Most Canadians leave money on the table with their credit cards. We at Financial Canadian believe you shouldn’t have to choose between earning rewards and paying excessive fees.

When you compare credit cards in Canada, the difference between a mediocre card and the right one can mean hundreds of dollars annually. This guide shows you exactly how to pick cards that match your spending, stack rewards, and dodge fees that eat into your gains.

What Credit Card Type Matches Your Spending?

Cash Back Cards: Immediate, Predictable Returns

Cash back cards dominate Canada’s market for one reason-they deliver immediate value. The Tangerine Money-Back World Mastercard gives you 2% cash back in up to three categories you choose from ten options, plus 0.5% on everything else, with no annual fee. The CIBC Dividend Visa Infinite delivers 4% cash back on groceries and gas with a $120 annual fee, but only if your household income hits $60,000. The Scotiabank Momentum Visa Infinite matches that 4% on groceries and varies between 1% and 4% on other purchases, also charging $120 annually with a first-year waiver. These cards pay you immediately-cash lands in your account or reduces your balance. You know exactly what you earn with no guesswork about redemption value.

Travel Rewards Cards: Flexibility and Higher Ceilings

Travel rewards cards operate on a different principle. The TD Aeroplan Visa Infinite earns roughly 1x to 1.5x Aeroplan points on everyday purchases, waives the annual fee in year one, and offers up to 40,000 welcome points plus free checked baggage on Air Canada flights. The American Express Aeroplan Reserve Card pushes harder with 60,000+ sign-up points, 1:1 transfers to airline partners, and lounge access through a $599 annual fee. Points don’t expire as long as your account stays active, and you can transfer them to airline and hotel partners at a 1:1 ratio through Aeroplan’s network, which includes Air Canada and Star Alliance members.

Calculating Real Value: Cash Back vs. Travel Points

The real difference emerges when you calculate actual value. Cash back is predictable-you know exactly what you earn. Travel rewards often deliver more value if you book strategically. Aeroplan points typically hold roughly 1 cent of value each, though booking during off-peak travel windows can push that to 1.5 cents or higher. If you spend $3,000 annually on groceries with a 4% cash back card, you pocket $120 before the annual fee. With a travel card earning 1.5x points on that same $3,000, you’d accumulate 4,500 points worth roughly $45 in value. Cash back wins for everyday essentials.

However, if you’re chasing a $500 flight that normally costs $800, and your travel card’s sign-up bonus delivers 60,000 points, you could redeem for that flight plus additional travel. The American Express Cobalt Card suits heavy dining and streaming spenders with 5x points on restaurants and delivery, 3x on streaming, and 2x on transit and gas, carrying a $191.88 annual fee. The SimplyCash Preferred from American Express gives 2% cash back on all purchases and 4% on groceries and gas for $119.88 yearly.

Match Your Card to Your Actual Spending Habits

Your spending pattern determines which structure wins. Frequent travelers who book through airline portals should prioritize travel cards. Regular grocers and gas buyers without travel plans should stick with cash back. The worst mistake is holding a premium travel card while earning flat-rate cash back rewards-you’re paying annual fees for benefits you don’t use. Once you identify which card type aligns with your lifestyle, the next step involves a more sophisticated strategy: combining multiple cards to capture rewards across all your spending categories.

How to Stack Cards and Time Bonuses for Maximum Rewards

The One-Card Trap Costs You Thousands

The single biggest mistake Canadians make is holding one card for all spending. You leave thousands of dollars on the table if you use a flat-rate card for groceries when a 4% grocery card exists, or a non-travel card while chasing flights. The math is straightforward: if you spend $8,000 annually on groceries and gas combined, a 4% card nets you $320 before fees. A 1.5x travel rewards card on the same spend delivers roughly $120 in value. That $200 gap compounds yearly, and it is entirely preventable.

A deliberate two or three-card strategy tailored to your actual spending breakdown outperforms any single premium card. Track your spending across six months to identify your top three categories. Most Canadians cluster heavily into groceries, gas, dining, and travel bookings. Once you know your pattern, assign cards strategically.

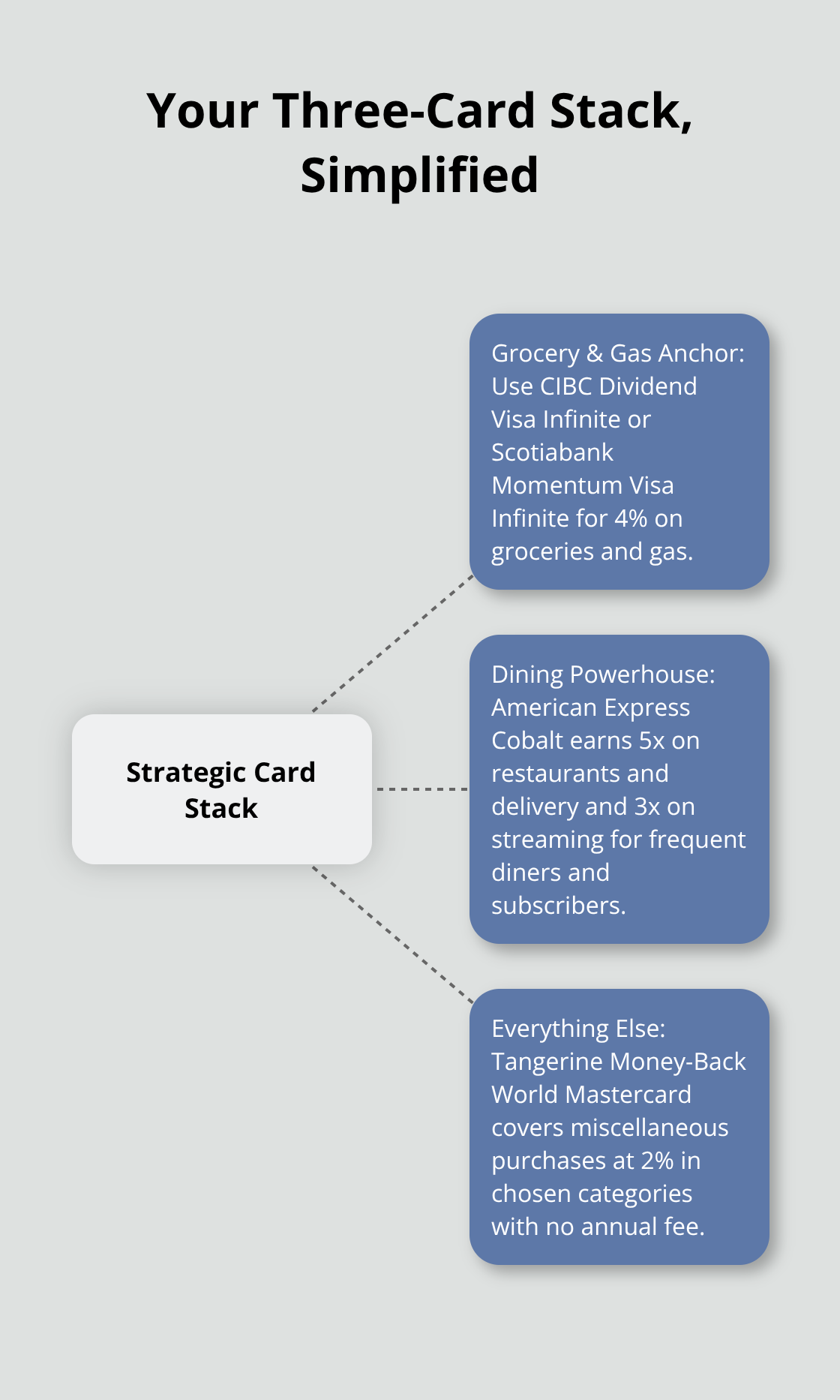

Building Your Strategic Card Stack

The CIBC Dividend Visa Infinite or Scotiabank Momentum Visa Infinite captures your 4% grocery and gas spending. The American Express Cobalt Card, which delivers 5x points on restaurants and delivery plus 3x on streaming, absorbs your dining category. For everything else, the Tangerine Money-Back World Mastercard with its 2% chosen categories covers miscellaneous purchases at no annual cost.

This three-card stack costs you roughly $240 yearly in fees but generates substantially more rewards than any single premium card. The key is ruthless category alignment: do not pay annual fees for benefits in categories where you spend little. If you dine out twice monthly, the Cobalt’s $191.88 fee does not justify itself unless you also use its streaming and transit bonuses heavily. Ratehub data shows that matching cards to your top spending categories delivers 30–50% more rewards than using a generalist card.

Activating Sign-Up Bonuses Without Overpaying Fees

Sign-up bonuses amplify this strategy considerably. The American Express Aeroplan Reserve Card offers 60,000+ welcome points after initial spend, equivalent to roughly $600–$900 in travel value depending on redemption timing and peak versus off-peak booking windows. Do not chase bonuses randomly.

Activate one new card every 3–4 months, meet its minimum spend requirement deliberately through planned purchases or bill consolidation, then shift to the next card. This prevents annual fee stacking on cards you have exhausted. The MBNA True Line Mastercard, which offers 0% balance transfers for 12 months with a 3% fee and no annual fee, works perfectly for this rotation. Consolidate a balance onto it during your application window, then switch to your rewards cards once the promotional period ends.

Timing Redemptions and Capped Earning Categories

Timing matters enormously. Book travel during off-peak windows to stretch point value. Aeroplan points hold value depending on when you book and redeem. A 60,000-point bonus redeems for a $600 flight in peak summer but covers $900 in March or September.

Activate bonus categories on quarterly-capped cards strategically. The Scotiabank Momentum Visa Infinite caps its 4% earning at $25,000 annual spending, meaning you hit that ceiling after $625 monthly spending. If you spend $800 monthly on groceries, that extra $200 earns only 1%, wasting potential. Supplement with Tangerine’s 2% chosen categories or SimplyCash’s consistent 4% on groceries to capture that overflow.

Maintaining Your System and Avoiding Costly Mistakes

This layering approach requires minimal effort once set up. Assign each card to one spending category, use it exclusively for that category, and automate payments to avoid interest charges that obliterate rewards value. One missed payment at 21% APR erases years of accumulated rewards gains.

Keep cards active by using them quarterly minimum; Aeroplan points and most rewards do not expire as long as your account remains open, but dormant accounts risk closure. A household spending $50,000 annually across groceries, dining, gas, and travel can realistically earn $1,000–$1,500 more in rewards value annually through strategic card stacking compared to using a single card, even after accounting for annual fees totaling $300–$400.

The rewards gains from stacking cards are substantial, but only if you avoid the fees that undermine them. Understanding which fees actually matter-and which ones you can eliminate entirely-separates strategic card users from those who accidentally pay their way to mediocre returns.

Common Credit Card Fees and How to Avoid Them

Annual Fees: Calculate Before You Apply

Annual fees dominate Canadian credit card discussions, but most people focus on the wrong ones. A $120 annual fee on a grocery card that delivers 4% cash back on $8,000 yearly grocery spending generates $320 in rewards, netting you $200 after the fee. That same $120 fee on a travel card you barely use becomes pure waste. The real question isn’t whether a fee exists-it’s whether the card’s earning structure covers it through your actual spending. Ratehub data shows the CIBC Dividend Visa Infinite and Scotiabank Momentum Visa Infinite both charge $120 annually but justify themselves completely if groceries and gas represent your top spending categories. The Scotiabank card even waives the fee in year one, letting you test whether the 4% earning rate on groceries and tiered rates elsewhere generate sufficient rewards.

Conversely, premium cards like the American Express Platinum at roughly $799 annually or the American Express Aeroplan Reserve at $599 only make sense if you redeem significant travel value or actively use lounge access. Calculate this before applying: estimate your annual spending in the card’s top categories, multiply by the earn rate, then subtract the annual fee. If the result is negative, the card costs you money regardless of how attractive the rewards sound.

Interest Charges and Balance Transfers: The Real Wealth Destroyers

Interest charges and balance transfers represent the fees that actually destroy wealth. Carrying a balance at 21% APR erases years of rewards accumulation instantly-one missed payment wipes out roughly $2,000 in accumulated rewards value on a $10,000 balance. Pay your full balance monthly or credit cards become financial traps regardless of rewards structure.

Balance transfers offer legitimate value when used strategically. The MBNA True Line Mastercard provides 0% APR on balance transfers for 12 months with a 3% transfer fee and no annual fee, meaning you pay roughly $300 to move a $10,000 balance and avoid $2,100 in interest charges at standard rates. The CIBC Select Visa extends the promotional window to 10 months with a 1% transfer fee, though the shorter window reduces total interest savings. These options work best when you commit to paying down the balance before the promotional period expires.

Foreign Exchange Fees: The Hidden Cost of International Spending

Foreign exchange fees disappear entirely on no-FX-fee cards, but most Canadian cards charge 2.5% on international purchases. The American Express Cobalt Card and premium Aeroplan cards typically include no foreign transaction fees, making them essential if you spend internationally or travel frequently. A $2,000 international purchase on a standard card costs $50–$60 in hidden FX fees; using a no-fee card eliminates that entirely.

The math proves brutal on this front: someone spending $5,000 annually abroad on a standard-fee card hemorrhages $125–$150 yearly to currency conversion markups alone. This hidden cost compounds faster than most people realize, and it affects every international transaction-from online purchases to restaurant bills while traveling.

Fee Waivers and First-Year Offers

Many premium cards waive annual fees in year one, which shifts the calculation significantly. The Scotiabank Momentum Visa Infinite waives its $120 fee initially, and the TD Aeroplan Visa Infinite does the same. This strategy lets you test whether the card’s earning structure justifies the ongoing fee without committing to a full year of charges. If the card doesn’t deliver sufficient rewards in year one, you can cancel before the fee kicks in.

First-year waivers also apply to premium travel cards. The American Express Aeroplan Reserve and American Express Platinum cards sometimes offer fee reductions or credits in initial periods, though these promotions vary. Check the specific offer terms before applying, as promotional structures change frequently across issuers.

Avoiding the Fee Trap Through Strategic Selection

The cards you choose determine whether fees enhance or undermine your rewards strategy. A $120 annual fee on a card matching your top spending categories represents an investment that pays dividends. That same fee on a card you use sporadically becomes an anchor dragging down your returns. Annual fees on cards-best for groceries and gas, best balance transfer, best no-fee cash back-help you identify which cards justify their fees based on your specific spending patterns. Select cards that align with your actual behavior, not aspirational spending habits, and you’ll find that fees either disappear into strong rewards gains or become immediately obvious as unnecessary costs.

Final Thoughts

The credit card landscape in Canada rewards deliberate choices and punishes passive decisions. Most Canadians earn a fraction of what their spending could generate because they treat credit cards as interchangeable tools rather than strategic assets. When you compare credit cards Canada offers by calculating whether each card’s annual fee and earning rates generate net positive returns based on your actual behavior, you transform how much value you extract from every purchase.

A household spending $50,000 annually can realistically earn $1,000 to $1,500 more through strategic card selection compared to using a single mediocre card. That same household avoids hundreds in interest charges and foreign exchange fees by selecting cards with promotional balance transfer rates and no FX markups. These gains compound year after year, and they require no additional effort once your system is established.

Start today by identifying your top spending categories, then select cards that reward those categories aggressively while keeping annual fees minimal. We at Financial Canadian created this guide to help you navigate the options and build a strategy that aligns your cards with your life. Use our card comparison tools to test different combinations and see exactly how much you could earn with the right approach.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment