Finding the right online loan in Canada means comparing rates, terms, and lender reliability. The options range from personal loans to payday advances, each with different costs and repayment schedules.

At Financial Canadian, we’ve created this online loans Canada guide to help you evaluate your choices side by side. You’ll learn what to look for and how to apply with confidence.

What Types of Online Loans Can You Actually Get

Personal Loans for Most Borrowing Needs

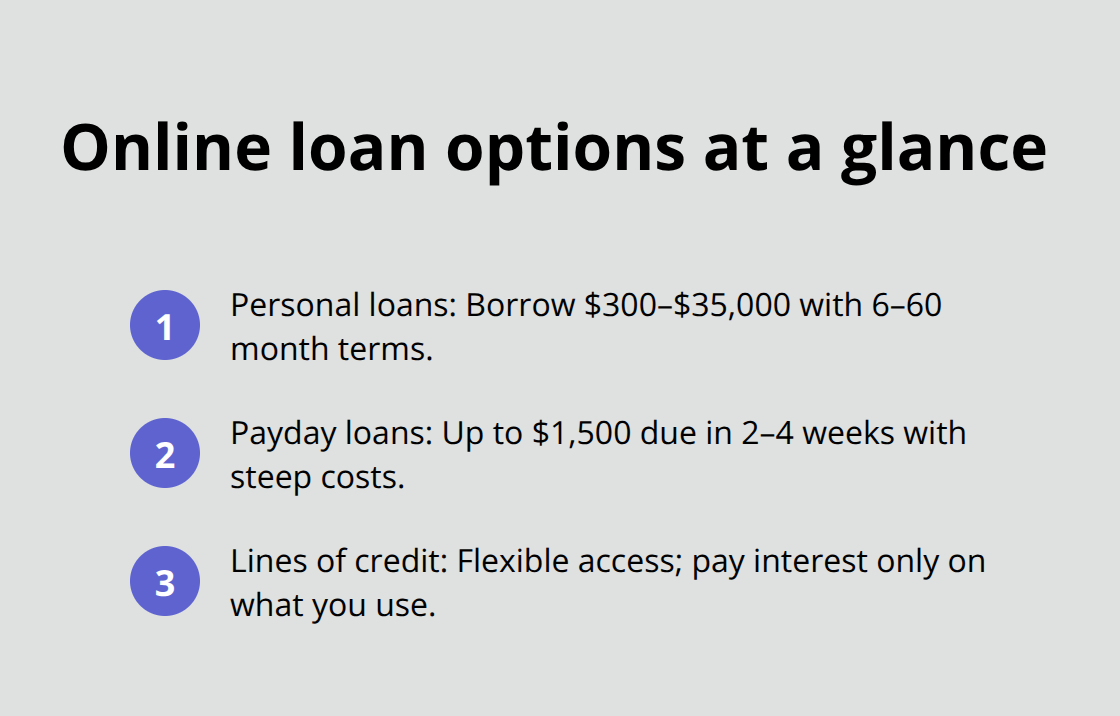

Personal loans top the list for most borrowers seeking online financing in Canada. These unsecured loans range from $300 to $35,000 and come with terms stretching from 6 to 60 months. You can use the funds for debt consolidation, home renovations, moving expenses, weddings, or emergency repairs without explaining your purpose to the lender.

Interest rates for personal loans vary significantly based on your credit profile. Major banks like TD, RBC, and Scotiabank typically offer rates between 6% and 10% APR for well-qualified borrowers, while online lenders like Borrowell and LoanConnect can match or occasionally beat these rates. If your credit sits below 620, expect rates climbing into the 15% to 40% range through online lenders.

The real cost difference emerges when you factor in origination fees, which range from 0.5% to 8% of your loan amount. A $5,000 personal loan at 10% APR over 12 months costs roughly $1,054.99 total-manageable if you need the cash quickly.

Payday Loans: Speed at a High Price

Payday loans occupy the opposite end of the speed-versus-cost spectrum. These short-term loans cap out at $1,500 and come due by your next pay period, typically within 2 to 4 weeks. The convenience comes at a steep price: interest rates often hit 30% APR or higher, making a $500 payday loan cost you $550 to $600 by repayment. We recommend treating payday loans as a genuine last resort, only when you face an immediate crisis and have exhausted every other option.

Lines of Credit and Flexible Access

Lines of credit offer a middle ground that many borrowers overlook. Unlike personal loans where you receive a lump sum, a line of credit gives you ongoing access to funds up to a set limit, and you only pay interest on what you actually borrow. This structure works well for people facing uncertain financial needs or those who prefer flexibility over fixed payments.

Online lenders increasingly offer these products with approval timelines of 24 to 48 hours, compared to the traditional 5 to 10 business days through banks. Your approval speed depends heavily on your credit score and income verification.

How Lenders Assess Your Application

Lenders pull your credit report from Equifax Canada or TransUnion Canada to assess risk, so checking your own credit score before applying helps you target lenders matching your profile. If you spot errors on your report-and roughly 1 in 5 Canadians do-dispute them immediately through the credit bureau’s website. This single step can lower your quoted rate by 2% to 4%.

The application process itself has simplified dramatically. Most online lenders now require just your government-issued ID, proof of residency, recent pay stubs or tax returns, and consent for a credit check. Pre-qualification tools let you see potential rates without a hard credit pull damaging your score. This means you can shop across Borrowell, LoanConnect, Fairstone, and traditional banks simultaneously to compare actual offers before committing to anything.

Now that you understand what loan types exist and how lenders evaluate your profile, the next step involves comparing the specific factors that separate a good deal from a costly mistake.

What Actually Matters When Comparing Online Loans

Understanding APR vs. Interest Rates

APR tells the full story that interest rates alone hide. When lenders advertise a 10% rate, they’re often omitting origination fees that push the actual cost much higher. The Annual Percentage Rate includes both interest and fees, so comparing APRs across Borrowell, LoanConnect, TD Bank, and Fairstone gives you an honest picture of total borrowing cost. A $5,000 loan at 10% APR over 12 months costs $1,054.99 total, while the same loan at 20% APR costs $1,111.61-that extra $56.62 compounds quickly across longer terms. Major banks typically quote 6% to 10% APR for borrowers with good credit, while online lenders range from 9.90% up to 46.96% depending on your profile. Online lenders often publish their full APR range upfront, which beats the vague “rates as low as” language banks use.

Checking Your Credit Score First

Pull your credit score from Equifax Canada or TransUnion Canada before shopping; lenders use these scores to determine your exact rate, and a score above 620 unlocks significantly better pricing across all platforms. If you spot errors on your report-and roughly 1 in 5 Canadians do-dispute them immediately through the credit bureau’s website. This single step can lower your quoted rate by 2% to 4%.

Evaluating Repayment Terms and Flexibility

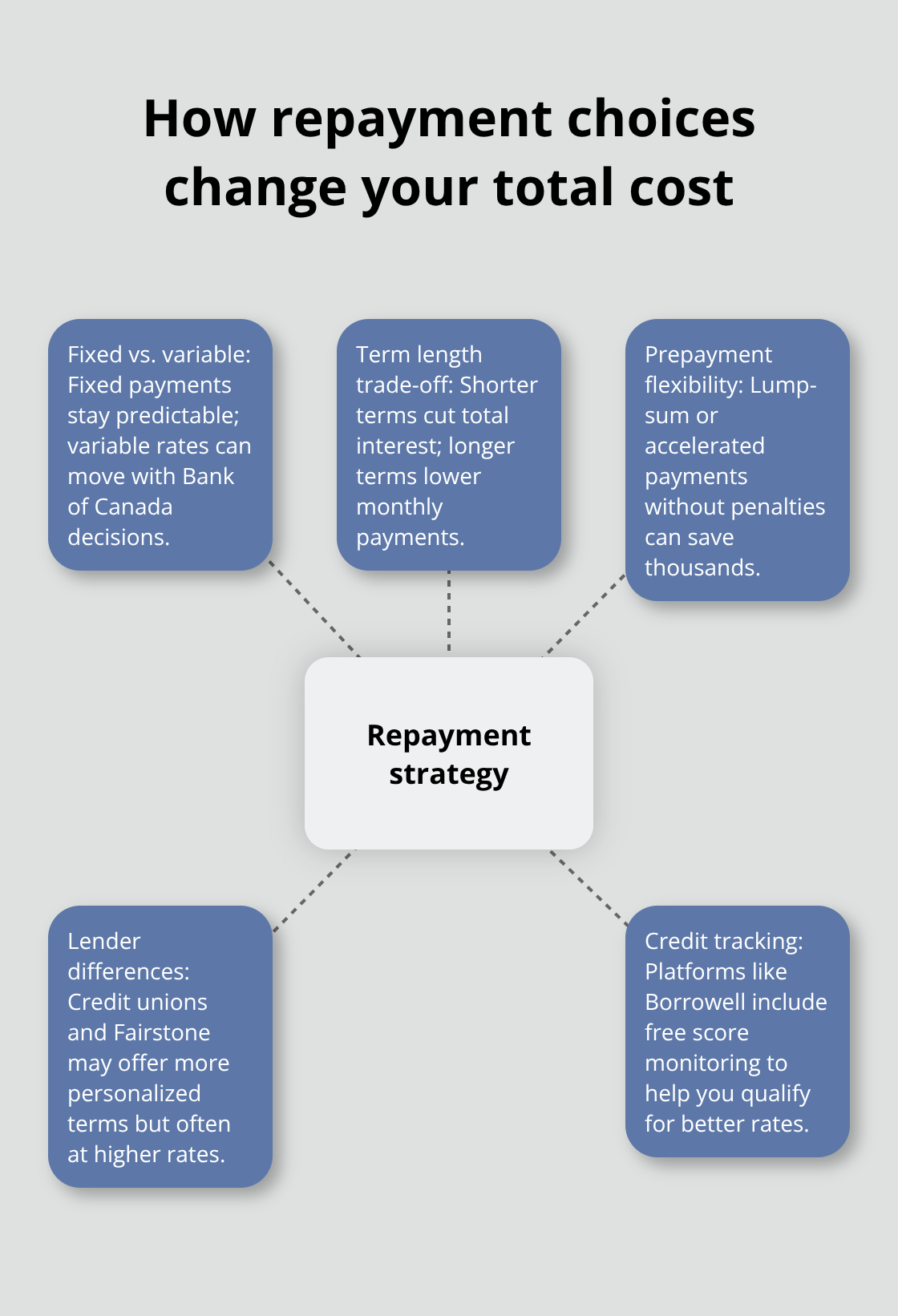

Repayment flexibility matters more than most borrowers realize, and it directly impacts how much interest you’ll ultimately pay. Fixed-rate loans lock in predictable monthly payments, while variable-rate loans tied to prime move with Bank of Canada decisions (though the March 2026 rate pause means variable loans won’t shift immediately). Loan terms stretch from 6 to 60 months, and this choice creates a real trade-off: a 12-month term on $5,000 costs less total interest than a 36-month term, but your monthly payment jumps substantially.

Always ask whether the lender allows lump-sum payments or accelerated payments without penalties; this flexibility lets you save thousands in interest if your financial situation improves. Fairstone and credit unions often carry higher rates but offer more personalized terms, while Borrowell’s platform includes free credit score monitoring that helps you track progress toward better rates.

Assessing Lender Reputation and Legitimacy

Lender reputation comes down to speed, transparency, and whether they actually deliver what they promise. Reddit discussions consistently highlight TD Bank and RBC for established credibility and branch access, though personal loan rates still require comparison. Online platforms like LoanConnect excel at showing you multiple offers without triggering hard credit pulls, letting you evaluate five different lenders in minutes. Avoid any lender guaranteeing approval regardless of credit or requesting upfront fees before funding-these are hallmarks of predatory operations. Check provincial licensing through your financial regulator and verify contact information; legitimate lenders publish clear terms and don’t use high-pressure sales tactics.

Moving Forward with Your Comparison

With these comparison factors in mind, you’re ready to move through the actual application process. The next section walks you through gathering the right documents, submitting your information, and securing funding from the lender that best matches your needs and financial situation.

Getting Your Online Loan Approved and Funded

Prepare Your Documents and Credit Profile

Pull your credit report from Equifax Canada or TransUnion Canada at least a week before applying anywhere. This gives you time to dispute errors if you find them-roughly 1 in 5 Canadians spot inaccuracies on their reports. Disputing errors takes 10 to 15 minutes online through the credit bureau’s website, and it can lower your quoted rate by 2% to 4% once resolved. Next, gather your government-issued photo ID, proof of residency (utility bill or lease agreement works), and recent pay stubs or tax returns showing your income. Most online lenders require these documents uploaded during application, and having them ready speeds up the entire process from hours to minutes.

Calculate Your Debt-to-Income Ratio

Lenders assess your debt-to-income ratio heavily, so calculate yours before applying. Divide your total monthly debt payments by your gross monthly income to get this figure. Generally speaking, you need a GDS between 32% and 39% to get a loan, but your bank may require a lower ratio. This threshold varies by lender, so check specific requirements before submitting your application.

Use Pre-Qualification Tools to Compare Offers

Once your documents are prepared and your credit score checked, use pre-qualification tools on Borrowell, LoanConnect, and your bank’s website simultaneously. Pre-qualification triggers only a soft credit pull, meaning your score stays intact while you see actual rates you’d qualify for. This step matters enormously because advertised rates mean nothing if you don’t qualify for them. Spend 20 to 30 minutes collecting five to seven pre-qualification offers, then compare the APRs side by side in a spreadsheet. Focus exclusively on APR, which includes all fees-ignore the interest rate alone. A $5,000 loan at 10% APR costs $1,054.99 over 12 months, while 20% APR costs $1,111.61 total. That $56.62 difference grows substantially on larger amounts or longer terms.

Complete Your Application and Review Terms

Once you’ve selected your preferred lender, complete the full application within 24 hours while your pre-qualification is still fresh. Most online lenders fund within 1 to 2 business days via e-Transfer or direct deposit, though some promise same-day funding if you apply before 2 p.m. Read the loan agreement’s fine print before signing, specifically checking for prepayment penalties, late fees, and origination fees. Many lenders now allow lump-sum payments without penalties, which means if your financial situation improves mid-term, you can eliminate the loan early and save thousands in interest. Fairstone and credit unions often charge prepayment penalties, so verify this detail before committing.

Manage Your Loan After Funding

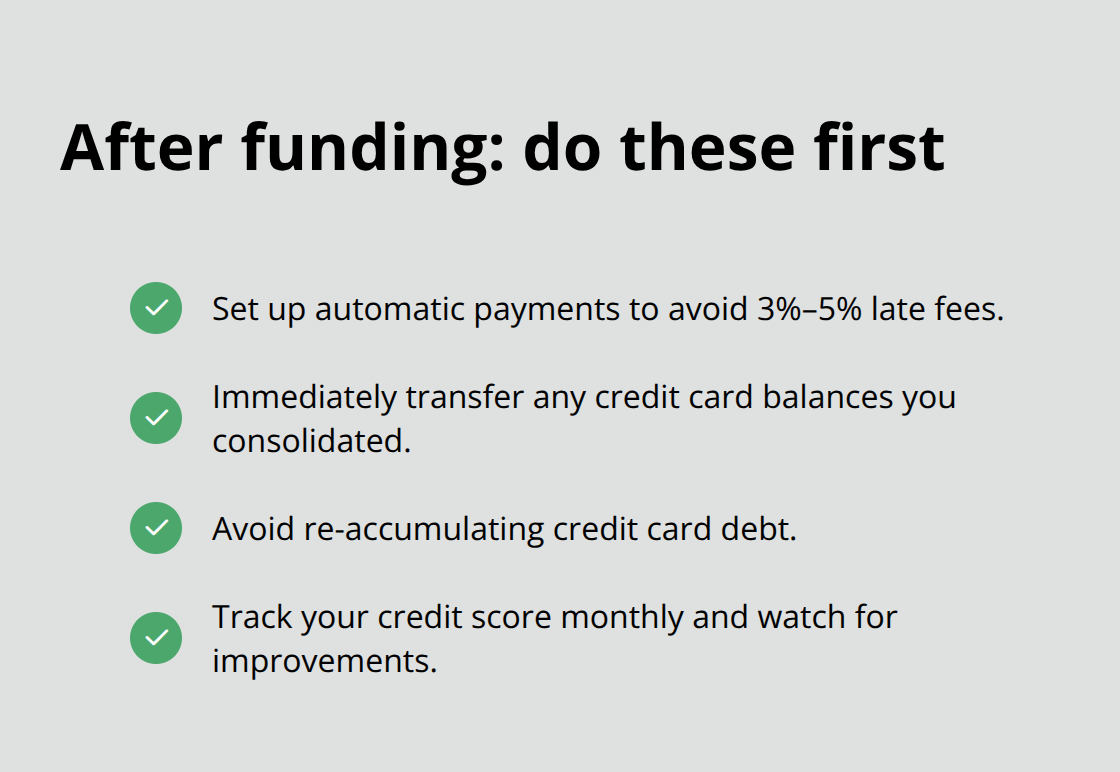

After funding hits your account, set up automatic payments matching your loan term to avoid missed payments, which trigger 3% to 5% late fees and damage your credit score. If you took a consolidation loan to pay off credit card debt, transfer that balance immediately rather than carrying both the new loan and old balances simultaneously. This approach eliminates the temptation to re-rack up credit card debt, which derails consolidation strategies entirely. Track your progress monthly by checking your credit score through free tools; as your loan balance drops, your score typically rises, positioning you for better rates on future borrowing.

Final Thoughts

Online loans in Canada serve different financial situations, and the right choice depends on your timeline, credit profile, and total borrowing cost. Personal loans work best for most borrowers seeking amounts between $300 and $35,000 with manageable terms, while payday loans exist for genuine emergencies only given their 30%+ APR costs. Lines of credit offer flexibility when your needs remain uncertain, and this online loans Canada guide emphasizes that comparing APR across multiple lenders-rather than fixating on advertised rates alone-reveals the true cost including all fees.

Your credit score determines everything in this process. Pull your report from Equifax Canada or TransUnion Canada before applying so you can dispute errors that could inflate your rate by 2% to 4%, and a score above 620 unlocks substantially better pricing across banks, online platforms, and credit unions. Pre-qualification tools from Borrowell, LoanConnect, and traditional banks show you actual offers without damaging your credit, so use them to compare five to seven options simultaneously and identify the best rate available to you.

The application itself takes minutes once your documents are ready, with government-issued ID, proof of residency, and recent pay stubs as standard requirements. Most online lenders fund within 1 to 2 business days via e-Transfer or direct deposit, and after funding arrives you should set up automatic payments immediately to avoid missed payments and re-accumulating debt. Shopping around saves thousands-major banks offer 6% to 10% APR for qualified borrowers while online lenders range from 9.90% to 46.96% depending on your profile, so spend 30 minutes comparing offers rather than accepting the first rate you see. Visit Financial Canadian to explore more resources on loans and personal finance strategies tailored to your situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment