Your credit score shapes your financial life in Canada. It determines whether you get approved for mortgages, car loans, and credit cards-and what interest rates you’ll pay.

At Financial Canadian, we’ve created this credit scores Canada guide to show you exactly how your score works, how to build it, and how to monitor it effectively. The practical steps and tools in this guide will help you take control of your credit profile.

How Credit Scores Work in Canada

Your credit score in Canada comes from five factors that lenders track closely. Payment history accounts for 35 percent of your score-this is the most important element. Credit utilization makes up 30 percent and measures how much of your available credit you actually use. The length of your credit history contributes 15 percent, while credit mix (having different types of credit like cards, loans, and mortgages) accounts for 10 percent. The final 10 percent comes from new credit inquiries and recently opened accounts. Equifax and TransUnion, Canada’s two major credit reporting agencies, calculate your score using these exact percentages, though their proprietary algorithms may weight certain factors slightly differently.

Understanding Your Three-Digit Score

Credit scores in Canada range from 300 to 900, and this range matters significantly for your borrowing power. A score between 660 and 724 is considered good, but lenders prefer scores above 750 for better interest rates. Scores above 800 qualify you for the best rates available, while anything below 600 signals serious financial risk to lenders. TransUnion and Equifax both use this same scale, so your score from either bureau should be roughly comparable. The difference between a 680 score and a 750 score can cost you thousands in additional interest on a mortgage-we’re talking about 0.5 to 1 percent higher rates on many lending products. Your exact score matters more than simply knowing it’s “good” or “bad.”

Why Payment History Dominates Your Score

Missing a payment by even one day gets reported to credit bureaus and damages your score immediately. A 30-day late payment can drop your score by 100 points or more, depending on your current score and payment history. Collections accounts, defaults, and bankruptcy filings stay on your credit report for six to seven years in Canada, continuously dragging down your score during that period. If you’ve missed payments, the good news is that their impact weakens over time-a late payment from five years ago hurts far less than one from last month. This means focusing on perfect payment performance right now will gradually rebuild your score, even if your history is damaged.

How You Can Improve Your Score Starting Today

Your payment history gives you the fastest path to improvement because lenders weight it most heavily. One month of on-time payments won’t fix years of damage, but consistent performance over several months will show measurable results. Lenders also notice when you reduce your credit utilization, so paying down balances before your statement closes can boost your score within weeks. These two actions-paying on time and lowering utilization-form the foundation for any credit repair strategy.

How to Build Credit Fast

Automate Your Payments to Eliminate Missed Deadlines

On-time payments matter more than anything else, so set up automatic transfers to your creditors on the day you receive income. This removes the human error that derails most credit repair efforts. If you earn a biweekly paycheck, split your monthly obligations into two payments timed to each paycheck. The automation costs nothing and eliminates the risk of a single missed deadline destroying months of progress. Many Canadian banks offer free bill payment scheduling through their online platforms, so you have no excuse to miss a due date.

Lower Your Credit Utilization Strategically

Credit utilization demands equal attention because lenders view high balances as a sign you’re financially stretched. Keep your total credit card balances below 30 percent of your combined credit limits, but try for 10 percent or lower to accelerate your score improvement significantly. If you have a $5,000 credit limit across three cards, your total balances should stay under $500. Pay down balances before your statement closing date rather than waiting until the due date, since credit bureaus record the balance shown on your statement. A cardholder with a 50 percent utilization rate who drops to 10 percent within two months typically sees a 30 to 50 point score boost. This happens because lenders interpret low utilization as responsible credit management, not because the payment itself rebuilds your history.

Identify and Dispute Errors on Your Credit Report

Your credit report contains errors that actively damage your score, so request a copy from Equifax or TransUnion and scan for inaccuracies. Late payments you never made, accounts you didn’t open, or incorrect balances appear on roughly 1 in 5 Canadian credit reports according to consumer advocacy data. Dispute these errors directly with the credit bureau in writing, providing documentation that supports your claim. The bureau must investigate within 30 days and remove unverified information. Removing even one false late payment or incorrect collection account can increase your score by 50 to 100 points instantly, making this effort worth your time. Once you’ve cleaned up your report, monitoring tools help you catch new errors before they damage your score further.

Monitor Your Credit in Real Time

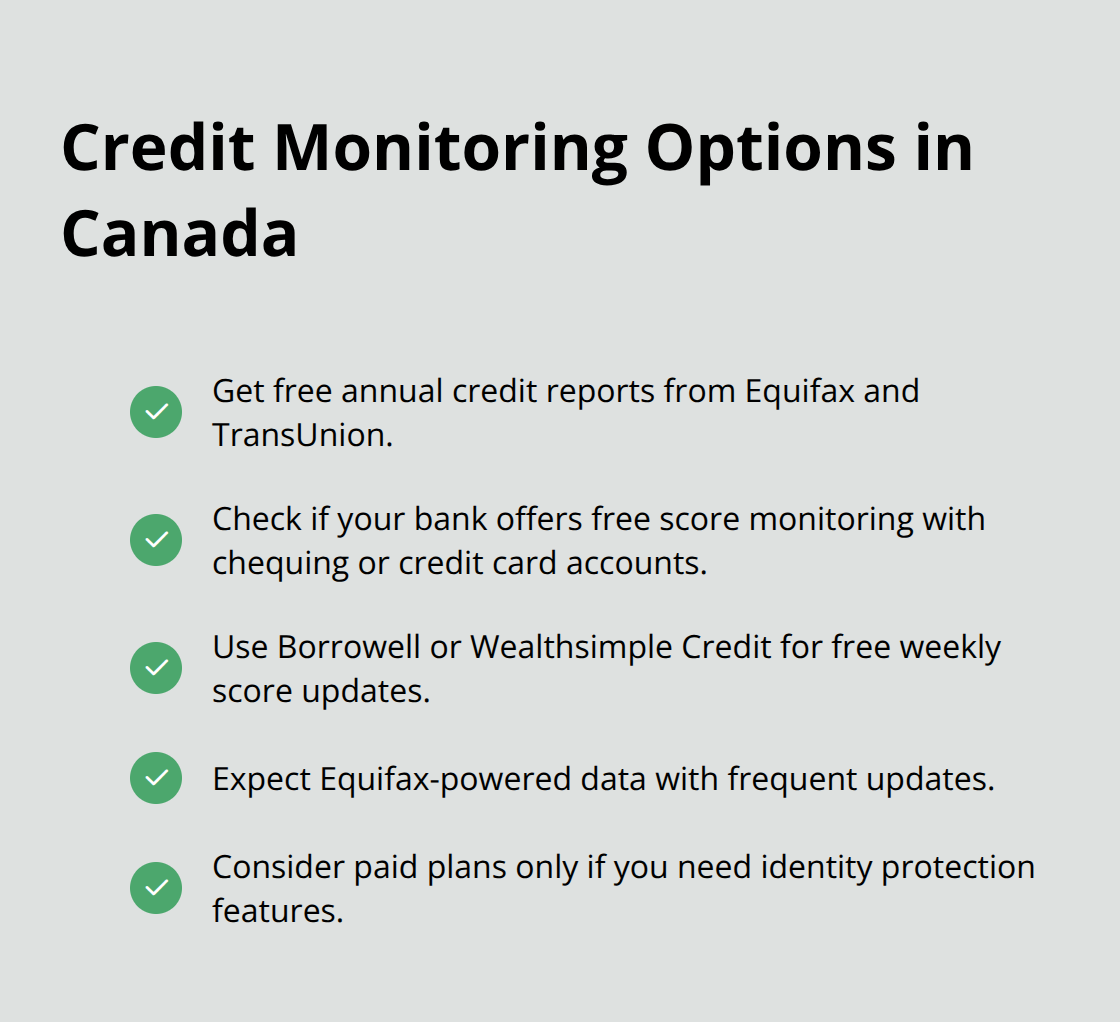

Monitoring your credit score regularly catches errors before they tank your rating, but most Canadians check their score only once yearly, if at all. Equifax and TransUnion both offer free annual credit reports through their websites, and you should access yours at least twice per year to spot inaccuracies early. The free reports come without your actual score, only your credit history details, which means you need a separate tool to track the three-digit number lenders actually use. Many Canadian banks now bundle free credit score monitoring into their premium chequing or credit card accounts, so check what your institution already provides before paying for additional services. If your bank doesn’t offer monitoring, services like Borrowell and Wealthsimple Credit provide free weekly score updates without hidden fees or premium upsells. These free tools use Equifax data and update frequently enough to show the impact of your payment and utilization changes within weeks. Paid services like Equifax Complete or TransUnion Plus offer deeper features such as dark web monitoring and identity theft protection, but they cost between 15 and 25 dollars monthly and add minimal value for most Canadians focused purely on score improvement. Start with free monitoring from your bank or Borrowell, and only upgrade to paid services if you have genuine identity theft concerns or require advanced features beyond score tracking.

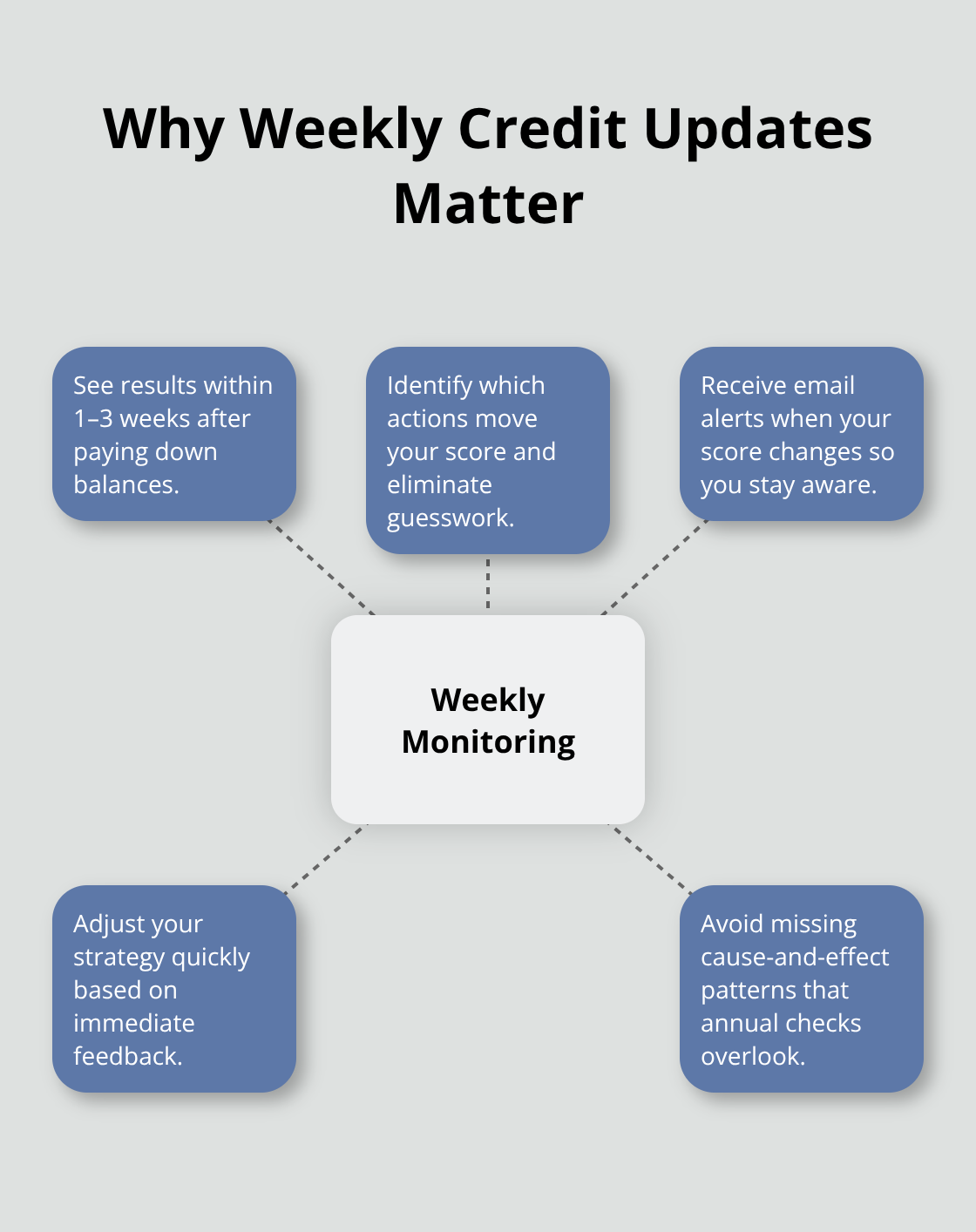

Why Weekly Updates Matter More Than Annual Reports

Weekly score tracking reveals which actions actually move your rating, eliminating guesswork from your credit repair strategy. After you pay down a credit card balance, you’ll see a score increase within one to three weeks as the new balance reports to credit bureaus, proving the effort worked. Monthly or annual checking misses these cause-and-effect patterns entirely, leaving you uncertain whether your actions produce results.

Free tools like Borrowell and Wealthsimple Credit send email notifications when your score changes, so you stay aware without constant checking. This feedback loop accelerates your improvement because you immediately see what works and adjust your strategy accordingly.

How Frequent Monitoring Personalizes Your Strategy

A cardholder who checks weekly discovers that paying down balances before statement closing boosts their score faster than paying on the due date, information they’d miss with annual checking. The data from these tools also reveals how inquiries, new accounts, and length of history affect your specific score, personalizing your improvement plan far beyond generic advice. You learn whether your score responds more strongly to utilization changes or payment consistency, then prioritize accordingly. This personalized approach works far better than following one-size-fits-all credit repair advice that ignores your unique credit profile.

Access Your Free Annual Reports Strategically

Request your free annual credit reports from Equifax and TransUnion at different times throughout the year rather than all at once. Spacing them three to six months apart gives you multiple checkpoints to catch errors before they compound. Each report shows your credit history details, late payments, collections accounts, and inquiries, allowing you to verify accuracy across both bureaus. Equifax and TransUnion sometimes report different information about the same accounts, so checking both reports ensures you catch all inaccuracies. Write to the bureau in question with documentation supporting your dispute, and they must investigate within 30 days and remove unverified information.

Final Thoughts

Building strong credit in Canada requires consistent action across two core areas: payment history and credit utilization. Your payment history accounts for 35 percent of your score, making on-time payments the single most effective lever you control, while lowering your credit utilization below 30 percent delivers measurable results within weeks. Monitoring your credit report catches errors that actively damage your rating, and these three actions form the foundation of any successful credit repair strategy that costs nothing to implement.

A score above 750 qualifies you for the best mortgage rates available, potentially saving you tens of thousands of dollars over a 25-year amortization. Better rates on car loans, credit cards, and personal loans compound these savings throughout your financial life, and lenders increasingly use credit scores to determine insurance premiums, rental approvals, and employment eligibility. Your next step depends on where you stand today-if you’ve never checked your credit report, request your free annual copy from Equifax or TransUnion immediately and scan for inaccuracies.

We at Financial Canadian created this credit scores Canada guide to help you take control of your credit profile and make better financial decisions. Start today with one action, then build from there using the framework we’ve provided.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment