Your credit score directly impacts your ability to borrow money, rent an apartment, and even land certain jobs. At Financial Canadian, we’ve seen how credit score improvement in Canada transforms people’s financial lives-and it doesn’t require years of waiting.

The good news: you can boost your rating faster than you think. These seven actionable steps work because they target the factors that matter most to lenders.

1. Check Your Credit Report for Errors

Your credit report contains hundreds of data points, and errors happen frequently. Pull both your Equifax and TransUnion reports-this step costs nothing and takes about 10 minutes. Look for accounts you don’t recognize, incorrect payment statuses, duplicate entries, or wrong personal information. A single reporting error can lower your score by 50 to 100 points, so this step matters. If you spot inaccuracies, file a dispute immediately with the bureau that reported the error.

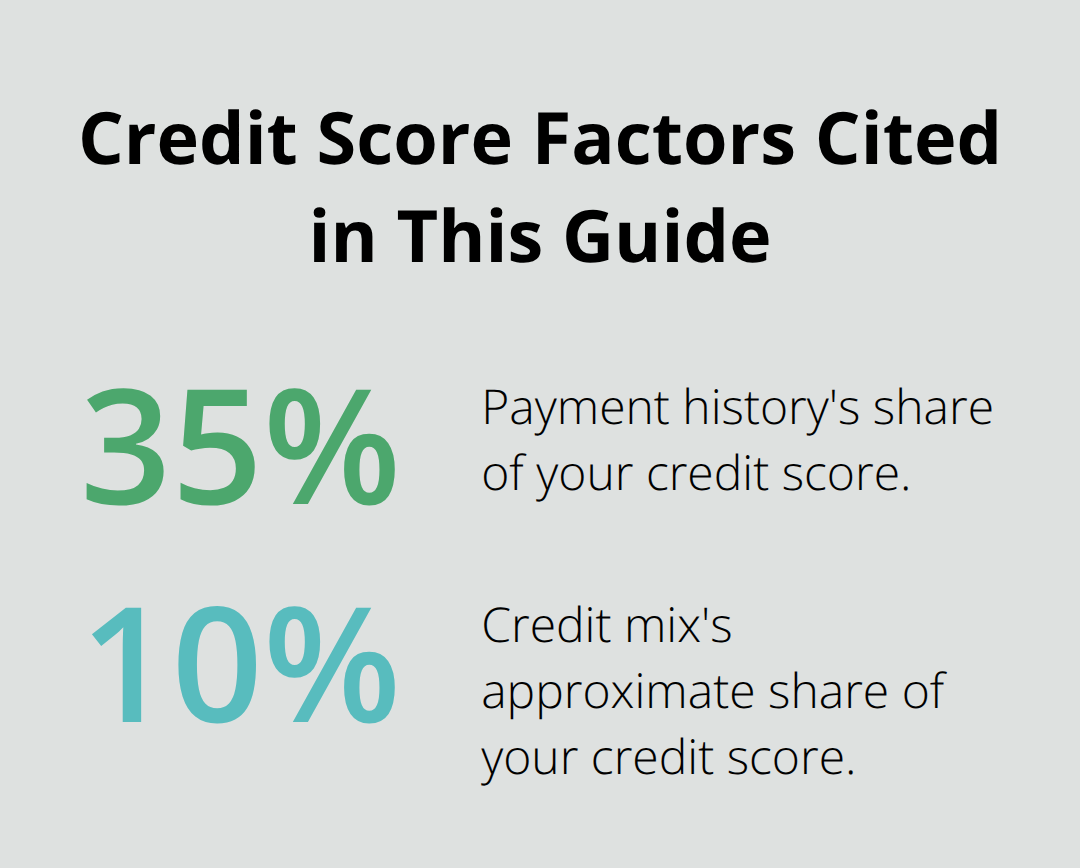

The dispute process takes 30 to 45 days, but it delivers results. Equifax and TransUnion must investigate your claim and contact the creditor or data furnisher for verification. If they cannot verify the information, they remove it from your report. Hard inquiries appear on your report when you apply for credit and typically stay for three years, while soft inquiries (like checking your own score) don’t affect your rating. Payment history makes up 35 percent of your score, so late payments listed incorrectly warrant immediate disputes-one successful dispute can improve your score by 10 to 50 points depending on what gets removed.

Check both bureaus because they sometimes maintain different information about you. Errors on one report won’t necessarily appear on the other, which means you could miss important inaccuracies if you only monitor a single bureau. This discrepancy between the two bureaus also explains why your Equifax and TransUnion scores often differ. Once you’ve cleaned up your report, the next step focuses on the behavior that matters most to lenders: your payment habits.

2. Pay Your Bills on Time Every Month

Payment history accounts for 35 percent of your credit score, making it the single most influential factor lenders examine. Even a single late or missed payment may impact your credit reports and credit scores, signaling to lenders that you’re a higher risk. The best defense is automation: set up automatic payments from your bank account for at least the minimum balance on every credit card and loan you carry. Most Canadian banks offer this service free through their online platforms, and it eliminates the human error that causes missed deadlines.

Even if you can’t pay the full balance automatically, schedule a payment for the minimum amount on the due date. This single action protects your score from the damage that late payments inflict. Late payments may remain on your credit reports for up to seven years, so a missed payment today affects your borrowing ability for years to come. If you’re carrying multiple debts with different due dates, consolidate them into a single payment day by contacting your creditors to adjust your due dates or by using your bank’s bill payment tools to schedule everything for the same calendar date. This approach removes complexity and reduces the chance of oversight that derails your credit improvement plan.

Once you’ve locked in on-time payments, your next opportunity lies in how much of your available credit you actually use. The ratio between your balances and your limits matters almost as much as paying on time, and controlling it requires a different strategy altogether.

3. Reduce Your Credit Utilization Ratio

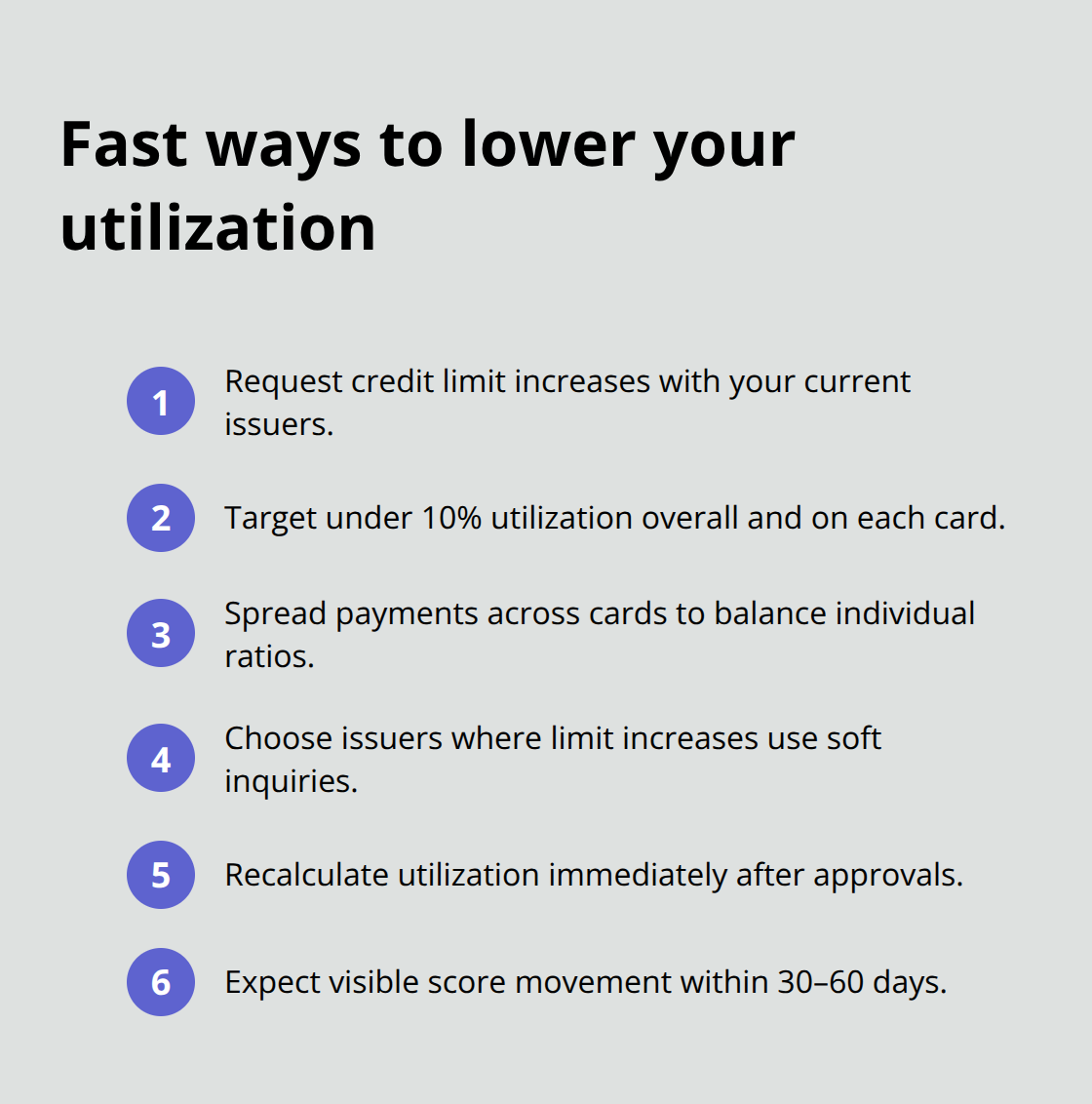

Reduce Your Credit Utilization Ratio-the percentage of your available credit you’re actively using-is often the second most important factor in calculating your credit scores, following payment history. The conventional wisdom says keep your utilization below 30 percent, but we believe that’s actually too high if you’re serious about rapid improvement. Try for below 10 percent across all your accounts combined, and you’ll see measurably faster score gains. If you have a credit card with a $5,000 limit, keep your balance under $500 at all times. This aggressive approach works because lenders interpret low utilization as a sign you don’t rely heavily on credit, which reduces their perceived risk.

The fastest way to lower utilization without paying off debt completely is requesting credit limit increases from your existing card issuers. Canadian banks like TD, RBC, and Scotiabank approve limit increases within days, and the request typically triggers only a soft inquiry that doesn’t harm your score. If you have three credit cards with $3,000 limits each and $2,000 in combined balances, your utilization sits at 22 percent-request a $3,000 increase on one card, and your utilization drops to 15 percent instantly without spending a dollar. Pay down balances strategically across multiple cards rather than zeroing out one card completely, since lenders examine both your overall utilization and individual card ratios.

This method delivers measurable score improvements within 30 to 60 days, far faster than waiting to pay down debt through regular monthly payments.

The next step involves leveraging someone else’s credit history to accelerate your own progress.

4. Become an Authorized User on Someone Else’s Account

Adding yourself as an authorized user on someone else’s credit card account transfers their payment history to your credit report, which can boost your score significantly within 30 to 60 days. This works because the card issuer reports the entire account history-including years of on-time payments-to your credit file, and lenders weight established payment patterns heavily in their scoring models. The effect is strongest when the account has a long credit history with perfect payments and a low balance relative to the credit limit. Ask a family member or trusted friend with a credit score above 750 to add you to their card, and your score can jump 50 to 100 points depending on the account’s age and payment record. You don’t need physical access to the card or permission to make purchases; you simply benefit from their established credit behavior.

Card issuers typically report authorized user accounts within one to two billing cycles, so you’ll see results faster than any other credit-building method. However, not all Canadian banks treat authorized users equally-some report them to both bureaus, while others report to only one, which means your Equifax and TransUnion scores may improve at different rates. TD, RBC, and Scotiabank all report authorized user accounts reported to credit bureaus to both Equifax and TransUnion, making them reliable choices if you pursue this strategy. Verify with the cardholder’s bank before committing, since this detail directly impacts how much your score will improve. The relationship requires trust, since the cardholder’s future late payments or increased balances will also appear on your report and drag down your newly improved score.

Once you’ve secured an authorized user spot, you can accelerate progress further through a dedicated credit-building product designed specifically for people starting from scratch.

5. Build Credit History With a Secured Credit Card

A secured credit card is the fastest way to establish credit from scratch or repair a damaged score, and it works fundamentally differently from the authorized user strategy. You deposit cash into a savings account held by the bank, then receive a credit card with a limit matching your deposit-typically between $500 and $2,500. The bank reports your monthly payments to both Equifax and TransUnion, building a positive payment history that demonstrates you can handle credit responsibly. Capital One Secured and Scotiabank Secured Card are the most accessible options for Canadian applicants, with approval decisions within days regardless of your starting credit score. Use the card for small purchases each month (groceries, gas, or utilities) and pay the full balance before the due date to maximize your score improvement.

After 12 to 18 months of perfect on-time payments, most issuers automatically graduate you to an unsecured card and return your deposit. The timeline depends on your bank and how consistently you manage the account, but banks reward disciplined behavior with faster upgrades. During those months with the secured card, your score typically climbs if you maintain zero missed payments and keep your utilization below 10 percent of your limit. Never carry a balance month-to-month or miss a single payment, since the entire purpose of this strategy collapses if you repeat the behaviors that damaged your credit initially. This method works slower than the authorized user approach but delivers permanent credit history that remains on your report for years after you graduate to unsecured products.

Once you’ve established a track record with secured credit, the next step involves mixing different types of credit to signal financial maturity to lenders.

6. Diversify Your Credit Mix

Lenders examine more than payment history and utilization-they want to see you manage different types of credit responsibly. Credit mix accounts for approximately 10 percent of your credit score, which means it matters less than payment history or utilization, but it still influences lending decisions. Revolving credit (credit cards and lines of credit where you borrow, repay, and borrow again) differs from installment credit (loans with fixed payments over a set period), and lenders value both. If your credit file shows only credit cards, adding an installment loan or line of credit signals that you handle multiple credit structures simultaneously. This diversity tells lenders you’re not dependent on a single credit type.

The critical mistake occurs when you open new accounts purely for variety, which triggers hard inquiries that damage your score by 5 to 10 points each. If you already carry student loans, a car loan, or a mortgage, you’ve already achieved the credit mix benefit without additional applications. Build credit mix naturally through your financial needs rather than artificially creating accounts-if you need a personal loan to consolidate debt or a line of credit for emergencies, that timing serves dual purposes. Space any new applications at least six months apart to minimize inquiry damage, and only pursue them when the underlying financial need is genuine.

The next step shifts your focus away from building new credit and toward protecting the progress you’ve already made.

7. Stop Making New Credit Applications

Every credit application triggers a hard inquiry that lowers your score by 5 to 10 points immediately. These inquiries remain visible on your credit report for three years, signaling to lenders that you’ve recently sought new credit, which raises concerns about financial desperation or overextension. Hard inquiries from credit applications also chip away at your score for about six months, so the damage compounds quickly when you apply for multiple products within a short timeframe. Most people underestimate how aggressively lenders penalize application activity, and if you’ve already completed the previous six steps, new applications will only reverse your progress. Space any future credit applications at least three months apart to allow the inquiry impact to fade and your score to stabilize at its new higher level.

The one exception involves mortgage applications within a 45-day window. Multiple mortgage inquiries from different lenders within 45 days count as a single inquiry for mortgage scoring purposes, so shopping around for the best rate doesn’t compound damage the way credit card applications do. However, this protection applies only to mortgage inquiries, not personal loans or credit cards, so don’t assume you can freely apply for multiple products within that timeframe. If you’re not actively house hunting, treat every application as a permanent score reduction that requires months of on-time payments and low utilization to recover from. The fastest path to an excellent credit score involves stopping new applications entirely until you’ve reached your target rating, then proceeding with only the credit products you genuinely need for your financial situation.

With new applications paused, your focus shifts to monitoring your progress and understanding what realistic timelines look like for credit score recovery.

Final Thoughts

Credit score improvement in Canada follows a predictable pattern when you execute these seven steps consistently. Most people see measurable gains within 30 to 60 days of implementing the strategies above, with scores typically climbing 10 to 20 points monthly through disciplined effort. The rate slows as you approach higher ratings since each additional point becomes harder to earn, and reaching 750 or above usually takes 6 to 18 months depending on your starting point.

Track your progress using free credit monitoring tools available directly from Equifax and TransUnion (both bureaus offer free annual reports, and several Canadian banks provide complimentary score monitoring through their online platforms). Monitoring both bureaus matters because they often report different scores, and lenders may rely on either one when making decisions about your application. The real victory isn’t reaching 750-it’s maintaining the financial habits that got you there.

Once your score improves, the temptation to return to old patterns intensifies, but the seven steps above become your permanent financial foundation. Keep utilization low, pay every bill on time, and avoid unnecessary credit applications. These behaviors compound over years and decades, building wealth and financial stability that extends far beyond your credit score, and we can help you establish a strong digital presence to support your financial goals.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment