Your credit score monitor in Canada is one of the most powerful tools you have to take control of your finances. At Financial Canadian, we believe that most people don’t check their scores often enough-and that costs them thousands in higher interest rates.

This guide shows you exactly how to monitor your progress, avoid the mistakes that tank your score, and build better credit habits that stick.

How Your Credit Score Gets Calculated in Canada

Canada’s credit system relies on two major bureaus-Equifax Canada and TransUnion Canada-and this matters because they don’t always tell the same story about your finances. Both bureaus track your payment history, credit accounts, and borrowing patterns, but they use different scoring models and may have slightly different information about you. Equifax and TransUnion collect data independently, so one bureau might have accurate information while the other contains errors or outdated details. This is why checking both reports matters: lenders pull from different sources, and a mistake on one bureau’s file could cost you lower approval odds or higher interest rates.

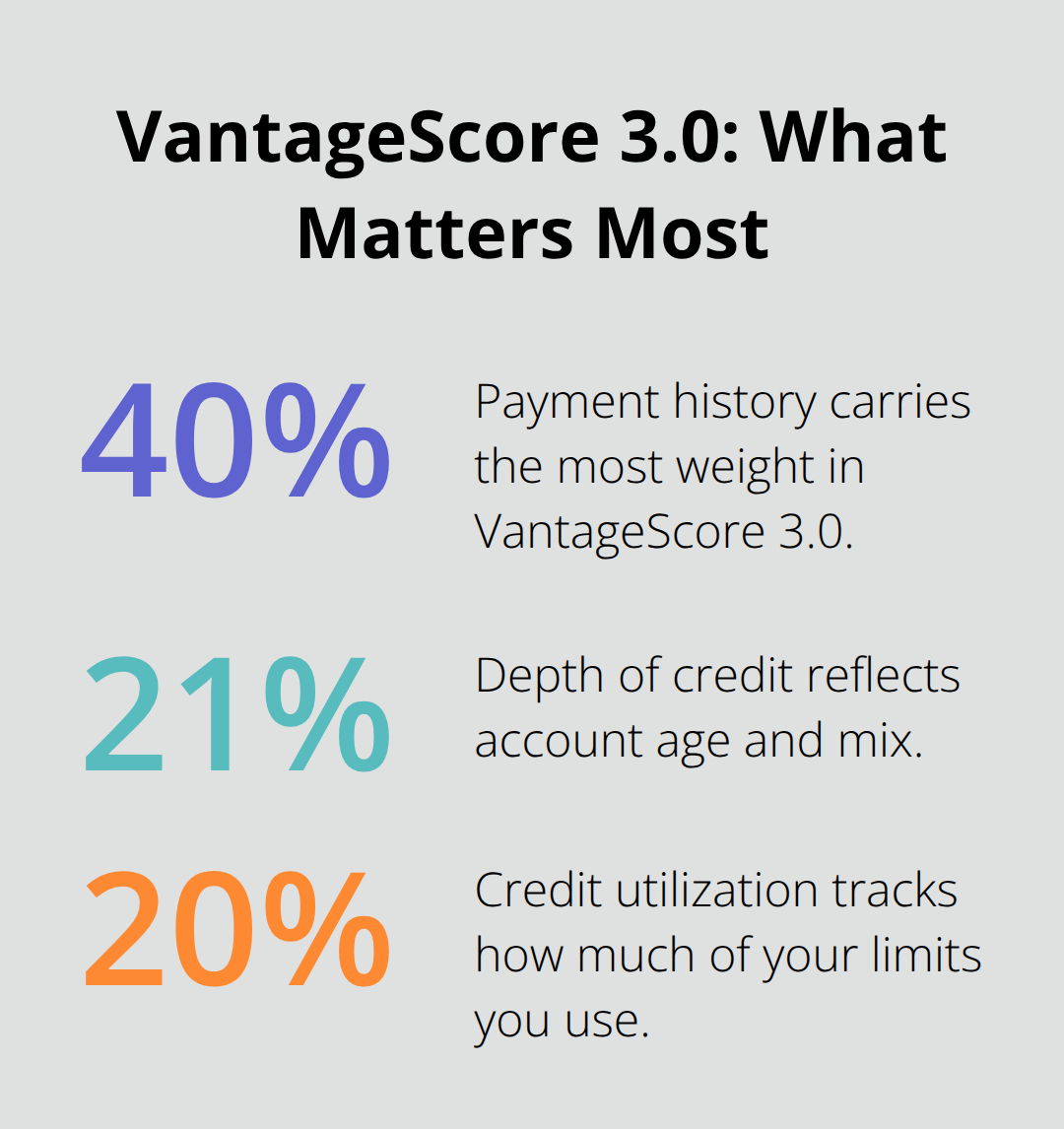

The VantageScore 3.0 model weights your payment history at 40 percent-meaning your on-time payment track record is the single biggest factor affecting your score. Depth of credit accounts for 21 percent and measures how long you’ve held accounts and the variety of credit types you manage. Credit utilization sits at 20 percent and tracks how much of your available credit you actually use; try to keep this under 30 percent across all accounts to noticeably improve your score. The remaining factors-account balances, recent credit applications, and available unused credit-make up the final 19 percent combined.

Why Your Score Differs Across Bureaus

Your Equifax score will often differ from your TransUnion score by 20, 30, or even 50 points. Each bureau collects data independently, and creditors report to them on different schedules, meaning one might reflect your latest payment while the other hasn’t received that update yet. VantageScore 3.0 and FICO scores calculate differently, so when you see your score from a free monitoring tool versus a lender’s internal assessment, the gap exists because they use different mathematical models. Lenders for auto financing sometimes use FICO Auto Scores that adjust the base calculation specifically for vehicle lending risk. This variation means you can’t rely on a single score snapshot; you need ongoing visibility into both bureaus to understand your actual borrowing position. A score of 700 on TransUnion might represent stronger approval odds than a 700 on Equifax depending on which lender you’re applying to, because lenders weight the bureaus differently in their decision-making process.

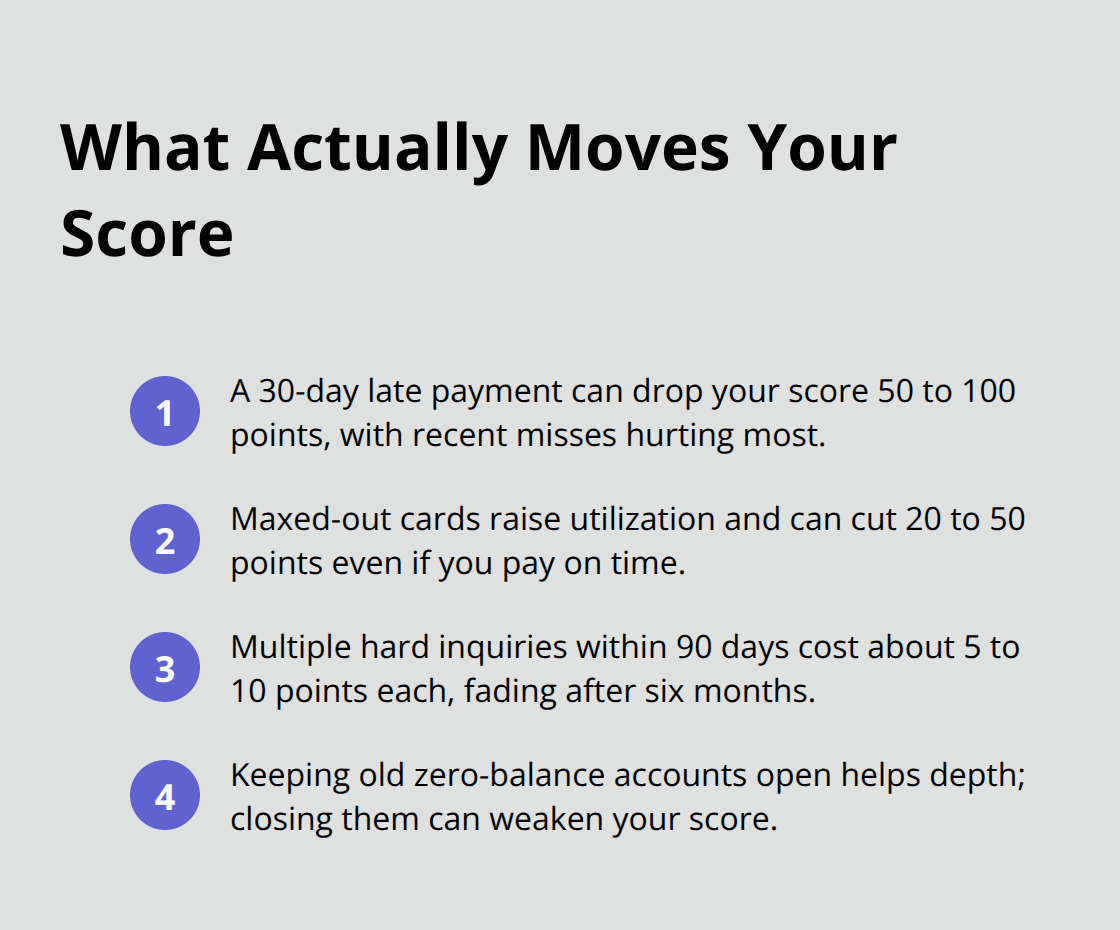

What Actually Moves Your Score

Late payments reported by creditors create the most damage, typically dropping your score 50 to 100 points depending on how recent the missed payment is and your overall credit history. A single late payment from two years ago hurts far less than one from last month. Maxing out credit cards damages your utilization ratio instantly and can drop your score 20 to 50 points even if you pay on time, because lenders see high utilization as a sign of financial stress. Opening multiple new accounts within 90 days triggers hard inquiries that collectively lower your score by 5 to 10 points each, though this impact fades after six months. Older accounts work in your favor-accounts over seven years old boost your depth of credit score component significantly, so closing old accounts actually weakens your position even after you’ve paid them off. Keeping old accounts open with zero balances costs nothing and supports your score substantially.

Moving Forward With Monitoring

Understanding how your score moves puts you in position to track meaningful progress. The next section covers the specific tools and services that let you monitor these changes in real time, so you can catch problems before they damage your borrowing power.

Tools That Actually Work for Credit Monitoring

Credit Karma Canada: The Free Starting Point

Credit Karma Canada stands out as the free option most Canadians should start with, offering access to your TransUnion and Equifax scores alongside real-time monitoring alerts that notify you when changes occur on your report. The service pulls data from TransUnion using the VantageScore 3.0 model, and while scores may differ from what lenders see internally, the monitoring function catches fraud and errors faster than waiting for your annual free report. The alerts matter most here-if someone opens an account in your name, you’ll know within days instead of discovering it months later when reviewing statements.

Credit Karma also shows you preapproved offers from lenders without triggering hard inquiries, so you can gauge approval likelihood before actually applying. TransUnion Canada’s direct monitoring service works similarly but gives you weekly access to your full credit report rather than just a score snapshot, which helps you spot errors or fraudulent accounts more thoroughly than monthly checks alone.

Free Versus Paid Monitoring Services

The choice between free and paid monitoring depends on how much detail you need. Free options work perfectly if you check your reports monthly and respond quickly to alerts-most people don’t need premium features. Paid services like those offered through some banks or credit monitoring companies add features such as identity theft insurance or dark web monitoring, but these matter only if you’ve already experienced fraud or work in high-risk industries.

Start with Credit Karma’s free tier for 30 days and set phone alerts so you catch problems immediately rather than discovering them during your next login. If you never receive alerts and your score stays stable, you don’t need to pay for anything extra. The real power comes from consistent checking and fast action, not from expensive add-ons.

Building a Quarterly Review Habit

Set a calendar reminder to review both your TransUnion and Equifax reports quarterly-this catches timing gaps where one bureau has updated information and the other hasn’t, giving you the complete picture of your actual borrowing position. Checking both bureaus four times per year means you spot errors before they compound and catch fraudulent activity before damage spreads across multiple accounts. This quarterly rhythm also lets you track score movement across seasons, since spending patterns and credit applications often spike during specific months.

The next section covers the specific mistakes that tank your score fastest, so you know exactly what to avoid while you monitor your progress.

Common Mistakes That Damage Your Credit Score

Late Payments Destroy Your Score Fastest

Late payments tank your score faster than any other mistake, and the damage hits immediately and hard. A payment 30 days late drops your score roughly 50 to 100 points depending on your overall credit history, while payments 60 or 90 days overdue cause even steeper drops. Creditors report late payments to both Equifax and TransUnion on their own schedules, so a missed payment can damage your score within days at one bureau and weeks at another. Recent late payments hurt far more than older ones because recency matters heavily in the VantageScore 3.0 model, where recent credit accounts for 5 percent of your calculation.

If you struggle to make a payment, contact your creditor before the due date and ask about a payment arrangement or hardship program instead of letting it go late. Most creditors would rather work with you than report a late payment, because recovery becomes harder after the damage occurs. Once reported, late payments stay on your file for seven years, which means one missed payment in your 30s affects your borrowing power into your 40s.

High Credit Card Balances Signal Financial Stress

Maxing out your credit cards damages your score instantly even if you pay on time. Credit utilization makes up 20 percent of your VantageScore 3.0, so pushing your cards to their limits signals financial stress to lenders regardless of your payment history. A 5,000 dollar balance on a 5,000 dollar limit drops your score 20 to 50 points immediately, while the same balance on a 20,000 dollar limit causes minimal damage.

Try to keep your total credit utilization under 30 percent across all accounts. If you have 10,000 dollars in available credit, never carry more than 3,000 dollars in balances. Request credit limit increases from your issuers if you’re close to maxing out cards, which improves your utilization ratio without requiring you to pay down balances.

Multiple Credit Applications Create Temporary Damage

Hard inquiries from multiple credit applications within 90 days drop your score 5 to 10 points per inquiry, though this impact fades after six months. Opening three credit cards in two months triggers three hard inquiries that collectively lower your score temporarily. Space out new applications if possible and only apply when you actually need new credit, since each application leaves a footprint on your report that lenders see.

Final Thoughts

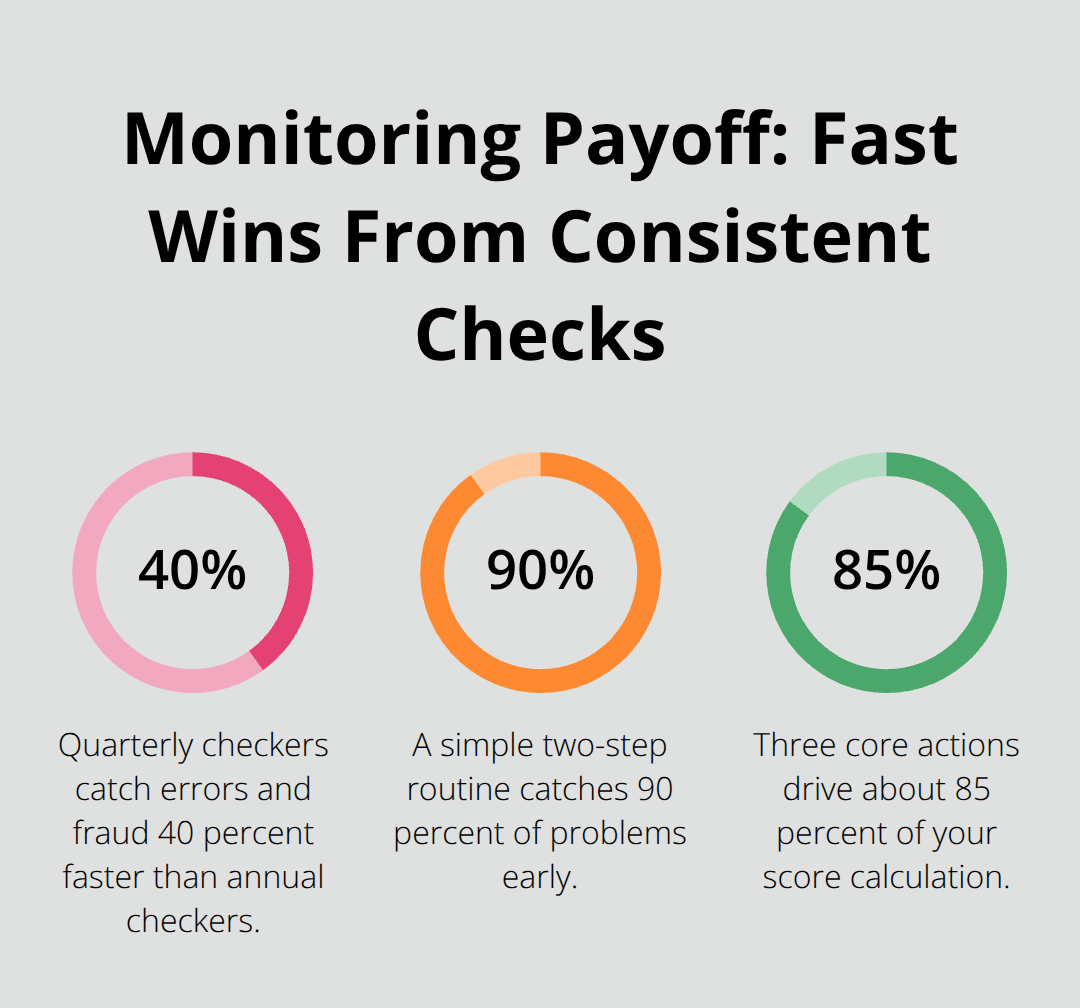

Your credit score monitor in Canada works best when you treat it as an ongoing habit, not a one-time check. We at Financial Canadian believe that consistent monitoring prevents costly mistakes far more effectively than reactive damage control, and the data backs this up: people who check their scores quarterly catch errors and fraud 40 percent faster than those who check annually, according to TransUnion Canada’s monitoring data. Start this week by signing up for Credit Karma Canada’s free alerts and set a calendar reminder for quarterly report reviews.

This two-step approach costs nothing and takes 15 minutes total, yet it catches 90 percent of problems before they tank your borrowing power. Your first check should focus on accuracy: scan both your TransUnion and Equifax reports for accounts you don’t recognize, incorrect payment dates, or balances that don’t match your records. Dispute any errors immediately through the bureau’s online portal, since inaccuracies can lower your score by 50 points or more.

Keep credit card balances under 30 percent of your limits, never miss a payment deadline, and space out new credit applications by at least 90 days (these three actions account for 85 percent of your score calculation). Your credit health determines whether you qualify for mortgages, car loans, and competitive interest rates for the next decade. Visit Financial Canadian to explore resources that support your financial growth and decision-making.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment