Your credit score directly affects your ability to borrow money, secure lower interest rates, and qualify for better financial products. At Financial Canadian, we’ve seen how even small improvements to your credit rating can save thousands of dollars over time.

The good news is that improving Canada credit scores doesn’t require complex strategies or years of waiting. This guide walks you through actionable steps you can start today.

Understanding Your Credit Score in Canada

How Credit Bureaus Calculate Your Score

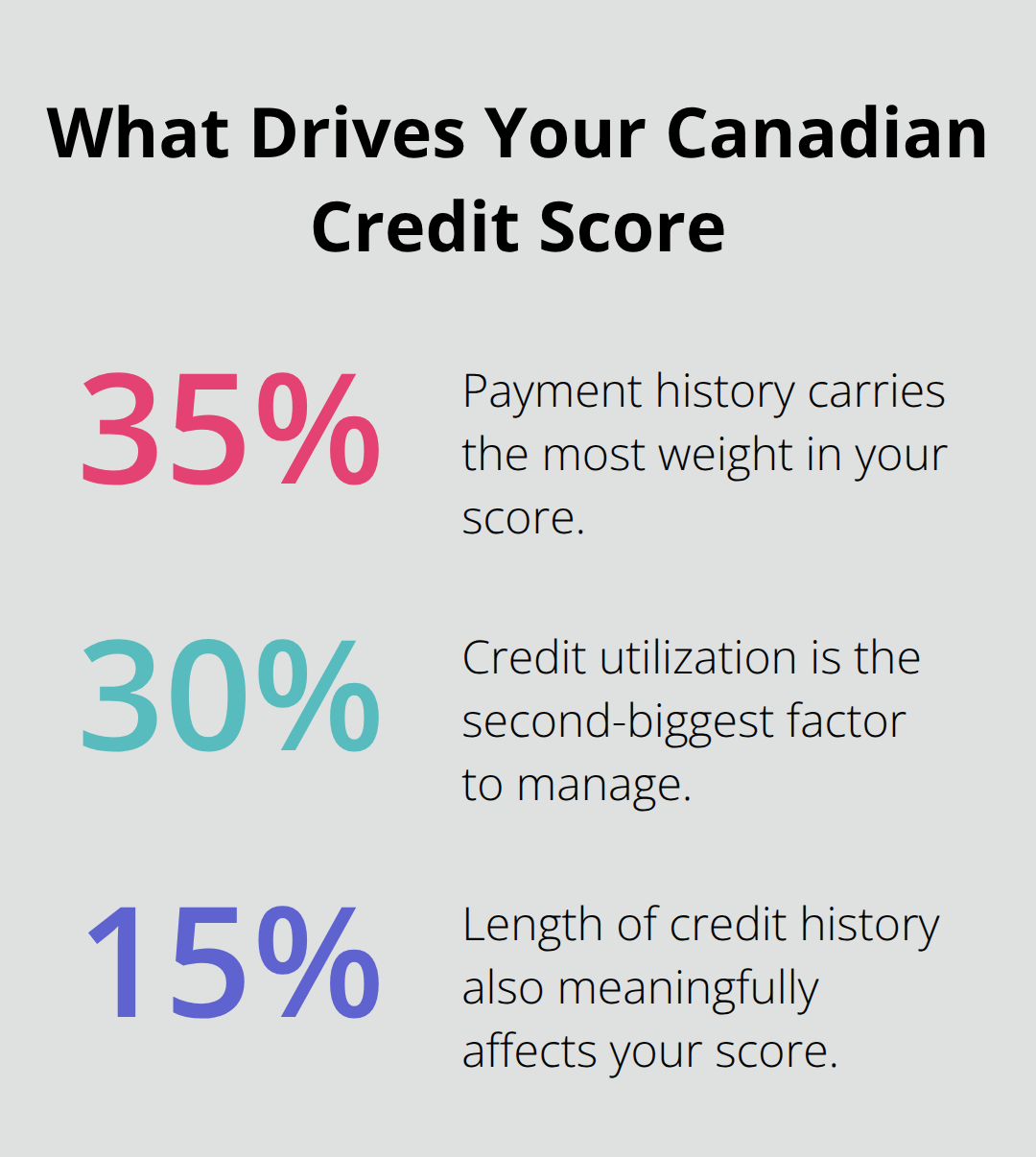

Canadian credit bureaus Equifax and TransUnion calculate your score using five key factors, and understanding this breakdown shows you exactly where to focus your efforts. Payment history accounts for 35% of your score, which means a single missed payment can damage your rating more than almost anything else. Credit utilization makes up 30%, so keeping your balances well below your limits directly protects your score. The length of your credit history counts for 15%, which is why closing old accounts actually hurts you even if those accounts are paid off. Credit mix represents 10%, meaning lenders want to see you handle different types of credit responsibly. The final 10% comes from new credit inquiries, so spacing out your applications matters more than most people realize.

TransUnion data from Q4 2025 shows that nearly 20% of Canadians improved their scores over the past year, proving that deliberate action works.

What Your Score Actually Means

Canadian credit scores range from 300 to 900, and the brackets matter more than the exact number. A score between 725 and 759 lands you in the very good category, where you’ll qualify for decent interest rates and better credit products. Scores above 760 put you in the excellent range, and these borrowers get the lowest rates and highest credit limits. Below 650 becomes problematic because lenders see you as high risk and either deny you or charge significantly higher rates.

TransUnion data shows that over 70% of credit-active Canadians sit in prime or better risk tiers, with the super prime segment reaching 42.1% in Q4 2025. This means the majority of Canadians have already built solid credit, which makes your path forward clear: focus on consistent on-time payments and low utilization to move into these healthier segments.

Why Your Score Controls Your Financial Life

Your credit score isn’t just about borrowing money. Employers sometimes check your score during hiring, insurance companies use it to set your premiums, cell phone providers reference it when approving contracts, and landlords check it before offering you a lease. A strong score saves you thousands in interest on mortgages, car loans, and credit cards over your lifetime.

If you’re applying for a mortgage, even a 50-point improvement in your score can lower your rate by 0.25%, which translates to tens of thousands in savings over 25 years. Canadian household debt reached $2.6 trillion in 2025 according to TransUnion, and most of that debt is held by borrowers in prime tiers who negotiated better rates because of stronger scores. Your score determines whether you pay 4% or 8% on a car loan, whether you get approved for a $5,000 or $15,000 credit limit, and whether you qualify for a mortgage at all.

Now that you understand how your score works and why it matters, the next section reveals the specific actions that move your rating upward fastest.

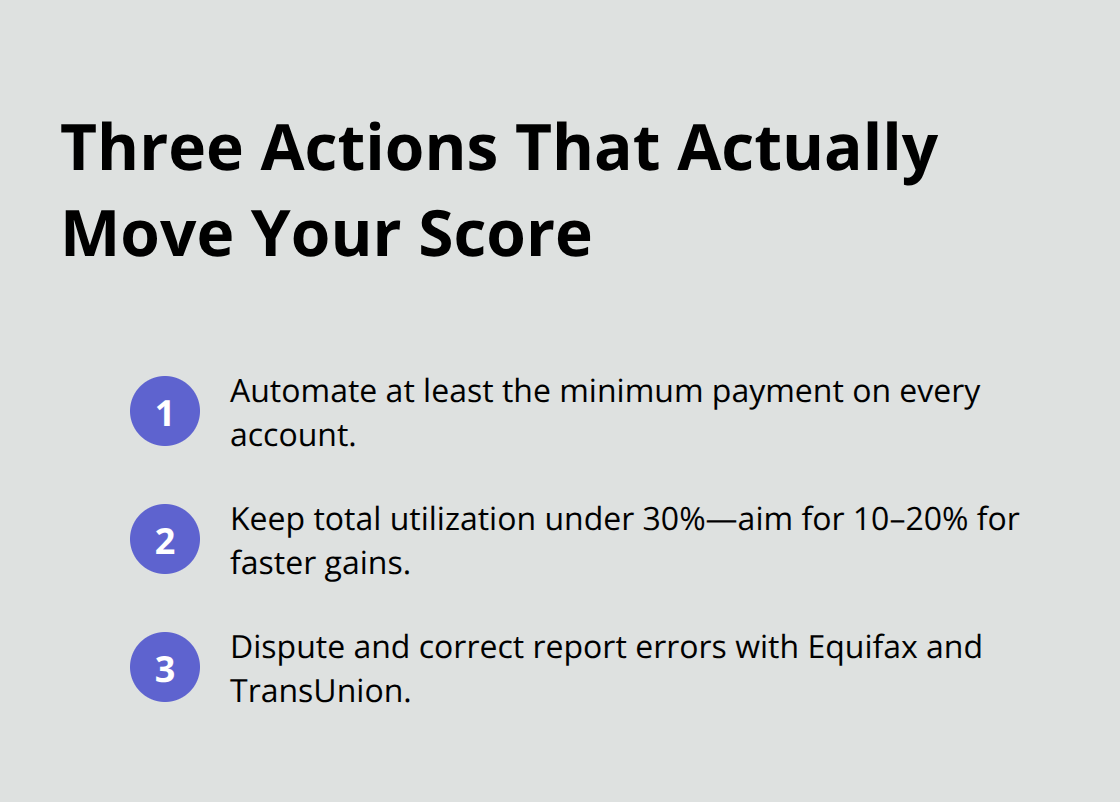

Three Actions That Actually Move Your Score

Automate Your Payments to Stop Missing Deadlines

Payment history dominates at 35% of your score, which means one missed payment can erase months of good behavior. The practical solution is automation. Set up automatic payments for at least the minimum on every credit account you hold, scheduled to post three days before the due date. This removes the human error that derails most people.

If you’re behind on payments right now, catch up immediately. Each month that passes with current payments rebuilds your standing faster than anything else. TransUnion data shows that over 70% of credit-active Canadians sit in prime or better risk tiers, and the single common thread among them is consistent on-time payment history. Your payment record matters so much that lenders using FICO scores treat it as the foundation of their risk assessment.

Lower Your Credit Utilization Ratio

Credit utilization is the second lever, and you control it completely. Keep your total balances across all cards under 30% of your combined limits, though try for 10–20% to see faster score gains. If you have a $5,000 limit and carry a $4,500 balance, you signal financial stress even if you pay on time. Drop that balance to $1,000 and your score climbs noticeably within 30–60 days.

The reason is straightforward: lenders interpret high utilization as desperation or poor money management. FICO score models penalize every single card individually, so maxing out even one card while keeping others low still damages your rating. Pay down your highest-balance cards first to free up utilization quickly.

Correct Errors on Your Credit Reports

Check your credit reports from both Equifax and TransUnion annually at no cost. Errors happen-accounts reported twice, fraudulent inquiries, or accounts you’ve already closed still showing as open. Dispute any inaccuracy in writing and request correction. These corrections can lift your score significantly if errors have dragged down your rating.

The three actions above-automating payments, cutting utilization below 30%, and correcting errors-form the foundation that moves your score upward consistently. With these fundamentals in place, you’re ready to tackle the longer-term strategies that separate good credit from excellent credit.

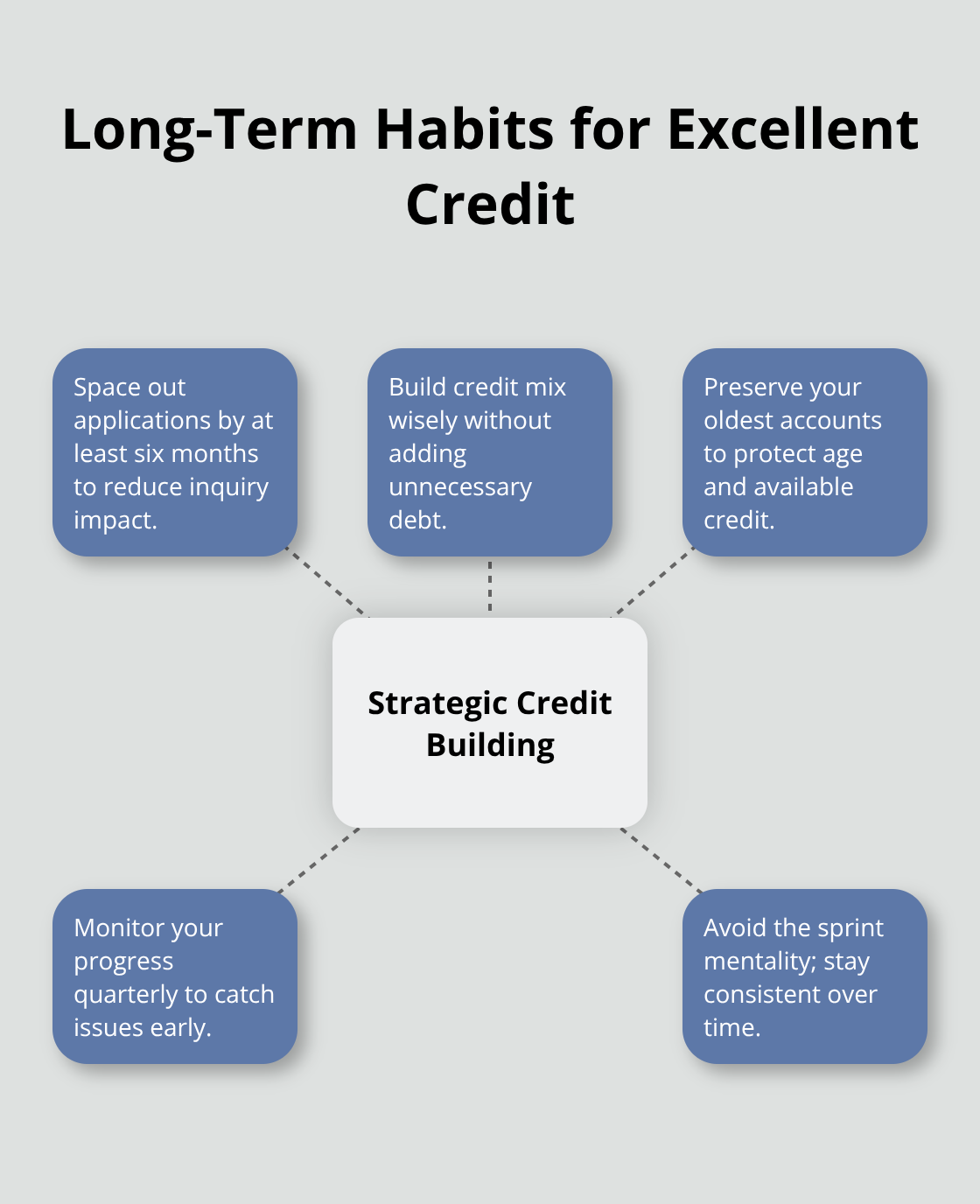

Build Credit Strategically Without Rushing

The actions you took in the previous section create momentum, but sustainable credit improvement requires a longer view. Two-thirds of Canadians stayed in the same risk tier over the past year according to TransUnion, while 19.4% improved to better tiers. The difference between stalling and advancing comes down to how deliberately you manage your credit portfolio over months and years, not days and weeks.

Avoid the Sprint Mentality

The biggest mistake people make is treating credit like a sprint. They obsess over their score for three months, then abandon discipline and undo their progress. Instead, think of credit as a managed system where each decision either supports or undermines your long-term standing. Most people fail because they lack patience, not because the strategy doesn’t work.

Space Out New Credit Applications

Spacing out new credit applications matters far more than most people realize. Each time you apply for credit, a hard inquiry lands on your report and stays for three years, though it affects your score most heavily in the first few months. If you apply for three credit cards within six months, lenders see this as a red flag signaling financial desperation.

Space applications at least six months apart, and only apply when you genuinely need new credit. This single discipline prevents unnecessary score damage and signals to lenders that you approach credit thoughtfully.

Build Credit Mix Wisely

Your credit mix influences your score, but this is where people get confused. Lenders want to see you handle revolving credit like credit cards and installment credit like car loans or personal loans responsibly. However, this does not mean you should rush out and take a car loan to improve your mix.

If you already have a credit card and are paying it on time with low utilization, your credit mix is adequate. Adding unnecessary debt to chase a better mix defeats the purpose of building healthy credit. Only apply for new credit types when you actually need them. Veteran credit accounts that have existed for five years or longer remain stable at approximately 32.8% utilization according to FICO benchmarking data, showing that long-standing borrowers maintain discipline.

Preserve Your Oldest Accounts

Preserve your oldest accounts even after paying them off completely. Closing old accounts shrinks your available credit, raises your utilization ratio instantly, and shortens your average account age. If an old card charges an annual fee, call and request a waiver or downgrade to a no-fee version. Keep it open with small occasional purchases to maintain activity.

Monitor Your Progress Quarterly

Monitor your credit progress quarterly by checking your score through free FICO Score Open Access tools or pulling your full reports from Equifax and TransUnion annually. Tracking your score reveals whether your actions are working or if external factors like errors are dragging you down. Many people check their score once, see improvement, then never look again. That’s precisely when old errors resurface or new problems emerge.

Quarterly monitoring catches problems early before they compound. Set a calendar reminder for the same month each quarter so checking your credit becomes automatic rather than forgotten.

Final Thoughts

Improving Canada credit scores comes down to three foundational actions: automating payments to eliminate missed deadlines, cutting credit utilization below 30%, and correcting errors on your reports. These steps address the factors lenders care about most, and they work because they target the mechanisms that directly influence your rating. You’ll see measurable movement within 30 to 60 days of lowering utilization, though payment history takes longer to rebuild if you’ve had recent missed payments.

Most people notice a 20 to 50-point improvement within three months of consistent on-time payments and lower balances, with larger jumps arriving after six months of sustained discipline. TransUnion data shows that 19.4% of Canadians improved to better risk tiers over the past year by staying disciplined with these fundamentals. The timeline matters less than the consistency you maintain each month, since your credit score responds to your actions and reflects your financial behavior in real time.

Space out new credit applications, preserve your oldest accounts, and check your progress quarterly to prevent backsliding and catch problems before they compound. We at Financial Canadian offer comprehensive resources and guidance to help you navigate your financial journey with confidence. Start your credit improvement today and watch your financial options expand as your score climbs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment