Mortgage rates in Canada have shifted significantly, and 2026 brings new decisions for homeowners and borrowers. Whether you’re locked into a fixed rate, managing a variable mortgage, or planning your next move, understanding the current landscape is essential.

At Financial Canadian, we’ve put together this guide to help you navigate mortgage rates Canada 2026 and adjust your strategy accordingly. The decisions you make now can save you thousands in interest payments over the life of your mortgage.

Where Mortgage Rates Stand in April 2026

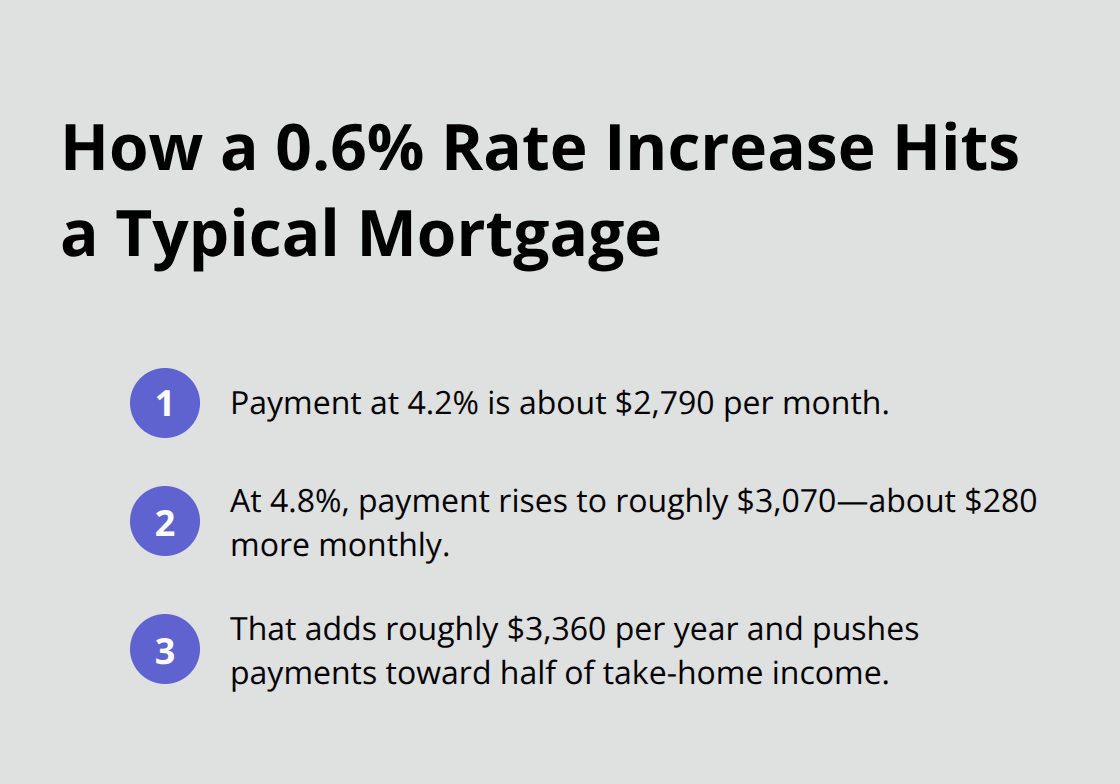

As of April 9, 2026, Canadian mortgage rates sit at a critical juncture. The 5-year fixed rate averages 4.52% across major lenders, with the lowest insured option at 3.99% according to current market data. Shorter terms tell a different story: 1-year fixed sits at 5.25%, while 2-year and 3-year fixed rates hover around 4.58% to 4.62%. These rates reflect the Bank of Canada’s policy rate of 2.25%, set in March 2026 with the next decision coming April 29. The spread between short and long-term rates signals what lenders expect about future inflation and economic growth. A typical Canadian household with a $520,000 mortgage at 4.2% over 25 years faces monthly payments around $2,790, with roughly $1,820 going to interest in the early years. For a family earning the median after-tax income of about $6,180 monthly, this mortgage payment consumes roughly 45% of take-home pay.

The Bank of Canada’s Cautious Stance

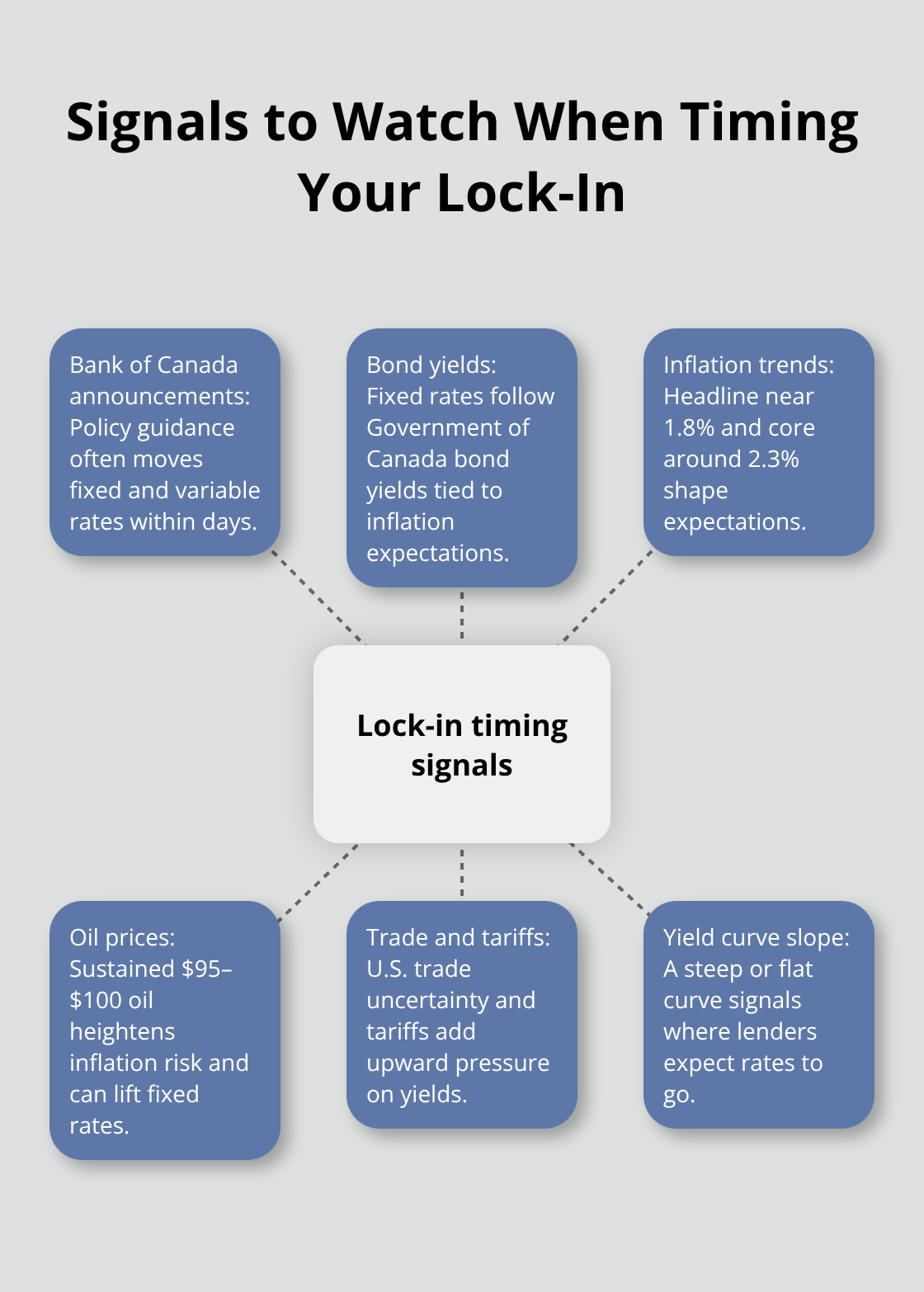

The Bank of Canada holds the policy rate at the low end of its neutral range of 2.25% to 3.25%, signaling a pause rather than aggressive cuts or hikes. Major Canadian banks including RBC, TD, Scotiabank, BMO, and CIBC all expect the policy rate to remain near 2.25% through 2026, with potential increases toward 2.75% to 3.25% by 2027. Fixed rates don’t automatically track the policy rate-they follow bond yields instead, which respond to inflation expectations and global economic sentiment. Canada’s headline inflation cooled to 1.8% in early 2026 with core inflation around 2.3%, but tariffs and oil-price volatility keep upward pressure on long-term yields. If oil sustains above $95 to $100 per barrel, inflation risks rise and fixed rates could spike regardless of BoC decisions. Variable-rate mortgages move with the prime rate, which currently sits around 4.45%. The disconnect between fixed and variable rates creates genuine strategic choices for borrowers.

Fixed Versus Variable: The 2026 Reality

Fixed-rate mortgages lock your payment in place for the term, protecting you if rates climb but costing more upfront if they fall. Variable-rate mortgages tie your rate to the lender’s prime rate, so payments can fluctuate. In April 2026, the spread between them is wide enough to matter. A variable-rate discount off prime typically sits 0.5% to 1.0% below the posted 4.45% prime, making variables attractive for borrowers who can handle payment uncertainty. However, here’s the practical truth: if the Bank of Canada raises rates toward 3.0% or higher by late 2026 or 2027, variable-rate payments will increase. The current rate path suggests modest moves, not aggressive hikes, but tariffs and trade uncertainty with the U.S. could change that calculus.

The Case for Shorter Fixed Terms

Many borrowers are increasingly choosing shorter fixed terms like 2 or 3 years as a balanced option. You lock in payment certainty now while keeping the ability to refinance in 2 to 3 years if rates have fallen or stabilized at a lower level. This strategy avoids the rate-forecasting trap while maintaining flexibility. The February 2026 labour market weakened with unemployment rising to 6.7%, which typically eases rate-hike pressure, but wage growth accelerated to 4.2%, complicating the inflation picture. These mixed signals mean that locking in for a shorter period protects you from immediate payment shock while leaving room to adapt if conditions shift. The next BoC decision on April 29 will provide more clarity on the central bank’s inflation assessment and rate trajectory for the remainder of 2026.

Impact on Mortgage Holders and Borrowers

What Rate Increases Cost You Monthly

Rising rates hit your wallet immediately if you renew or refinance in 2026. A $520,000 mortgage at 4.2% costs $2,790 monthly over 25 years. If rates climb to 4.8% on renewal, that same mortgage jumps to roughly $3,070 per month-an extra $280 you need to find every month, or $3,360 annually.

For the median Canadian household taking home about $6,180 monthly after tax, that increase alone pushes your mortgage payment from 45% to nearly 50% of take-home income, leaving less room for other expenses.

The impact compounds over time. Equifax data shows 28% of homeowners renewing in 2025 switched to better deals, and Mortgage Professionals Canada reported a 46% year-over-year surge in rate-shopping activity. That trend accelerates in 2026 because the stakes are real. If you renew soon, shopping across multiple lenders isn’t optional-it’s how you recover thousands. The lowest insured 5-year fixed currently sits at 3.99% versus the 4.52% average, meaning active shopping nets you roughly $20 to $40 monthly savings on a $520,000 mortgage. Over a five-year term, that’s $1,200 to $2,400 back in your pocket.

Labour market weakness in February 2026, with unemployment rising to 6.7%, suggests the Bank of Canada may hesitate on rate hikes, but don’t rely on that hope. Shop now, lock in what’s available, and move fast because rate holds expire quickly.

The Refinancing Trap: When Breaking Your Mortgage Costs Too Much

Refinancing carries real risks that borrowers often overlook. If you break a closed mortgage early to refinance, lenders charge either interest rate differential or three months’ interest-sometimes both. On a $520,000 mortgage, three months’ interest at 4.2% equals roughly $5,460. You need rates to drop significantly to justify that cost. A fall from 4.2% to 3.8% saves only $165 monthly, so you’d need nearly 33 months to recover the penalty. That math only works if you plan to stay in the home for years and rates fall sharply, neither guaranteed in 2026.

For renewals, the picture differs entirely-no penalty applies, so refinancing to a better rate is pure gain. The strategic move involves timing your renewal carefully around Bank of Canada announcements. The next decision comes April 29, 2026, and major banks expect the policy rate to hover near 2.25% through 2026 with potential increases toward 2.75% to 3.25% by 2027. If the April 29 announcement signals pause or caution, fixed rates may stabilize or dip slightly, making that an ideal moment to lock in. Conversely, if the Bank of Canada hints at future hikes, rates typically spike before any actual move happens.

Timing Your Lock-In Around Economic Signals

Don’t wait for cuts that may not arrive-secure your rate when the economic signals align. For new mortgage applications, shorter terms protect you from this uncertainty. A 2 or 3-year fixed lets you refinance in 2026 or 2027 if conditions improve, avoiding the trap of locking into today’s rates for five years when tariffs and trade tensions could ease by 2028.

The decision between refinancing now and waiting hinges on three factors: your current rate, the penalty cost, and your time horizon in the home. If you’re within 12 months of renewal, refinancing early rarely makes sense unless rates have fallen more than 0.5%. If you’re three or more years away, monitor the BoC’s inflation assessments and bond-market sentiment quarterly. The spread between short-term and long-term rates tells you what lenders expect-a steep curve suggests they anticipate rate stability or eventual declines, while a flat curve signals uncertainty.

Your next decision point arrives when you understand how much flexibility you actually need in your mortgage structure.

How to Adjust Your Mortgage Strategy in 2026

Lock In Around Bank of Canada Announcements

The Bank of Canada announcements on April 29 marks your first strategic checkpoint. If the central bank signals pause, fixed rates may stabilize within days, creating a window to lock in before sentiment shifts. If it hints at future rate increases, rates typically spike before any actual hike occurs, so locking in immediately becomes the smarter move. The practical reality is that waiting for perfect timing costs more than acting decisively around economic announcements. For borrowers renewing in the next six months, the math favors locking now rather than gambling on rate declines that major banks don’t expect. Major banks expect the policy rate to hover near 2.25% through 2026 with potential increases toward 2.75% to 3.25% by 2027, meaning rates are more likely to rise than fall.

A 5-year fixed at 4.52% average or lower insured rates at 3.99% protect you against that trajectory. If you’re not renewing until 2027, a 2 or 3-year fixed term at today’s 4.58% to 4.62% rates keeps you flexible while avoiding the trap of locking into five years at the top of the rate cycle.

Shop Across Multiple Lenders to Find Real Savings

Shop across at least five lenders because the difference between the lowest insured rate at 3.99% and the 4.52% average equals roughly $200 to $300 annually on a $520,000 mortgage. That gap widens on larger mortgages, making active comparison non-negotiable. A $520,000 mortgage renewed at 4.5% instead of 4.8% saves $155 monthly or $1,860 annually. Most lenders allow you to lock in a rate hold for 120 days without penalty, giving you time to shop and decide without pressure.

Contact at least three mortgage brokers and four banks directly because brokers access lenders that direct customers cannot, and banks sometimes offer better rates to new renewals than to existing clients. Mortgage Professionals Canada reported a 46% year-over-year surge in rate-shopping activity in 2025, and that momentum accelerates in 2026 because the savings are substantial.

Evaluate Early Refinancing Costs Carefully

Breaking a closed mortgage early to refinance only makes sense if rates drop more than 0.75% and you plan to stay in the home for at least three more years. Three months’ interest on a $520,000 mortgage at 4.2% costs roughly $5,460, so a 0.4% rate reduction saves only $165 monthly and requires 33 months to recover that penalty. The exception is if you locked in at 5% or higher during a recent renewal-then a 0.75% drop to 4.25% saves $260 monthly and justifies the penalty within 21 months.

For renewals without early-break penalties, the decision simplifies entirely: shop aggressively and switch if another lender offers 0.3% or more below your current rate. This approach costs nothing and puts thousands back in your pocket over the term.

Use Rate Paths to Guide Your Timing

Build your decision on concrete rate paths from major banks and the timing of Bank of Canada announcements, not on hope. This trajectory means rates are more likely to rise than fall, so locking in sooner rather than later protects your payment stability. The spread between short-term and long-term rates tells you what lenders expect-a steep curve suggests they anticipate rate stability or eventual declines, while a flat curve signals uncertainty about the path ahead.

Final Thoughts

Your mortgage strategy in 2026 hinges on three concrete decisions: locking in rates around Bank of Canada announcements, shopping across multiple lenders to capture real savings, and understanding when refinancing penalties justify the cost. Major banks expect the policy rate to stay near 2.25% through 2026 with potential increases toward 2.75% to 3.25% by 2027, meaning mortgage rates Canada 2026 will likely rise rather than fall. A 5-year fixed at 4.52% average or the lowest insured rates at 3.99% protect your payment stability against that trajectory.

Start by calculating your renewal or refinancing date and marking the Bank of Canada’s April 29 decision on your calendar. If you renew within six months, lock in now rather than gamble on declines that forecasters don’t expect. If you’re renewing in 2027, a 2 or 3-year fixed term at 4.58% to 4.62% keeps you flexible while avoiding the trap of locking into five years at today’s rates. Contact at least three mortgage brokers and four banks directly because the difference between the lowest and average rates equals $200 to $300 annually on a $520,000 mortgage.

Monitor the spread between short-term and long-term rates quarterly because it signals what lenders expect about future inflation and growth. Track unemployment and wage growth data from Statistics Canada because labour weakness eases rate-hike pressure while wage acceleration complicates the inflation picture. These signals guide your timing far better than headlines about single-day rate moves, and we at Financial Canadian help you build a strong financial strategy through professional mortgage guidance tailored to your situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment