Your home is likely your biggest asset. A home equity loan in Canada lets you borrow against that value to fund major expenses or consolidate debt.

We at Financial Canadian believe most homeowners don’t fully understand how these loans work or what rates they’re actually paying. This guide breaks down the real numbers, hidden costs, and smart ways to use this borrowing tool.

How Home Equity Loans Work

A home equity loan is a lump-sum borrowing product secured against your home’s equity. Unlike a line of credit that you tap into gradually, a home equity loan gives you one cash payment upfront, which you then repay on a fixed schedule over a set term, typically 5 to 20 years. This structure appeals to homeowners who fund one-time expenses like renovations or debt consolidation because the fixed repayment schedule makes budgeting straightforward. The loan sits behind your primary mortgage in terms of legal priority, which is why lenders charge interest rates that are generally lower than unsecured personal loans but higher than your mortgage rate.

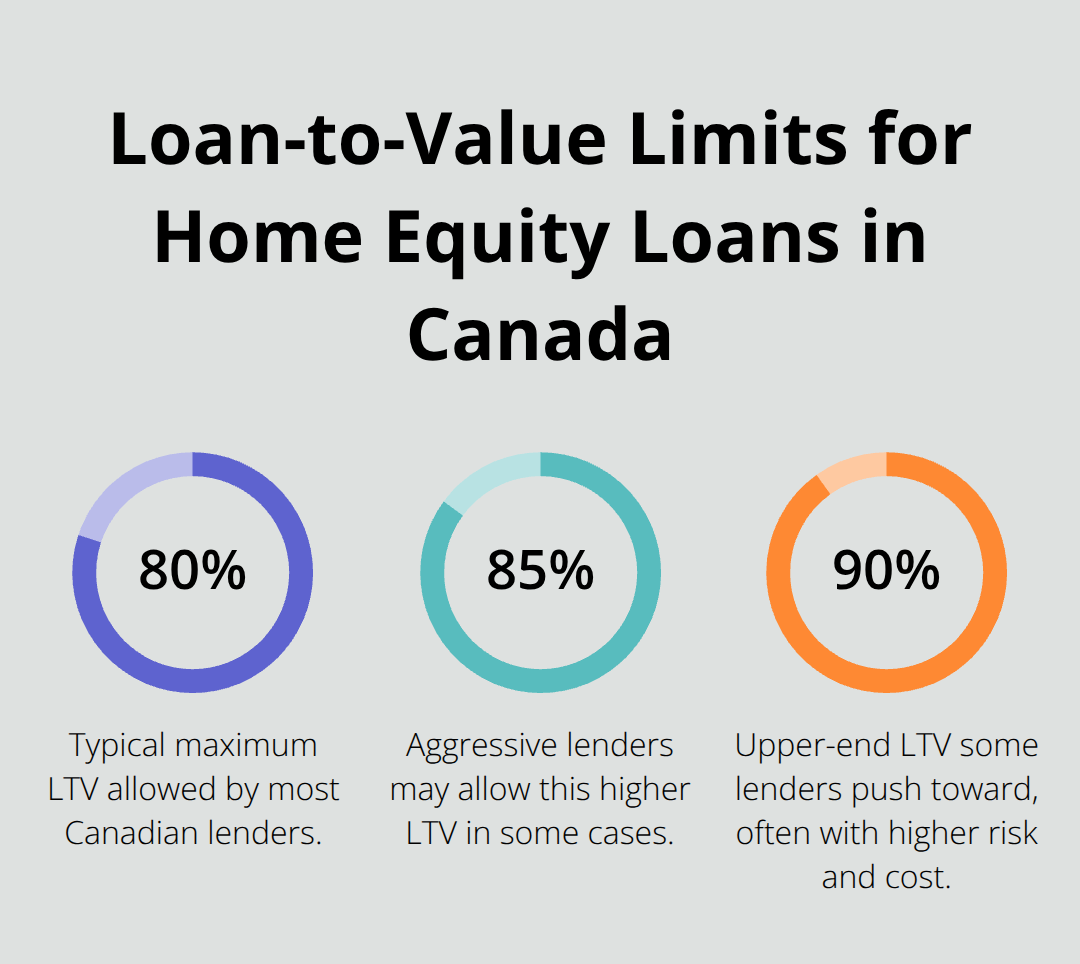

What Your Lender Actually Counts as Available Equity

Lenders calculate your available equity by taking your home’s current market value and subtracting what you still owe on your mortgage and any other secured debts against the property. Most Canadian lenders will let you borrow up to 80 percent of your home’s value minus your existing mortgage balance, though some aggressive lenders push closer to 85 or 90 percent. If your home is worth $250,000, the maximum amount you can borrow on home equity is $200,000 (80% of $250,000). At an 80 percent loan-to-value threshold, you could theoretically borrow up to $200,000 total against the property.

The catch is that lenders use their own appraisals or automated valuation models, so your home’s appraised value might differ from what you think it’s worth. A professional appraisal costs between $300 and $600, but it prevents surprises when you apply.

Home Equity Loans Versus HELOCs

A HELOC, or home equity line of credit, works fundamentally differently. You receive approval for a maximum credit limit but only pay interest on what you actually draw. This flexibility suits ongoing projects or situations where you don’t know the exact amount upfront. A home equity loan, by contrast, hands you all the money immediately, and you start repaying it right away whether you use every dollar or not. If you’re renovating your home and expenses might stretch across 18 months, a HELOC lets you draw funds as invoices arrive. If you consolidate debt today and won’t need more cash later, a home equity loan avoids the temptation to borrow additional funds. HELOCs typically carry variable interest rates that fluctuate with prime rate changes, whereas home equity loans usually lock in a fixed rate for the entire term. Fixed rates mean your payment never changes, making long-term budgeting predictable. Variable rates on a HELOC might start lower but expose you to payment increases if rates rise, particularly when the Bank of Canada’s policy rate affects borrowing costs across the economy.

Why Interest Rates Matter for Your Decision

The rate you qualify for depends on your credit score, income stability, and how much equity you’re borrowing against. Lenders view home equity loans as lower-risk than personal loans because your home secures the debt, so they offer rates that typically fall between your mortgage rate and unsecured loan rates. A fixed-rate home equity loan locks in your rate for the entire term, protecting you from future increases. This predictability helps you plan your budget with confidence, especially if you’re consolidating high-interest debt or funding a major expense. The next section examines current rates across Canadian provinces and the fees that lenders often hide in the fine print.

Current Home Equity Loan Rates and Costs in Canada

Home equity loan rates in Canada vary significantly by province and lender, but the real cost extends far beyond the advertised interest rate. As of early 2026, fixed-rate home equity loans typically range from 6.5 percent to 8.5 percent depending on your province, credit profile, and how much equity you’re borrowing. Ontario and British Columbia tend to offer slightly lower rates due to higher competition among lenders, while Atlantic provinces often see rates drift toward the higher end. The difference between a 6.8 percent rate and a 7.8 percent rate on a $100,000 loan over 10 years costs you roughly $5,000 more in total interest, which is why shopping multiple lenders matters.

The Hidden Fees That Add Up Fast

Lenders rarely advertise the full cost upfront, and most homeowners focus only on the interest rate while overlooking setup fees, appraisal costs, legal fees, and prepayment penalties. An appraisal typically runs $300 to $600, legal fees range from $500 to $1,500, and some lenders charge origination fees of 1 to 2 percent of the loan amount. A $100,000 home equity loan with a 1.5 percent origination fee immediately costs you $1,500 before you access a single dollar. Prepayment penalties are particularly problematic because they penalize you for paying off the loan early, which defeats the purpose of using a home equity loan to consolidate high-interest debt faster. Always request a complete cost disclosure that itemizes every fee, not just the interest rate, and compare the total cost across at least three lenders before committing.

How to Compare Offers Without Wasting Time

Most Canadian homeowners compare only one or two lenders, which leaves thousands of dollars on the table. Banks, credit unions, and online lenders all offer home equity loans, but their pricing and terms vary dramatically. Credit unions often charge lower rates than major banks because they’re member-owned and operate on lower profit margins, yet many homeowners never check their local credit union. Online lenders process applications faster, sometimes approving funds within days rather than weeks, though their rates aren’t always lower than traditional banks.

The fastest way to compare is requesting quotes from at least three different sources: your current mortgage lender, a competing bank, and a credit union. Request quotes in the same format to ensure apples-to-apples comparison, specifying the exact loan amount, term length, and whether you want a fixed or variable rate. Many lenders offer online pre-qualification tools that show you a rate estimate without a hard credit inquiry, so use these first to narrow your list before requesting formal quotes.

Calculate Total Cost, Not Just Monthly Payments

Once you have three quotes, calculate the total cost over the full term, not just the monthly payment, because a slightly lower rate compounds into substantial savings over 10 to 20 years. A lender offering 7.2 percent versus 7.8 percent might seem like a minor difference, but over a 15-year term on $150,000, that 0.6 percent difference saves you approximately $8,000 in interest charges. Avoid lenders that pressure you to decide quickly or that refuse to disclose all fees in writing, as legitimate lenders welcome comparison shopping and transparency. The fees and rates you negotiate now directly affect how much your home equity loan actually costs you over its entire lifespan.

Once you’ve identified the right lender and locked in your rate, the next critical decision is how to use that cash wisely-whether for debt consolidation, home improvements, or other major expenses.

Using Home Equity for the Right Financial Goals

The smartest home equity borrowers treat this tool as a targeted solution for specific high-cost problems, not as a general spending vehicle. Consolidating high-interest debt stands out as the most mathematically defensible use because the math works in your favor immediately.

Debt Consolidation: The Numbers That Matter

If you carry $25,000 across credit cards at 19.99 percent interest, you pay roughly $5,000 annually in interest alone before touching principal. A home equity loan at 7.5 percent on that same $25,000 costs you approximately $1,875 per year, saving you over $3,000 annually. The trap most people fall into is consolidating debt while keeping credit cards open and maxed out, which doubles their total debt load. Close the consolidated accounts after paying them off through the home equity loan, or you’ll end up owing both the home equity loan and new credit card balances.

Calculate your actual interest savings before applying because consolidation only makes sense if your home equity loan rate is genuinely lower than what you’re currently paying. Use a loan calculator to determine your actual interest savings, as some homeowners with excellent credit scores carry 12 percent debt and find that consolidating into a 10 percent home equity loan saves money, but the savings disappear if rates are closer together.

Home Renovations: Which Upgrades Justify the Debt

Home renovations represent a legitimate use, though not all upgrades create value. Kitchen and bathroom renovations typically return a good return on investment at resale, meaning a $20,000 kitchen upgrade might add significant value to your home. Major structural repairs like roof replacement or foundation work don’t add resale value but prevent catastrophic losses, so financing these through a home equity loan makes sense because they’re necessary investments.

Cosmetic upgrades like painting or landscaping typically return less than 30 percent, so financing these through a home equity loan only makes financial sense if you plan to stay in the home long enough to enjoy them personally rather than chase resale value.

Education and Emergency Expenses: Assess the Return

Emergency expenses and education funding remain valid uses, but they require honest self-assessment. If you borrow $40,000 against your home for education, verify that the program leads to measurable income increases that justify the debt. Someone pursuing a trades certification that increases annual income by $15,000 has a clearer return on investment than someone pursuing a degree with uncertain employment outcomes (particularly in saturated fields).

Never borrow against your home for lifestyle spending, vacations, or vehicle purchases because these depreciating assets don’t justify secured debt backed by your primary residence.

Final Thoughts

A home equity loan in Canada works best when you treat it as a precision tool for specific financial problems, not as a general spending vehicle. The three strongest use cases-consolidating high-interest debt, funding essential home repairs, and financing education with measurable income returns-share one common trait: they solve problems where the math clearly favors borrowing against your home rather than alternatives. Before applying, honestly assess whether your situation matches these criteria, because the difference between a defensible use and a risky one determines whether this borrowing tool strengthens or weakens your financial position.

The practical next step is requesting quotes from at least three lenders: your current mortgage provider, a competing bank, and your local credit union. Compare total costs over the full term, not just monthly payments or advertised rates, and factor in every fee (appraisal costs, legal fees, origination charges, and prepayment penalties). A 0.6 percent rate difference compounds into thousands of dollars saved over 10 to 20 years, which is why shopping multiple lenders directly impacts your financial outcome.

Once you’ve locked in your rate and received funding, execute your plan immediately. If consolidating debt, close those accounts after paying them off; if funding renovations, stick to your budget and avoid scope creep; if financing education, verify the program genuinely leads to income increases that justify the debt. We at Financial Canadian understand that navigating borrowing options requires clear information and practical guidance, so visit Financial Canadian to explore how we support financial education and transparency across the industry.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment