Buying a home in Canada means navigating multiple mortgage options, each with different costs and benefits. Your choice between fixed-rate, variable-rate, or hybrid mortgages will shape your monthly payments and long-term finances.

At Financial Canadian, we’ve created this guide to help you understand what lenders look for and how to compare rates across banks, credit unions, and private lenders. The right mortgage path depends on your credit score, down payment, and debt situation-and we’ll show you how to evaluate all three.

Your Mortgage Options: Fixed, Variable, or Hybrid

Canada’s mortgage market offers three main paths, and the current rates matter when you’re deciding which one fits your situation. Fixed-rate mortgages currently sit around 3.94–3.99% for 5-year terms, locking in your payment for the entire period. This stability appeals to homebuyers who want predictable monthly payments and protection against rate hikes. If rates climb over the next few years, your payment stays the same while others face increases. However, fixed rates carry higher penalties if you need to break the mortgage early-typically three months of interest or an interest rate differential charge. Variable-rate mortgages are priced lower at Prime minus 0.95%, currently around 4%, but your payment fluctuates when the Bank of Canada adjusts its policy rate. The advantage is clear: if rates fall, you save money immediately without refinancing. Variable mortgages outperform fixed rates over the long term, though this depends heavily on timing and how much rates actually move. The real risk appears when rates spike suddenly; without a solid financial buffer, rising payments can strain your monthly budget.

When Fixed Rates Make Financial Sense

Choose a fixed-rate mortgage if you plan to stay in your home for 5+ years and value payment certainty. This approach eliminates the stress of wondering whether your mortgage payment will jump next quarter, especially valuable during economic uncertainty. Locking in near 3.94% provides a safety net if the Bank of Canada raises rates. Your monthly payment covers the same amount every month, making household budgeting straightforward.

When Variable Rates Offer Real Savings

Variable mortgages work best if you have emergency savings covering 6+ months of expenses and can absorb payment increases even if rates rise by 2%. The Prime minus 0.95% discount means you benefit immediately if rates decline, and variable mortgages typically carry lower break penalties than fixed options, making them ideal if you might sell or refinance within 3–5 years. Calculate the true cost: apply the discount to the current prime rate to see your actual payment, then compare it against fixed-rate offers from multiple lenders.

Hybrid Mortgages for Balanced Flexibility

Hybrid mortgages split your loan between fixed and variable portions, letting you hedge your bets without committing entirely to either path. You might lock in 60% at a fixed rate and leave 40% variable, balancing payment predictability with savings potential. This approach suits homebuyers uncertain about rate direction or those wanting to reduce risk without sacrificing upside. The trade-off is slightly higher administrative complexity and potentially higher rates than pure fixed or variable options, but the flexibility often justifies the cost for borrowers in transitional financial situations.

Moving Forward With Your Choice

Your mortgage type shapes not only your monthly payment but also your ability to refinance or sell without penalty. Understanding these three paths prepares you to evaluate what lenders actually look for when they assess your application. The next step involves examining the specific qualification criteria that determine whether lenders approve your mortgage and at what rate.

Key Factors That Affect Your Mortgage Qualification

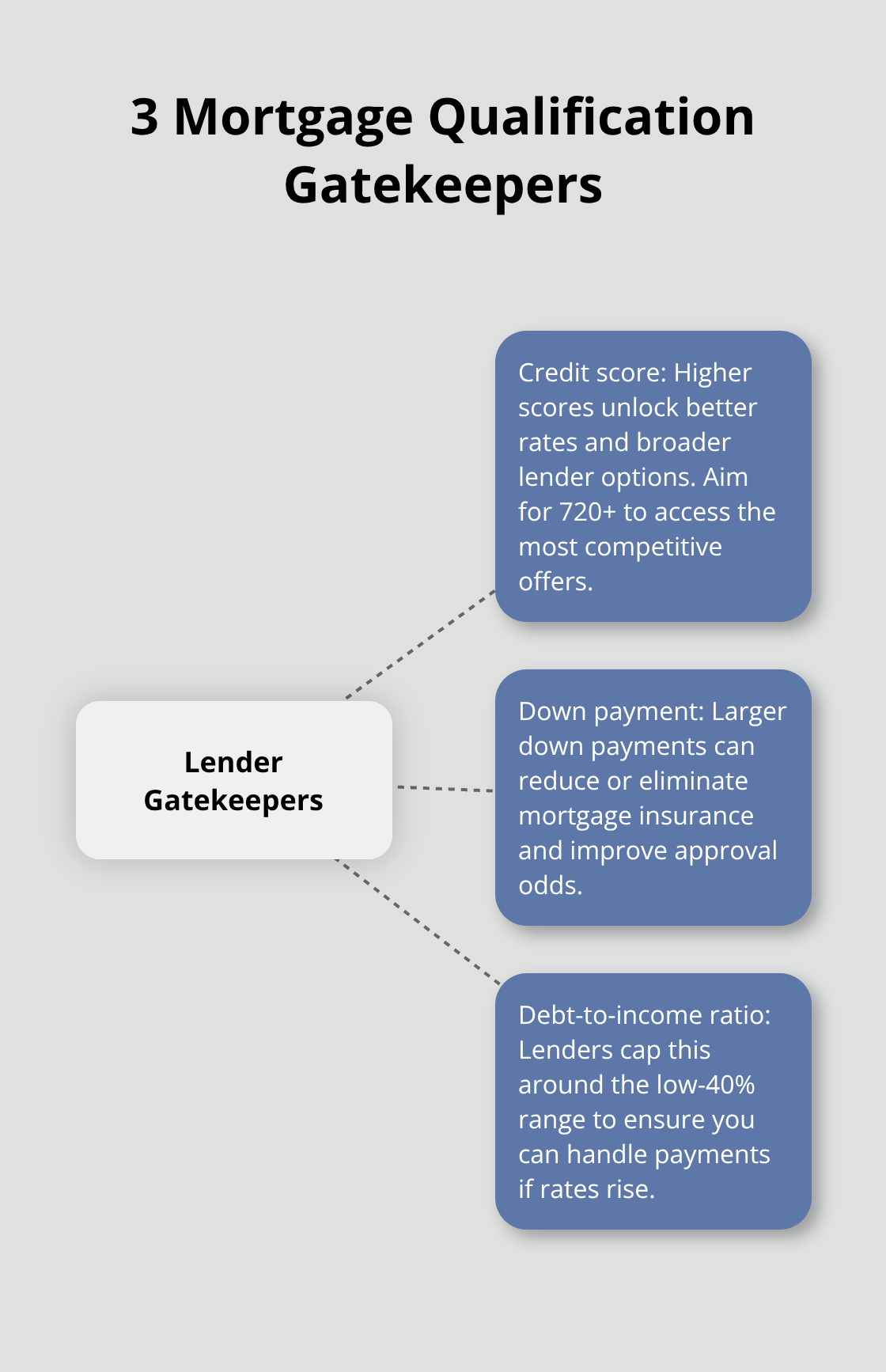

Your credit score, down payment, and debt-to-income ratio act as the three gatekeepers lenders examine before approving your mortgage. Lenders use these metrics to assess risk, and they’re not subjective-each one has concrete thresholds that determine whether you qualify and what rate you’ll receive.

Credit Score Requirements and Impact

A credit score below 620 makes it nearly impossible to secure a conventional mortgage from major Canadian banks, while scores between 620 and 680 typically qualify you but at higher rates due to increased perceived risk. Scores above 720 unlock the best rates available, so if yours sits below that, paying down existing debt or disputing errors on your credit report can yield meaningful savings over a 25-year mortgage. Even a 40-point improvement from 680 to 720 can reduce your rate by 0.25% to 0.50%, translating to thousands of dollars in savings across your loan term.

Down Payment Size and Mortgage Insurance

Your down payment size directly affects mortgage insurance costs, which lenders add to your loan if you put down less than 20%. A 15% down payment triggers CMHC mortgage insurance that can add 2.8% to 4% to your mortgage amount, while a 5% down payment pushes insurance costs to 4.00% or higher. On a $400,000 home, the difference between 5% and 15% down means paying roughly $18,000 more in insurance premiums over the life of your loan. If you’re short on down payment savings, CMHC’s First-Time Home Buyer Incentive lets the government co-invest in your mortgage, reducing your monthly payment obligation without requiring you to save an additional 10% upfront.

Debt-to-Income Ratio and Lender Assessment

Your debt-to-income ratio tells lenders how much of your gross income already commits to debt repayment, and most Canadian lenders cap this at 39% to 44% depending on the lender and mortgage type. Calculate this yourself: add up all monthly debt payments (car loans, credit cards, student loans, existing mortgages) and divide by your gross monthly income. If you earn $5,000 monthly and carry $1,800 in existing debt payments, your ratio sits at 36%, leaving room for a mortgage payment of roughly $360 to stay within the 44% threshold. Lenders scrutinize this ratio heavily because it indicates your ability to absorb rate increases without financial strain. Paying down credit card balances before applying improves this ratio immediately, even if you don’t increase your income. Some lenders also consider your gross debt service ratio, which includes property taxes and heating costs alongside mortgage payments, tightening the acceptable threshold further.

Getting Pre-Approvals and Rate Quotes

Getting pre-approved forces lenders to verify your income, pull your credit report, and confirm your debt obligations, giving you a concrete number for how much you can borrow rather than guessing. Pre-approvals remain valid for 120 days in most cases, providing a window to house hunt with confidence and make offers knowing your financing is secure. Request pre-approvals from at least three lenders because rates and approval terms vary significantly; one lender might approve you at 3.95% while another quotes 4.15% for identical financial circumstances. Once you understand what lenders look for, the next step involves comparing those lenders themselves-banks, credit unions, and private lenders each offer different advantages depending on your financial profile and timeline.

Comparing Mortgage Lenders and Finding the Best Rates

Banks dominate Canada’s mortgage market, but they’re not your only option and often aren’t your cheapest. The Big Five banks-Royal Bank, TD, Scotiabank, BMO, and CIBC-control roughly 75% of Canada’s mortgage business, which means they can afford to be less competitive on rates because borrowers default to them out of habit. Credit unions like Meridian and Desjardins frequently undercut bank rates by 0.15% to 0.30%, translating to thousands of dollars saved over a 25-year mortgage.

On a $350,000 mortgage at 3.95% versus 3.70%, the credit union option saves you approximately $21,750 in interest alone. Private lenders and mortgage brokers add another layer: they access wholesale rates and niche products that banks won’t touch, especially valuable if your credit score sits between 650 and 700 or you’re self-employed with irregular income. The catch is that private lenders charge higher rates-typically 0.50% to 1.50% above conventional rates-because they accept higher risk. Use them only when traditional lenders reject you, not as your first choice.

Banks Versus Credit Unions and Private Lenders

Credit unions consistently offer better rates than the Big Five banks for borrowers with solid credit and stable income. A credit union saves you money without sacrificing service quality; many offer the same pre-approval timelines and closing processes as major banks. Private lenders serve a specific purpose: they approve mortgages when your credit score or income situation falls outside conventional lending criteria. However, their higher rates mean you should exhaust bank and credit union options first. Mortgage brokers occupy a middle ground, accessing multiple lenders simultaneously and often absorbing their commission from the lender’s side, making their service free to you.

Getting Pre-Approvals and Rate Quotes

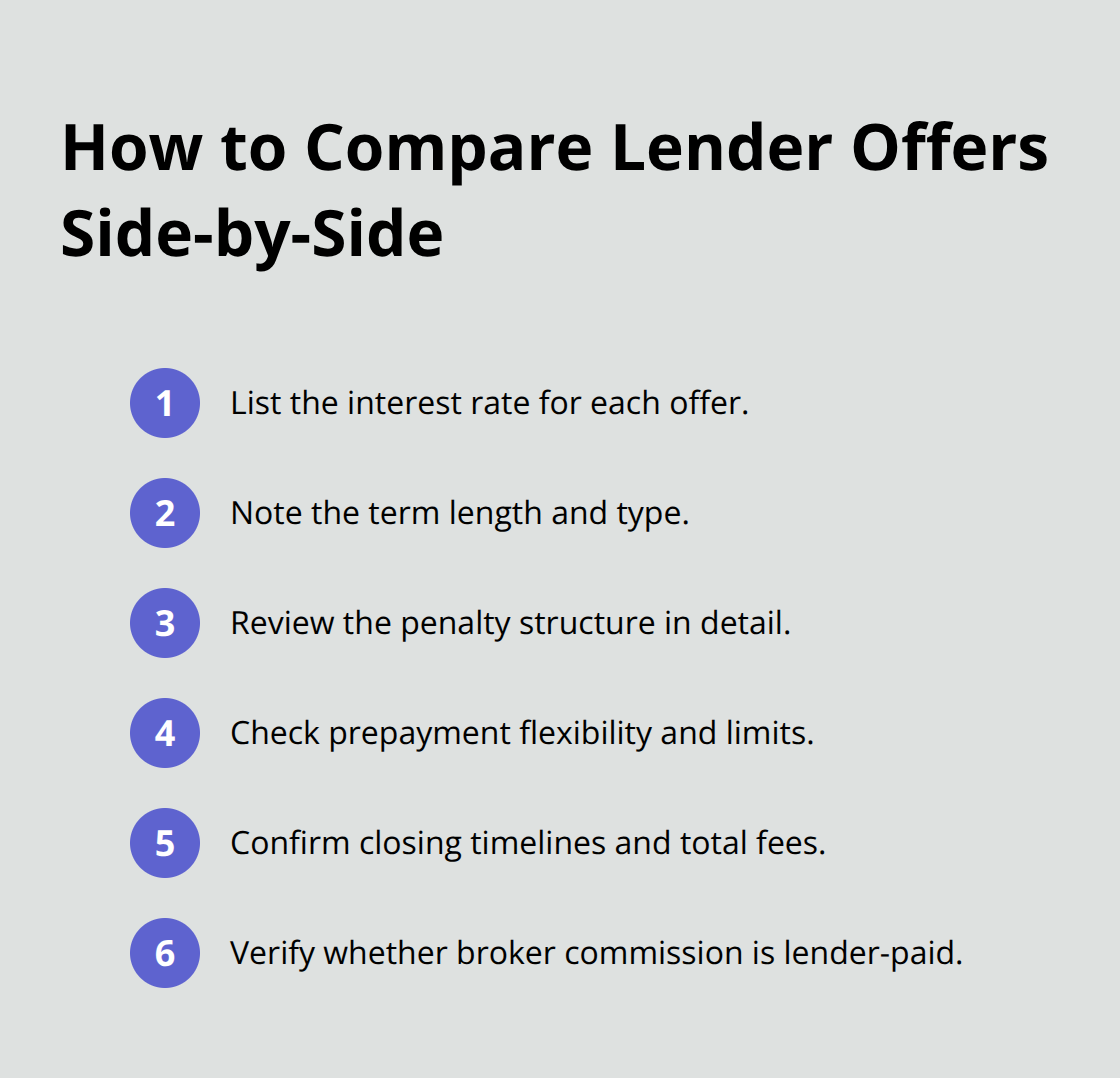

The real leverage comes from collecting competing offers simultaneously. Request pre-approvals from at least three institutions on the same day, because rates shift constantly and timing matters. Don’t assume your primary bank offers the best rate; borrowers often save $200+ monthly simply by switching to a credit union for the same mortgage terms.

Once you have multiple pre-approvals in hand, compare not just the interest rate but the penalty structure and prepayment terms. Some lenders let you pay down your mortgage without penalty; others charge three months’ interest or apply an interest rate differential. Ask each lender explicitly about these terms because they rarely volunteer the information.

Tools and Resources for Mortgage Comparison

CMHC’s Affordability Calculator helps you understand how much you can borrow before approaching lenders, preventing wasted applications on homes outside your range. This calculator removes guesswork and focuses your search on realistic price points. Mortgage brokers can accelerate the comparison process by shopping multiple lenders at once, saving time if you’re willing to pay a 0.50% fee split between you and the lender (though many brokers absorb this cost entirely from the lender’s side). Compare offers side-by-side using a simple spreadsheet: list the rate, term, penalty structure, and prepayment flexibility for each lender. This approach reveals which lender truly offers the best value, not just the lowest headline rate.

Final Thoughts

Your choice of mortgage type matters far less than matching it to your actual financial situation. If you have stable income, solid emergency savings, and plan to stay in your home for five years or longer, a fixed-rate mortgage near 3.94% eliminates payment uncertainty and lets you budget confidently. If you can absorb rate fluctuations and expect to move or refinance within three to five years, a variable mortgage at Prime minus 0.95% offers genuine savings potential. Hybrid mortgages work best when you’re genuinely uncertain about rate direction but want some protection without sacrificing all upside.

Your credit score, down payment, and debt-to-income ratio determine not whether you qualify, but at what rate and with what insurance costs. Improving any one of these metrics before applying pays dividends across your entire mortgage term (a 40-point credit score improvement or paying down existing debt by $5,000 can reduce your rate by 0.25% to 0.50%, saving thousands of dollars over 25 years). Start your homeownership journey by requesting pre-approvals from at least three lenders simultaneously and comparing their rates, penalty structures, and prepayment terms side-by-side rather than accepting the first offer.

Credit unions consistently beat the Big Five banks on Canada mortgage options, and mortgage brokers can accelerate the shopping process by accessing multiple lenders at once. CMHC’s Affordability Calculator removes guesswork about how much you can actually borrow before approaching lenders. Take time to understand your own situation before committing to any mortgage, and explore more insights about mortgages and homeownership planning with Financial Canadian.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment