 to 639 typically sees fair rates around 23%, though some lenders quote up to 46.96%, which crosses into exploitation territory. Spring Financial and goPeer typically offer more reasonable pricing in the 9.99% to 34.99% range for similar borrowers.

Origination fees vary wildly across lenders, so a lender quoting 25% APR with an 8% origination fee charges substantially more than one quoting 25% with no upfront fee. Calculate total cost over your loan term by comparing monthly payments and total interest paid, not just the advertised rate alone. This approach prevents you from selecting a loan that looks cheap initially but costs far more by maturity.

Prepayment Flexibility Separates Honest Lenders From Predatory Ones

Predatory lenders lock you into rigid payment schedules and charge penalties if you pay early, trapping you in high-interest debt longer than necessary. Fair lenders allow you to make extra payments or lump-sum prepayments without penalty, giving you control over your debt timeline. If a lender refuses to disclose prepayment terms upfront or charges fees to pay down your loan faster, walk away immediately.

A borrower with improving finances might land a better-paying job or receive an inheritance, and the ability to eliminate your debt without penalty distinguishes honest lenders from those betting on your financial distress. This flexibility costs lenders nothing but reveals whether they prioritize your financial health or their interest income.

Fee Stacking and Hidden Costs Expose Lender Intent

Red flags appear when lenders bury fees in fine print or quote rates that exclude mandatory charges. Beyond origination fees, watch for application fees (legitimate lenders rarely charge these), appraisal fees on secured loans, and document preparation fees. Some lenders add insurance products automatically unless you explicitly opt out, inflating your monthly payment without your knowledge.

Loan terms also determine whether you’re getting fair value because a 60-month loan costs more total interest than a 36-month loan at the same rate, yet lenders sometimes hide this by advertising only the monthly payment. A $20,000 loan at 15% costs roughly $3,200 in total interest over 36 months but $4,900 over 60 months. Secured loans backed by collateral should offer substantially lower rates than unsecured loans because your asset reduces lender risk. If a secured loan rate barely undercuts an unsecured offer, the lender is overpricing the security benefit and you should decline.

Comparing Offers Across Multiple Lenders Reveals Market Reality

Shopping across a broad pool of lenders uncovers competitive pricing that single-lender quotes never reveal. Major banks, credit unions, private lenders, and peer-to-peer platforms each price risk differently based on their funding costs and risk appetite. A rate that seems fair from one bank might look expensive when you compare it to three others, and this comparison process takes only hours but saves thousands in interest. The next chapter walks you through the specific tools and steps that make rate comparison fast and effective, turning you from a passive borrower into an informed negotiator.

How to Compare Loan Offers and Improve Your Odds

Gather Your Documents and Shop Across Multiple Lenders

The comparison process separates borrowers who pay fair rates from those who accept whatever first offer arrives. Start with your financial documents before shopping anywhere: government-issued ID, two recent pay stubs or tax returns, and a bank statement showing your account balance. Lenders need these to generate real quotes rather than estimates, and having them ready means you can apply across multiple lenders within hours before their rate locks expire. Most online lenders respond with decisions within minutes to 24 hours, so speed matters when comparing offers.

Pull your credit reports from Equifax Canada and TransUnion simultaneously because lenders pull from different bureaus, and you want to know exactly what they see before they see it. Check for errors like accounts you never opened or payment histories marked incorrectly, then dispute inaccuracies immediately since fixing them can boost your score 10 to 20 points within weeks. Shopping across multiple lenders reveals pricing variations that single-bank visits never expose.

Understand Why Rate Differences Matter

Major banks rarely offer their best rates to walk-in customers anymore; they reserve competitive pricing for online applications where their cost structure improves. A $20,000 loan at 12% costs $2,195 in total interest over 60 months, while the same loan at 14% costs $2,670-meaning just two percentage points difference equals $475 in unnecessary interest paid. This is why comparing across Scotiabank, BMO, TD, CIBC, RBC, Spring Financial, goPeer, and Mogo simultaneously takes three hours maximum but saves thousands.

Improve Your Credit Score Before Applying

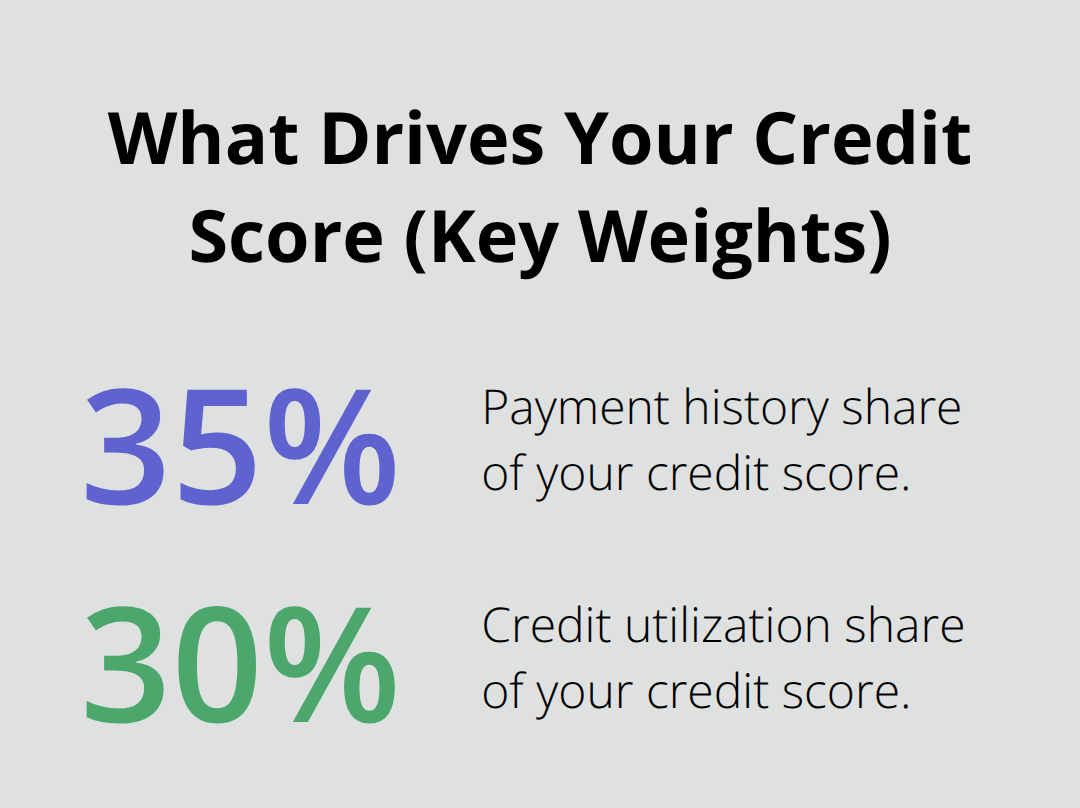

Improving your credit score before applying delivers faster results than negotiating with lenders after rejection. Focus on reducing your revolving debt first because credit utilization accounts for 30% of your score calculation, and dropping your credit card balances from 80% of limits to 20% can raise your score 40 to 60 points within 30 days. Payment history matters most at 35% of your score, so if you’ve missed payments recently, waiting three months after catching up shows lenders you’ve stabilized (though older missed payments hurt less each year).

A borrower sitting at 620 who improves to 700 within 90 days by paying down cards and catching up on missed payments can reduce their loan rate from approximately 29% to 10.99%, cutting total interest on a $20,000 loan by $7,800 over five years. Getting a personal loan with average credit becomes significantly easier once you’ve raised your score above 650.

Leverage Secured Loans and Competing Offers

Secured loans backed by collateral offer lower rates than unsecured loans because your asset reduces lender risk, so if you own a vehicle worth $5,000 or more, applying for a secured loan instead of unsecured can cut your rate by 5 to 8 percentage points. Lenders rarely negotiate rates downward after quoting, but they do compete for your business before you accept an offer, so use competing quotes as leverage. Tell each lender you have three other offers at lower rates and ask what they can improve (though most will decline rather than match).

Your credit profile and shopping strategy determine your actual cost entirely.

Final Thoughts

Fair personal loan rates in Canada exist if you know where to look and what to compare. Your credit score determines your starting point, but your effort determines your actual cost. Start by pulling your credit reports from Equifax Canada and TransUnion to see exactly what lenders will see, then dispute any errors immediately because fixing inaccuracies can boost your score enough to qualify for substantially better rates.

Once your credit profile is solid, gather your ID, recent pay stubs, and bank statements, then apply across at least three to five lenders simultaneously. Major banks, online lenders, and credit unions price risk differently, so comparing Scotiabank, BMO, TD, CIBC, RBC, Spring Financial, goPeer, and Mogo reveals the true market range for your situation. Focus on APR rather than advertised interest rates because APR includes origination fees that can hide substantial costs, and calculate total interest paid over your loan term rather than just monthly payments.

Reject any lender who charges prepayment penalties, buries fees in fine print, or refuses to disclose terms upfront, as these red flags indicate predatory intent. We at Financial Canadian help you navigate financial decisions with expert guidance and resources, and the same principle applies to your borrowing strategy: a solid foundation and transparent comparison process deliver results that shortcuts never match. Once you’ve narrowed your options to two or three competitive offers, verify that each lender allows extra payments without penalty so you can accelerate payoff if your finances improve.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment