Digital finance technologies are reshaping how people access banking services worldwide. The impact of digital finance on financial inclusion and stability reaches far beyond traditional banking boundaries.

We at Financial Canadian examine how mobile payments, digital lending, and identity verification systems break down barriers for underserved populations. These innovations create new pathways to financial services for millions previously excluded from the formal banking system.

How Technology Breaks Financial Barriers

Mobile money accounts in Sub-Saharan Africa demonstrate that technology bypasses traditional bank infrastructure entirely, with 21% of adults in the region having mobile money accounts, making it the global leader in mobile money usage. Digital payment platforms like Kenya’s M-Pesa moved 2% of households out of poverty between 2008-2014, while mobile money increased household consumption by 44% in Mozambique during flood emergencies. These platforms work because they require only basic mobile phones and local agent networks, not expensive bank branches.

Mobile Payment Revolution Changes Everything

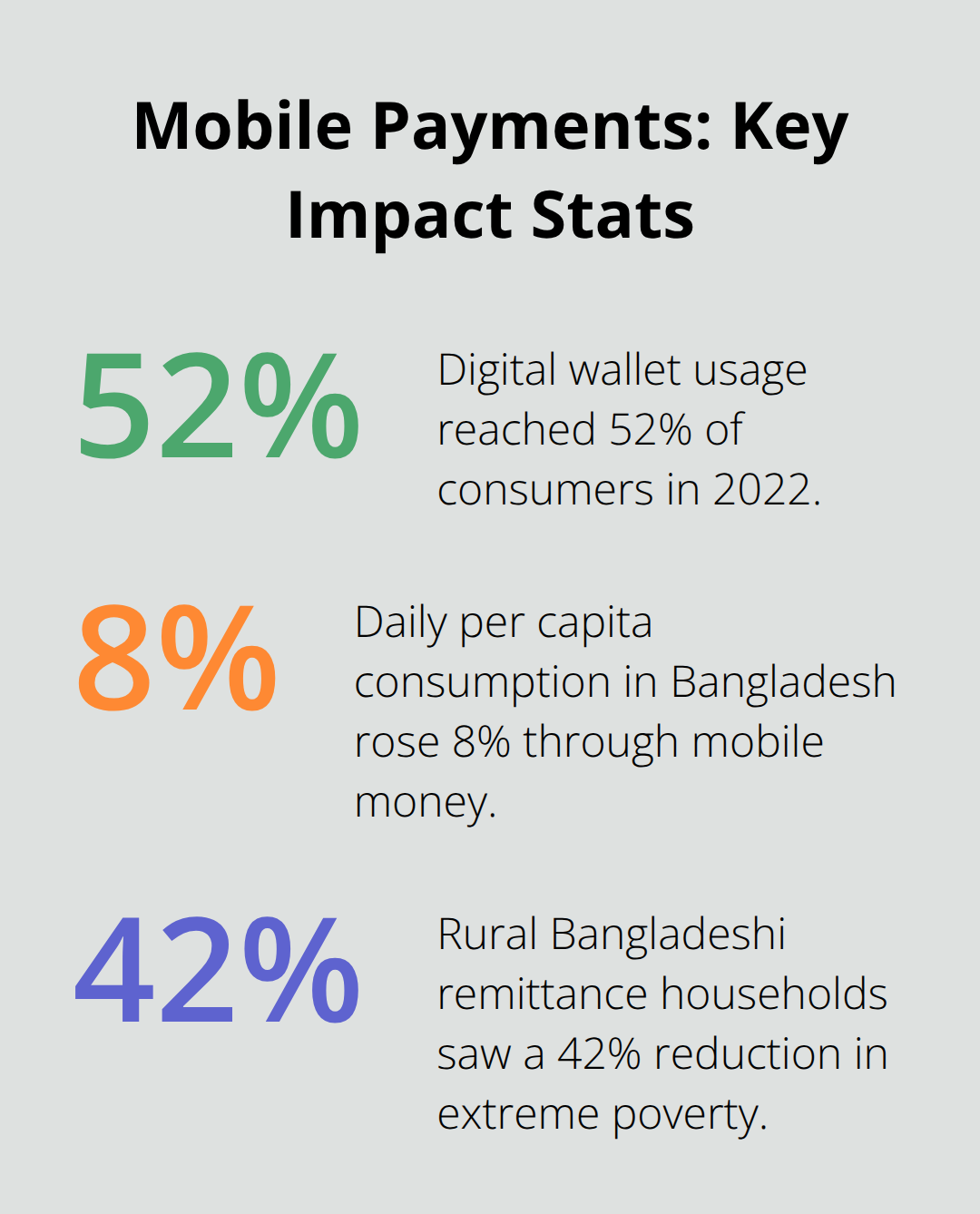

The numbers tell the real story. Digital wallet usage jumped to 52% of consumers in 2022 according to Statista, while mobile banking users surpassed 1.2 billion globally. Countries that implement government-to-person payments through mobile platforms see immediate financial inclusion gains.

Bangladesh saw daily per capita consumption rise 8% through mobile money, with rural households that receive remittances experiencing a 42% reduction in extreme poverty. Mobile payments cut transaction costs by up to 20% compared to traditional remittance methods (according to the Better Than Cash Alliance).

Digital Lending Opens Credit Access

Fintech companies use alternative data for credit scoring and reach small businesses in developing countries that face a finance gap of $5.7 trillion in emerging markets and developing economies. Peer-to-peer platforms eliminate bank intermediaries entirely, while AI-powered credit models analyze mobile usage patterns, utility payments, and social data to assess creditworthiness. These automated systems process loan applications in minutes rather than weeks, which makes microfinance scalable for millions whom traditional banks ignore.

Identity Verification Solves Documentation Problems

Digital identity systems that use biometric data and blockchain technology eliminate the documentation barriers that exclude 1.7 billion unbanked adults worldwide (according to World Bank figures). Mobile-based KYC solutions verify identity through facial recognition, fingerprints, and government database connections, which reduces onboarding costs by 90% while meeting regulatory requirements. Countries that implement digital ID systems see immediate jumps in formal financial service adoption rates.

These technological advances create the foundation for broader financial inclusion, but their real impact becomes clear when we examine how they transform access for specific underserved communities across different regions and demographics.

Who Benefits Most From Digital Finance

Digital finance transforms specific communities that traditional banks consistently fail to reach. Rural populations in Northern Uganda experienced a 45% increase in food security through mobile money services, particularly households located far from brick-and-mortar banks. Ghana’s mobile money adoption demonstrates how remote areas adopt digital finance faster than urban centers when infrastructure limitations disappear.

Remote Areas Skip Traditional Bank Infrastructure

Rural communities bypass expensive bank branch networks entirely through agent networks that convert cash into digital value. Countries with vast rural populations like Bangladesh and Kenya demonstrate that mobile money agents who operate from small shops create financial access points every few kilometers. These agents process transactions with basic smartphones and earn commission income while they serve communities that banks consider unprofitable.

The agent network model reduces operational costs by 80% compared to traditional branches while it provides services directly in remote villages. Small businesses in these areas access capital through digital platforms that analyze transaction histories rather than require collateral or credit scores.

Women Gain Economic Independence Through Mobile Access

Mobile money accounts close the gender gap in financial access because women control their own devices and transactions without male family member approval. Mobile banking has emerged as an important means to increase financial inclusion of women in developing countries. Digital platforms enable women entrepreneurs to receive payments, build credit histories, and access microfinance without visits to physical bank locations.

The convenience factor proves decisive since women often face mobility restrictions or lack time for bank visits during business hours. Female-owned small businesses that adopt mobile payment systems report 25% higher revenue growth rates than cash-only operations.

Small Businesses Access Capital Without Collateral

Digital platforms analyze transaction data, utility payments, and mobile usage patterns to assess creditworthiness for small business owners who lack traditional credit histories. Fintech companies process loan applications in minutes rather than weeks, which makes microfinance scalable for millions whom traditional banks ignore. Small retailers and service providers build credit scores through consistent mobile money transactions, which opens doors to larger loans and business expansion opportunities.

These success stories highlight how digital finance creates opportunities, but implementation faces significant obstacles that threaten to limit its transformative potential.

What Stops Digital Finance From Reaching Everyone

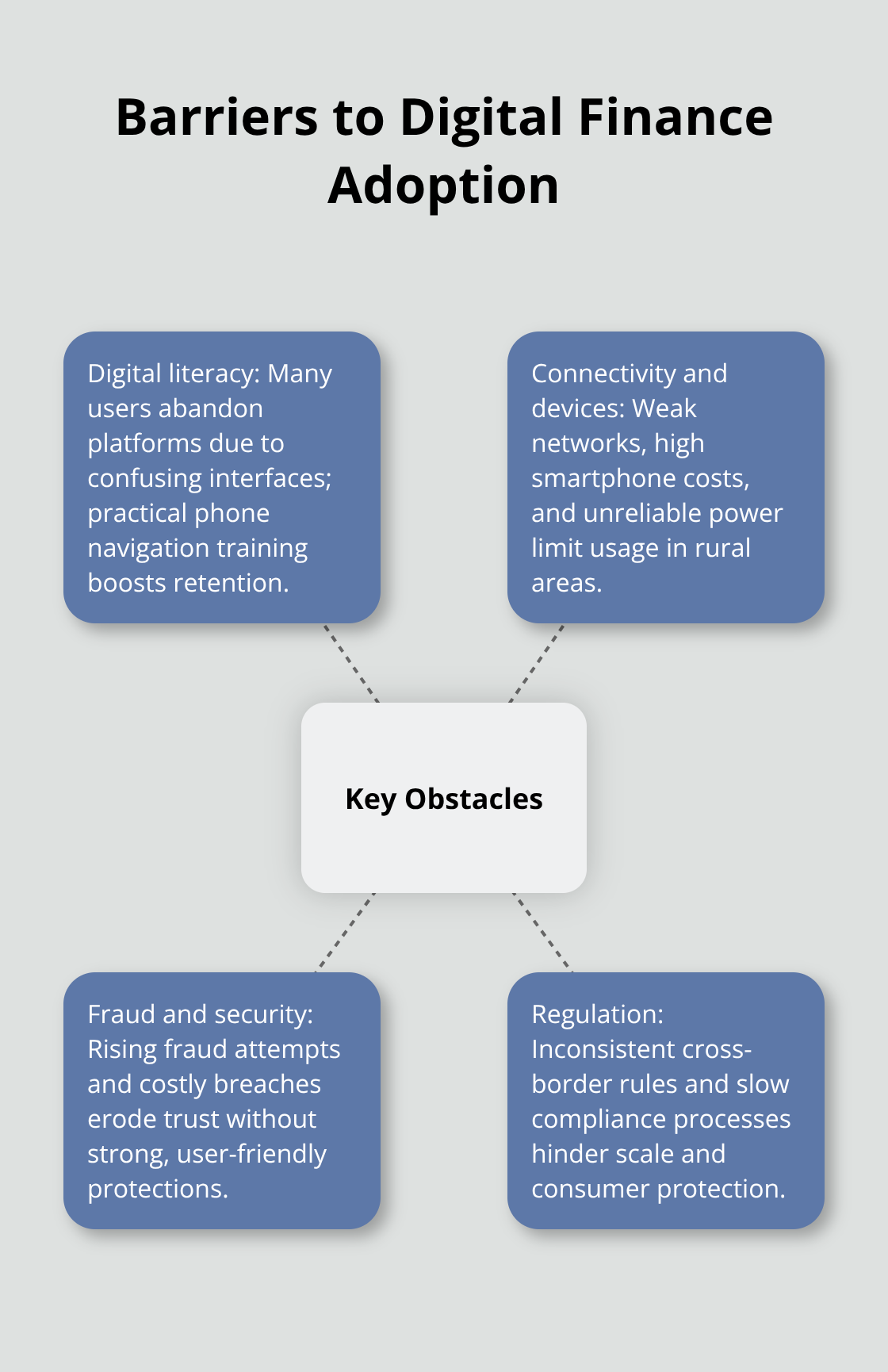

Digital literacy barriers prevent many adults from using mobile financial services effectively, despite 84% of adults in low and middle-income countries owning mobile phones. Most people abandon digital finance platforms within the first month due to interface confusion and fear of making costly mistakes.

Training programs that focus on practical phone navigation skills rather than theoretical financial concepts show 85% higher retention rates. Countries like Rwanda address this challenge through community-based digital literacy programs that teach mobile money operations in local languages with familiar transaction scenarios.

People need hands-on practice with actual transactions in safe environments before they trust digital platforms with their money. The gap between technology availability and user capability creates the biggest obstacle to widespread adoption.

Technology Access Creates Geographic Divides

Rural areas face network connectivity issues that make digital transactions unreliable or impossible. Poor internet infrastructure forces users to travel to urban centers for basic financial services, which defeats the convenience purpose of digital platforms.

Smartphone costs remain prohibitive for low-income populations who earn less than $2 daily. Basic feature phones support limited financial applications, while smartphones that handle complex banking apps cost 3-6 months of average income in developing countries.

Power grid instability in remote regions means users cannot charge devices consistently. Solar charging stations and battery-sharing programs help address this challenge, but coverage remains spotty across most rural areas.

Fraud Threatens User Trust and Platform Adoption

Cybersecurity incidents cost mobile money providers an average of $4.44 million per breach, but user trust damage creates longer-term problems. Kenya’s mobile money ecosystem processes over $50 billion annually, yet fraud attempts increase by 15% each year as platforms scale.

Effective fraud protection requires real-time transaction monitoring, SMS authentication, and spending limits that users can adjust themselves. Countries that implement national digital identity systems connected to mobile money accounts reduce fraud rates by 60% compared to platforms that rely only on phone number verification.

Consumer education about phishing scams and secure PIN practices proves more effective than complex security features that confuse users. Simple security measures that users understand and control build more trust than sophisticated systems they cannot navigate.

Regulatory Gaps Allow Exploitation

The regulatory framework challenge centers on speed versus safety: regulators who require extensive compliance checks delay market entry for legitimate providers while creating space for unregulated operators who exploit vulnerable users.

Cross-border payment regulations vary dramatically between countries, which makes remittances expensive and complicated. Inconsistent rules force providers to maintain separate systems for each market rather than scale efficient solutions across regions.

Consumer protection laws lag behind technology development (particularly in emerging markets), which leaves users vulnerable to predatory practices. Weak dispute resolution mechanisms mean customers have little recourse when transactions go wrong or accounts get compromised.

Final Thoughts

Digital finance transforms financial inclusion through measurable economic improvements that extend far beyond payment processing. Mobile money platforms lifted 2% of Kenyan households out of poverty while they reduced extreme poverty by 42% for rural Bangladeshi families who receive remittances. The impact of digital finance on financial inclusion and stability creates real pathways to economic opportunity for millions of previously excluded individuals.

Success depends on three core elements that work together: reliable technology infrastructure, comprehensive user education, and balanced regulatory frameworks. Countries that combine agent networks with digital literacy programs achieve 85% higher user retention rates than those that focus solely on technology deployment. Rwanda’s community-based approach proves that local language instruction builds trust and drives adoption rates significantly higher.

The future expands access as smartphone costs drop and network coverage improves across developing regions. Blockchain identity systems will eliminate documentation barriers for 1.7 billion unbanked adults worldwide (according to World Bank data). We at Financial Canadian help businesses navigate digital transformation through our web design services that connect financial service providers with underserved communities effectively.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment