When unexpected expenses hit, waiting days for a loan approval isn’t an option. Same day funding in Canada gives you access to cash within hours, not weeks.

At Financial Canadian, we know that financial emergencies don’t follow a schedule. This guide breaks down your fastest options and shows you which solution actually makes sense for your situation.

How Fast Can You Actually Get Same Day Funding

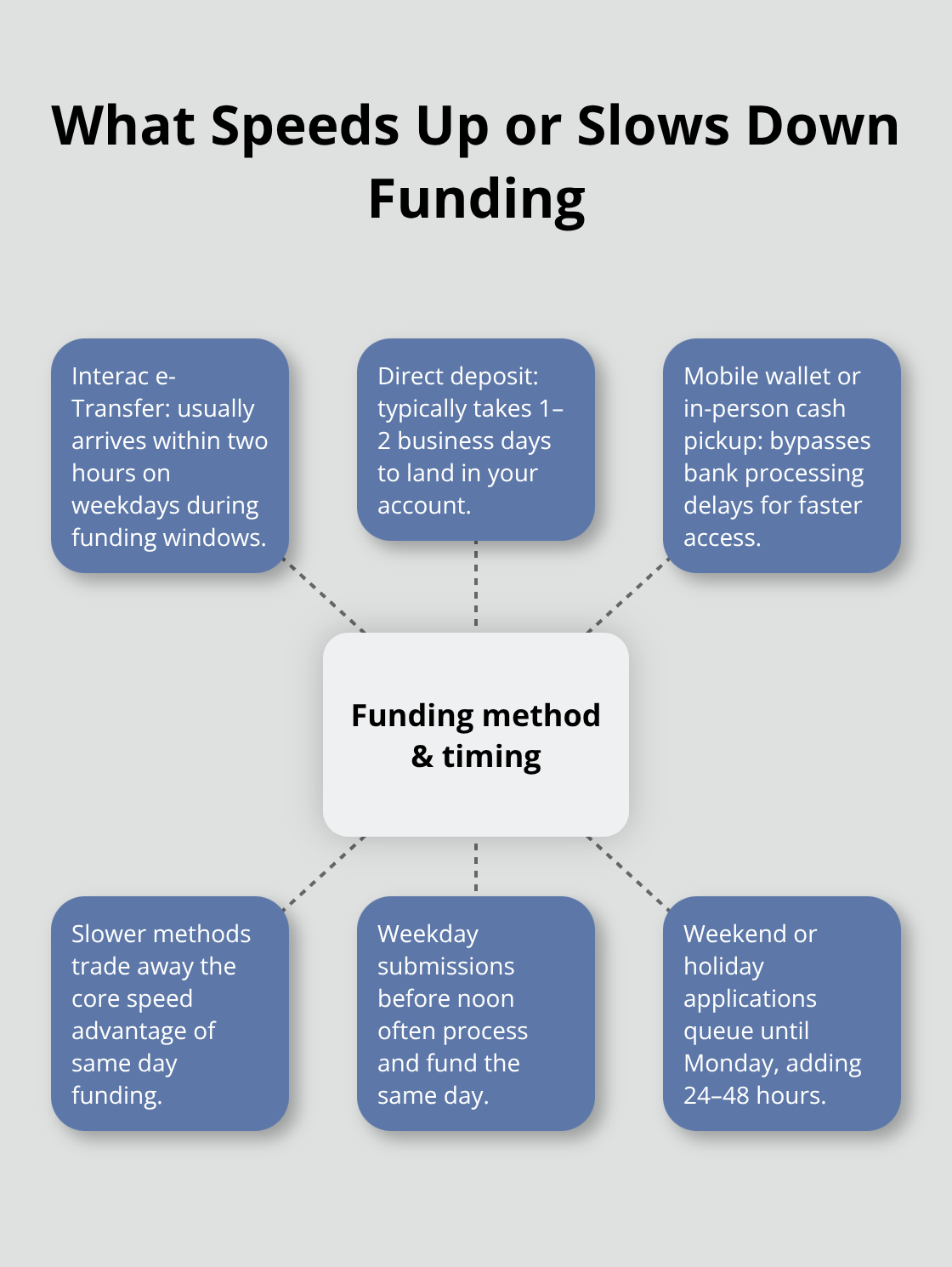

Receiving money within 24 hours of applying is what same day funding means in Canada, though many lenders deliver cash in as little as 15 minutes. The speed depends entirely on your lender choice and funding method. Money Mart, for example, offers funds within 15 minutes for certain payment methods or within 24 hours to 1–2 days depending on how you receive the money. Online Interac e-Transfer typically arrives within two hours on weekdays during funding windows, usually between 6:00 a.m. and 10:00 p.m. ET. The reality is that same day funding isn’t actually same day for most people-it’s next business day funding, which matters if you need cash on a Friday evening.

What happens during the application process

The application itself takes minutes, not hours. Most online lenders complete eligibility checks within minutes and offer 24/7 online account access, meaning you can apply at 2 a.m. on a Sunday if needed. The lender runs a credit check and verifies your income, employment status, and banking details. This is where speed varies dramatically. Some platforms like Money Mart provide quick decisions in minutes with no impact on your credit score during the eligibility check phase. However, the actual loan approval happens after you submit full documentation. If you apply during business hours on a weekday, approval typically happens the same day. Apply on Friday evening or weekend and expect approval Monday morning at best.

Timeline expectations from start to cash

Here’s the practical timeline: application takes 10–15 minutes, eligibility check takes 5–10 minutes, approval decision takes 30 minutes to 2 hours during business hours, and funding delivery takes 15 minutes to 24 hours depending on your bank. Total time from start to cash in your account ranges from 30 minutes to 48 hours in real-world scenarios. If you need cash today and it’s already 3 p.m. on a Friday, you won’t get it today. Apply before noon on a weekday at an online lender and you’ll likely have cash by evening.

The fastest option is payday loans and cash advances, which prioritize speed over everything else. Personal lines of credit take longer because banks conduct more thorough financial reviews. Online alternative lenders fall somewhere in between, typically delivering within 24 hours. Your bank matters too-some financial institutions process incoming transfers faster than others.

Speed varies by funding method

The method you choose to receive your money directly impacts how quickly you access it. Interac e-Transfer arrives fastest (within two hours on weekdays), while direct deposit to your bank account takes 1–2 business days. Some lenders offer mobile wallet transfers or in-person cash pickup, which eliminates bank processing delays entirely. If you select a slower funding method, you sacrifice the speed advantage that same day funding promises. The lender’s operating hours also matter significantly. Weekend and holiday applications sit in a queue until Monday morning, adding 24–48 hours to your timeline.

Weekday applications submitted before noon typically process and fund the same day.

Which lenders actually deliver fastest

Payday lenders and cash advance companies prioritize speed because their entire business model depends on quick turnaround. They approve applications in minutes and fund within hours. Personal lines of credit from traditional banks move slower because underwriters conduct deeper financial analysis. Online alternative lenders (like Money Mart) split the difference-they approve quickly but may take 24 hours to fund depending on your bank’s processing speed. Your credit score affects approval speed too. Applicants with strong credit histories move through underwriting faster than those with poor credit, who may face additional verification steps.

Understanding these timelines helps you choose the right lender for your situation and set realistic expectations about when cash actually arrives in your account.

Your Fastest Same Day Funding Options

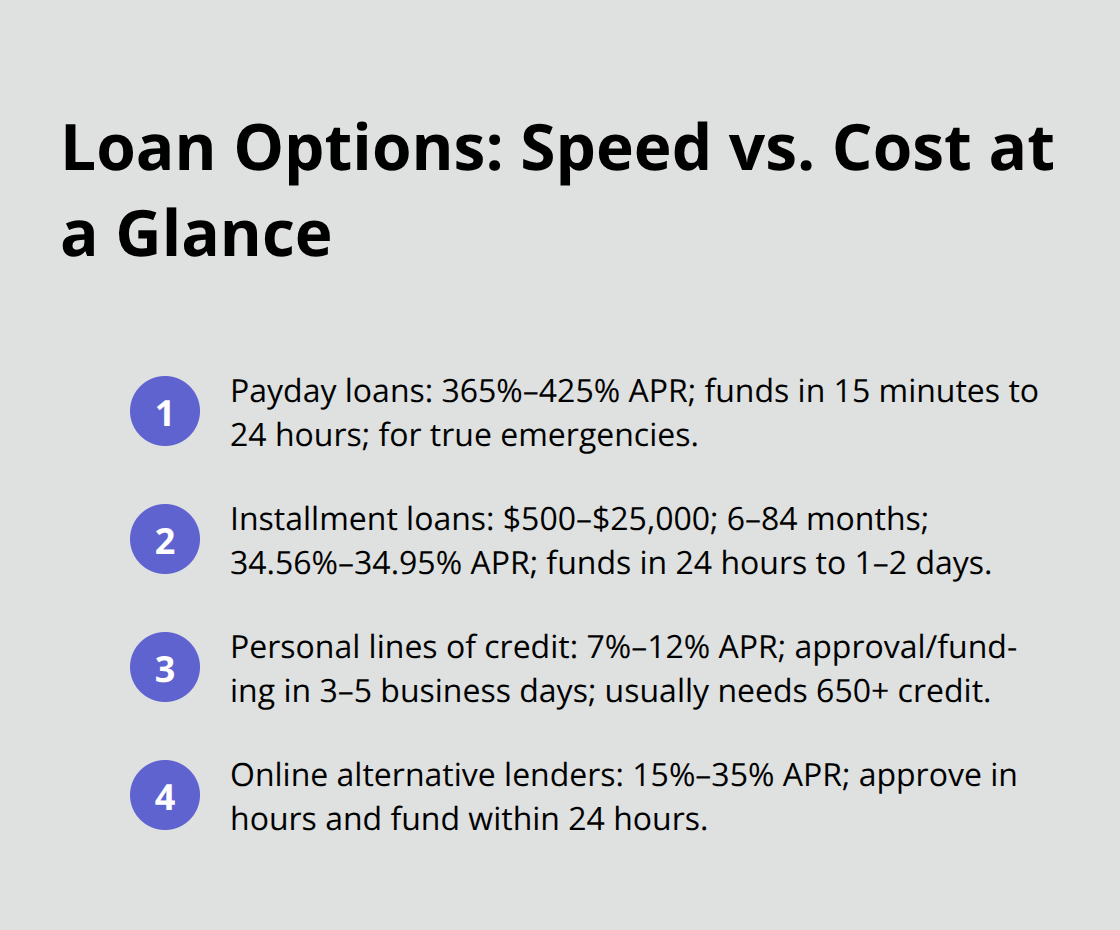

Payday loans and cash advances dominate the speed category because lenders strip away the complexity that slows down traditional financing. Money Mart’s cash advance products deliver funds in as little as 15 minutes for certain payment methods, with online applications processed 24/7 and decisions made within minutes. The trade-off is obvious: payday loans charge between 365% and 425% APR depending on your province. Ontario charges $14 per $100 borrowed over 14 days (365% APR), while Manitoba charges the same fee over 12 days (425.83% APR). A $500 payday loan costs you roughly $70 in fees if you repay within two weeks. These products exist for genuine emergencies, not for covering everyday expenses you could otherwise plan around. If you need $300 today and can repay it in two weeks, a payday loan makes sense. If you need $5,000 and cannot repay it quickly, the interest compounds into a serious financial problem.

Payday advances for immediate cash needs

Money Mart’s Payday Boost offers between $100 and $1,500, with new customers receiving their first $300 interest-free as a promotional offer (subject to change and availability varies by province). This product targets people who face genuine cash shortfalls and can repay within weeks, not months. The speed advantage comes from minimal underwriting-lenders verify your income and banking details but conduct no deep financial analysis. You apply online, receive approval within minutes, and access funds within hours. The high APR reflects the lender’s risk; they accept applicants with poor credit histories that traditional banks reject outright.

Installment loans for larger amounts

Installment loans let you borrow larger amounts with longer repayment terms, which dramatically changes the math. Money Mart’s installment loans range from $500 to $25,000 with repayment periods of 6 to 84 months and APR between 34.56% and 34.95%. A $5,000 installment loan at 46.9% APR costs around $4,399.24 in total interest over the loan term, while a $4,500 loan at 34.95% APR requires approximately $203.42 in monthly payments over 36 months. The speed is slightly slower than payday loans-you’re looking at 24 hours to 1–2 days for funding-but you gain payment flexibility. Installment loans work when you need more than $1,500 and can handle monthly payments. British Columbia and Manitoba classify installment loans as high-cost credit products requiring specific licensing, so verify your province’s regulations before applying. An optional Loan Protection Plan, underwritten by Canadian Premier Life Insurance Company, covers payments during job loss, injury, sickness, or death, adding a safety layer for around $30–50 per month depending on your loan size.

Personal lines of credit for lower costs

Banks and credit unions offer personal lines of credit with APR typically between 7% and 12%, far below payday and installment loan rates. The catch is timing: traditional lenders conduct thorough financial reviews, taking 3–5 business days for approval and funding. This option only works if your emergency can wait until mid-week. Personal lines of credit require stronger credit scores (usually 650+) and employment stability, making them inaccessible for many people facing urgent cash needs.

Online alternative lenders for balance

Online alternative lenders split the difference between speed and cost. They approve applications within hours and fund within 24 hours, with APR ranging from 15% to 35% depending on your creditworthiness. These lenders pull your credit report and verify income through your bank connections, streamlining the underwriting process. If you have moderate credit and need cash within 24 hours, online lenders offer the best balance of speed and affordability. Your choice depends on your timeline and how much you can afford to repay monthly, not on marketing claims about speed. The next section examines the hidden costs that transform what looks like a quick solution into a long-term financial burden.

When Same Day Funding Actually Makes Sense

Real emergencies that justify the cost

Same day funding solves genuine problems during true crises, but the cost structure makes it unsuitable for everyday financial gaps. A burst pipe requiring $2,000 in repairs today justifies a payday loan’s 365% APR because waiting five days means water damage compounds into tens of thousands in property loss. A car breakdown preventing you from reaching your job warrants immediate borrowing because losing income creates a worse crisis than the loan’s interest charges. These situations exist, they happen regularly, and same day funding addresses them directly.

The problem emerges when people use these products for non-emergencies. Taking a $1,500 payday loan to cover a vacation you cannot afford, or borrowing at 34.95% APR to replace a phone you could repair instead, transforms a speed advantage into a financial trap. The genuine benefit of same day funding is access during crises when no other option exists, not convenience when you could plan differently.

Why speed carries such a steep price

The cost structure reveals why speed comes at such a steep price. Payday lenders operating at 365% to 425% APR face regulatory restrictions on how long they can hold your money and what collateral they can demand, so they compensate through astronomical interest rates. A $500 payday loan costs $70 in fees over two weeks, which sounds manageable until you cannot repay it.

Most borrowers roll over their loans, extending the initial two-week term into months of accumulated interest. Payday loan rollovers show that borrowers extend their loans multiple times, transforming a $500 emergency loan into significantly higher interest charges on the same original debt.

Comparing total costs across loan types

Installment loans at 34.95% APR appear reasonable until you calculate the total cost. Online alternative lenders at 15% to 35% APR are dramatically cheaper, but still cost three to five times more than a personal line of credit at 7% to 12% APR.

The speed advantage has a measurable price tag, and you need to decide whether the emergency justifies paying it. A genuine medical emergency does. A purchase you wanted but did not need does not. The distinction determines whether same day funding helps or harms your financial situation over the next twelve months.

Making the right decision for your situation

Your choice depends on whether the emergency would cause greater financial damage if you waited. A job loss requiring immediate living expenses justifies borrowing at high rates. A desire for new furniture does not. Ask yourself whether the crisis would worsen significantly if you waited three to five business days for a cheaper loan option. If the answer is yes, same day funding makes sense. If the answer is no, you should explore lower-cost alternatives instead.

Final Thoughts

Same day funding Canada offers a genuine solution when financial emergencies demand immediate cash, but only when the crisis justifies the cost. The speed advantage comes with a measurable price tag that ranges from 365% APR for payday loans to 34.95% APR for installment loans. Your decision should hinge on one question: will waiting three to five business days for a cheaper loan option cause greater financial damage than paying the premium for speed?

Payday loans and cash advances deliver the fastest access to money, with funds arriving within 15 minutes to 24 hours depending on your funding method. This speed makes sense for genuine emergencies like urgent medical expenses or critical home repairs that worsen without immediate attention. Installment loans provide larger amounts with manageable monthly payments, working well when you need $500 to $25,000 and can handle repayment over months or years.

The critical distinction separates genuine crises from wants disguised as needs. A burst pipe, unexpected job loss, or vehicle breakdown that prevents work justifies borrowing at high rates, while a vacation you cannot afford or new furniture does not. Before applying for same day funding, honestly assess whether the situation would deteriorate significantly if you waited, then compare your options across multiple lenders to find the best APR and repayment terms for your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment