You need fast cash, but you also need protection. That’s the reality of getting online loans approval in Canada-lenders can move quickly without bypassing the rules that keep you safe.

At Financial Canadian, we’ve seen borrowers waste weeks on applications that could’ve been approved in days. The difference comes down to strategy, not luck.

How Fast Can Online Loans Actually Get Approved in Canada

Instant approval sounds like marketing hype, but it’s partially real. Most online lenders in Canada deliver a decision within minutes, not hours or days. A $5,000 loan receives approval in under 10 minutes if you apply during business hours with documents ready. However, approval and funding are two different things. Approval means the lender has said yes; funding means money in your account. That gap matters. After approval, identity verification typically takes 10 minutes to a few hours, then your bank processes the deposit. Same-day funding happens, but next-business-day funding is more realistic.

Speed Varies by Lender Type

Payday lenders move fastest because they check less. They verify income, run a credit check, and confirm your banking information. That entire process takes 15 to 30 minutes. You see the offer immediately. Personal loan lenders like Fig take longer because they are more thorough. Fig shows you a rate offer in seconds without a hard credit pull, but once you consent to a full application, they perform deeper checks. Fig can fund as early as one business day, but their process involves more underwriting than payday options. The speed difference comes down to what lenders verify. Payday lenders focus on whether you have income and a bank account. Personal loan lenders assess your credit history, debt-to-income ratio, and repayment capacity. That’s why payday approvals feel instant while personal loans feel slower, even though both can complete in hours.

What Actually Slows Your Application Down

Your documents represent the biggest speed factor. Missing pay stubs, outdated ID, or unclear bank statements force lenders to request more information, adding days to your timeline. Apply during business hours, keep documents digital and ready, and choose lenders that use digital ID verification. Weekends and after-hours applications sit in queue until Monday morning. Your credit profile also matters. A clean banking history with regular deposits and few overdrafts speeds approval. Irregular deposits, frequent NSF fees, or gaps in employment history trigger manual review. Lenders that use algorithms can approve you in minutes if your financial pattern matches their risk model. One rejection within 30 days can disqualify you from certain lenders, forcing you to apply elsewhere and restart the clock. Income verification is where delays happen. Self-employed applicants need 2 years of tax returns; T4 employees just need recent pay stubs. Government-funded income sometimes gets excluded or requires additional proof. High loan amounts relative to your income invite deeper scrutiny than smaller requests.

Getting Funded Fastest

Direct deposit beats e-transfer for speed. Banks process direct deposits overnight, while e-transfers sometimes take hours. Apply with the bank where you receive your paycheck to eliminate transfer delays. Lenders that partner with multiple banks move faster than those that use a single processor. Check the lender’s stated deposit timeline before you apply. If they promise same-day funding, confirm whether that applies to business days only or includes weekends. Most don’t fund on weekends despite what their marketing suggests. Payday lenders typically deliver within 15 minutes to a few hours. Personal lenders like Fig take one business day minimum. Online platforms that match you to multiple lenders can slow things down because each lender has its own timeline, but they increase your approval odds if one lender declines.

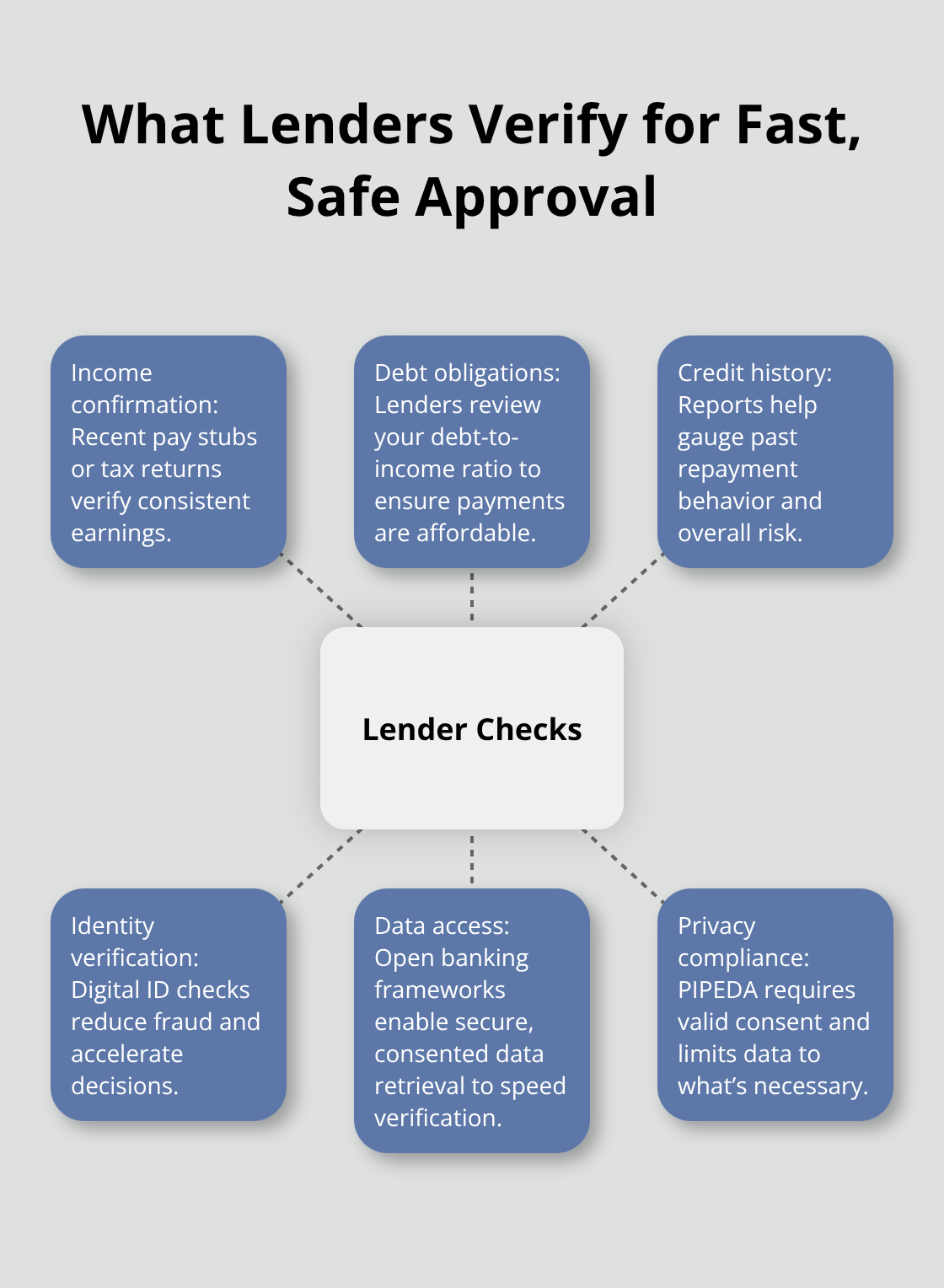

What Lenders Actually Check Before They Say Yes

Canadian financial rules require lenders to verify that you can repay what you borrow. This verification process-not bureaucratic red tape-is what separates fast approval from reckless lending. Lenders must confirm your income, assess your debt obligations, and check your credit history. These checks protect you from taking on debt you can’t handle.

The Consumer-Driven Banking Act created a framework for safe data sharing between consumers and fintech apps, which actually speeds up verification. Lenders can now access your financial data more efficiently while maintaining strict privacy standards under PIPEDA. This means faster approvals without cutting corners on consumer protection. Payday lenders perform lighter checks because their loans are smaller and shorter-term. Personal loan lenders dig deeper because they’re committing more capital over longer periods. Neither approach is wrong-they’re just calibrated to different risk levels. Understanding what lenders check helps you prepare documents that move your application forward instead of holding it back.

Why Regulation Enables Fast Approvals

Canadian financial rules don’t slow down online loans-they actually enable faster approvals by creating standardized verification processes that lenders can automate. When the Consumer-Driven Banking Act took effect, it created a framework for safe data sharing between consumers and fintech apps. Lenders can now access your financial information directly from your bank instead of requesting documents manually, which speeds up verification dramatically. The Financial Consumer Agency of Canada oversees compliance with these requirements, ensuring that lenders follow consistent standards across the country. This consistency allows algorithms to work effectively. A lender using automated checks can approve you in minutes because the system knows exactly what data to verify and in what format. Without regulation, lenders would each create their own verification process, which would be slower and less reliable.

How Licensing Creates Speed Through Standardization

Payday lenders in provinces like Ontario, British Columbia, Alberta, and Manitoba operate under specific licensing requirements (Ontario lender 4721539, BC lender 52546, Alberta lender 342618, and Manitoba lender 67816). These licenses exist precisely because regulators want to protect borrowers while allowing fast lending to continue. The trade-off isn’t between speed and safety-it’s between speed and fraud. Thorough vetting catches applicants who lie about income or hide debts, which protects both you and the lender. Lenders must verify your income, assess your debt-to-income ratio, and confirm your credit history before approving you. These checks take time, but they’re the reason you won’t end up borrowing more than you can repay.

How the Interest Rate Cap Changed Lending Standards

The criminal interest rate cap Canada changed on January 1, 2025, dropping to 35% APR. This shift forced lenders to adjust pricing and tighten their underwriting standards. The regulatory change actually improved approval quality because lenders can no longer rely on extremely high rates to cover risky approvals. Instead, they focus on lending to people who genuinely can repay. When a lender offers rates starting at 8.99% for personal loans up to $35,000 with terms of 24 to 84 months, that’s possible because their underwriting is thorough enough to approve lower-risk borrowers at lower costs. Payday lenders charging 365% APR in Ontario for a $500 loan over 14 days operate within legal limits, but that cost structure only works for short-term borrowers with stable income who can repay quickly. Regulation doesn’t prevent either model-it just requires transparency and prevents predatory practices.

What Disclosure Requirements Mean for You

When you apply, lenders must disclose the full cost of borrowing including APR and all fees upfront. This disclosure requirement means you can compare offers accurately before committing. Self-employed applicants face longer approval times because regulators require two years of tax returns as proof of income stability, while T4 employees just need recent pay stubs. This difference isn’t bureaucratic burden-it’s risk management. A self-employed income can fluctuate significantly, so deeper verification protects you from overextending.

How Privacy Rules Actually Speed Things Up

Under PIPEDA, lenders must obtain valid consent before accessing your data and must limit collection to what’s necessary. This privacy requirement actually speeds approval because you consent once and lenders access verified information directly rather than requesting documents repeatedly. The standardized data-sharing framework means lenders know exactly which financial details they can access and in what format, eliminating back-and-forth requests that waste time. Your next move determines whether you’ll actually qualify for the fastest approvals available-and that depends on how well you prepare your application before you submit it.

How to Prepare Your Application for Instant Approval

The fastest approvals go to applicants who arrive prepared. Lenders make decisions in minutes when your documents are organized, your information is accurate, and your profile matches their lending criteria.

Check Your Credit Score First

Start with your credit score before you apply. Knowing whether you fall into the poor, fair, good, or excellent range tells you which lenders will actually approve you quickly. If your score sits below 650, payday lenders will move faster than personal loan providers. If your score exceeds 700, personal lenders like Fig become viable and often offer better rates. A 2021 Loans Canada survey of 3,480 online loan applicants found that 52.6% had low credit scores, yet 71.4% received at least one approval. The difference between those approved and rejected came down to matching the right lender to their profile.

Apply to lenders that accept your credit tier, not lenders that market to everyone. This single decision cuts approval time from days to hours because you’re not fighting against their lending standards.

Organize Your Documents in Advance

Lenders require proof of income, valid ID, recent bank statements showing regular deposits, and proof of residence. Self-employed applicants need at least two years of tax returns, while T4 employees just need the most recent pay stub and notice of assessment. Have these files digital and ready on your phone or computer. When a lender requests verification, you respond within minutes instead of spending hours searching for documents. The Loans Canada survey showed that incomplete applications and missing documents were primary reasons applications stalled.

If you work irregular hours or receive government income, prepare additional documentation upfront. Some lenders exclude government-funded income or require extra verification steps, so confirming this before applying prevents rejection after you’ve already submitted.

Time Your Application Strategically

Apply during business hours on a weekday. Your application enters the processing queue immediately instead of sitting until Monday morning. Direct deposit to the bank where you receive your paycheck eliminates transfer delays during funding. Most online lenders process direct deposits overnight, while e-transfers sometimes take hours. This choice alone can mean same-day funding versus next-business-day funding.

Final Thoughts

Online loans approval in Canada works fast because regulation creates standardized processes, not because rules are bypassed. The Consumer-Driven Banking Act, the criminal interest rate cap at 35% APR, and provincial licensing requirements all enable lenders to verify your information quickly while protecting you from predatory practices. Your approval timeline depends entirely on preparation-applicants who arrive with organized documents, accurate information, and realistic expectations receive approval in hours.

Speed without sacrificing rules means understanding your rights and responsibilities as a borrower. You have the right to transparent disclosure of all costs, the right to privacy protection under PIPEDA, and the right to fair treatment under provincial lending laws. You also have the responsibility to provide accurate information, to borrow only what you can repay, and to understand the total cost of borrowing before you commit. A $500 payday loan costing $70 in interest over 14 days in Ontario carries a 365% APR-that’s legal and disclosed, but it’s expensive.

The fastest online loans approval Canada offers comes from matching yourself to the right lender, preparing thoroughly, and respecting the regulatory framework that protects you. Check your credit score first, gather your documents before applying, and choose lenders that actually accept your financial profile. We at Financial Canadian offer comprehensive web design services with responsive layouts, SEO optimization, and user-friendly navigation to establish your strong online footprint.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment